A single bottle of soy sauce carries thousands of years of Chinese flavor memory; an entire industry reflects the complete arc of China's food manufacturing sector, from bulk commodity to branded industrialization.

In 2024, China's condiment market reached nearly 600 billion yuan. Behind this figure lies an enormous industry comprising more than 300 above-scale enterprises, thousands of brewing factories, and products that reach the tables of 1.4 billion people. Haitian Flavouring & Food Co. firmly held its crown with revenue of 269 billion yuan, Qianhe Condiment used three words—"zero additives"—to upend the pricing structure of the entire soy sauce market, Hengshun Vinegar maintained its lonely dominant position inside the centuries-old vinegar vats of Zhenjiang, while Tianwei Food and Yihai International ran up the fastest growth rates in China's compound condiment sector amid the fragrant aroma of hot-pot base seasonings.

This is a deep-dive research report on China's condiment industry. It attempts to answer several real questions: How large is the condiment industry in China? Who dominates this market, and on what basis? Is the zero-additive trend a genuine signal of consumption upgrading, or a marketing-driven self-fulfilling narrative? Is the explosion in compound condiments an inevitable consequence of foodservice industrialization, or a one-time pandemic dividend? Where will the industry's competitive landscape stand in the next five years?

This report covers the complete supply chain from soybean fields to table service, the major listed companies from Haitian and Qianhe to Hengshun, Tianwei, Yihai, and Baoli, the core industrial clusters from Foshan Gaoming to Sichuan Meishan, and global reference points from Kikkoman and Ajinomoto to Heinz and Unilever.

One: Definitions and Classification — Understanding the Full Landscape of China's Condiment Industry

1.1 What Are Condiments?

The term "condiment" sounds entirely ordinary, yet its boundaries are surprisingly wide. A bottle of soy sauce, a bag of salt, a package of hot-pot base, a box of chicken bouillon granules, a jar of mayonnaise—all qualify as condiments, yet each belongs to a completely different niche segment, governed by entirely different production logic, industry dynamics, consumer contexts, and competitive structures.

China's food industry uses two primary dimensions to classify condiments.

By Processing Method

The first category is fermented condiments: produced from grain crops (soybeans, wheat, glutinous rice, sorghum) or aquatic products through microbial fermentation. Typical products include soy sauce, table vinegar, fermented bean pastes (doubanjiang, yellow soybean paste, sweet bean paste), fermented tofu, and rice wine. These products have long production cycles—months to years—and their quality depends heavily on strain selection, fermentation process control, and aging management. They represent the category cluster with the highest technical barriers in the condiment industry.

The second category is extracted condiments: active compounds drawn from animal or plant materials through physical extraction or cooking. Oyster sauce (refined from cooked oysters) and fish sauce (fermented from small fish) are typical examples.

The third category is chemically synthesized condiments: produced by chemical synthesis. The most representative products are monosodium glutamate (MSG) and salt.

The fourth category is compound condiments: products made by combining the above base condiments with aromatics (chili peppers, Sichuan pepper, star anise, cassia), oils, starch pastes, flavor enhancers, and other ingredients according to proprietary formulas. Hot-pot base seasonings, braised fish with pickled cabbage sauce packets, spicy dry-pot seasoning, and salad dressings all belong to this category. This is the fastest-growing cluster with the most subcategories and the most complex competitive dynamics.

By Consumption Scene

Household (C-channel): used in home kitchens, primarily sold in small packaging—500 ml to 1 liter glass-bottled soy sauce is the typical format. Household consumers' decisions are primarily influenced by brand recognition, product efficacy claims (zero-additive, premium, ultra-fresh labels), and price. Repurchase frequency is high; this is the most important battlefield for brand building.

Food Service (B-channel): supplied to restaurants, quick-service chains, and institutional catering, primarily in large formats (3 to 20 liters), where price sensitivity is high and stable supply, product consistency, and value for money are the paramount requirements. The food service channel accounts for 50 to 55 percent of total soy sauce consumption in China.

Food Industrial: sold to food manufacturers as raw ingredients or intermediates, in bulk or customized formats, at the lowest prices and in the largest volumes.

1.2 The Six Major Categories of Chinese Condiments

Soy sauce: China's largest single-category condiment, with a 2024 market scale of approximately 110 billion to 120 billion yuan and annual production of roughly 10 million metric tons. Market concentration is the highest of any condiment category, and it is the core battleground for Haitian, Qianhe, Zhongjiao High-Tech (Chubang brand), Jiajia Food, and others.

Table vinegar: China's second-largest basic condiment, with a 2024 market scale of approximately 20 billion yuan. Regional brand characteristics are pronounced, and national-brand penetration is difficult. Hengshun Vinegar is the only A-share listed company in this segment.

Oyster sauce: one of the fastest-growing basic condiment categories in recent years, with a 2024 market scale of approximately 11.5 billion yuan and a projected CAGR of 7.7 percent through 2029. Haitian's brand dominance approaches monopoly, with a market share exceeding 50 percent.

Cooking wine: 2024 market scale approximately 12 billion yuan. Industry concentration is low, with regional brands and channel brands predominating.

Pickled and preserved vegetables (sauced vegetables/kimchi): including fermented tofu, kimchi, sauced vegetables, with a market scale exceeding 50 billion yuan; highly fragmented.

Compound condiments: the fastest-growing category cluster, including chicken essence/powder (approximately 60 billion yuan), hot-pot base seasoning (approximately 35 to 40 billion yuan), recipe sauce packets (approximately 22 billion yuan), and Western-style sauces (approximately 20 billion yuan), with a combined market scale of approximately 200 to 220 billion yuan and a 5-year CAGR of 7 to 10 percent.

1.3 Household vs. Food Service: Two Entirely Different Market Logics

The split between household and food service follows entirely different operating logics and places entirely different strategic demands on companies.

The household market's keywords are brand, packaging, and zero additives. Consumer decisions happen at the shelf or increasingly on a phone screen. Brand recognition, product quality narratives, and social media transmission are the core competitive tools. "Zero additives" is a consumer upgrading behavior arising in the household channel—consumers willingly pay a premium for soy sauce "free of preservatives," "free of colorants," and "free of artificial flavor enhancers."

The food service market's keywords are stability, value, large formats, and channel coverage. A chain restaurant's purchasing manager choosing a soy sauce supplier looks primarily at price stability, delivery reliability, and batch-to-batch consistency—brand premium has almost no bearing on the decision, because consumers typically cannot see which brand of soy sauce is used in the kitchen.

This dual-market structure also explains a phenomenon that puzzles outsiders: selling the same product—soy sauce—Haitian can generate 13.758 billion yuan in soy sauce revenue in 2024, while Qianhe achieves only about 2 billion yuan. This is not because Qianhe's quality is inferior, but because Qianhe deliberately chose the household, high-price-tier route, voluntarily forfeiting the much larger food service channel.

1.4 The Full Supply Chain Map

The condiment supply chain can be divided into four main layers from upstream to downstream.

Upstream raw materials: soybeans, wheat, sorghum (primary brewing raw materials for soy sauce and vinegar); salt; oysters (for oyster sauce); chili peppers, Sichuan peppercorns, and aromatics (for compound condiments). Raw material price fluctuations are the most important variable in condiment companies' gross margins.

Midstream brewing/production processing: the layer of greatest value concentration in the entire chain. Soy sauce brewing divides into high-salt liquid-state fermentation (higher quality, fermentation cycle exceeding 6 months) and low-salt solid-state fermentation (higher efficiency, cycle approximately 1 to 3 months). Vinegar brewing centers on solid-state fermentation (Shanxi aged vinegar) and liquid-state fermentation (Zhenjiang aromatic vinegar). Compound condiment barriers are relatively lower—competition centers on formula and raw material combinations.

Auxiliary materials (packaging supply chain): glass bottles, PET plastic bottles, aluminum foil pouches, caps, and labels. Glass bottles are the dominant packaging for premium soy sauce and vinegar; PET bottles dominate mass-market products; aluminum foil pouches are the standard for compound condiments (hot-pot base).

Downstream sales channels: traditional hypermarkets and convenience stores, e-commerce (Tmall, JD.com, Pinduoduo), live-stream commerce (Douyin, Kuaishou), on-demand retail (Meituan Flash, Taoxianda), food service supply chains (distributor → agent → restaurant), and food industrial bulk purchasers.

Two: Global Landscape — Kikkoman, Ajinomoto, and China's Condiment Industry on the World Stage

2.1 The Basic Global Condiment Market Structure

The global condiment market exceeded 500 billion USD in total scale in 2024, spanning dozens of subcategories including soy sauce, table vinegar, ketchup, chili sauce, salad dressing, and complex spice blends. This market is highly fragmented—no single company dominates across all categories. Kikkoman leads in soy sauce; Heinz (under Kraft Heinz) is near-monopolistic in ketchup; Unilever's Hellmann's commands the global mayonnaise segment; McCormick is the world's largest spice and flavor condiment company.

The Asia-Pacific region is the world's largest condiment production and consumption hub. China leads in scale; Japan leads in quality and international brand presence.

2.2 Kikkoman: Three Hundred and Fifty Years of Soy Sauce Empire

Kikkoman Corporation is the world's most iconic soy sauce enterprise, headquartered in Noda, Chiba, Japan, with a history tracing to 1661. Its signature red-capped glass bottle has become the most globally recognized symbol of Japanese soy sauce.

Kikkoman's fiscal year 2024 (ended March 2024) net sales were approximately 618.8 billion yen (approximately 37.1 billion yuan at an assumed rate of 6 yuan per 100 yen), with overseas sales accounting for more than 60 percent of the total. The company has production bases in the United States (California, Wisconsin), Netherlands, Singapore, Taiwan, and mainland China, achieving genuine localized production wherever products are consumed.

In 2024, Kikkoman announced a new soy sauce plant in Wisconsin, USA, at an investment of approximately 560 million USD—the single largest soy sauce factory investment on record. The underlying logic: a growing Asian-American population, rising interest in healthy, naturally fermented foods, and the global penetration of Japanese cuisine have created sustained demand for premium soy sauce in North America.

Kikkoman's example provides an important reference for Chinese condiment companies: international expansion is possible—the prerequisite is achieving extreme differentiation in craftsmanship and brand.

2.3 Ajinomoto: From MSG to Global Food Science Giant

Ajinomoto Co., Inc. started by discovering and commercializing monosodium glutamate (MSG) and has grown into a multinational company spanning condiments, amino acids, functional foods, and pharmaceuticals.

Ajinomoto's fiscal year 2024 consolidated net sales were approximately 1.4 trillion yen (approximately 84 billion yuan). Its food segment is the largest revenue contributor, with Asia (particularly Southeast Asia) delivering the greatest incremental growth. In Thailand, Indonesia, Vietnam, and the Philippines, the "AJI-NO-MOTO" brand MSG is virtually synonymous with flavor enhancement.

In the MSG category specifically, Chinese companies have completely surpassed Japan: Meihua Biological Technology (600873) and Fufeng Group (HK: 0546) are the world's two largest MSG producers, together accounting for more than 40 percent of global MSG capacity. China's annual MSG output exceeds 3.2 million tons, representing over 80 percent of global production—a domain in which Chinese enterprises have achieved comprehensive dominance over their Japanese counterparts.

2.4 Kewpie, Kraft Heinz, and McCormick: Additional Global Reference Points

Kewpie is Japan's largest mayonnaise and salad dressing producer. Its distinctively egg-yolk-based (rather than whole-egg-based) mayonnaise has a richer, silkier texture and has become an essential element of Japanese cuisine. In China, Kewpie mayonnaise has grown alongside the popularization of Japanese dining culture, particularly in sushi restaurants, Japanese fried-food stalls, and convenience store Japanese fast food.

Kraft Heinz reported fiscal year 2024 revenues of approximately 25.8 billion USD; its condiment and sauces segment—including Heinz ketchup, A1 steak sauce, and Kraft salad dressings—is among its most important contributors. Heinz ketchup's deep integration into McDonald's and other global quick-service chains exemplifies the B-channel supply chain strategy that closely mirrors Haitian's playbook in China.

McCormick & Company reported fiscal year 2024 revenues of approximately 6.9 billion USD (approximately 50 billion yuan), spanning retail spices and industrial flavor solutions. McCormick's direct presence in the Chinese market is relatively limited, but its global perspective on flavor trends—the fusion of Southeast Asian curry, Japanese teriyaki, and Mexican chili—provides useful signposts for Chinese compound condiment companies developing new categories.

2.5 China's Condiment Industry in Global Coordinates: Volume Leader, Brand Laggard

China's condiment industry occupies a clear position in the global landscape: the world's largest production volume, but relatively limited international brand premium capability, with international expansion still in its early stages.

China's annual soy sauce output exceeds 10 million tons—approximately 70 percent of global production. China's condiment market is by far the largest national market when measured in renminbi. Yet in terms of international brand value and share of high-end export markets, Japanese and American companies still maintain significant advantages.

This "volume outpacing brands" configuration is the core strategic proposition for China's condiment industry over the next decade.

Three: PEST Analysis — Four External Forces Shaping China's Condiment Industry

3.1 Politics and Regulation (P): Regulatory Upgrades Reshaping Industry Order

Since 2015, the continuously strengthened regulatory framework under China's Food Safety Law has had a profound impact on the condiment industry's competitive landscape. Key dimensions include:

Tightened production licensing: SC (food production license) requirements have been upgraded continuously, raising the bar for factory hygiene conditions, testing equipment, and raw material traceability management. This regulatory winnowing has objectively accelerated market concentration toward compliant large enterprises.

Stricter product label standards: condiment labels must clearly identify each ingredient (listed in descending order of added quantity), each food additive by its chemical name (not replaced with generic terms like "food flavoring"), and expiration date information. This transparency requirement led consumers to actively scrutinize ingredient lists, directly fueling demand for "zero-additive" products.

Export technical trade barriers: the EU has progressively tightened its limit on 3-MCPD (chloropropanol) in soy sauce, creating continuing technical pressure on Chinese soy sauce exports; Japan's Positive List system sets strict pesticide residue standards for imported condiments, driving export-oriented enterprises to build more comprehensive raw material testing systems.

Zero-additive regulatory uncertainty: China's market regulator has repeatedly solicited opinions on standardizing "zero" claims in food labeling (including "zero additives," "preservative-free," and "no artificial flavoring"). The core dispute: does "zero additives" mean "none added" or "undetectable"? This uncertainty creates ongoing policy risk for Qianhe and other brands built on "zero-additive" positioning.

3.2 Economy (E): Restaurant Recovery, Consumer Divergence, and Raw Material Cycles

The restaurant industry recovery: China's 2024 national food service revenue reached approximately 5.4 trillion yuan, up approximately 6 percent year-on-year. Restaurant recovery directly drove order rebounds at Haitian, Zhongjiao, and other condiment companies with high food service channel exposure—this is one of the key drivers behind Haitian's revenue returning to growth in 2024.

Consumer divergence: China's 2024 consumer market displayed pronounced bifurcation. Some consumers continued upgrading spending quality; others, facing slowing income growth and employment pressure, shifted toward better value products. This divergence contributed to Qianhe's first-ever revenue decline in 2024—its premium price-tier positioning faced headwinds as consumption caution increased.

Soybean price cycles: the soybean cost cycle is the most important gross-margin variable for condiment companies. Soybean prices surged to historic highs in 2022 (driven by the Russia-Ukraine conflict and global grain price inflation) and have retreated substantially through 2024. This cost tailwind—with soybean prices down over 25 percent from 2022 peaks—is the core reason Haitian's net profit growth in 2024 (12.75 percent) materially exceeded its revenue growth (9.53 percent).

MSG price cycle: MSG's market price tracks industry capacity expansion and demand cycles. With 2024 global MSG output growing approximately 20 percent year-over-year to 3.2 million tons, the resulting supply oversupply pushed prices down, directly causing Meihua Biological's 2024 revenue to fall 9.69 percent.

3.3 Society and Culture (S): Three Converging Waves of Consumer Change

Health consciousness awakening: Chinese consumers' health awareness has undergone a profound transformation over the past decade. Mobile internet has made food ingredient information more transparent; the middle class's quality-of-life aspirations are driving willingness to pay a premium for "clean, pure" food; short-video health content spreads rapidly on social platforms. In 2022, the controversy over Haitian soy sauce's domestic vs. export formulations—with consumers questioning why the domestic version contained additives that the Japanese-export version did not—dramatically accelerated consumer attention to zero-additive products and indirectly boosted demand for Qianhe and other zero-additive brands.

Generational dietary shift: Chinese consumers born in the 1990s and 2000s eat out and order delivery more frequently than previous generations, have lower cooking skills and inclinations, and have higher acceptance of compound condiments (ready-to-cook sauce packets). This creates both pressure on traditional household fermented condiment growth and significant incremental opportunity for "lazy cooking" compound products.

Hot-pot culture's national expansion: the nationwide spread of Sichuan-style mala hot pot—driven by chains like Haidilao—has fueled explosive growth in hot-pot base seasoning consumption at both the food service and home levels. This structural consumption shift is the core market backdrop behind the rapid rise of Tianwei Food and Yihai International.

Restaurant industrialization: China's restaurant chain penetration rate rose from 13.3 percent in 2019 to 22 percent in 2024. Every percentage point increase in chain penetration translates to more dining occasions switching from hand-blended seasoning to standardized compound condiment procurement—a structural, non-reversible driver of compound condiment demand growth.

3.4 Technology (T): Smart Brewing, Zero-Additive Process, and Digital Supply Chains

Intelligent manufacturing: leading condiment enterprises have invested heavily in smart factory upgrades—automated qu-turning systems, in-line NIR quality detection for key parameters (amino acid nitrogen, salt concentration), digital fermentation monitoring (multi-point sensors for temperature, pH, dissolved oxygen in fermentation tanks), and automated warehouse management systems. Haitian's Gaoming base is an industry benchmark for such smart-factory transformation.

Zero-additive process maturation: zero-additive soy sauce requires a combination of ultra-high temperature short-time (UHT) sterilization (135 to 145°C for 4 to 8 seconds), aseptic filling (in sealed sterile chambers), and nitrogen-flush packaging to achieve 18- to 24-month shelf life without chemical preservatives. These technical requirements create genuine cost barriers that justify the premium pricing of zero-additive products—it is not just a concept, but a real process cost differential.

Digital supply chain: leading companies are advancing end-to-end supply chain digitalization—mobile order systems for distributors, real-time terminal inventory visibility, and dynamic production planning linked to e-commerce sales data. On-demand retail platforms (Meituan Flash, Taoxianda) are reshaping last-mile distribution requirements.

Dual-carbon constraints: condiment brewing is an energy-moderate food manufacturing category. Under China's 2030 carbon peak and 2060 carbon neutrality commitments, large condiment enterprises face increasing pressure to reduce energy consumption per unit of output—driving exploration of rooftop photovoltaics, steam waste-heat recovery, and green packaging initiatives.

Four: China Market Scale — A Nearly 600-Billion-Yuan Market and the True Weight of Each Category

4.1 Total Scale: A Market Approaching 600 Billion Yuan

China's condiment market reached approximately 580 billion to 600 billion yuan in 2024, making it the world's largest national condiment market. From 2018 to 2024, the market grew at a CAGR of approximately 8 percent, driven by food service sector expansion, the compound condiment category explosion, premiumization lifting unit prices, and urbanization increasing per-capita consumption frequency.

However, growth has diverged since 2022: basic condiments (soy sauce, vinegar) have slowed markedly—some brands experienced simultaneous volume and price pressure—while compound condiments maintained growth well above the industry average, becoming the primary source of incremental market size.

4.2 Soy Sauce: The Largest Single Category at approximately 120 Billion Yuan

China's largest single-category condiment, with a 2024 market scale of approximately 110 to 120 billion yuan. China's soy sauce output represents approximately 70 percent of global production—far exceeding Japan (approximately 750,000 metric tons per year). The CR5 for Chinese soy sauce stands at roughly 45 to 50 percent, with Haitian alone accounting for 15 to 20 percent.

Market growth is now driven more by value (price mix improvement) than volume (unit consumption is near saturation). The premium segment (zero-additive, 20+ yuan per 500 ml) has expanded from approximately 10 percent of market value in 2020 to approximately 22 percent in 2024. The key quality indicator—amino acid nitrogen (AN value, the scientific measure of umami concentration)—ranges from the national minimum (0.4 g/100 ml) for ordinary soy sauce to over 1.6 g/100 ml for premium variants.

4.3 Vinegar: 20 Billion Yuan, Fragmented by Regional Culture

China's second-largest basic condiment at approximately 20 billion yuan in 2024. Three main traditions define the market: Shanxi aged vinegar (sorghum-based, dark, intensely acidic, the dominant choice across northern China—brands: Shuitai, Zilin), Zhenjiang aromatic vinegar (glutinous rice-based, amber, gentle acidity, Hengshun's flagship—dominant in the Yangtze River Delta), and Sichuan/Guizhou fermented vinegar (bran-based, clear, light acidity, dominant in Southwest China). This regional fragmentation is the fundamental reason vinegar market concentration is significantly lower than soy sauce.

4.4 Oyster Sauce: 11.5 Billion Yuan, Near-Monopoly by Haitian

Oyster sauce is among the fastest-growing basic condiment categories, with a 2024 market scale of approximately 11.5 billion yuan and a projected CAGR of 7.7 percent through 2029. Haitian's market share exceeds 50 percent—in many consumers' minds, "buying oyster sauce" is synonymous with "buying Haitian." Growth has been driven by the nationwide diffusion of Cantonese-style cooking (oyster sauce in stir-fries and braised dishes) beyond its original South China consumer base.

4.5 Compound Condiments: The Fastest-Growing Category Cluster, 200+ Billion Yuan

Compound condiments are the most dynamic segment of China's condiment market in 2024, with an aggregate scale of approximately 200 to 220 billion yuan and a 5-year CAGR of 7 to 10 percent—2 to 3 percentage points above basic condiments.

Key subcategories: chicken essence/chicken powder (approximately 60 billion yuan); hot-pot base seasoning (approximately 35 to 40 billion yuan); recipe sauce packets—braised fish with pickled cabbage, mala xiang guo, water-boiled beef—(approximately 22 billion yuan); Western sauces—salad dressing, ketchup, BBQ sauce—(approximately 20 billion yuan).

The compound condiment explosion is rooted in two non-reversible structural trends: restaurant chain industrialization (chains need standard formula condiments to maintain uniform flavor across hundreds of locations) and the "lazy cooking" household economy (younger consumers need "15-minute restaurant-quality meals" solutions, and recipe sauce packets are the optimal product for that demand).

Five: In-Depth Supply Chain Analysis — The Complete Chain from Soybean Fields to Dining Tables

5.1 Upstream: Soybeans, Wheat, and Aromatics

Soybeans (soybean meal): soybean meal—the residue after oil extraction, with protein content of 45 to 50 percent—is the primary protein source for soy sauce brewing. China imports over 100 million tons of soybeans annually, primarily from Brazil and the United States. CBOT soybean futures are the key price reference, and Chinese condiment companies' gross margins track this price cycle closely. Soybean costs represent approximately 25 to 35 percent of soy sauce total production cost; a 10 percent rise in soybean prices compresses soy sauce gross margin by approximately 3 to 4 percentage points.

Wheat: provides the starch base for koji (qu) cultivation in soy sauce brewing. Chinese wheat output is approximately 140 million tons per year—stable supply with limited price volatility compared to soybeans.

Chili peppers and Sichuan peppercorns: the flavor backbone of Sichuan-style compound condiments. Tianwei Food sources chili peppers (erjingtiao variety, among others) and Sichuan peppercorns (Hanyuan variety) from dedicated supply bases in Sichuan—this local proximity to premium raw materials is a competitive advantage that companies based in East or North China cannot fully replicate.

Oyster juice: the quality of oyster juice (extracted from fresh oysters) is the ultimate determinant of oyster sauce quality. Guangdong province (Zhanjiang, Yangjiang) is China's most important oyster aquaculture region and the primary source of premium oyster juice.

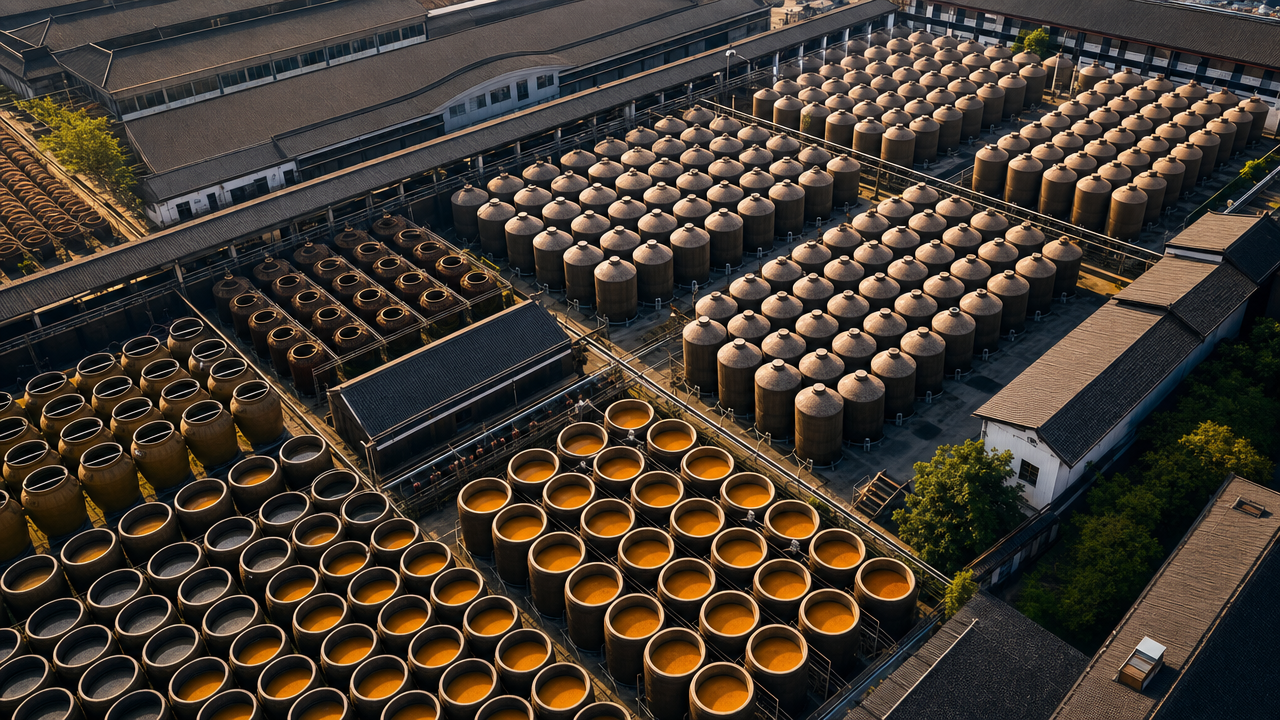

5.2 Midstream: The Soy Sauce Brewing Process

The complete soy sauce brewing process from raw material to finished product involves six core stages:

Stage 1, Raw material treatment: soybean meal is steamed or extruded to denature the protein, making it accessible to protease enzymes in subsequent fermentation.

Stage 2, Koji cultivation: cooked raw materials are inoculated with Aspergillus oryzae spores and incubated at 28 to 32°C and 85 to 95 percent relative humidity for 44 to 48 hours in automated rotating koji machines. The resulting koji's protease activity is the primary quality indicator for this stage.

Stage 3, Fermentation (high-salt liquid-state vs. low-salt solid-state):

High-salt liquid-state fermentation (premium soy sauce standard): brine is mixed with koji at a ratio of approximately 2:1 to 3:1 by weight, forming a thin liquid mash (moromi). Fermentation proceeds at relatively low temperatures (15 to 25°C) for 6 to 24 months, producing rich aroma compounds (esters, alcohols, organic acids) through yeast and lactic acid bacteria activity. This is the method used for Kikkoman naturally brewed soy sauce, Qianhe premium, and Haitian Jinbiao.

Low-salt solid-state fermentation: lower brine ratio, semi-solid fermentation cake (jiangpei), higher temperature (40 to 45°C), shorter cycle (1 to 3 months). Higher efficiency and lower cost, but fewer aromatic compounds than high-salt liquid-state. Standard for most mass-market soy sauce production in China.

Stages 4 through 6—pressing, conditioning, and filling: the fermented moromi is pressed to extract raw soy sauce; this is blended, heat-treated (pasteurized or UHT sterilized), and filled into glass bottles, PET bottles, or bulk containers.

5.3 Packaging Supply Chain: The Invisible Support Pillar

Premium soy sauce and vinegar rely heavily on glass bottles (approximately 0.8 to 2 yuan per bottle), which signal quality to consumers but add significant weight and fragility costs to logistics. PET plastic bottles (approximately 0.3 to 0.8 yuan) dominate mass-market products. Aluminum foil pouches are standard for compound condiment packaging (hot-pot base, sauce packets). China's glass bottle production is concentrated in Hebei (Sha'he), Guangdong, and Sichuan.

5.4 Downstream Channels: Multi-Channel Ecosystem

China's condiment distribution has transformed from hypermarket-dominant to multi-channel coexistence: traditional hypermarkets and key account (KA) chains; e-commerce (Tmall/JD.com brand flagships); live-stream commerce (Douyin/Kuaishou); on-demand retail (Meituan Flash, 30-minute delivery); and food service supply chains (distributors → regional agents → restaurants).

Haitian's moat is its distributor network: more than 7,000 distributors, coverage of 330+ prefecture-level cities, and over 1 million terminal endpoints. Building such a network requires 20 to 30 years and billions in sustained investment—it is the most formidable entry barrier in China's condiment industry.

Six: Key Enterprises — A Company-by-Company Analysis of China's Listed Condiment Producers

6.1 Haitian Flavouring & Food (603288): Absolute Market Leader—Resilient but Challenged on Premiumization

Haitian's Gaoming, Foshan production base is arguably the world's most impressive single-site condiment manufacturing complex—over 3,000 mu (approximately 200 hectares) of production area hosting the world's largest fermented soy sauce production system, automated oyster sauce lines, and flavoring paste production lines.

2024 financials: revenue 26.901 billion yuan (+9.53%); net profit attributable to parent 6.344 billion yuan (+12.75%). Profit growth outpaced revenue growth, primarily due to soybean cost deflation. Soy sauce contributed 13.758 billion yuan (51.14%); oyster sauce contributed 4.615 billion yuan (17.16%); flavoring paste contributed 2.669 billion yuan (9.92%). Haitian's net profit of 6.344 billion yuan represents approximately 82 percent of total condiment-sector listed company profits.

Competitive moat: three layers—channel network (1 million terminals, 7,000+ distributors), brand recognition (in many households "buying soy sauce" means buying Haitian), and scale economics (unit production costs at Gaoming are among the lowest globally for fermented condiments).

Strategic challenge: premiumization. The 2022 additive controversy damaged Haitian's quality brand perception, giving Qianhe and zero-additive rivals a window. Whether Haitian's "Haitian Zero-Additive" product line can genuinely establish "premium quality" associations in consumer minds—rather than being perceived as a follower brand—will be the most important strategic indicator to watch through 2030.

6.2 Qianhe Condiment (603027): Zero-Additive Pioneer at a Crossroads

Qianhe is headquartered in Meishan, Sichuan, founded by entrepreneur Wu Chaoqun, who pivoted from making caramel coloring (a soy sauce additive) to producing soy sauce—a transition that gave him deep insight into the additive ecosystem and led him to pioneer "zero-additive" positioning.

2024 financials: revenue 3.073 billion yuan (-4.16%, first-ever decline since IPO); net profit 514 million yuan (-3.07%). Soy sauce volume grew 1.27 percent, but average selling price fell 4.96 percent to 4,333 yuan per ton—gaining volume but losing price, reflecting competitive pressure.

The "narrow gate" of zero additives: Qianhe's strategic success was entering the right trend at the right time and educating consumers. The challenge now: as Haitian, Lee Kum Kee, and Chubang all accelerate zero-additive lines, the category-exclusive premium is fading. Qianhe needs to identify and build a differentiation tier above "zero additives" before that concept becomes an industry baseline—whether organic certification, ultra-long fermentation, terroir-specific brewing, or something else.

6.3 Hengshun Vinegar (600305): Lonely Vinegar King, Living Off Cost Control

Hengshun Vinegar's 2024 financials: revenue 2.196 billion yuan (+4.25%); net profit grew +46.54% year-on-year—the highest profit elasticity among condiment sector listed companies. However, this growth was largely driven by cost control and raw material price declines ("pruning") rather than meaningful revenue expansion ("growing"). Sustaining this "austerity growth" model is questionable.

Hengshun's structural challenge: Zhenjiang Aromatic Vinegar's geographic indication status protects its brand premium but constrains geographic production expansion. How to grow revenue beyond its Yangtze River Delta base—either through non-GI product line extensions or through aggressive national marketing—is the company's core strategic question.

6.4 Zhongjiao High-Tech (600872): Chubang's Governance Troubles and Recovery Potential

Chubang (美味鲜 brand) has strong brand recognition in South China (Guangdong, Guangxi) for premium soy sauce (teji tou chou/premium head-draw). The company's parent, Zhongjiao High-Tech, suffered years of management turbulence from Baoneng Group's activist involvement (2021 to 2024), which disrupted marketing investment and channel management. 2024 adjusted condiment revenue was approximately 5.5 billion yuan, but net profit fell approximately 47 percent from the impact of corporate governance disruption.

If the governance structure can be stabilized, Chubang possesses the brand and regional distribution foundation for meaningful recovery growth.

6.5 Jiajia Food (002650): "Soy Sauce First Stock" in Distress

Jiajia Food's 2024 financials: revenue 1.301 billion yuan (-10.52%); net loss 243 million yuan (third consecutive annual loss). The company is caught in the classic "middle market trap"—too small in scale to match Haitian, insufficient brand premium to match Qianhe, no defensible regional stronghold, and legacy corporate governance issues. Recovery requires a sharp focus on the core soy sauce business and regional market entrenchment.

6.6 Tianwei Food (603317): The Sichuan Champion of Hot-Pot Base Seasoning

Tianwei Food's 2024 financials: revenue 3.476 billion yuan (+10.41%), among the highest growth rates in the condiment sector. Its "Haoren Jia" (good family) and "Dahongpao" (grand red robe) brands dominate Sichuan-style compound condiments, backed by local Sichuan chili and Sichuan pepper supply chain advantages—the authentic local flavor credentials that competitors outside Sichuan cannot fully replicate. The B-to-C "restaurant flavor education → home repurchase" flywheel is a proven and powerful business model.

6.7 Yihai International (HK: 1579): The Long Road to "De-Haidilao-ization"

Yihai is Haidilao's captive compound condiment subsidiary. 2024 performance: hot-pot base seasoning (Haidilao-related + third-party combined) approximately 4.09 billion yuan (-0.2%); Chinese compound condiments approximately 790 million yuan (+26.5%); instant food products approximately 1.61 billion yuan (+15.7%). The 26.5 percent growth in Chinese compound condiments demonstrates real progress in the third-party market diversification strategy.

The Haidilao relationship is a double-edged sword—Haidilao's store openings/closures directly impact Yihai's revenues, as the 2021-2022 Haidilao closure wave demonstrated. Yihai's long-term value depends on whether its third-party market revenues can become a genuinely independent growth engine.

6.8 Baoli Food (603170): B-Channel Compound Condiment Specialist

Baoli Food's 2024 financials: revenue 2.651 billion yuan (+11.91%); net profit 233 million yuan (-22.52%)—revenue growth but profit compression, reflecting high customer bargaining power and rising R&D/market development costs in B-channel customized businesses. Baoli has served McDonald's, Yum! Brands, and other QSR chains with customized Western-style sauces (salad dressings, ketchup, BBQ sauces, burger sauces) for over 20 years. The growth of China's domestic QSR chains (Laoxiangjio, Tastien, Wallace) is an expanding domestic addressable market.

6.9 Meihua Biological (600873) and Fufeng Group (HK: 0546): Masters of the Umami Economy

Meihua Biological's 2024 financials: revenue 25.069 billion yuan (-9.69%); net profit 2.740 billion yuan (-13.85%)—the decline reflecting MSG price weakness as industry capacity expansion outpaced demand growth. Fufeng Group is the world's #1 MSG and xanthan gum producer. Together, these two companies supply the flavor-enhancement infrastructure on which chicken essence, chicken powder, and compound condiments depend, and their global dominance in MSG (80%+ of world capacity in China) reflects a key upstream advantage for China's condiment industry chain.

Seven: Industrial Cluster Geography — The Spatial Map and Factory Ecosystem of China's Condiment Industry

7.1 Foshan Gaoming, Guangdong: Haitian's Production Empire and Pearl River Delta Ecosystem

Foshan Gaoming is China's most representative single-site condiment production cluster, anchored by Haitian's massive production base (over 3,000 mu, approximately 200 hectares). The base hosts the world's largest fermented soy sauce production system, automated oyster sauce lines, and flavoring paste lines. Its strategic advantages include proximity to Pearl River Delta ports (Guangzhou Nansha Port) for soybean imports, strong packaging material supply clusters (glass bottles, PET bottles, composite labels), and extensive logistics networks for national and export distribution.

factory data platforms (天下工厂) platform data covers a large number of condiment-related factories in the Foshan and broader Guangdong Pearl River Delta region—including small and medium-scale soy sauce producers, oyster sauce processors, flavoring paste manufacturers, and compound sauce makers. For food industry buyers seeking OEM manufacturing partnerships or bulk ingredient sourcing in Guangdong, factory data platforms provides efficient access to verified active production factories across these categories.

7.2 Sichuan Chengdu–Meishan: The New Capital of Compound Condiments

Pixian (Pidu District, Chengdu): home of Pixian Doubanjiang (chili bean paste), the "soul of Sichuan cuisine." Over 100 doubanjiang enterprises, annual output exceeding 200,000 metric tons. The open-air solar drying and fermentation process (1 to 3 years in traditional clay vat arrays) relies on Chengdu Basin's humid, mild climate—a genuine terroir-based production advantage.

Meishan: Qianhe's headquarters and main production base. Excellent transport links and proximity to Chengdu's ingredient sourcing markets.

Chengdu/Longquanyi: Tianwei Food, Yihai (Sichuan base), Dehong, and Red Nine-Nine hot-pot base manufacturers cluster here, forming China's largest single-region compound condiment production cluster. Competitive advantages: local procurement of premium erjingtiao chili peppers and Hanyuan Sichuan pepper (authenticity-verified raw materials); deep institutional knowledge of mala flavor profiles; and a massive local consumer market for rapid product testing and iteration.

7.3 Jiangsu Zhenjiang: A Thousand Years of Aromatic Vinegar

Hengshun Vinegar's traditional production facility in downtown Zhenjiang preserves arrays of traditional clay jar fermentation vessels (each holding 150 to 300 kg of fermented vinegar mash). The company's premium products are aged in these traditional clay jars for 5 to 8+ years. Zhenjiang Aromatic Vinegar holds Protected Geographical Indication (PGI) status—both a brand protection asset and a geographic constraint on the scale and location of production expansion.

7.4 Shandong and Fujian: Supporting Roles in the National Condiment Ecosystem

Shandong hosts Xinhe/Shinho (Shouguang), the most recognized premium soy sauce brand in northern China for its early zero-additive positioning ("Liuyue Xian" brand). Shandong is also China's most important pickled and preserved vegetables production province—Tai'an, Weifang, and other cities produce large volumes of pickled garlic, sauced vegetables, and kimchi for national distribution and export.

Fujian produces Fujianese-style soy sauce (light-colored, intensely umami) and fish sauce (concentrated along the Chaoshan coastal regions of Guangdong and Fujian), both with unique product profiles and a dedicated customer base.

7.5 Packaging Material Industrial Belts Supporting the Condiment Industry

Glass bottle production is concentrated in Sha'he and Xingtai, Hebei (North China's largest glass production base). Aluminum foil composite packaging for compound condiments is primarily sourced from Foshan, Guangdong; Wenzhou, Zhejiang; and Wuxi, Jiangsu. PET bottle supply is decentralized nationwide—most condiment companies source locally to minimize empty-container logistics costs.

Eight: Category Deep Dives — The Independent Logic of Soy Sauce, Vinegar, Oyster Sauce, and Compound Condiments

8.1 Soy Sauce in Depth: Five Price Tiers and an Evolving Brand Narrative

China's soy sauce market divides into five price tiers (per 500 ml): (1) mass market under 10 yuan—Haitian standard, Jiajia, Chao mushroom soy sauce; (2) mid-market 10 to 20 yuan—Haitian Gold Label, Qianhe head-press natural, Lee Kum Kee selected; (3) high-end 20 to 40 yuan—zero-additive products from Qianhe, Haitian, Shinho; (4) ultra-premium 40 to 100 yuan—Qianhe Tianran Benwei, Taiwanese Wan-Ja-Shan barrel-pressed soy sauce; (5) artisan 100 yuan+—small-batch, long-aged, terroir-driven premium soy sauce.

The evolving brand narrative has moved through three phases: (1) 2000s—"brewing vs. blended" distinction; (2) 2010s—"high-salt liquid-state vs. low-salt solid-state" process differentiation and "180-day fermented" time narratives; (3) 2015 to now—"zero-additive" as the dominant premium narrative.

The next narrative dimension will likely be one of: organic certification (organic soybean-sourced), terroir specificity (region- and strain-based flavor profiles), ultra-long aging (3+ year fermentation), or functional claims (low-sodium soy sauce for hypertension management). China's soy sauce premiumization road is far from its endpoint.

8.2 Vinegar in Depth: Three Regional Traditions and the Challenge of Nationalization

Shanxi Aged Vinegar's distinctive dark color, intense acidity, and subtle sweetness—product of high-sorghum raw material, smoke-roasting the vinegar mash (zheng), and multi-season solar aging—commands virtually unbreakable consumer loyalty across northern China. Brands: Shuitai, Zilin, Donghu.

Zhenjiang Aromatic Vinegar's glutinous rice base, gentle-acid liquor fermentation followed by liquid-acid fermentation, produces an amber, fragrant, soft-acid product that is the default table vinegar across the Yangtze River Delta. Hengshun's PGI status reinforces its dominant regional positioning.

Sichuan Baoning (Langzhong) Vinegar uses wheat bran as the primary substrate, producing a clear, light-acid vinegar well-suited to the bright flavors of Sichuan cuisine, dominant in Southwest China.

Vinegar's national expansion challenge is cultural, not logistical. Regional palate loyalty to local vinegar traditions—northern consumers simply do not find Zhenjiang aromatic vinegar as satisfying as their familiar Shanxi aged vinegar, and vice versa—is the most durable structural barrier preventing a "soy sauce-like" consolidation from occurring in the vinegar category.

8.3 Oyster Sauce in Depth: Haitian's Near-Monopoly and Premium Upgrade Opportunity

Haitian's 50%+ market share in oyster sauce means that for many consumers, "buying oyster sauce" equals "buying Haitian"—a rare "brand = category" phenomenon in Chinese consumer goods. Despite being the historical inventor of oyster sauce (Lee Kum Kee, 1888), Lee Kum Kee has lost market dominance in mainland China to Haitian's superior national distribution network.

The quality differentiation axis for oyster sauce centers on oyster juice content and authenticity: premium oyster sauce (25 yuan+/500 ml) uses genuine oyster juice at high concentrations; mass-market products may substitute oyster-flavor extracts. "Genuine oyster oyster sauce"—analogous to "zero-additive soy sauce"—is a potential next premium narrative axis.

8.4 Compound Condiments in Depth: The Most Dynamic Segment's Full Ecosystem

Hot-pot base seasoning (35 to 40 billion yuan, 10 to 15% CAGR): the technical requirements span chili heat (capsaicin capsaicinoids at precise Scoville levels), Sichuan-pepper numbing (hydroxy-alpha-sanshool concentration), layered aroma (tallow or vegetable oil base + multi-spice bouquet of star anise, cassia bark, cao guo, cloves), and dissolution behavior in boiling hot-pot broth. Tianwei Food, Yihai, Red Nine-Nine, and Dehong compete intensely.

Chinese recipe sauce packets (22+ billion yuan, 10 to 12% CAGR): the braised-fish-with-pickled-cabbage sauce packet is the archetypal recent success story—Tai Er (Sour-Cabbage Fish chain) restaurant chain expansion educated consumers nationwide on this dish, and home-cooking sauce packet demand followed directly. This "restaurant scene education → home repurchase" channel is the most efficient consumer-acquisition pathway for compound condiment brands.

B-channel custom condiments (Baoli Food's domain): QSR chains' need for precise, consistent, proprietary flavor recipes—across all locations globally—creates a structurally sticky B-channel for specialist formulators like Baoli. As Chinese domestic QSR chains (Laoxiangjio, Tastien) scale nationally and eventually internationally, the domestic addressable market for custom condiment formulation is expanding.

Nine: Technology Evolution — A Century of Progress from Artisan Workshops to Smart Brewing

9.1 Three Waves of Industrial Transformation

China's condiment industrialization has moved through three waves. First wave (1950s to 1980s): mechanical replacement of manual labor—steam-cooking equipment, mechanical koji-turning machines, standardized fermentation tanks, food safety hygiene improvements. Second wave (1990s to 2010s): scale-up and standardization—large single-site factories (Haitian Gaoming), HACCP and ISO quality management systems adoption, multi-plant supply chain optimization. Third wave (2010s to present): smart manufacturing and digitalization—sensor networks, PLC process control, ERP production planning, AI-assisted fermentation optimization.

9.2 Strain Engineering: The Deepest Competitive Moat

Aspergillus oryzae strain selection is the invisible core of soy sauce quality differentiation. Decades of systematic screening and adaptation for high protease activity, rapid growth, low harmful by-product generation, and salt/temperature tolerance have produced proprietary strain libraries at leading companies. These strain libraries cannot be replicated quickly with capital alone—they require the same decades of systematic development. This explains why small-scale producers cannot match the quality consistency of large-scale leaders regardless of equipment investment.

Key secondary microorganisms: Saccharomyces rouxii and related yeasts producing esters and alcohols (the aromatic complexity of premium soy sauce); Lactobacillus plantarum and Tetragenococcus halophilus producing lactic acid (the soft acidic background note). Precise management of the full microbial succession—from A. oryzae protease activity through yeast ester production to lactic acid bacteria acid development—is the art and science of premium soy sauce production.

9.3 Zero-Additive Technology: The Science Behind the Marketing Claim

Zero-additive soy sauce requires three technical pillars in combination: (1) UHT sterilization (135 to 145°C, 4 to 8 seconds)—complete elimination of all microorganisms including heat-resistant spores, replacing the need for chemical preservatives; (2) aseptic filling (sealed sterile chambers, continuous CIP/SIP cleaning and sterilization of product-contact surfaces, positive-pressure HEPA-filtered air)—preventing post-sterilization contamination; (3) nitrogen-flush packaging (displacement of headspace oxygen to below 1%)—suppressing oxidative degradation and residual aerobic microorganism growth. The capital cost of this system is substantially higher than conventional filling lines—this real cost differential is the legitimate technical justification for zero-additive premium pricing.

9.4 Compound Condiment Technology: Formulation Science

Compound condiment development is formula science, not fermentation science. Core technical capabilities: (1) sensory research—large-scale consumer taste testing to optimize flavor parameter weighting across multiple dimensions (heat level, numbing, umami, salt, sweetness balance); (2) flavor protection—encapsulation of volatile aromatics (capsaicinoids, hydroxysanshool) in food-grade microcapsules for controlled release at cooking temperatures; (3) emulsification stability—preventing oil-water separation in complex sauce formulations during storage; (4) shelf-life engineering—maintaining flavor integrity across 12 to 18 month shelf life despite temperature variation and oxygen exposure.

9.5 Digital Fermentation Management: From Black Box to Visualization

Traditional fermentation relied on master brewers' accumulated sensory judgment—color, aroma, and taste evolved over decades of experience, impossible to transfer quickly. Modern smart fermentation installs dense sensor arrays (multi-point temperature probes, pH electrodes, dissolved oxygen meters, gas analyzers for CO₂ and NH₃ evolution) that continuously capture the fermentation state. Historical batch data libraries (years of batch records → machine learning models) progressively build predictive "process parameter → final quality" models that augment human decision-making with data-driven process adjustment recommendations.

9.6 Future Technology: AI-Enabled Brewing and Synthetic Biology

Two frontier technologies merit monitoring. AI-enabled fermentation optimization: training models on large historical fermentation datasets to predict optimal control parameters and recommend process adjustments could progressively shift brewing from "expert judgment-assisted by sensors" to "data-driven AI optimization of the full fermentation process." Synthetic biology: gene-engineered A. oryzae strains capable of directionally synthesizing high-value flavor compounds (specific esters, high-purity nucleotides) at higher efficiency than natural strains; regulatory pathways (GMO microorganisms in food) and consumer acceptance remain major near-term barriers but could transform industry cost structures over a 10- to 20-year horizon.

Ten: Risk Landscape — Five Dimensions of Uncertainty in the Condiment Industry

10.1 Consumer Downtrading: Cyclical Pressure on Premium Strategy

Qianhe's 2024 first-ever revenue decline exemplifies the downtrading risk. Economic pressure reduces consumer willingness to pay premium prices for condiments: average unit price for premium soy sauce declines as consumers shift to mid-tier alternatives; white-label and private-label products (growing on Pinduoduo) gain share among price-sensitive buyers. Counter-strategy: multi-price-tier product portfolios to hedge against single-tier exposure (Haitian's model—maintaining mass-market lines alongside premium zero-additive lines).

10.2 Food Service Cyclicality: The Double-Edged B-Channel Dependency

Restaurant industry profitability continues under pressure despite revenue recovery (rent, labor, and ingredient costs rising faster than customer spending). B-channel condiment buyers have very limited price-increase tolerance. Simultaneously, rising chain penetration rates create both an opportunity (large-scale customers consolidate purchasing toward capable national suppliers) and a bargaining-power threat (chain customers' scale enables aggressive price negotiation—Yihai/Haidilao relationship exemplifies this duality).

10.3 Food Safety and Reputational Risk: The Most Fragile Asset in the Social Media Age

The 2022 Haitian additive controversy—a viral social media storm over domestic vs. export formulation differences that technically required no product recall yet caused 15%+ stock price decline and years of brand repair—is the defining case study for condiment industry reputational risk management. In the current media environment: food safety perceptions spread at exponential speed; PR responses (technical explanations) travel far slower than the original fear narrative; even technically correct products can suffer lasting brand damage from poorly managed online controversies. Defense requires proactive transparency (ingredient education, factory tours, third-party certification) rather than reactive crisis response.

10.4 Channel Disruption: The Ambivalent Impact of Live-Stream Commerce and On-Demand Retail

Live-stream commerce drives new customer acquisition and rapid product launches but undermines channel price discipline—"lowest price guaranteed" demands from top streamers conflict directly with maintaining uniform pricing across traditional distribution channels. On-demand retail (30-minute delivery) serves the condiment category's high-frequency repurchase nature ideally but requires denser urban front-warehouse networks, increasing last-mile logistics costs. Private-domain traffic (brand WeChat groups, membership systems) enables direct consumer relationships and reduces platform intermediary fees, but requires sustained content investment and has scale ceiling constraints.

10.5 Raw Material Price Volatility: The Profit Cycle's Most Important Driver

The asymmetric price transmission mechanism—"cost rises difficult to pass through via price increases, cost declines not fully passed through to consumers"—is the fundamental explanation for condiment profit margin cyclicality. When soybean prices rise, companies absorb margin compression to protect channel relationships; when prices fall, they retain the benefit rather than cutting prices. Tracking CBOT soybean futures (or domestic soybean meal spot prices) with a 6- to 12-month lag, is the most reliable leading indicator of condiment sector gross margin trends.

Eleven: 2026–2030 Outlook — Compound Condiments Lead, Premium Penetrates the Cycle, and Internationalization Breaks Through

11.1 Macro Foundation: Long-Term Growth Logic Remains Intact

China's condiment market baseline projection for 2026 to 2030: CAGR of 5 to 7 percent, reaching approximately 750 to 800 billion yuan by 2030. Core assumptions: China GDP growth of 4 to 5 percent per year; food service sector broadly maintaining current scale; compound condiment categories sustaining high growth; health-premiumization trend continuing to elevate average unit prices.

11.2 Soy Sauce, Vinegar, and Oyster Sauce: "Volume Stable, Value Ascending"

Soy sauce: projected 2030 market scale of approximately 140 to 150 billion yuan, primarily value-driven (price tier upgrade). CR5 to rise from current 45 to 50 percent to approximately 55 to 60 percent by 2030. Key unknown: whether China can establish a viable 100 yuan+ premium soy sauce category (analogous to Japan's artisan soy sauce segment) before 2030.

Vinegar: 2030 projected market scale approximately 23 to 25 billion yuan, modest CAGR of 3 to 5 percent. Hengshun's progress toward genuine national brand status remains the key observable.

Oyster sauce: 2030 projected market scale approximately 16 to 17 billion yuan, maintaining 7 to 8 percent CAGR, with "genuine-oyster-juice oyster sauce" potentially emerging as the next quality differentiation narrative axis.

11.3 Compound Condiments: The Most Certain High-Growth Segment—Targeting 300 Billion Yuan by 2030

Compound condiments are projected to maintain 10 to 12 percent CAGR through 2030, reaching a combined market scale exceeding 300 billion yuan—surpassing basic condiments and becoming China's largest single condiment category cluster. Key drivers: restaurant chain penetration rate projected to exceed 30 percent by 2030 (each percentage point of chain penetration growth creates tens of billions yuan of incremental compound condiment demand); continued young-adult household lazy-cooking trend; and ongoing new category/regional-flavor recipe product innovation.

11.4 Industry Concentration: Five Paths to Continued Consolidation

Industry consolidation will advance through: (1) organic share gain by leaders through scale and channel advantages; (2) M&A acceleration—Haitian has the strongest balance sheet and strategic motivation for acquisitions; (3) food safety regulation eliminating below-standard small producers; (4) e-commerce algorithm feedback loops amplifying brand recognition advantages; and (5) early international brand-building successes further reinforcing domestic premium positioning.

11.5 Zero Additives: From Differentiator to Baseline Standard

By 2028 to 2030, the 20 to 30 yuan/500 ml mid-market soy sauce segment will be predominantly zero-additive—at which point zero-additive will no longer command premium pricing but will become a baseline consumer expectation. Qianhe's strategic imperative: establish the next differentiation tier above zero-additive before this transition completes. Candidate axes: organic certification, ultra-long fermentation, terroir/strain specificity.

11.6 Internationalization: Southeast Asia as the Realistic First Beachhead

Southeast Asia (Indonesia, Vietnam, Thailand, Malaysia, the Philippines, Singapore) is the most actionable near-term international market for Chinese condiment brands. The region has large ethnic Chinese communities with cultural affinity for Chinese condiment brands; the restaurant chain penetration rate is on a rapid upward trajectory creating growing demand for standardized condiments; and the spread of Chinese mala hot-pot chains (Haidilao, Xiao Fei Yang) is educating local consumers on Chinese flavor profiles, directly creating brand awareness and demand for Chinese compound condiments.

North America and Europe remain much longer timelines for Chinese condiment brands—Kikkoman's decades of investment in building mainstream (non-Asian) consumer acceptance is the benchmark for how long this takes. Chinese brands' international expansion journey, from the Asia-Pacific Chinese community base to mainstream non-Chinese consumer markets, has barely begun.

Twelve: Conclusions — Soy Sauce Duopoly, the Lonely Vinegar King, and the New Order of the Compound Era

12.1 The Narrative: Three Parallel Industry Story Lines

Story line one: The soy sauce duopoly in bifurcation. Haitian demonstrated the reality and durability of its competitive moat in 2024—269 billion yuan in revenue, 6.344 billion yuan in net profit, 9.53 percent revenue growth, 12.75 percent profit growth. The channel network built over three decades cannot be dismantled by a competitive concept. But premiumization remains unresolved: will Haitian's late-entry "zero-additive" line build genuine "premium quality" consumer associations, or remain perceived as a follower product? Qianhe's first-ever revenue decline signals that the "narrow gate" of zero-additive exclusivity is becoming a highway crowded with competitors. Its next differentiation dimension must be identified and built before the current one commoditizes.

Story line two: The lonely vinegar king and the limits of terroir advantage. Hengshun's 46.54 percent net profit growth is impressive in isolation, but "pruning" (cost control) rather than "growing" (revenue expansion) is not a sustainable value creation engine. Zhenjiang's terroir advantage is a real but geographically bounded asset. Hengshun's long-term value depends on whether it can transcend its Yangtze River Delta cultural footprint.

Story line three: The compound era's explosion and the race to build moats. Tianwei (+10.41%), Yihai Chinese compound condiments (+26.5%), Baoli (+11.91%)—three different business models, three different market positions, all confirming the structural high-growth of compound condiments. Restaurant industrialization and household lazy-cooking economics are two independent and mutually reinforcing structural drivers. As long as China's economy maintains basic stability, these drivers remain intact.

12.2 Five Core Conclusions

Conclusion 1: Haitian's competitive moat is real and will not be fundamentally disrupted in the next five years. Its strategic question is premiumization trajectory, not existential threat.

Conclusion 2: Zero additives will become a mid-market baseline standard by approximately 2028. Qianhe must establish its next differentiation tier before this transition completes.

Conclusion 3: Compound condiments are the most certain high-growth segment in China's condiment industry through 2030, with a CAGR of 10%+.

Conclusion 4: Southeast Asia is the most realistic first international expansion beachhead for Chinese condiment brands.

Conclusion 5: Industry concentration will continue increasing across all segments, with soy sauce advancing fastest and vinegar slowest.

12.3 The Supply Chain Perspective: factory data platforms's Condiment Factory Ecosystem

Beyond the listed company analysis, thousands of small and medium-scale condiment factories form the essential capillary network of this industry—providing OEM manufacturing capacity, regional ingredient supply, and customized formulation services that listed companies alone cannot cover.

factory data platforms covers 4.8 million active production factories, including a large number of condiment manufacturers across Guangdong (soy sauce, oyster sauce, flavoring paste), Sichuan (compound condiments, douban paste), Jiangsu (vinegar, condiment sauce), Shandong (pickled vegetables), and Fujian (fish sauce, Fujianese-style soy sauce). For B2B condiment buyers—food brands seeking OEM partners, restaurant chains seeking customized compound condiment suppliers, or cross-border traders seeking export-ready condiment factories—factory data platforms provides efficient access to verified, currently operating production facilities searchable by product category, geographic region, enterprise scale, and production certifications.

12.4 Closing Reflection: Flavor Memory and Industrial Evolution

China's condiment industry today is the product of decades of evolution. Haitian's channel scale was accumulated distributor by distributor across three decades. Qianhe's brand was forged in the confluence of consumer health awakening and precisely timed market positioning. Hengshun's Zhenjiang aromatic vinegar carries over a thousand years of regional culinary culture.

The next five years will see this industry advance simultaneously on premiumization depth, compound condiment category explosion, channel transformation, and international expansion. No single company can win on all fronts simultaneously. But making the right strategic choices—and having the discipline to sustain them through cycle and competition—is what separates the enduring winners from the temporary ones.

A drop of soy sauce. A spoonful of vinegar. A packet of hot-pot base seasoning. Simple seasonings, complex business, deep culture. This is the full picture of China's condiment industry.

This report is for research reference only and does not constitute investment advice. Market data are sourced from public information; where sources differ, please refer to official company disclosures.

Thirteen: Appendix — Industry Data Compilation, Enterprise Financial Comparison, and Extended Reference

A.1 Major Listed Enterprise Financial Comparison (2024)

| Company | Stock Code | Revenue | YoY Growth | Net Profit | Net Margin | Core Category |

|---|---|---|---|---|---|---|

| Haitian Flavouring | 603288 | 26.901 bn yuan | +9.53% | 6.344 bn yuan | 23.6% | Soy sauce/oyster sauce/flavoring paste |

| Zhongjiao High-Tech | 600872 | ~5.5 bn yuan (est.) | — | Significant decline | — | Soy sauce (Chubang brand) |

| Tianwei Food | 603317 | 3.476 bn yuan | +10.41% | — | — | Hot-pot base/compound condiments |

| Qianhe Condiment | 603027 | 3.073 bn yuan | -4.16% | 514 m yuan | 16.7% | Zero-additive soy sauce |

| Baoli Food | 603170 | 2.651 bn yuan | +11.91% | 233 m yuan | 8.8% | Western compound condiments (B-channel) |

| Hengshun Vinegar | 600305 | 2.196 bn yuan | +4.25% | +46.54% YoY | — | Zhenjiang aromatic vinegar |

| Yihai International | HK: 1579 | ~6.5 bn yuan (est.) | — | — | — | Hot-pot base/Chinese compound condiments |

| Jiajia Food | 002650 | 1.301 bn yuan | -10.52% | -243 m yuan | -18.7% | Soy sauce |

| Meihua Biological | 600873 | 25.069 bn yuan | -9.69% | 2.740 bn yuan | 10.9% | MSG/amino acids |

A.2 Soy Sauce Industry Output Trend

2010: approximately 6 million metric tons; 2015: approximately 8 million metric tons; 2018: approximately 8.7 million metric tons; 2020: approximately 9.4 million metric tons; 2024: approximately 10 million metric tons (estimated). Growth rate deceleration (from 5 to 8% annual growth before 2015 to 1 to 3% since 2020) reflects approaching category saturation in volume terms; market value continues growing through premiumization.

A.3 Key Regulatory Standards

Soy sauce: GB 18186 (brewed soy sauce standard); GB 2717 (soy sauce food safety standard). Vinegar: GB 18187 (brewed vinegar standard). Compound condiments: GB 31644. Food additives: GB 2760. Food labels: GB 7718. Regulating bodies: SAMR (food production licensing, market supervision), NHC (food safety standards), GACC (import/export inspection and quarantine).

A.4 Key Industry Terminology

Amino acid nitrogen (AN value): the primary umami intensity indicator for soy sauce, measured in g/100 ml. National standard specifies Grade 1 soy sauce ≥0.8 g/100 ml; premium ≥1.2 g/100 ml. Higher AN = higher umami, more technically demanding fermentation.

High-salt liquid-state fermentation: brine-to-koji ratio of approximately 2:1 to 3:1, liquid moromi, 6 to 24 months fermentation at 15 to 25°C. Produces premium flavor complexity. Standard for Kikkoman naturally brewed and Chinese premium soy sauce.

Zero-additive: refers to absence of preservatives (sodium benzoate, potassium sorbate), artificial colorants (caramel color), and artificial flavor enhancers (MSG, nucleotides). Requires UHT sterilization + aseptic filling to achieve shelf life without chemical preservatives.

Pixian Doubanjiang: a PGI-protected Sichuan chili bean paste produced in Pixian (Pidu District, Chengdu), fermented for 1 to 3 years in open clay vats under natural climate conditions. A fundamental flavoring agent for Sichuan cuisine.

B-channel custom condiments: condiment products formulated specifically for named commercial clients (QSR chains, food manufacturers) under the client's brand specifications. Higher development cost but structurally sticky customer relationships once established.

Compound condiment: per GB 31644, a product made from two or more condiments as primary ingredients, with or without added aromatics and food additives, used for flavor adjustment.

Data Sources

This report's data derive from the following publicly available sources as of June 2026:

Company annual reports: Haitian Flavouring (603288), Qianhe Condiment (603027), Hengshun Vinegar (600305), Zhongjiao High-Tech (600872), Jiajia Food (002650), Tianwei Food (603317), Yihai International (HK: 1579), Baoli Food (603170), Meihua Biological (600873) — all 2024 annual reports.

Industry association and government data: China Condiment Association industry statistics; National Bureau of Statistics food industry production data; GACC import/export statistics.

Third-party research: iMedia Research 2024 China Condiment Food Industry Market Research Report; ASKCI 2024 China Condiment Market Scale Forecast; 21st Century Business Herald 2024 China Condiment Fermentation Industry Research Report; Grand View Research Soy Sauce Market Size Report 2030; Market.us Soy Sauce Market Size, Share CAGR 5.2%.

International company data: Kikkoman Corporation Flash Report Fiscal 2024; Ajinomoto Annual Report 2024; Kraft Heinz Annual Report 2024; McCormick Annual Report 2024.

Media and analyst reports: 21jingji.com condiment sector coverage; Sina Finance condiment company annual report analyses; Jiemian News condiment industry deep dives; Beijing News condiment annual report disclosures.

Disclaimer: All data in this report are derived from public information. Market scale figures are estimates compiled from multiple sources; discrepancies between sources may exist. This report is for industry research and reference purposes only and does not constitute investment advice. For any data discrepancies, please refer to official listed company announcements.