Chapter 1 Industry Overview and Global Landscape

A Seriously Underestimated Segment

In China's equipment manufacturing landscape, mechanical seals have long held an awkward position. They lack the constant media attention given to high-end bearings, the "stranglehold technology" label that drives traffic for hydraulic components, or the national focus given to CNC machine tools. Yet wherever a shaft crosses a housing in any rotating equipment — centrifugal pumps, compressors, reactors, steam turbines, gas turbines, nuclear primary pumps — there must be a seal holding back the high-pressure, high-temperature, toxic or flammable medium inside. The mechanical seal is that final line of defense, the last-mile barrier protecting equipment operation, and a critical variable affecting maintenance cycles, safety incidents, and unplanned plant shutdowns.

Industry insiders often say: valves block flow, pumps push flow, mechanical seals keep flow in the line. For a million-dollar refinery main pump, the mechanical seal may account for only 3 to 5 percent of pump body cost — but a single seal failure stops the pump immediately, cascades downstream shutdowns, and can cause losses of tens of millions to hundreds of millions in yuan. This asymmetry between extremely low cost share and extremely high failure cost makes mechanical seals a classic case of "small component, big stakes" economics.

In 2025, the global mechanical seal market measured roughly 9 billion US dollars. By downstream application: petrochemicals and chemicals account for about 40 percent, power and water for about 20 percent, general industry for about 20 percent, new energy and high-end equipment for about 15 percent, with food and pharma making up the rest. Annual compound growth runs about 4 to 5 percent — unimpressive at first glance, but this is a highly durable installed-base market. The world's installed pump base exceeds 20 million units, and counting compressors, reactors, and steam turbines, annual replacement demand alone supports a stable 6-billion-dollar base.

Import Dependence Remains High

China's mechanical seal market measured about 18 billion yuan in 2025, roughly 20 percent of the global market. But two facts must be separated immediately: low-end general seal domestic production share already exceeds 90 percent, while high-end dry gas seals, nuclear primary pump seals, and gas turbine seals still carry 60 to 80 percent import dependence. This is the industry's recurring paradox: "70 percent of units made locally, 70 percent of value still imported."

Specifically by product category:

- Single-face general water seals: domestic share above 95 percent, unit price ranging from tens to several thousands of yuan, supplied primarily by hundreds of small-to-mid mills in Wenzhou, Ningbo, and Guangzhou.

- Double-face and cartridge mechanical seals: domestic share about 65 percent, with main players being China Sealing Components Industrial (Cdsii), Nippon Pillar China subsidiary, Huaxiang Sealing, Ningbo Eastern, etc. Unit prices range 3,000 to 30,000 yuan.

- Dry gas seals (for centrifugal compressors, syngas compressors, ethylene cracker compressors): domestic share about 30 percent, unit prices 300,000 to 2 million yuan. Global leaders John Crane (UK Smiths Group) and EagleBurgmann (German Freudenberg) dominate.

- Nuclear primary pump seals: only a handful of Chinese suppliers can deliver, unit prices 2 to 8 million yuan, domestic share below 20 percent. AESSEAL (UK) and Flowserve (US) remain mainstream choices.

This distribution means the story is not "substitution complete" but rather "advancing toward the high end." This article's main thread decomposes that advance.

Unit Price Range and Service Order Structure

Mechanical seals are an "equipment + spare parts + service" three-source revenue business, with the latter two growing in share. A refinery centrifugal pump seal kit might sell for 50,000 to 200,000 yuan, but its lifecycle (over 20-year equipment life) seal-related spending may total 1.5 to 3 million yuan, including periodic replacement, dynamic seal repair, modification upgrade, and emergency repair. Global leaders like John Crane and EagleBurgmann long ago transitioned from pure seal sales to "seal + condition monitoring + lifecycle service" solutions, with service revenue exceeding 40 percent of total. Chinese local players have accelerated this transition in the past five years. Cdsii 2025 annual report disclosed service and parts revenue rose to 38 percent of total, up from 21 percent in 2020.

Mechanical seal downstream concentration is extremely high: petrochemicals and chemicals combined contribute over 60 percent of high-end seal demand; power (thermal, nuclear, wind, gas turbines) about 20 percent; the remaining 20 percent comes from general industry, semiconductors, new energy vehicles, aerospace, and other long-tail demand. This structure means seal manufacturers' fortunes are tightly bound to downstream equipment investment cycles.

Non-Typical Characteristics of the Industry

Mechanical seals are among the few equipment manufacturing segments with several non-typical characteristics. First, non-typical durability: top-end dry gas seals can run 15-plus years in European refineries without failure. Second, non-typical hidden process depth: a silicon carbide ring looks like a piece of black ceramic, but its internal material structure, grain size, porosity, surface wettability, and self-lubrication additives can each significantly affect seal performance. Third, non-typical customer structure: end customers are refinery, chemical plant, and power plant maintenance teams of dozens to one or two hundred people — short decision chains, high technical sophistication, deep personal experience. Fourth, non-typical supply chain structure: core raw materials are highly concentrated.

Geographic Structure of the Global Seal Market

Geographically, the global seal market shows a clear triangle: North America roughly 30 percent, Europe roughly 28 percent, Asia-Pacific roughly 38 percent, with the rest at 4 percent. But this counts installation locations. By supplier headquarters, Europe (including UK) is close to 55 percent, North America about 25 percent, Asia (including China, Japan, Korea) about 18 percent. R&D and high-end manufacturing concentrate in Europe and America; applications and low-end manufacturing concentrate in Asian emerging markets.

China is the largest application market by volume (surpassing the US) and the largest low-end manufacturing base (over half of global output), but it remains in catch-up position for high-end manufacturing and global brand influence. This "big market, weak brand" asymmetry is the logical starting point of the domestic substitution story.

Comparison with Adjacent Sectors

Comparing mechanical seals with adjacent equipment component sectors: industrial bearings are 10 times the size globally; hydraulic components 4 times; industrial valves 10 times; industrial pumps 8 times. Mechanical seals are a "relatively small but high-margin, customization-heavy, service-intensive" segment. This determines the industry pattern — head concentration steadily rises, but it is hard to see rapid consolidation like in auto parts.

Long-Cycle Evolution Direction

Looking at 20-30 year evolution: from "single seal" to "seal system solutions"; from "mechanical contact" to "non-contact"; from "passive response" to "active prediction"; from "geographic localization" to "globally networked." These long-cycle directions correspond to clear technology and business model transitions, and form the main development thread for mechanical seals over the next 20-30 years.

Chapter 2 Product Classification and Technology Tiers

Mechanical seals split into dozens of types by structure, use, and working medium, but six main forms carry production load. Understanding each form's technical boundary is the prerequisite for understanding industry competition.

Note that classification is multi-dimensional. The same seal may simultaneously belong to "double-face," "cartridge," "metal bellows," "silicon carbide vs silicon carbide" categories. This chapter divides by "primary working form" — the conventional product classification.

Single-Face Mechanical Seals

The most basic form: a friction pair (rotating and stationary rings) pressed together, separated by a lubricating film, blocks outward flow. Most municipal water pumps, agricultural irrigation pumps, building HVAC pumps, light chemical pumps, and food pumps use single-face seals priced from tens to thousands of yuan. Technology is mature. Industry insiders call it "rubber rings a few cents each, ring pairs a few tens" red ocean.

Sub-forms include balanced vs unbalanced, internal vs external, stationary vs rotating, single-spring/multi-spring/bellows. Even in this "red ocean," differentiated opportunities exist — food-grade, semiconductor-grade, low-temperature single-face seals are high-margin niche categories at 5 to 20 times general unit price.

Field Service Practice for Single-Face Seals

Even technologically simple single-face seal field service has details worth studying. Replacing a 3-year-old municipal water pump seal seems simple but involves disassembly, inspection, alignment, pressure test, and monitoring. An experienced technician finishes in 30 minutes; a novice may take 3 hours and still fail. This is why even in low-end seal market, head suppliers like Cdsii and Ningbo Eastern can maintain stable share in some customer segments — they provide not just seal product but "seal + installation training + emergency response" service bundles.

Double-Face Mechanical Seals

When process medium is toxic, flammable, hot, or requires strict zero leakage, double-face seals are mandatory — two friction pairs in series with a clean barrier fluid (mineral oil or water-based) in between forming two defenses. Even if process side leaks, only the barrier fluid cavity is affected, not the atmosphere. Chemical reactor agitators, hazardous chemical pumps, high-purity chemical pumps, and pharma fermentation tanks must use double-face seals.

Double-face seal pricing is 5-10 times single-face, typically 3,000 to 30,000 yuan per unit. Technical difficulty rises beyond structural complexity to barrier fluid system design — how to maintain pressure 0.15 to 0.3 MPa above process, how to control temperature, how to cool barrier fluid, how to monitor liquid level for leak detection. These auxiliary systems (Plan 53, Plan 54, Plan 74 in API 682) are core indicators of seal maker technical maturity.

Cartridge Mechanical Seals

Cartridge seals are the most important engineering innovation in seal industry in the past 20 years. Traditional split seals require field assembly, spring compression adjustment, and alignment, with installation error rates 15 to 20 percent. Cartridge seals pre-assemble the entire seal module (rotating and stationary rings, O-rings, sleeve, gland, springs, auxiliary system connections), factory pressure-tested, ready for direct installation on site.

Core values: cuts install time from hours to under 30 minutes; reduces startup failure rate from 15 to under 3 percent; decouples seal replacement cycle from pump overhaul. Today 80 percent of new seal installations in US, European, and Japanese refineries are cartridge type. China penetration is only about 50 percent, the core incremental market for domestic substitution.

Cartridge seal pricing is 30-50 percent above split seals, but lifecycle cost (including install labor, downtime loss, startup failure loss) drops significantly. Cdsii, Ningbo Eastern, Wenzhou Liwei, etc., all have cartridge design and manufacturing capabilities, but in large-size (shaft diameter 200mm+), high-pressure (10 MPa+) cartridge, foreign players still hold clear advantage.

If China cartridge penetration rises to 60 percent over 10 years, just this upgrade order alone gives the industry cumulative market opportunity over 100 billion yuan.

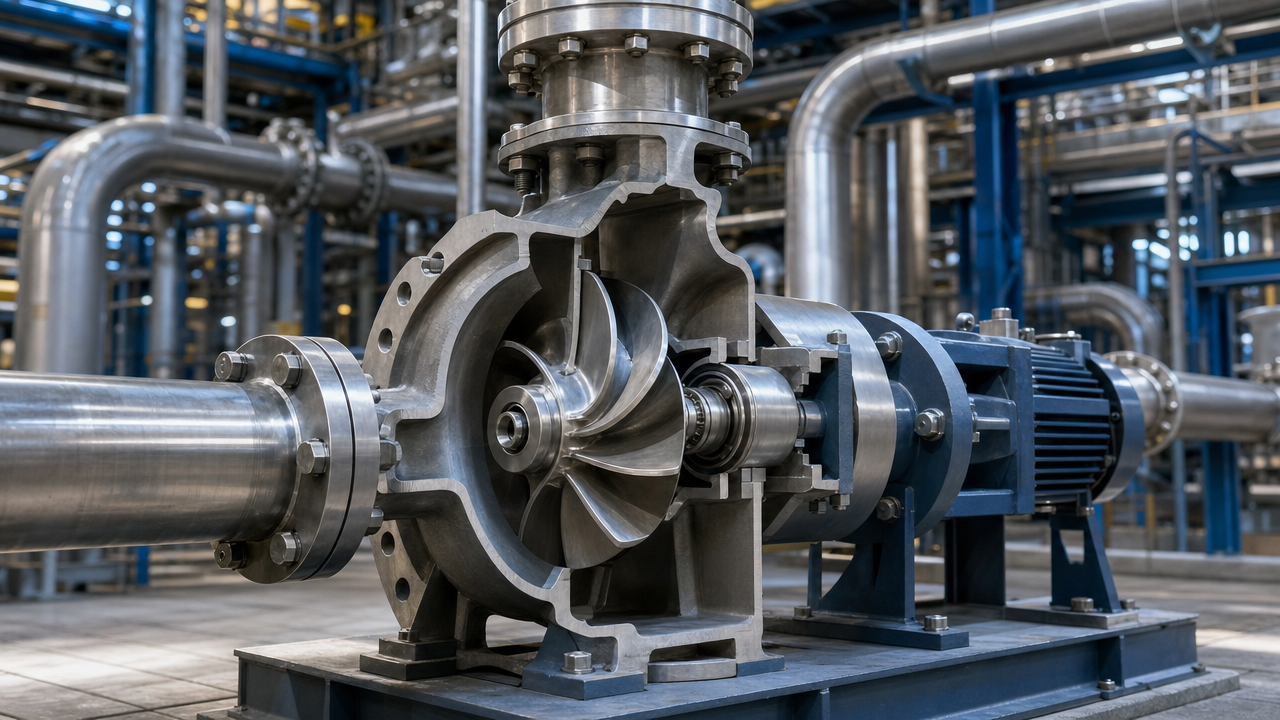

Dry Gas Seals

Dry gas seals are the jewel in the crown. Traditional liquid-lubricated seals rely on liquid film to separate rings, but when sealed medium is high-speed rotating gas (syngas compressors, ethylene cracker compressors, natural gas pipeline compressors), liquid film cannot form. Must switch to gas dynamic pressure effect — extremely precise spiral or T-shaped shallow grooves (only 3 to 10 microns deep) machined on rotor surface. High-speed rotation pumps gas into grooves forming a pressure film, lifting rings apart by a few microns for non-contact sealing.

Dry gas seal technical barrier is extremely high: groove geometry, depth, and angle directly determine film stiffness and stability, machining precision must reach sub-micron level; rotor material must be silicon carbide or CVD diamond coating; seal gas system must be strictly dried, filtered, pressure-controlled; fault diagnosis needs differential pressure, flow, vibration multi-parameter online monitoring. A large ethylene main compressor dry gas seal unit can reach 1 to 3 million yuan.

Global dry gas seal market is divided by John Crane and EagleBurgmann, combined share over 70 percent. John Crane 2025 financials disclosed dry gas seal division revenue of about 900 million pounds, nearly 60 percent of total. China has fewer than five with complete dry gas seal design capability: Cdsii (gained foundation by acquiring Germany's DMK in 2018), Ningbo Eastern (with Siemens collaboration), Tianjin Dingming (with Nippon Pillar collaboration).

The dry gas seal working principle is essentially an extension of gas dynamic bearings. A large dry gas seal typically uses tandem arrangement — main seal bearing the main pressure drop, secondary seal as safety backup. Between the two seals, separation gas (typically dry filtered nitrogen or process gas) is injected, forming multiple protection layers.

By downstream application: large ethylene main compressor (unit 2-3M yuan, global annual demand 100-150 units, most competitive); syngas compressor (1-2M yuan, 300-400 units, good domestic substitution progress); air separation main compressor (0.8-1.5M yuan, 200-300 units, good domestic progress); CO2 compressor (0.6-1.2M yuan, 150-200 units, new emerging market driven by dual-carbon); natural gas pipeline compressor (0.5-1M yuan, 200-300 units, foreign suppliers dominant); gas turbine dry gas seals (1-3M yuan, 100+ units, almost entirely monopolized by foreign suppliers).

Operation Ecosystem of Dry Gas Seals

Once a dry gas seal is installed, its operation ecosystem forms a relatively closed long-term supplier-owner relationship. From installation to first major overhaul of a large ethylene main compressor dry gas seal typically takes 8-12 years. During this period the seal manufacturer provides periodic inspection (1-2 times per year), condition monitoring analysis, emergency response, etc. These long-term service relationships bring stable service revenue. Annual service contract fee per main compressor dry gas seal can reach 200-500K yuan — a substantial "cash cow" business.

Magnetic Seals and Magnetic Drive

Magnetic seals are not strictly "sealing" but a zero-leakage power transmission solution: a pair of magnetic couplers transmits motor torque through a hermetic isolation sleeve to the pump impeller. No rotating shaft penetrates the housing from the medium side, fundamentally eliminating leakage. Widely used in highly toxic, strongly corrosive, precious metal catalyst, and radioactive medium scenarios.

Magnetic Drive Market Extension

Magnetic drive was originally limited to small pumps (under 50 kW, processing highly corrosive, toxic, flammable media). But in recent years, KSB Germany, Ebara Japan, KLAUS UNION Germany, and others have boosted torque transmission via magnetic material upgrades and structure optimization, extending magnetic drive to mid-size pumps (200-500 kW). This may cause localized impact on traditional mechanical seal markets. For instance, pumps for strong-corrosive media (sulfuric acid, hydrochloric acid, hydrofluoric acid chemical pumps) that previously required double-face seals may switch to mid-size magnetic drive solutions, completely eliminating seal leak risk.

Lip Seals and Oil Seals

Lip seals and oil seals — the simplest seal forms, mainly used for motor shafts, gearbox shafts, and low-speed rotating equipment dust and leak prevention. China is the world's largest lip oil seal producer, annual output over 5 billion units, suppliers concentrated in Zhejiang, Shanghai, Guangdong. Low technical threshold, low unit price (cents to a few yuan), basically not in the same competitive dimension as high-end mechanical seals.

Seal Auxiliary Systems: Overlooked High-Margin Segment

Beyond the six main seal types is an often-overlooked but highly profitable product — seal support systems. A complete seal support system includes barrier fluid tank, circulation pump, heat exchanger, pressure monitoring instruments, flow meter, control valve, piping, local panel. Prices range from 50,000 to 500,000 yuan, with margins often higher than main seals (35-45 percent range).

The international API 682 standard defines 65 seal auxiliary plans (Plan 01 to Plan 75). Common ones: Plan 11, Plan 13, Plan 32, Plan 53A/B/C, Plan 54, Plan 72/74/75. Complete seal system design capability is the moat of high-end seal makers.

Boundary Between Lip and Mechanical Seals

Although both lip and mechanical seals serve dynamic sealing, their principles differ fundamentally: lip seals are contact-type elastic seals (rubber lip interference compressing shaft); mechanical seals are precision-matched end faces with relative motion (extreme flatness with liquid film lubrication). The former is simple, short-lived (6 months to 2 years), unsuitable for high pressure; the latter is complex, long-lived (years to over a decade), the mainstream choice for process equipment.

Chapter 3 Process Barriers and Materials System

Mechanical seals look like "two rings pressed together," but doing them well — strong enough to last 20 years of heavy-duty operation — requires comprehensive contests across materials, machining, design, and inspection systems.

Global Supply Pattern of Materials

Core raw material supply is highly concentrated. Silicon carbide substrate top global suppliers: Japan Shinagawa Refractories, Germany Schunk Group, US Saint-Gobain, Japan Tokai Carbon, Japan Nissin Denki. China local suppliers: Shandong Jinning, Weifang Huamei, Yantai Tongli — can supply mid-low end SiC substrates; high-end still mainly imported. Metal bellows top suppliers: US BellowsTech, Switzerland Witzenmann, Germany Senior, UK Servometer. Perfluoroelastomer (FFKM) suppliers extremely concentrated: US Chemours (DuPont's Kalrez brand) about 50 percent global share, Japan Daikin (DAI-EL Perfluor) about 20 percent, Switzerland Solvay (Tecnoflon) about 15 percent. Special alloys (Hastelloy, Inconel, duplex stainless steel, super duplex stainless steel) global suppliers include US Special Metals, US Haynes International, Germany VDM Metals, Austria Voestalpine.

Friction Pair Material Combinations

The rotor and stator material combination is the root of seal performance. Each material's physical and chemical properties differ greatly.

Silicon carbide (SiC) is the most important end-face material today. Stable crystal structure, Mohs hardness 9.3 (second only to diamond and cubic boron nitride), thermal conductivity 120 W/(m·K), extremely low thermal expansion, extreme chemical inertness. But brittle, impact-intolerant, machining 3-5 times the cost of cemented carbide. By manufacturing process: reaction-bonded SiC (RB-SiC), pressure-sintered SiC (SSiC), chemical vapor deposition SiC (CVD-SiC).

Diamond coating is the crown of seal end-face materials. Mohs 10 hardness, thermal conductivity over 2000 W/(m·K), wear rate an order of magnitude below SiC. Mainly used in dry gas seals. Global makers capable of stable production fewer than five. China cannot yet industrialize high-quality diamond coating seal rings — an important domestic gap.

Carbon graphite is another important end-face material. Excellent self-lubrication (even without liquid film won't burn immediately), good thermal stability (above 500°C), low density (1.8-2.0 g/cm³, well below SiC's 3.2). But low hardness, limited compressive strength, unsuitable for high pressure. By impregnation material: resin-impregnated, metal-impregnated (copper, antimony, lead, nickel, etc.).

Common combinations: cemented carbide vs carbon graphite (most classic, single-face mainstay); silicon carbide vs carbon graphite (standard for double-face and chemical seals); silicon carbide vs silicon carbide (high-pressure, high-speed, abrasive, corrosive extreme conditions); silicon nitride vs carbon graphite (semiconductor ultra-pure water, pharma pure water); diamond coating (CVD/PCD on SiC substrate).

SiC ring production is China seal makers' key bottleneck. High-end reaction-bonded SiC substrate long depended on imports from Japan Shinagawa, Germany Schunk, US Saint-Gobain, priced 3-5 times generic SiC. Domestic SiC makers like Jinning and Huamei are catching up, but high-purity, large-size, low-porosity SiC ring domestic share remains under 30 percent.

Friction Pair Operating Mechanism and Wear Modes

End-face wear during seal operation is a fine science. Ideally a stable mixed-lubrication state forms — small amounts of liquid or gas filling micro-gaps to form a few-micron film. Under this state wear is minimal, seals run continuously for years.

Actual operation conditions produce abnormal wear modes: dry friction wear, abrasive wear, corrosive wear, cavitation wear, crystallization wear. Understanding these is the basis of seal selection and failure diagnosis. Global leaders like John Crane and EagleBurgmann have built complete failure case libraries over decades. Chinese local makers are catching up — Cdsii has been systematically building failure case databases in recent years.

Elastic Element Design

The seal's elastic compensation relies on springs or bellows. Its role is to compensate end-face wear, accommodate axial movement, compensate assembly errors, and maintain proper contact pressure.

Single-spring is simple and cheap but immersed in medium prone to corrosion blockage; multi-spring distributes evenly but demands precise machining; metal bellows (multilayer stainless steel or Hastelloy welded thin-plate bellows) serve both sealing and elastic compensation, the top choice for high-temperature (300°C+), toxic, high-pressure conditions.

Metal bellows manufacturing is extremely fastidious: plate thickness only 0.15 to 0.30mm, hydraulic forming dozens of uniform bellow nodes, every two connected by laser precision welding. A high-end metal bellows yield is only 60-70 percent — one of the highest cost components in seal manufacturing.

Auxiliary Sealing Rings

Auxiliary sealing rings (O-rings, wedge rings, V-rings) seal stationary joint surfaces. Material selection directly determines seal lifespan. Common materials: fluororubber (FKM/Viton), perfluoroelastomer (FFKM/Kalrez), EPDM, PTFE+graphite composite, soft metals.

API 682 Standard and Industry Specifications

The most important international mechanical seal standard is API Standard 682 fifth edition (2024). All major Chinese seal makers like Cdsii, Ningbo Eastern, Huaxiang Sealing have completed API 682 fifth edition certification. Other standards include ISO 21049, ASME B73 series, DIN 24960, JIS B 2405, etc.

Machining Precision and Inspection

Rotor and stator end-face flatness must be within three light bands (about 0.9 microns), surface roughness Ra under 0.05 microns, perpendicularity under 5 microns. Such precision requires dedicated end-face grinders and high-precision platform inspection tools.

Design Capability and Field Experience

Hardware is the threshold; design capability and field experience are the software thresholds — often the more critical differentiator. From theoretical design to successful operation, dozens of engineering problems must be solved: thermal-mechanical-flow coupling analysis; secondary seal compensation design; medium compatibility; failure mode analysis.

Inspection Capability Hidden Barrier

Seal performance final validation depends on full-condition test stands — capable of simulating real customer conditions: high pressure, high temperature, high-speed rotation. Single test stand construction cost exceeds 30 million yuan; fewer than 20 global makers can build complete ones.

Digital Manufacturing Introduction

In recent years seal manufacturing has rapidly digitalized. Traditional seal manufacturing relied on master technician feel and experience, but in the past 5 years all global heads invest in "digital twin factories" — collecting equipment, parameters, and product quality data from each process to cloud in real time, continuously optimizing manufacturing with AI algorithms.

Chapter 4 Major Manufacturers and International Benchmarks

Mechanical seals are a classic "global top 5 take 70 percent, local dozen-plus split the rest" pattern. Understanding it requires global perspective.

Global Top 10 Seal Makers Overview

By 2025 revenue: 1. John Crane (UK) 14.4B RMB; 2. EagleBurgmann (Germany) 7.2B; 3. Flowserve Seal Division (US) 4.3B; 4. AESSEAL (UK) 2.6B; 5. Cdsii (China) 2.6B; 6. Chesterton (US) 1.8B; 7. Nippon Pillar China (Japan-Germany JV) 1.2B; 8. Smiths Mechanical Seals (US) 0.9B; 9. Ningbo Eastern (China) 0.8B; 10. Hatebur (Switzerland) 0.6B.

China local makers occupy two of top 10 (Cdsii, Ningbo Eastern), combined about 4.5 percent share — clearly mismatched with China's 30 percent share of global mechanical seal consumption.

International Four Major Seal Giants

John Crane (UK Smiths Group): Undisputed global mechanical seal champion. FY2025 (ended April 2026) revenue about 1.6 billion pounds, roughly 14.4 billion yuan. Product line spans low-end single-face to top dry gas seals across full spectrum, but the real moat is dry gas seal — Type 28 series is the de facto standard for petrochemical compressors.

EagleBurgmann (Germany Freudenberg + Japan EKK JV): Second-largest globally. 2025 revenue about 900M euros, roughly 7.2B yuan. Dry gas seal technologies DGS9, HSE series are John Crane's main competitors. Headquartered in Wolfratshausen, Germany; large Suzhou manufacturing base in China.

Flowserve Mechanical Seal Division (US): US fluid equipment integrated giant. 2025 seal division revenue about 600M USD, roughly 4.3B yuan. Strength is synergy with own pumps and compressors.

AESSEAL (UK): Family business. 2025 revenue about 300M pounds, roughly 2.6B yuan. Smallest of the four giants but fastest growing — past decade compound 12 percent. Specialty: nuclear seals.

Chesterton (US): Old US seal maker, founded 1884. 2025 revenue about 250M USD, roughly 1.8B yuan. Specialty: refinery centrifugal pump seals.

Global Seal Industry M&A History

The seal industry over past 30 years has seen significant M&A consolidation. 1990s horizontal consolidation: Smiths Group acquired John Crane in 1999; Freudenberg and EKK formed EagleBurgmann JV in 2004; Flowserve acquired Durco in 1997. 2000s vertical integration. 2010s service transformation. 2020s Chinese participation: Cdsii 2018 acquisition of DMK Germany marked first major Chinese participation in global seal consolidation.

R&D Investment Comparison

R&D intensity (R&D expense / revenue) is a key metric. John Crane 9.4%, EagleBurgmann 9.4%, Flowserve Seal 8.1%, AESSEAL 9.2%, Cdsii 6.2%, Ningbo Eastern 5.3%, Huaxiang 5.4%. Chinese local makers' R&D intensity is clearly behind foreign giants — a core reason China still needs time to catch up in top-end technology.

Global Employee Distribution

By geographic employee distribution: John Crane 6700 globally (6% China, 28% NA, 42% Europe, 24% other); EagleBurgmann 5800 (9% China, 56% Europe); Cdsii 3800 (91% China, only 5% Europe via DMK + Shenyang); Ningbo Eastern 1200 (97% China). Chinese local makers are still early-stage in internationalization.

Chinese Local Leading Manufacturers

Cdsii (300470.SZ): Absolute leader of Chinese mechanical seal industry. 2025 revenue about 2.6 billion yuan, attributable net income 470 million yuan, net margin 18 percent — the most profitable in domestic seal industry.

Nippon Pillar China: Strictly a Japan-Germany joint China manufacturing platform. 2025 China revenue about 1.2 billion yuan.

Ningbo Eastern Seal: Veteran private seal maker. 2025 revenue about 800 million yuan.

Huaxiang Sealing (Huaxiang Shares subsidiary, 002048.SZ): Specializes in metal bellows mechanical seals. 2025 seal business revenue about 500 million yuan.

Wenzhou Liwei Seal: Representative of Wenzhou seal cluster. Unlisted, estimated annual revenue around 400 million yuan.

Beyond these, hundreds of small-to-mid seal makers cluster in Wenzhou and Ningbo (Zhejiang), Guangzhou (Guangdong), Zhangzhou (Fujian), Suzhou (Jiangsu), Yantai (Shandong), Dalian (Liaoning), mainly making low-end general seals.

Foreign Giants' China Localization Strategy

John Crane China: "Service network first" strategy. Shanghai HQ plus large service centers in Beijing, Yantai, Guangzhou, Chengdu, Wuhan.

EagleBurgmann China: "Manufacturing localization" strategy. Suzhou plant heavy investment from early 2010s.

Flowserve China: "Pump channel" strategy. All Flowserve centrifugal/chemical pumps in China standard-equipped with own seals.

AESSEAL China: "Nuclear specialty" strategy. Shanghai office mainly serves nuclear customers.

Chesterton China: "JV + localization" strategy.

Second-Tier Chinese Makers

Ningbo Sanli, Wuhan Eastern, Sichuan Bluestar, Shaanxi Blower Group (Shaangu Power, 601369.SH) Seal Division are second-tier local players in specific niches.

Industry Human Capital Structure

Mechanical seals depend heavily on engineer experience. A senior engineer able to independently handle large project seal design and field service typically takes 8-12 years to train.

Chapter 5 Downstream 1 — Petrochemicals and Chemicals

Petrochemicals and chemicals together contribute over 60 percent of high-end seal demand.

Refinery Major Pump Seals

China is the world's second-largest refining nation. By end-2025, China's total refining capacity reached 940 million tons per year, second only to the US's 970 million tons. A 10 million ton modern refinery has over 1000 internal centrifugal pumps, dozens of reciprocating pumps and compressors, with about 200 key process pumps, each with one or two mechanical seals.

The 2025 China refinery process pump seal market is about 2.8 billion yuan, with domestic share about 70 percent.

By installation type seal demand structure: atmospheric and vacuum distillation (per 8-10M ton year about 80-120 critical pumps, seal unit price 30-80K yuan, total 4-7M); catalytic cracking (per 2-3M ton about 50-80 critical pumps, 50-150K, total 4-10M); hydrocracking (per 2-3M ton about 40-60 critical pumps, 80-200K, total 5-10M); ethylene installation (per 1M ton about 200-300 process pumps + 3-5 main compressors, total 20-40M); polyethylene installation (per 0.3-0.5M ton about 50-80 process pumps, total 3-6M).

A 10M ton/year modern integrated refining base seal procurement total during construction is 150-250M yuan, with annual operating maintenance about 15-30M yuan. The highest-value customer segment.

Procurement Characteristics of Major Domestic Refineries

Sinopec system (Maoming, Yangzi, Zhenhai, Shanghai, Yanshan, Qilu, Qingdao): regulated central enterprise procurement, strict supplier qualification, prefer products with long-term operating track records.

CNPC system (Daqing, Fushun, Liaoyang, Dushanzi, Lanzhou, Guangxi, Jieyang): similar central procurement, with some regional subsidiary autonomy.

CNOOC system (Huizhou, Dalian): smaller but newer equipment.

Private refining (Hengli Dalian, Zhejiang Petrochemical Zhoushan, Shenghong Lianyungang, Dongming, Jingbo): most friendly to local Chinese seal makers, fast decisions, price-sensitive, demanding response time.

Private chemical new materials (Wanhua Chemical, Satellite Chemical, Huafeng Group, Lomon Billions, Hoshine Silicon): growing segment leaders, specialized seal demand, prefer long-term cooperation with domestic makers.

Chemical Reactor Agitator Seals

Chemical reactor agitator seals are another major mechanical seal application. China chemical industry 2025 new reactor investment about 90 billion yuan; per 3 percent seal share, new reactor seal market about 2.7 billion yuan, plus existing replacement 1.5 billion, totaling 4.2 billion. Domestic share about 75 percent.

By process subdivision: strong-exothermic polymerization reactors (SBR, ABS); high-temperature high-pressure reactors (urea, ammonia synthesis, methanol synthesis); corrosive reactors (chlor-alkali, nitric acid, sulfuric acid); food and pharma reactors; semiconductor wet electronic chemical reactors.

Coal Chemicals: Overlooked Major Customer

China coal chemical industry is another major mechanical seal downstream often overlooked. 2025 China coal chemical industry scale about 8 trillion yuan, including coal-to-oil, coal-to-olefins (MTO), coal-to-ethylene glycol, coal-to-gas, coal-to-hydrogen, coal-to-ammonia.

Coal chemical mechanical seal demand emphasizes "reliability under extreme conditions." A large MTO unit (100M tons/year olefins) seal procurement is 80-150M yuan. Representative projects include Ningxia Baofeng Energy, Inner Mongolia Zhongtian Hechuang, Shaanxi Yanchang Petroleum, Xinjiang Guanghui Group.

High-End Chemicals: Specialty and New Materials

Fine chemicals and new materials industry is the high-value low-volume market for seals. Nylon 66 adiponitrile polymerization reactors, polyimide monomer reactors, PEEK resin reactors — these chemicals usually combine high temperature, strong corrosion, and easy polymerization, demanding engineering-limit seal performance. Unit seal price can reach 200-500K yuan.

Domestic share about 40 percent for this type. Less than 5 domestic makers have this capability. PEEK projects (Jilin Zhongyan, Suzhou Junding, Shanghai Hecheng, Jinan Tianfu) still procure mostly John Crane and EagleBurgmann.

Pesticide and Pharma Intermediate Industry

Pesticide and pharma intermediate industry is another important reactor seal segment. China is the world's largest pesticide and pharma intermediate producer, 2025 combined output over 15 million tons.

Food-Grade and Beverage-Grade Reactors

Food, beverage, dairy, condiment, health product reactors are also important seal downstream. China food industry 2025 scale over 12 trillion yuan, related seal market about 6 billion yuan, domestic share about 75 percent.

Gas Turbine Dry Gas Seals: Cross-Industry Bridge

Gas turbines are a cross-industry equipment between petrochemicals and power. Large gas turbine shaft seals must use dry gas seals, technical difficulty only second to nuclear primary pump seals. Chinese in-service gas turbines (GE 9F, 9HA; Siemens-Energy SGT5-8000H; Mitsubishi M501J) seals are basically Western brand originals.

Private Refining Rise Reshapes Seal Procurement

Past decade biggest change in Chinese refining: private refineries rising. Hengli Petrochemical Dalian (20M ton refining + 4.5M ton ethylene), Zhejiang Petrochemical Zhoushan (40M + 2.8M), Shenghong Lianyungang (16M + 1.1M) — these large private projects came online 2018-2024.

Private refineries' attitude toward seal procurement differs significantly from central enterprises. Driven by "cost control + domestic substitution" dual logic, they clearly prefer domestic seal makers. Hengli, Zhejiang Petrochemical, Shenghong new installations have over 65 percent domestic share in critical process pump seals, with Cdsii as biggest beneficiary.

High-End Chemical New Materials High-Margin Opportunities

Chemical new materials are another high-growth seal sub-market. POE, PEEK, PPS, PI, PA66, ECH — these high-end chemical new materials projects open intensively in 2024-2026.

POE example: planned projects include Wanhua Chemical (Penglai, Yantai), Satellite Chemical (Lianyungang), Jingbo Petrochemical, Dongfang Shenghong — combined design capacity over 2M tons/year. POE process involves highly active catalysts and low-temp low-pressure polymerization, with extremely demanding reactor seals. Cdsii, Zhonghao Chenguang, and others are codeveloping POE-specific seal solutions, single price 300-800K yuan, margin over 35 percent.

Chapter 6 Downstream 2 — Nuclear, Water Pumps, Wind, Rail

If petrochemicals and chemicals are seals' "main battlefield," then nuclear, water pumps, wind, rail are technology content and strategic value "high ground."

Nuclear Primary Pump Seals: Industry Crown

Nuclear power plant reactor coolant primary pump (nuclear primary pump) is the peak of mechanical seal technology. A 1 million kW PWR plant has 4 primary pumps; each needs 3 mechanical seals in series — total 12 seals per plant; operating condition is 155 atm, 290°C radioactive high-pressure water, 1500 rpm, demanding 12,000 hours continuous leak-free operation.

Global suppliers: Flowserve (US, AP1000 etc.), AESSEAL (UK, VVER, CANDU), John Crane (some Gen 2+). Cdsii is the only domestic supplier capable of complete nuclear primary pump seal design.

China nuclear power fast track: by end-2025, 60 units in operation, 27 under construction, over 80 planned. Future decade core primary pump seal new + replacement market over 12 billion yuan.

Special Challenges of Nuclear Seals

Nuclear power seal requirements far exceed normal industrial scenarios: medium radioactivity, long operating cycles, accident condition design, extremely long validation cycles (typically 8-12 years from design to first commercial), strict regulation.

Other Nuclear Plant Seals

Nuclear plants also have many other dynamic equipment needing seals: charging pumps, safety injection pumps, auxiliary feedwater pumps; residual heat removal pumps, circulating cooling water pumps; emergency diesel cooling water pumps, fire pumps. A 1M kW nuclear plant total construction phase mechanical seal procurement 30-50M yuan, annual operation maintenance about 10M yuan.

Nuclear Industry Chain Seal Value Transmission

Building 8-10 new nuclear units per year for the next decade, total seal procurement of 6-8 billion yuan for construction plus 7-9 billion yuan for operating maintenance — combined 13-17 billion yuan. Mostly split among Cdsii, AESSEAL, Flowserve.

Procurement Characteristics of Nuclear Operators

Chinese nuclear operators: CGN, CNNC, SPI, Huaneng, Huadian, Datang, China Energy Investment. CGN and CNNC combined run over 80 percent of units. Key procurement characteristics: strict nuclear safety qualifications, long supplier certification (5-8 years), unified parts catalog, centralized tender, strict operating record requirements.

Large-Scale Water Transfer and Water Conservancy Pumps

South-to-North Water Diversion (East, Central, West routes), Yangtze-to-Huai, Central Yunnan Water Diversion, Xinjiang Water Diversion, Xiongan Water Diversion — large national water projects use many giant axial and mixed flow pumps. Per pump seal value 50-200K yuan, project total 100-300M yuan.

Procurement Characteristics of Major Water Projects

Large sizes (500-1500mm shaft diameter), low pressure low temp (under 1 MPa, room temp), super long life requirement (15-25 years no major overhaul), highly local procurement. Domestic share near 100 percent.

Wind and Offshore Wind

Wind energy main mechanical seal applications: gearbox seals, main shaft seals, yaw/pitch hydraulic seals. Onshore wind per turbine seal value 10-30K yuan; offshore due to extreme environment (salt fog, humidity, vibration, hard to inspect) — per turbine seal value can reach 50-100K yuan.

China 2025 new wind capacity 130 GW (onshore 110 + offshore 20), per average 6 MW unit, about 21,700 new turbines, seal procurement alone over 600M yuan.

Special Technical Challenges of Wind Gearbox Seals

Wind gearbox seals are a relatively independent sub-category with very different requirements from traditional petrochemical seals. Super-long maintenance-free cycle (onshore 8 years, offshore 15), extreme condition fluctuation, lubricant compatibility, large size (600-1000mm OD).

High-Speed Rail and Rail Transit

High-speed train key seal components are EMU transmission gearbox seals and brake system hydraulic seals. CRRC Qingdao Sifang, Changchun Rail, Tangshan Rail, Zhuzhou Electric — domestic share is high.

Semiconductor Ultra-Pure Chemical Plant Seal Requirements

Semiconductor ultra-pure chemical plants demand top industry cleanliness for seals. A seal component releasing even a few ppb of metal ions can cause downstream semiconductor chip defects. Detailed by subsegment: SPM, hydrofluoric acid (HF), isopropanol (IPA), photoresist auxiliary chemical plants.

China semiconductor wet electronic chemical plant total construction bases: Shanghai, Beijing, Suzhou, Wuxi, Wuhan, Hefei, Xi'an, Chengdu, Shenzhen. Annual seal procurement 500-800M yuan, domestic share under 20 percent.

Chapter 7 Platform Perspective: From Downstream Factory Identification to Seal Procurement Matching

Understanding mechanical seals cannot avoid a fundamental question: How do seal makers find downstream factories actually using seals? Among them, which are refineries, which are chemical plants, which have hundreds of installed pumps?

This is not a new question in the seal industry. Foreign giants like John Crane have deployed in China for two decades, relying on dozens of seal engineers permanently rooted at Sinopec, CNPC, CNOOC refining and chemical sites, building databases of every critical pump's model, seal model, last replacement date, next replacement date. This "human on site" approach is extremely costly and only covers central enterprise customers. For private refining, chemical new materials, fine chemicals — small-to-mid customer groups — seal makers still rely on exhibitions, industry associations, and old customer introductions for customer acquisition, with extremely low coverage efficiency.

Tianxia Gongchang as a B2B platform covering 4.8 million active manufacturing factories in China, differs fundamentally from full business registries like Qichacha or Tianyancha — those have 170 million enterprise records, but over 95 percent are not manufacturing factories (trading, consulting, shell, individual businesses, food service, retail). The remaining 5 percent contain many "zombie factories" that have closed, transformed, or changed business scope. The platform uses business registration, tax data, electricity, patents, recruitment, official website, customs data and other multi-dimensional cross-validation to remove this noise and build a "active, with real production site, real order flow" factory pool. For seal makers this means filtering at source — identifying real seal-purchasing customers rather than wasting time across 170 million enterprise records.

Specifically several typical filter paths for mechanical seal downstream identification:

First, "filter refineries by installation type": filter domestic refineries, catalytic cracking installations, hydrocracking installations, ethylene installations, polyethylene installations, polypropylene installations, aromatic installations, coal chemical installations.

Second, "filter reactor seal downstream by chemical product": filter epoxy resin factories, polyamide factories, polyester chip plants, PEEK plants, polyimide plants, pesticide active ingredient plants, pharma intermediate plants, fine chemical plants.

Third, "filter supply channels via equipment OEM": filter centrifugal pump manufacturers, multistage pump manufacturers, reactor manufacturers, agitator manufacturers, compressor manufacturers, steam turbine manufacturers, gas turbine manufacturers, nuclear main equipment plants, pump valve clusters.

Fourth, "filter industrial clusters by region": Wenzhou seal cluster, Ningbo seal plants, Guangzhou seal components, Shanghai high-end seals, Suzhou precision seals.

Fifth, "filter subdivision customers by high-end condition": nuclear plant list, offshore wind farms, semiconductor wafer fabs, semiconductor chemical plants, biopharma GMP plants, food fermentation plants, coal gasification plants, chlor-alkali plants, sulfuric acid plants, nitric acid plants, urea plants, ammonia synthesis plants.

Combining these four-dimensional cross-filtering can refine seal sales target customer lists from "1 million potential national enterprises possibly buying seals" down to "5000 factories actually with seal procurement need," boosting sales lead efficiency by dozens of times.

Key Points for Different Seal Categories

Different seal categories' downstream targeting differs greatly. Single-face general (municipal supply, light industry): targets at municipal water supply equipment plants, HVAC engineering companies, irrigation equipment plants. Double-face chemical seal: hazardous chemicals production enterprises, pesticide intermediates plants, fine chemicals new materials. Cartridge high-end: 10M ton refineries, million-ton ethylene plants, extra-large chemical bases. Dry gas seal: air separation projects, ammonia synthesis projects, CO2 utilization plants. Top-end nuclear/turbine: nuclear power operators, gas turbine plants, offshore wind operators.

Application of Factory Identification in Seal Sales

Concrete example: a Chinese mid-sized seal maker (500M annual revenue) targeting "chemical reactor seal" segment. Step 1: filter chemical products — chlor-alkali chemical plants, chemical mixing, polyethylene production, polypropylene production, ABS production, PVC production — getting 5000-8000 initial leads. Step 2: geographic filtering — focus on Jiangsu chemical, Shandong chemical, Zhejiang chemical industrial parks. Step 3: scale filtering — large chemical groups, listed chemical companies. Step 4: product combination — same customer producing epichlorohydrin and epoxy resin. Through four-step filter, refine 5000-8000 leads to 200-300 priority targets. Per sales engineer monthly deep-dive 20-30 customers, annual signed 50-80 customers, average single order 3-5x traditional mode.

Long-Term Significance of Factory Identification for Seal Industry

From "relationship sales" to "precision sales" transformation. From "broad net" to "key breakthrough" strategy upgrade. From "selling product" to "selling solutions" mode upgrade. "Lane changing" opportunity for small-to-mid seal makers.

Chapter 8 High-End Breakthrough: Dry Gas Seal, Nuclear, Gas Turbine Three Main Battles

The real plot of domestic substitution story plays out in three high-end main battles.

Dry Gas Seal: Breakthrough from Mid-Parameter to Ethylene Main Compressor

A large ethylene installation main compressor dry gas seal is worth 2-3M yuan, with margin over 40 percent. China dry gas seal market 2025 about 2.2 billion yuan, domestic share only 30 percent, expected to reach 3.5 billion by 2030 with domestic share to 50 percent. Three core drivers: Cdsii's DMK technology digestion; new domestic ethylene capacity bringing 80 main compressor dry gas seal demand; first-batch large ethylene installations entering major overhaul replacement cycle.

Nuclear Primary Pump Seal: Highest-Value Domestic Substitution

Cdsii started nuclear primary pump R&D in 2018, first supplied Hualong One demo reactor in 2022, achieved 12,000-hour validation in 2024. By 120B nuclear primary pump market over next decade with Cdsii targeting 40 percent domestic share — single category over 48 billion yuan, annual 5 billion.

Gas Turbine Dry Gas Seal: Energy Transition Spillover

As energy transition advances, demand for natural gas peaking, distributed, offshore platform gas turbines rises fast. China 2025 gas turbine installed capacity over 120 GW. Annual gas turbine dry gas seal market about 800M-1.2B yuan, domestic share under 15 percent.

High-End Breakthrough Technology Path Choice

Three typical paths: independent R&D + own test stand (Cdsii); overseas M&A + technology absorption (Cdsii DMK); technology cooperation + co-development (Ningbo Eastern with Siemens).

High-End Breakthrough Customer Access Logic

Strict customer access logic: operating track record, trial validation, qualifications, field service capability — all are hidden barriers.

Overseas Market Expansion Possibility

Cdsii has secured orders in Middle East, Southeast Asia, Africa, but scale still small (2025 overseas share about 10 percent). By 2030, expected overseas share rising to over 20 percent.

Chapter 9 Capacity Expansion: Three Representative Companies Breakdown

Industry sentiment directly reflects in head company capacity expansion pace. 2024-2026 obvious capacity expansion cycle in China mechanical seal industry, driven by: downstream petrochemical project investment, accelerated domestic substitution, foreign giant localization counter-thrust, structural tightness in high-end categories.

Cdsii Chengdu Base and DMK Shenyang Base

Cdsii 2025 disclosed capacity investment plan: new Chengdu high-end seal production base, 850M yuan, 500K seals per year, online mid-2027. DMK Shenyang base planned annual dry gas seal 3000 sets, 2025 actual utilization about 87 percent. Second phase 2027 +2000 sets.

R&D Investment Direction of Head Manufacturers

Cdsii 2025 R&D investment 160M yuan: dry gas seal technology upgrade (30%), nuclear seal technology (25%), semiconductor ultra-pure seal (15%), digital technology (15%), new seal forward research (10%), other basics (5%).

Cdsii Chengdu HQ Capacity Upgrade

Chengdu HQ 280 acres, 1800 employees. 2025-2027 plans 650M yuan total capex.

Foreign Giants' China Base Capacity Trends

John Crane Shanghai +80K seals (2026), EagleBurgmann Suzhou +150K (2027), Flowserve Suzhou +60K (2026), Chesterton +20K (2025). Total +310K, about 60 percent of Chinese local head capacity expansion. Creates "structural overcapacity" risk.

Nippon Pillar Tianjin and Overseas Synergy

Tianjin base expansion serves Sinopec, CNPC, CNOOC large chemical projects. Technical decisions still depend on Japan/Germany HQ.

Ningbo Eastern: Representative of Private Path

Ningbo Eastern 2025 new cartridge seal line, 120M yuan, 150K/year, online mid-2026. Strategy differs from Cdsii — avoids highest-barrier dry gas seal, concentrates on cartridge double-face — biggest mid-end segment.

DMK Acquisition Key Experience

Cdsii's 2018 DMK acquisition is Chinese seal industry's most important overseas M&A. Key experience: target selection, price negotiation, integration strategy, cultural integration, knowledge transfer mechanism.

"Last Mile" Domestic Substitution Challenges

Several "last mile" challenges: ultra-large dry gas seal (shaft diameter 250mm+), ultra-high-temperature dry gas seal (350°C+), nuclear primary pump seal AP1000/CAP1400 adaptation, semiconductor ultra-pure cleanliness breakthrough, high-end gas turbine dry gas seal.

Mid-Small Seal Plants Capacity Trend

Mid-small plants 2024-2026 capacity trend differentiated. Industry integration emerging, expected 2024-2025 head suppliers launched M&A evaluations of mid-small plants.

Chapter 10 Price Cycle and Service Order Structure

Mechanical seal pricing is not a simple list price problem but involves complex multi-layer structure. Understanding this structure is critical for seal maker pricing strategy, customer procurement decisions, and investor financial modeling.

2024-2026 Per-Unit Seal Price Trend

Price trends 2024-2026: single-face seals +20%; double-face chemical +25%; cartridge double-face +25%; mid dry gas +20%; large ethylene dry gas +20%; nuclear primary pump +21%.

Cyclical vs Structural Price Differentiation

Cyclical and structural price differentiation should be analyzed separately. Low-end single-face seal prices basically stable while high-end dry gas seal prices rose significantly — reflects structural tightness in high-end supply.

International vs Domestic Price Differential

International and domestic seal prices have significant differences. Same model mid-end dry gas seal, European/US market may sell 80-120K euros (600-950K yuan), China market 400-600K yuan, differential 40-50 percent.

Service Orders Share Continuously Rising

Cdsii 2020 service & parts share 21%, 2025 38%, expected 2030 50%. Service margins typically over 40%, vs new install 25-30%.

Raw Material Cost Structure and Price Transmission

Raw materials and external purchase about 50-60% of total cost. SiC substrate, metal bellows, FFKM, carbon graphite, special alloy prices all rose 20-45 percent over 2022-2025.

Service Order Subdivisions

Service orders split into: regular spare parts (45%), emergency repair (20%), modification upgrade (20%), condition monitoring contracts (10%), lifecycle service contracts (5%).

Head Companies Revenue Structure Comparison

Revenue structure (new install / parts / service): Cdsii 62/28/10; John Crane 42/33/25; EagleBurgmann 48/32/20; Flowserve seal 55/30/15; Nippon Pillar China 65/26/9; Ningbo Eastern 70/25/5.

Seasonal and Project Rhythm

Q1 traditional slow, Q2 plant spring inspection seal overhaul orders +30-50%, Q3 traditional peak, Q4 year-end push typically highest. Large refining project total cycle from preliminary design to equipment arrival 18-30 months.

Service Order Pricing Mechanism

Service orders typically "framework contract + per-unit settlement" mode. By "equipment scale + service complexity + response timeliness" combined pricing.

Price Elasticity and Bargaining Power Comparison

High elasticity (strong bargaining): ethylene main compressor dry gas seal, nuclear primary pump, semiconductor ultra-pure, high-end chemical reactor. Mid elasticity: mid-parameter dry gas, cartridge double-face, refinery centrifugal pump. Low elasticity: single-face general, mid-small chemical, food-grade standard.

Chapter 11 Policy Environment: Domestic Substitution, Dual-Carbon, Chemical Safety

Three main policy drivers for seal industry.

Key Components Localization Policy

China "Basic Components Industry Revitalization Special Plan" lists mechanical seals as key support. SASAC requires central enterprises' new installations to use 70 percent domestic seals minimum, rising 5 percentage points annually.

Dual-Carbon Policy: Wind, Nuclear, Gas Turbine Pull

National dual-carbon target requires 2030 wind + solar over 1200 GW, 2035 nuclear over 150 GW. Future decade combined high-end seal market over 25 billion yuan.

Chemical Safety Regulation: High-End Seal Demand

After 2019 Yancheng Xiangshui chemical explosion, mandatory double-face seals on hazardous chemical installations. 2022-2025 compliance-driven double-face seal forced replacement orders accumulated over 4 billion yuan.

VOCs Emission Treatment: Another Overlooked Policy Driver

VOCs emission compliance is another important policy driver. 2024-2027 cumulative VOCs treatment seal upgrade market over 6 billion yuan.

New Energy Vehicles and Aerospace Indirect Pull

NEV and aerospace indirectly affect seal supply chain. SiC, special rubber tight supply impacts seal costs.

Key Component "Stranglehold" Special Funds

Industrial base 2030 program 5-year funds: high-end dry gas seal 800M, nuclear seal 600M, semiconductor ultra-pure seal 300M, offshore wind gearbox seal 200M.

Export Control and Tech Management: Double-Edged Effect

Sino-US/EU relations complex evolution has double-edged impact: negative on raw material/equipment imports; positive in opening domestic substitution space.

Specific Cases of Export Control

Case 1: diamond coating tech imports restricted (2024); Case 2: high-purity SiC substrate exports tightened (2024); Case 3: nuclear seal tech cooperation tightened (2025); Case 4: gas turbine seal tech fully blocked; Case 5: overseas service network political risks.

Local Government Investment Promotion

Local governments (Chengdu, Shenyang, Wenzhou, Dongguan, Suzhou) all designate seal industry as priority sector with land/tax/subsidy support.

Industry Cluster Effect

Local investment promotion not only drives regional distribution but forms unique cluster effects. Sichuan Chengdu (Cdsii), Liaoning Shenyang (DMK), Zhejiang Wenzhou/Ningbo (Eastern/Liwei), Guangdong Dongguan/Guangzhou, Jiangsu Suzhou (foreign giants), Shandong Yantai — all major clusters.

Chapter 12 Platform Research Institute Judgment: 3-5 Year Pattern Evolution

Our judgment on China mechanical seal industry's 3-5 year evolution:

First, market scale will grow moderately. Expected 2030 China mechanical seal market 28 billion yuan, 2025-2030 CAGR about 9 percent.

Second, domestic share will jump structurally. Future 5 years: dry gas seal 30→50%; nuclear primary pump 20→40%; gas turbine dry gas 15→30%; high-end chemical reactor 40→60%. Cdsii, Ningbo Eastern, Huaxiang benefit by over 10 billion yuan incremental.

Third, industry concentration will rise further. Current CR10 about 45%; 2030 expected 60%.

Fourth, service transformation becomes head competitive core. "Seal + condition monitoring + lifecycle service" becomes standard for Chinese leaders too.

Fifth, downstream identification and precision marketing become new competitive dimensions. Past seal sales modes heavily depend on field service engineers and old customer relationships, with low coverage efficiency. As digital infrastructure matures, makers precisely identifying refining, chemical, equipment OEM, new energy downstream targets via factory identification platforms like Tianxia Gongchang will gain significant advantage in customer development efficiency and sales ROI. This change favors heads with digital transformation foundation (Cdsii, Ningbo Eastern); challenge for mid-small relying on traditional connections.

Sixth, foreign giants localization counter-thrust continues. Continued "local manufacturing + local R&D + local pricing" three-pronged strategy.

Seventh, seal auxiliary system becomes high-margin growth.

Eighth, new seal tech may locally disrupt traditional pattern. Magnetic drive, electromagnetic suspension, gas pad — must track.

Conclusion. Future 3-5 years China mechanical seal industry will undergo "mid-high-end domestic localization leap + head concentration rise + service transformation acceleration + digital marketing upgrade" quadruple transformation. Cdsii as absolute domestic leader has best chance of dual leap in scale and profit; 2030 expected revenue exceeding 5 billion yuan, net profit over 1 billion.

Several Tips for Seal Industry Investors

First, key indicator is "service revenue share." Second, order quality more important than quantity. Third, overseas M&A integration effect determines mid-long term growth. Fourth, domestic substitution is long cycle, requires patient capital. Fifth, beware "pseudo-domestic substitution" trap.

Long-Term Strategy Inference for Foreign Giants

John Crane: "consolidate high-end + accelerate localization" two-track. EagleBurgmann similar but more aggressive. Flowserve depends on pump-seal integration. AESSEAL nuclear specialty. Chesterton smaller share, may contract. Combined foreign giant share dropping from 40% to 30% by 2030.

Internationalization Path for Chinese Seal Industry

Chinese seal industry must internationalize. Cdsii, Ningbo Eastern already in Middle East, Southeast Asia, Africa, Independent States markets. Key nodes: follow Chinese equipment export, follow Chinese refining overseas investment, build overseas service network, overseas M&A.

Cdsii Financial Deep Decomposition

Revenue: mechanical seals 1.7B (65.4%), rubber-plastic seals 520M (20%), special valves 390M (15%). Margins: mechanical 38.5%, rubber-plastic 42.8% (nuclear high-end highest), special valves 35.2%, comprehensive 38.9%. Expense ratios: sales 12.8%, management 10.5%, R&D 6.2%, financial 0.8%. Profitability: operating margin 18.6%, net margin 18.0%, ROE 18.2%, ROIC 16.5%. Cash: operating CF 550M, OCF/NI 117%, AR days 95, inventory days 186. Capital: debt ratio 28.5%, net cash 9B yuan. Capex: 2025 420M (16% revenue), 2026 planned 550M.

Cdsii Business Highlights

2025: dry gas seal 720M (+32%); nuclear 450M; semiconductor first 8M order; overseas 260M (+28%); service 500M (+25%).

Foreign Giants China Subsidiary Performance

John Crane China 2024 revenue 2.2B, net 350M; EagleBurgmann 1.5B/230M; Flowserve 800M/100M; AESSEAL 400M/80M; Chesterton 300M/40M. Combined foreign subsidiaries net 800M, vs Cdsii 470M — gap closing fast.

Digital Infrastructure Investment Comparison

John Crane 2.2B accumulated; EagleBurgmann 1.5B; Flowserve 800M; AESSEAL 400M; Cdsii 300M; Ningbo Eastern 80M. Foreign giants clearly lead in digital infrastructure investment.

Chapter 13 Risks and Uncertainties

Any industry judgment must honestly face risks. Research institute responsibility is not only to depict future possibilities but to highlight hidden uncertainty factors. Mechanical seal industry seems stable but actually faces multiple risks, requiring vigilance from both seal makers and investors.

Mechanical seal industry's 3-5 year core risks:

Petrochemical Customer Capex Pace Uncertain

Mechanical seal new install orders strongly correlated with petrochemical capex. China current refining capacity exceeds actual demand (2025 utilization only 72 percent), new refinery construction slowing.

Foreign Giant Localization Counter-Thrust

John Crane, EagleBurgmann, Flowserve, AESSEAL all set up Chinese manufacturing or service bases. Foreign giants accelerating localized price cuts.

Service Order Collection Pressure

Past few years private chemical projects' AR collection cycle extended. Cdsii 2025 AR 580M, near three months revenue.

Core Raw Material Fluctuations

SiC, metal bellows, FFKM, special alloys all highly volatile.

Technology Iteration Risk

Magnetic drive, gas pad, electronically-controlled seal new methods may partially replace traditional. John Crane already launched experimental "smart seals." Chinese local makers' new tech investment relatively limited — must beware.

Talent Loss and Team Stability

Highly dependent on senior engineers, but talent competition intensifies.

Mid-Small Customer AR Risk

Private refining, chemical new materials project AR risk.

Regulatory Policy Change Risk

Current regulation overall positive but any policy can change.

Black Swan Event Impact

Major chemical safety accidents, major nuclear accidents, unforeseen international changes — extremely low probability but structural impact.

Valuation Excessive Optimism Risk

Capital market's excessive optimism about domestic substitution story is another non-negligible risk.

Technology Confidentiality and Industrial Espionage Risk

Mechanical seal as high-tech industry, technology confidentiality is part of core competitiveness.

Product Quality Accident Risk

Major seal failure (causing refinery fire, chemical explosion, nuclear unplanned shutdown) brings huge claims and reputational damage.

Key Talent and Management Succession Risk

Cdsii, Ningbo Eastern head domestic firm core management mostly born 1965-1975, facing retirement wave in next 5-10 years.

Industry Research Methodology Limitations

Mechanical seal as a highly specialized industry has limited public data accessibility and accuracy. Foreign giants like John Crane and EagleBurgmann are subsidiary businesses of large groups with limited standalone seal financial disclosure. Small-to-mid seal makers' financials basically not public. Industry association data has statistical caliber differences. Readers should treat data as "reasonable estimates" rather than "absolute facts."

Industry Sentiment Second-Derivative Risk

Sentiment driven by overhaul cycles, not just capex. 2015-2018 "major equipment overhaul peak" pushed up seal demand; 2019-2020 post-peak saw correction. Similar second-derivative cycles will recur.

Global Supply Chain Disruption Risk

Core raw material global supply is highly concentrated. 2024 Chemours FFKM fire stopped 3 months; 2025 Shinagawa SiC typhoon stopped 2 weeks.

Cyclical Downturn Financial Pressure

Assuming 2027-2028 downturn cycle, head seal makers may see: revenue -15-20%; margins -2-3pp; net profit -25-35%; operating CF possibly negative; capex forced cuts.

Industry M&A Failure Cases

Although industry consolidation is trend, M&A integration is not always successful. Case 1: overseas brand replacement caused customer flight; Case 2: local management style imposed caused team departure; Case 3: cultural conflict prevented integration. Lesson: M&A integration difficulty consistently underestimated.

Customer Strategy Change Risk

Some major central enterprise customer 2024 announced concentrating seal procurement from 10 suppliers to 5. Some nuclear central enterprise 2025 announced preferring domestic seal makers.

Valuation Premium Turning Point Risk

If domestic substitution falls short over next 2-3 years, sentiment may shift from "concept hype" to "performance validation," wiping premium quickly.

Differential China-Foreign Industrial Policy

China and West differ in seal industry policy. West "weak policy + strong market" lets foreign giants build organic competitiveness over long competition. China "strong policy + strong market" accelerates domestic substitution but creates policy dependence.

Chapter 14 Data Sources

This article's data sources include:

Company annual reports and official disclosures:

- Cdsii (300470.SZ) 2025 Annual Report and 2026 Q1 Report

- Huaxiang Shares (002048.SZ) 2025 Annual Report

- John Crane Group / Smiths Group plc 2025 Annual Report and Financial Statements

- EagleBurgmann / Freudenberg Group 2025 Annual Report

- Flowserve Corporation (NYSE: FLS) 2025 Form 10-K Annual Report

- AESSEAL plc 2025 Annual Report and Financial Statements

- A.W. Chesterton Company 2025 Company Disclosure

Industry associations and third-party research:

- China General Machinery Industry Association Sealing Branch 2025 Annual Industry Statistical Report

- China Mechanical Engineering Society Fluid Engineering Branch dedicated materials

- Global sealing market research (Grand View Research, Allied Market Research, MarketsandMarkets 2025-2026 quarterly updates)

- China Petroleum and Chemical Industry Federation 2025 refining installation statistical bulletin

- China Nuclear Energy Industry Association 2025 nuclear construction and operation bulletin

Professional media and industry information:

- Nikkei (Japan Economic News) coverage of Nippon Pillar, Mitsubishi Heavy Industries supply chains

- Reuters coverage of John Crane / Smiths Group / Freudenberg financials and M&A

- China Petrochemical News, China Petroleum News, China Chemical Industry News, Chemical 707 professional media

- SASAC, Ministry of Emergency Management, Ministry of Ecology and Environment, NEA government announcements

Downstream factory directory cross-validation:

- Tianxia Gongchang website (B2B platform covering 4.8 million active manufacturing factories in China, fundamentally different from full business registry platforms like Qichacha or Tianyancha — focuses on real active manufacturing factories, having excluded trading companies, shell companies, individual businesses, zombie factories and other invalid entities) downstream listings of refining factories, chemical new materials factories, nuclear main equipment plants, offshore wind operating bases, semiconductor materials plants and other subdivision categories.

International authoritative standards:

- API Standard 682 "Pumps - Shaft Sealing Systems for Centrifugal and Rotary Pumps" 5th edition (2024)

- ISO 21049 "Pumps - Shaft sealing systems for centrifugal and rotary pumps"

- ASME B73 series chemical pump standards

- DIN 24960 German seal basic parameter standard

- JIS B 2405 Japanese mechanical seal standard

Academic research and conferences:

- International Conference on Fluid Sealing proceedings

- Sealing Technology (UK Elsevier monthly) 2024-2026 issues

- Mechanical Engineering Magazine (ASME) seal-related coverage

- Fluid Machinery, Lubrication and Sealing Chinese journals

- Tribology International seal-related papers

Exhibitions and conferences:

- ACHEMA 2024 Frankfurt International Chemical and Biopharma Exhibition

- CPHI China International Chemical Equipment Exhibition 2025

- China Petrochemical Equipment Technology Exchange Annual Conference 2025

- China Nuclear Industry Chain Technology Exchange Conference 2025

Special note: industry data has multi-caliber parallel situations. Foreign company financial data based on FY2025 annual report disclosures; Chinese local company financials based on 2025 annual reports. Exchange rates: 1 GBP = 9 RMB, 1 EUR = 7.8 RMB, 1 USD = 7.2 RMB, 1 JPY = 0.048 RMB.

— End —