Chapter 1: Industry Overview and the Definition of Industrial Valves

I. What Is an Industrial Valve

An industrial valve is a fundamental component of fluid transport and control systems. By opening, closing, or regulating the fluid channel within a pipeline, it achieves precise control over the flow rate, pressure, temperature, and direction of gases, liquids, and even solid particulates. It is the "joint" of petrochemical installations, the "lifeline" of nuclear power plant safety systems, and the core component that keeps LNG receiving terminals operating under extreme cryogenic conditions.

The definition of industrial valves is typically set in contrast to "civilian valves." Civilian valves mostly refer to low-pressure general-purpose products used in urban water supply, domestic gas, and HVAC applications, where technical barriers are relatively low. Industrial valves, by contrast, serve the harsh operating conditions of oil and gas, chemicals, power generation, metallurgy, semiconductors, and nuclear power. They must operate stably over the long term in high-temperature, high-pressure, deep-cryogenic, strongly corrosive, or radioactive environments, imposing extremely high demands on material properties, manufacturing precision, and sealing reliability. The unit price of a nuclear-grade main steam isolation valve can reach several million yuan — five orders of magnitude above a civilian ball valve — a direct reflection of the difference in technical content and application environment.

II. Main Product Categories of Industrial Valves

Classified by structure and function, industrial valves can be subdivided into more than ten major categories, each with its core application environment:

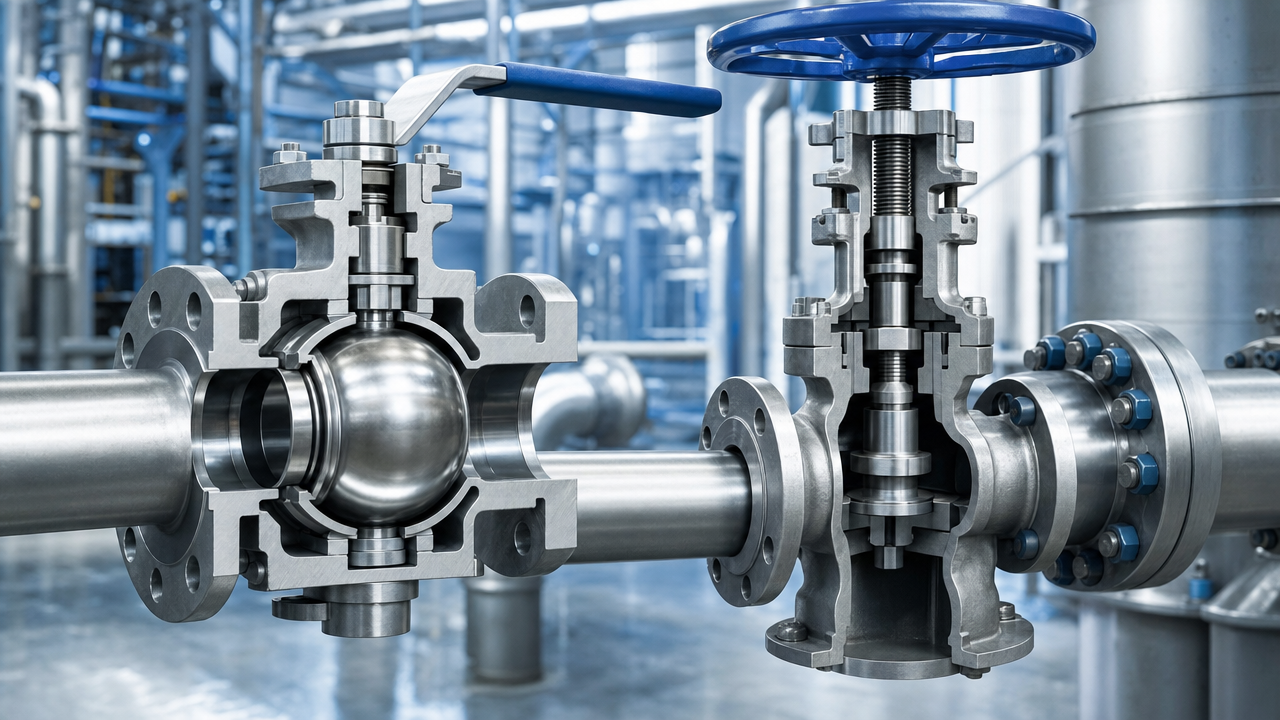

Gate valve: The gate moves perpendicular to the pipe axis; low flow resistance, suitable for fully open or fully closed service. This is the dominant valve type for long-distance oil and gas pipelines and water treatment systems, and one of the highest-volume categories domestically.

Ball valve: Uses a spherical plug as the closure element; easy to operate and reliably sealed, a 90° rotation completes the open or close action. Widely used in petrochemicals, LNG, and long-distance natural gas pipelines; it is China's largest single exported valve type. Nuclear-grade ball valves additionally require nuclear-grade materials and seismic qualification.

Butterfly valve: A disc-shaped flap rotates about an axis; compact structure, light weight, suitable for large-bore, low-pressure service. Urban water supply, wastewater treatment, and HVAC are the main downstream applications, but industrial-grade triple-offset butterfly valves are also widely used in petrochemicals and power generation.

Globe valve: The disc moves up and down along the fluid direction; better throttling performance than a gate valve, especially suited for applications requiring precise flow restriction. Nuclear-island steam circuits and precision chemical pipelines are typical applications.

Check valve: An automatic control valve that prevents backflow; widely used at pump outlets and compressor discharge lines to ensure one-directional fluid flow.

Control valve: Also called a regulating valve; works together with actuators and positioners to achieve continuous flow control, and is the core control element in process automation. Can be classified by actuator type into pneumatic, electric, and hydraulic control valves. Emerson Fisher and Chuan Yi Automation compete in this sub-market over the long term.

Safety valve: An overpressure protection device that automatically opens to relieve pressure when system pressure exceeds the limit, and closes automatically when pressure recovers. It is the last line of defense in pressurized systems, and is divided into spring-loaded, pilot-operated, and rupture-disc types.

Pressure reducing valve: Reduces high-pressure media to the pressure required by the process. The high-pressure pressure reducing valve for hydrogen refueling stations (70 MPa) is one of the current difficult challenges for domestic substitution.

Cryogenic valve: Designed specifically for extreme cryogenic service below -46°C. LNG systems commonly operate at -162°C; liquid hydrogen service can reach -253°C. Cryogenic valves must use austenitic stainless steel or aluminum alloys, and packing and sealing elements must pass dedicated cryogenic certification.

High-temperature, high-pressure valve: Ultra-supercritical (USC) coal-fired power units operate at 600°C/30 MPa; nuclear power primary-circuit conditions are approximately 345°C/17 MPa. Materials must resist creep and radiation damage, making manufacturing extremely demanding.

Vacuum valve: Used to maintain cleanliness and sealing in vacuum systems; a critical component in semiconductor fabrication, accelerators, and vacuum coating equipment. Domestic self-sufficiency is below 25%, with foreign brands such as Switzerland's VAT dominant.

Hydrogen refueling station valves: Valves dedicated to 35 MPa and 70 MPa hydrogen service must address hydrogen embrittlement and ultra-high-pressure sealing challenges. Domestic 35 MPa products have achieved breakthroughs, while 70 MPa still relies on imports.

Additional subcategories include semiconductor ultra-high-purity (UHP) valves, breather valves, blowdown valves, and steam traps, collectively forming a highly fragmented, technically stratified major product category.

III. Historical Evolution and Technology Generations of Industrial Valves

Industrial valves are not static traditional products; they have continually evolved with every leap in industrial civilization. A historical review of technology-generation transitions helps explain the origins of current technology directions:

First generation (19th century – early 20th century): Cast-iron and cast-steel valves, primarily simple gate valves and globe valves, manually operated, mainly serving steam engines, early oil refining, and waterworks systems, with relatively low working pressures and temperatures.

Second generation (early to mid 20th century): With the rapid development of the oil and chemical industries, valves advanced significantly in materials, pressure ratings, and sealing technology; ball valves and butterfly valves successively appeared. Steam globe valves gradually evolved toward higher temperatures and pressures, and standards bodies such as API and ASME were established during this period.

Third generation (late 20th century): The rise of extreme-condition applications in nuclear power, deep-sea oil, and LNG gave birth to high-end specialty categories such as nuclear-grade and cryogenic valves. At the same time, pneumatic and electric actuators matured, and control valves evolved from purely mechanical control toward instrument-control integration; flow control precision and sealing ratings improved greatly.

Fourth generation (early 21st century to the present): Intelligentization and digitalization are the core themes. The proliferation of HART/Fieldbus communication protocols enabled seamless integration of control valves with distributed control systems (DCS); smart positioners gave control valves self-diagnostic capability; IoT sensors and cloud data analytics moved valve condition monitoring from "reactive maintenance" to "predictive maintenance." At the same time, the semiconductor industry's extreme cleanliness requirements drove ultra-high-purity valve technology to a new frontier of precision manufacturing.

Fifth generation (2025 onward): AI-enabled autonomous optimization control: Artificial intelligence algorithms are beginning to participate in optimizing control strategies for regulating valves. In large refinery units, machine learning models trained on real-time process data have already helped optimize PID parameters and valve path selection for control valves, reducing unnecessary frequent actuation (extending actuator life) while improving process efficiency. This direction is still in its early stages, but it represents the long-term trajectory of industrial valves evolving from "execution elements" to "intelligent process optimization nodes."

IV. Core Technical Parameters of Industrial Valves

The key parameters for evaluating the quality of an industrial valve typically include the following dimensions:

Nominal pressure (PN/Class): Industrial valve pressure ratings range from PN10 (approximately 1.0 MPa) to Class 2500 (approximately 42 MPa); nuclear power primary-circuit valves must meet Class 1500 and above.

Nominal diameter (DN): From DN15 (15 mm) to DN2400 (2,400 mm) and larger. For large-bore valves, the difficulty of castings/forgings, assembly, and sealing increases exponentially.

Operating temperature: From LNG cryogenic temperatures of -196°C to ultra-supercritical coal power at 620°C; materials and seal design must be precisely matched.

Leakage class: Industrial valves typically comply with national standards or API, ASME, and ISO specifications; nuclear-grade valves must meet the most stringent Class A or Class AA sealing requirements, with leakage measured in mL/min.

Drive type: Manual, pneumatic, electric, hydraulic, and electro-hydraulic combined drives. Smart actuation has become standard for modern industrial automation.

V. Industry Scale and Structural Stratification

China's industrial valve industry has a large scale but is highly differentiated in structure. In 2024, the Chinese industrial valve market was approximately RMB 170–250 billion, with export volumes ranking first globally, but a significant proportion of mid-to-high-end core categories still relies on imports.

By price and technology tier, the market structure can be divided into three layers:

Bottom tier — general-purpose commodities (approximately 60% of scale): Standardized civilian/general-purpose products such as gate valves, globe valves, and butterfly valves. More than 5,000 domestic manufacturers exist, the localization rate approaches 100%, price competition is fierce, and profit margins are thin. Production capacity is highly concentrated in valve factories in Wenzhou, Shanghai, and Chengdu.

Middle tier — industry-grade products (approximately 30% of scale): Petrochemical valves, power valves, and municipal water-works valves at medium technical requirements. Domestic leaders such as Neway Valve (603699) and Kaiquan have essentially covered this tier, but top-end product lines still lag international brands.

Top tier — high-end specialty products (approximately 10% of scale, contributing 30%+ of value): Nuclear-grade valves, LNG cryogenic valves, semiconductor UHP valves, and ultra-high-pressure hydrogen valves — high unit prices, small volumes, extremely high technical barriers, and the main battlefield for domestic substitution.

This polarized pattern of "bottom-tier saturation, top-tier gap" is the fundamental frame of reference for understanding all policy trends, technology breakthroughs, and commercial narratives in China's industrial valve industry in 2026.

VI. Industry Chain Position

The industrial valve supply chain reaches upstream to casting and forging, specialty steels, sealing materials, precision machining, and surface treatment, and extends downstream to virtually every heavy-industry sector: oil and gas, power generation, chemicals, metallurgy, semiconductors, and municipal water works. This "connector" nature means that the valve industry has a high degree of cyclical correlation with the broader industrial economy, and any significant change in large industrial projects is rapidly transmitted to valve demand.

During 2025–2026, the simultaneous resonance of multiple downstream drivers — mass construction of "Hualong One" nuclear units, expansion of LNG receiving capacity, equipment replacement under the "dual renewal" policy, and accelerated semiconductor localization — is driving the overall operating climate for industrial valves steadily upward. High-end specialty categories in particular, supported by policy guidance and capital investment, are experiencing a once-in-a-decade technology leap window.

VII. The Deep Relationship Between Industrial Valves and Industrial Civilization

Understanding the strategic value of industrial valves requires moving beyond the "component" perspective and re-examining them from the standpoint of industrial systems theory. In any continuous-process industry (petrochemicals, pharmaceuticals, nuclear power, LNG), the number, quality, and reliability of valves determines whether the entire system can operate safely, efficiently, and continuously. A large petrochemical complex is fitted with more than 100,000 valves of various types; the failure of any single critical process valve can cause unplanned shutdowns, resulting in losses of several million to tens of millions of yuan per hour. The failure of a nuclear-grade valve carries the unacceptable risk of radioactive material release.

It is precisely this combination of "high reliability requirements + high failure consequences" that builds the unique commercial logic of high-end industrial valves: plant owners (refineries, nuclear power stations, LNG receiving terminals) are extremely conservative in valve selection — "not seeking the cheapest, only the most reliable" — and once a supplier is established, the motivation to switch is extremely weak. This is the fundamental reason why foreign brands have been able to maintain high market share and high gross margins in the high-end industrial valve market for so long — it is not the technology barrier alone, but the double reinforcement of technology barrier and customer stickiness.

China's manufacturing industry breaking through in high-end industrial valves is essentially a matter of breaking through this dual barrier: not only must technical standards equal or approach international levels, but sufficient engineering application records must also be accumulated over time before plant owners' trust can truly be won and a stable supplier qualification achieved. This path is bound to be long, but once it is successfully traveled, the barriers are equally solid and the likelihood of reverse substitution is equally low.

VIII. The Digital Transformation Trajectory of the Valve Industry

In recent years, the digital transformation of the industrial valve industry has advanced along two distinctly different paths: one is intelligentization at the product level (described above); the other is digital factory transformation at the production and manufacturing level. The two reinforce each other and are collectively reshaping the competitive landscape.

On the manufacturing digitalization side, leading valve companies are advancing the following core transformations: MES (Manufacturing Execution System) coverage of the entire production process, achieving real-time traceability of every step from casting to finished product; CAD/CAE 3D design and finite element analysis assisting in structural optimization and shortening new-product development cycles; automated inspection equipment (coordinate measuring machines, laser trackers, machine vision) replacing manual measurement and improving inspection efficiency and consistency; and ERP and supply chain digital platforms integrated to enable electronic management of nuclear-grade valve lifecycle documentation (nuclear QA system requirements for document traceability are extremely high, making digitalization an inevitable path).

On the sales and service digitalization side, valve selection software (such as Emerson's Control Valve Handbook online tool and Flowserve's valve selection calculation platform) has become the standard interface for providing technical services to downstream engineers. Domestic companies are also building similar technical selection support platforms to lower the threshold for design-institute engineers and improve the technical visibility of domestic valves. Remote valve diagnostic services (connecting field valves to service centers via IoT) are moving from concept to commercialization and are an important direction for digitalization in the valve aftermarket.

IX. The Talent Ecosystem of the Industrial Valve Industry

Industrial valves — especially high-end specialty valves — are a typically talent-intensive manufacturing sector; a considerable proportion of core competitiveness is embedded in the knowledge and experience of the engineering workforce and cannot be rapidly replicated through simple equipment investment.

Nuclear-grade valve engineers: Composite engineers who master both the nuclear QA system and nuclear-grade material processes are extremely scarce in China. The special nature of the nuclear industry (classified, closed, and subject to special certification) means that the career paths for nuclear-grade valve engineers are highly concentrated, mainly through research institutes under CNNC and China General Nuclear (CGN) and operational experience at nuclear power stations. Jiangsu Shentong and CNNC Sufa (000777), by virtue of their close cooperation with nuclear power groups, have formed relatively complete nuclear-grade valve engineer training systems internally, which is an important component of their technical barriers.

Cryogenic valve engineers: LNG cryogenic valve engineers must master cryogenic physics (phase-transition thermodynamics and cryogenic material mechanics), sealing engineering, and cryogenic testing technology; the training period is approximately 5–8 years. Domestic talent supply mainly comes from the cryogenic engineering programs at Tianjin University and Zhejiang University, and from internal training systems at Neway Valve (603699), Zhongke Fuhai, and similar companies.

Control valve process engineers: Control valve engineers who master process control (PID tuning and control valve sizing), field instrumentation (HART and Profibus communication protocols), and equipment diagnostics are in high demand but relatively abundant supply, coming mainly from industrial automation and chemical machinery programs.

Semiconductor UHP valve engineers: UHP valve engineers who combine semiconductor process knowledge (cleanliness standards and gas chemistry) with precision mechanical manufacturing capability are an almost entirely new talent category in China. Currently only a very small number of companies have begun targeted training. As semiconductor localization deepens, demand for this type of composite talent will grow rapidly.

Looking at the industry as a whole, the shortage of high-end valve talent is a substantive constraint on the acceleration of localization, not merely a technical-level problem. A relatively optimistic variable is that, as domestic high-end valve companies expand their market footprint and elevate their technical standing, the valve industry's appeal to recent university graduates is rising — improvements in salary levels and career development prospects will help to improve the talent supply structure over a longer time horizon.

X. The Role of Industrial Valves in the "Dual Carbon" Targets

China's push toward "carbon peak and carbon neutrality" has both brought structural demand realignment to the industrial valve industry and raised new requirements for product technology upgrading.

Valve demand from CCUS facilities: As large industrial enterprises such as Sinopec and China Coal Group begin to build CCUS (Carbon Capture, Utilization and Storage) demonstration projects, high-concentration CO2 capture and injection systems have created new requirements for specialized valves. Supercritical CO2 (pressure > 7.38 MPa, temperature > 31°C) has extremely strong permeability; conventional sealing materials are prone to swelling failure and require special PTFE or dedicated elastic sealing systems. High-pressure CO2 injection pipelines require Class 900–Class 1500 high-pressure ball valves and globe valves. Domestic substitution of valves for supercritical CO2 service is still in its infancy.

Fluid control in green hydrogen production systems: The key fluid control components in electrolytic water hydrogen production systems (PEM electrolyzers and alkaline electrolyzers) include high-purity hydrogen outlet valves, high-pressure pressure reducing valves, and water-circuit control valves, with demanding requirements for medium purity and sealing reliability. As green hydrogen demonstration projects and large-scale electrolysis projects are densely implemented (Sinopec's Kuqa 70,000-ton/year green hydrogen project, Sinohydro's Xinjiang project, and others), demand for matched high-purity hydrogen valves has begun to reach scale. Domestic companies have already developed dedicated valves for electrolytic hydrogen production systems and are conducting engineering validation jointly with downstream green hydrogen producers.

Control valve optimization in industrial energy-saving renovations: The "dual carbon" targets are driving extensive energy-saving renovations at in-service industrial installations, and intelligent control valves have played an important role in this renovation wave. By replacing aging control valves with higher-precision smart control valves and coupling them with advanced process control (APC) systems to optimize valve-position control strategies, installations can reduce overall energy consumption by 2%–5% without replacing major equipment — an energy-saving benefit that holds significant economic appeal for large refineries and chemical enterprises.

Chapter 2: Global Landscape and China's Position

I. Overview of the Global Industrial Valve Market

In 2025, the global industrial valve market was approximately USD 77.4 billion (approximately RMB 560 billion), projected to reach USD 96.5 billion by 2030, with a compound annual growth rate of approximately 4.5%. This growth rate reflects both the long-term logic of continuous global energy infrastructure investment and benefits from three structural drivers: the nuclear power revival, expansion of LNG trade, and upgrading of industrial automation.

In terms of regional distribution, the Asia-Pacific region is the world's largest industrial valve market, with a global share of approximately 40.1% in 2025, with China, Japan, South Korea, and India as major consuming nations. North America and Europe together account for approximately 45%, but in terms of growth rates, the Middle East, Southeast Asia, and South Asia are demonstrating faster momentum — Saudi Arabia's valve procurement grew approximately 45% year-on-year in 2025, with overall Middle East growth approximately 28%, driven by mega-projects such as NEOM, Saudi Aramco capacity expansion, and Egyptian gas projects.

In terms of product structure, ball valves and gate valves together account for approximately 45% of global industrial valve sales, making them the two largest categories. Control valves, benefiting from the industrial automation wave, are among the fastest-growing categories over the past five years, with a compound annual growth rate approaching 6%. Vacuum valves and semiconductor-specific valves, though relatively small in volume, have the highest technical added value, with a global market size of approximately USD 1.2 billion and the most concentrated competitive landscape.

II. Global Competitive Landscape: European-American Oligarchs and China's Scale

The global industrial valve competitive landscape shows a clear dual structure of "European-American technology oligarchs + Chinese-scale manufacturing."

European-American technology oligarchs: Represented by Emerson Fisher (control valves), Flowserve (integrated pump-valve solutions), Crane Co, IMI Critical Engineering, Cameron Baker Hughes, and Velan (nuclear power specialist), these companies share the following characteristics: deep technical roots (most with over a century of history), extreme depth in niche categories (Emerson Fisher's market share in pneumatic control valves exceeds 35%), comprehensive global service networks, and being primary drafters and participants in standards bodies.

Velan is a typical case. This Canadian company has dedicated itself to nuclear-grade valves for fifty years, with total revenue of approximately USD 347 million in 2024, a considerable portion from the Chinese nuclear power market — having successively secured contracts exceeding USD 36 million and USD 34 million with Chinese nuclear power, supplying critical nuclear island equipment such as high-temperature, high-pressure globe valves and safety valves. Even against the backdrop of continuously increasing localization pressure, Velan's position in the nuclear-grade "crown" category remains extremely difficult to shake.

Flowserve's FCD (Flow Control Division) is one of the world's largest industrial control valve manufacturers, focusing on PETROVAL cast specialty alloy valves, serving the world's top refineries and LNG terminals, with annual revenue of approximately USD 1.2 billion.

Chinese-scale manufacturing: China has the world's largest number of valve manufacturers, with more than 2,000 above-scale enterprises and over 500,000 employees. In general mid-to-low-end products, Chinese manufacturing has come to near-monopolize global supply with significant price advantages.

III. Value Distribution by Sub-Category in the Global Valve Market

Looking at the value distribution by sub-category in the global industrial valve market, while ball valves and gate valves have the largest volumes, their value density (per-valve value) is lower. Control valves, though fewer in number, have high unit values and rich service revenues, making them one of the most profitable sub-segments.

The global control valve market is approximately USD 12 billion (2025), accounting for approximately 15% of the overall industrial valve market, but contributing approximately 30%–35% of industry profits, because control valves have not only high unit values but also a large associated business in actuators, positioners, spare parts, and maintenance services. Emerson's valve and actuator business, within its global industrial automation segment, has among the highest gross margins of any sub-segment, confirming the high-value nature of the control valve segment.

The highest unit-price categories in the global industrial valve market (nuclear-grade valves, large-bore LNG cryogenic valves, semiconductor UHP valves) account for no more than 5% of total market size, but concentrate approximately 15%–20% of the industry's profit pool — the core profit source for a small number of top suppliers.

IV. China's True Position in the Global Value Chain

China's position in the global industrial valve value chain presents a typical "high volume, low value" paradox: China produces approximately 40% of global valve volumes but likely creates less than 20% of global value.

For nuclear-grade valves, a mature nuclear power station requires thousands of valves; a Hualong One unit requires approximately 18,000 valves worth approximately RMB 200–300 million. Nuclear-grade valve unit prices are ten to a hundred times that of ordinary industrial valves, and while Chinese nuclear-grade valve manufacturers (including Jiangsu Shentong and CNNC Sufa) can now produce many nuclear-grade types, the most technically demanding "crown" categories (main steam isolation valves, pilot-operated pressurizer safety valves, bursting discs) still partially come from imports by Velan and IMI.

In the LNG cryogenic valve field, large-bore (42 inches and above) cryogenic ball valves for China's large receiving terminals were previously almost entirely dependent on import brands such as Neles (now part of Metso) and Velan. Only around 2023 did the Longkou LNG project achieve the engineering application breakthrough of a complete series of 42-inch domestically produced cryogenic ball valves, marking China's major breakthrough in LNG large-bore cryogenic valves. However, approximately 60% of products outside small-to-medium bore still come from imports.

In semiconductor UHP valves, the domestic production rate is below 10%. Swiss VAT Group holds approximately 75% market share in vacuum valves, and Swagelok and Fujikin dominate process fluid valves. Domestic companies are essentially in the early stages of catching up.

V. New Variables in China's Valve Trade Landscape: U.S. Tariff Impact

In Q1 2025, the United States imposed approximately 54% combined additional tariffs on Chinese industrial valves, causing China's valve exports to the U.S. to decline approximately 18% year-on-year. This was a short-term severe shock, forcing many export-oriented valve companies to rapidly adjust their destination markets.

The market redistribution effect has begun to emerge: Chinese valve exports to Middle Eastern markets grew approximately 28% year-on-year (Saudi Arabia +45%), to Southeast Asia approximately 15%, and to South Asia approximately 12%. Some companies have begun establishing assembly or trade nodes in Thailand and Vietnam to circumvent U.S. trade barriers.

From a long-term perspective, U.S. tariffs have actually accelerated two effects: first, forcing Chinese valve exporters to upgrade toward higher added-value products; second, promoting domestic high-end valve localization, with the political legitimacy and capital attractiveness of import substitution simultaneously elevated. For domestic mid-to-high-end valve companies with technical accumulation, this is actually a passive catalyst.

VI. The Competitive Landscape of Japanese and Korean Valve Enterprises

Japanese valve industry: Represented by companies such as ASAHI, Kitz Corporation, and Fujikin, Japanese valves are known for high-precision hygienic valves, semiconductor UHP valves, and precision control valves, positioned in the high end, with exports primarily to Asia and Europe-America. In the global semiconductor UHP valve market, Fujikin is the second largest player after Swiss VAT, occupying an important position in gas panels and liquid distribution valves.

Korean valve industry: Represented by Rexnord Korea, DK-Lok, HanMi, and others, the Korean valve industry is relatively weak, primarily serving domestic semiconductors, petrochemicals, and shipbuilding. South Korea is the world's largest LNG ship builder, and construction by Samsung Heavy Industries, Hyundai Heavy Industries, and DSME drives substantial marine LNG valve demand, forming a relatively closed supply chain ecosystem.

Overall, Japan and Korea both have their advantages in high-end industrial valve technical accumulation, but in terms of manufacturing scale, price competitiveness, and market breadth, they lag significantly behind Chinese valve industry, with overall market share in a long-term contraction trend.

VII. The Core Narrative of 2026: Breaking Through to the High End

Synthesizing the global landscape and China's current situation, the core narrative of China's industrial valve industry in 2026 is: amid the historical inertia of "high volume, low value," achieving a targeted breakthrough toward the upper end of the value chain through batch localization of nuclear power valves, engineering validation of LNG large-bore cryogenic valves, the initial phase of semiconductor UHP valves, and intensive efforts on high-pressure hydrogen refueling station valves.

This breakthrough has both policy backing ("dual renewal" policy, nuclear power restart, hydrogen energy development roadmap), capital drivers (nuclear power valve-related companies generally outperformed the broader market in 2024–2025), and technical accumulation (Jiangsu Shentong's domestic market share in nuclear-grade valves exceeds 90%; CNNC Sufa has cumulatively secured hundreds of billions of yuan in nuclear power valve orders). The direction of the breakthrough is clear, but the remaining hard battles — particularly conquering the "crown" categories — still require time.

VIII. The Far-Reaching Impact of the Global Nuclear Power Revival on the Valve Market

In 2024–2025, global nuclear power experienced the strongest policy revival signals since the Fukushima accident. France announced plans to restart nuclear construction, building 14 EPR2 units; the UK's Sizewell C project was formally approved; Belgium and the Netherlands announced plans to extend nuclear lifetimes and consider new builds; the U.S., supported by the IRA Act, is accelerating development of small modular reactors (SMRs), with TerraPower, NuScale, X-Energy, and others entering engineering verification phases.

From a technology trend perspective, the SMR procurement strategy for valves is becoming a new strategic focus for the global nuclear valve industry. Compared to large reactors, SMR valve procurement amounts are smaller (approximately RMB 50–100 million per unit), but with higher standardization (modular design making valve specifications more uniform), shorter construction periods, and greater batch deployment potential. For valve companies that establish supply qualifications in the first batch of SMR units, their supply chain position in subsequent tens or even hundreds of SMR constructions will be extremely stable.

This global nuclear power revival wave has a dual impact on the nuclear-grade valve market: on one hand, directly driving new global demand for nuclear-grade valves; on the other hand, the European-American nuclear restart provides a potential export market for domestic nuclear-grade valve companies — the international promotion of Hualong One provides the most credible technical verification endorsement for domestically produced nuclear-grade valves accompanying exports.

IX. The Rise of the Indian Market and the Real Impact of the "China Replacement" Strategy

India is the single country factor with the greatest variability in the 2024 global industrial valve market landscape.

Domestic manufacturing rise: India's "Make in India" policy explicitly lists industrial valves as a key domestic manufacturing category, with L&T Valves, Kirloskar, and other domestic valve companies recently taking on large Indian domestic petrochemical and power projects, partially replacing Chinese export valves that previously held larger shares.

"China +1" impact on Chinese valve exports: When Western buyers (particularly chemical and petrochemical EPC contractors) build "China +1" backup sourcing strategies, India has become one of the alternative procurement locations for some general-purpose valves. In the short term, this substitution effect has a relatively limited impact on Chinese export volumes (approximately 5%–8% magnitude), as Indian valve companies' production scale, delivery capability, and price competitiveness still lag significantly behind China.

China's reverse exports to India: Notably, despite India's emphasis on localization, its actual valve procurement from China remains at a considerable scale — especially for infrastructure projects with high price sensitivity (municipal water supply and drainage, industrial park support).

Strategic significance for Chinese valve industry: Chinese valve manufacturers facing Indian competitive pressure should not engage in price competition in the general-purpose market, but instead seize the window to complete the technology leap toward high-end products, while actively building local service networks (warehouses, service stations) in India, Southeast Asia, and the Middle East. China has over 32,000 valve manufacturers, of which those truly possessing high-end technical qualifications and export engineering records number less than 1% — this differentiation will intensify over the next five to ten years.

X. Evolution of China's Regional Export Landscape

From 2023 to 2025, the regional focus of China's industrial valve exports has undergone notable migration:

U.S. direction: Hit by additional tariffs, exports to the U.S. fell approximately 18% year-on-year in 2025, with the share in total exports shrinking from approximately 12%–15% to approximately 8%–10%.

Middle East direction: Saudi Arabia, the UAE, and Qatar are the most important incremental target markets, with overall Middle East exports growing approximately 28% in 2025, with Saudi Arabia the largest growth (approximately 45%).

Southeast Asia direction: Vietnam, Indonesia, Thailand, and the Philippines, with accelerating industrialization, are driving continued growth in industrial valve demand.

South Asia direction: India's "National Infrastructure Pipeline" is driving large energy and chemical project investments, with Chinese valve penetration in India gradually increasing.

Overall, the U.S. tariff shock is driving China's industrial valve export structure toward accelerated diversification and dispersal to a wider range of developing markets.

Chapter 3: Core Technology: Materials, Sealing, and Control Drive

I. Material Technology: The First Barrier of High-End Valves

Materials are the starting point of the industrial valve technology chain, and also the most difficult link to break through in localization. Different operating conditions impose entirely different requirements on valve materials.

Nuclear-grade materials: Nuclear power valves must use materials meeting RCC-M (French nuclear island materials and welding specifications) or ASME III standards. Primary-circuit valves typically use low-cobalt austenitic stainless steel (such as 316L and 304L low-carbon types) to reduce the radioactive cobalt-60 dose generated by neutron activation. Nuclear-grade castings and forgings require batch-by-batch certification of chemical composition, metallographic structure, and mechanical properties, with a complete traceability chain from the melting furnace number to the final product.

Cryogenic materials: LNG and liquid hydrogen applications require cryogenic valves that maintain toughness at -162°C or even -253°C. Eligible materials include: austenitic stainless steel (304/316 series, with ductile-to-brittle transition temperature below -270°C, the mainstream choice for LNG valves); aluminum alloys (for -196°C and below liquid nitrogen and liquid hydrogen applications); and chromium-nickel alloys (Inconel 625, etc., for special cryogenic high-pressure situations). PTFE (polytetrafluoroethylene) remains elastic at -196°C and is the preferred packing material for cryogenic valves.

High-temperature, high-pressure materials: Ultra-supercritical coal power valves must operate at 600°C and 30 MPa for extended periods. The mainstream solution is martensitic high-temperature steel (P91, P92), with extremely demanding welding processes requiring precise preheating before welding and strict post-weld heat treatment. Harbin Electric Valves has accumulated over twenty years of P91/P92 welding process experience, which is one of the technical foundations of its approximately 70% domestic market share in ultra-supercritical valves.

Corrosion-resistant materials: Chemical installations involving strong acids, alkalis, and high-temperature organic solvents require valves made of Hastelloy (C276/C22), duplex stainless steel (2205/2507), or titanium alloys. Domestic high-end corrosion-resistant casting and forging capabilities have improved significantly in recent years, but for extra-large specifications and ultra-high cleanliness castings and forgings, there is still a gap compared with German and Japanese suppliers.

Valve castings and forged steel valves: The forming method of the valve body affects mechanical properties and applicable scenarios. Cast valve bodies (cast iron valves, carbon steel cast valve bodies) have lower cost and suit complex shapes, but relative density is weaker; forged valve bodies have uniform and dense microstructure with excellent fatigue and impact resistance, preferred for high-pressure and nuclear-grade applications. Stainless steel valves have seen the fastest demand growth in recent years.

II. Sealing Technology: The Core Indicator of Industrial Valve Quality

Sealing performance is the most critical technical indicator of industrial valves, directly determining process system safety and medium loss.

Soft sealing and metal sealing: Soft seals (PTFE, Devlon, Nylon, etc.) provide good sealing effect with low friction coefficients, but the upper temperature limit is typically below 200°C; metal seals (stainless steel, chrome alloys, hard-surface weld overlays) can be used at temperatures above 600°C, but require extremely high machining precision (sealing surface roughness Ra 0.4 μm or below). Nuclear-grade valves typically use metal-to-metal hard sealing with precision lapping processes.

Challenges of localizing valve seals: The localization level of high-end valve seals (particularly nuclear-grade flexible graphite packing rings, cryogenic PTFE O-rings, and semiconductor-grade pure polymer seals) varies. Semiconductor-grade UHP seals are essentially nonexistent domestically, primarily relying on imports from Japan's Shin-Etsu and America's Parker.

Valve stem sealing: The valve stem is the key component for dynamic sealing. Packing Seal and Bellows Seal are the two mainstream technology routes. Bellows sealing completely isolates rotary/linear motion from the fluid with zero leakage, the preferred choice for highly toxic medium pipelines.

III. Control Drive Technology: Intelligentization Is an Active Present-Tense Trend

Pneumatic actuators: Still the mainstream drive method for industrial control valves, with fast response speed and intrinsic safety (no electric sparks), suitable for hazardous areas. Domestic pneumatic actuators are basically localized, but high-precision smart positioners are still dominated by foreign brands such as Rotork, Biffi, and Emerson.

Electric actuators: With the growing demand for factory digitalization and remote control, the market penetration rate of electric actuators is rising rapidly. UK's Rotork is the absolute dominant player in global electric actuators, with China market share exceeding 40%.

Smart control valves and digital twins: The Industrial 4.0 wave is driving control valves toward integrated "sensing-diagnosis-optimization." Modern smart valves can not only execute control commands but also monitor real-time status parameters such as stem friction, packing wear, and valve position deviation, providing early warnings of valve faults through vibration analysis and pressure signal characteristics, enabling predictive maintenance. Emerson's AMS Valve Link and Fisher FIELDVUE DVC6200 are representative products of this technology direction.

Semiconductor UHP control valve technology: Semiconductor wafer fabrication imposes the most stringent cleanliness requirements, with internal wall surface roughness after electropolishing required to be Ra < 0.1 μm, metal ion contamination controlled below ppb levels, and all non-metallic internals required to pass SEMI standard certification. Domestic semiconductor-specific valve companies are in the early "zero to one" stage, with overall technology readiness level (TRL) approximately 5–8 years behind Swagelok and Fujikin.

IV. Manufacturing Processes and Precision Inspection

Precision machining is the key capability for high-end valve manufacturing. Sealing surface lapping must control surface accuracy to optical-grade levels; nuclear-grade valve bodies require 100% radiographic testing (RT), ultrasonic testing (UT), and penetrant testing (PT); cryogenic valves must undergo cryogenic leak tests at liquid nitrogen temperature; control valves must pass precise flow characteristic curve measurements (Cv value calibration).

Jiangsu Shentong has a dedicated nuclear-grade valve test bench that can simulate the combined pressure-temperature-radiation conditions of nuclear power primary circuits; Neway Valve's LNG valve factory is equipped with dedicated cryogenic leak test equipment capable of conducting full-size cryogenic ball valve sealing verification in liquid nitrogen at -196°C.

V. Surface Treatment and Protection Technology

Hard chrome plating and HVOF (High Velocity Oxy-Fuel) thermal spray: Due to tightening environmental regulations for hexavalent chromium (particularly the EU's REACH regulations), high-performance HVOF tungsten carbide and chromium carbide coatings are gradually replacing traditional hard chrome plating.

Electropolishing and mechanical polishing: The internal surfaces of semiconductor UHP valves and food/pharmaceutical valves must undergo multiple grinding and electropolishing steps to control roughness below Ra 0.25 μm, with high-end semiconductor valves requiring Ra < 0.1 μm (mirror-grade).

Anti-corrosion coatings: Epoxy powder electrostatic spraying and fusion-bonded epoxy (FBE) are the mainstream anti-corrosion solutions for long-distance pipeline ball valves.

Passivation treatment: Stainless steel and nuclear-grade valves must undergo strict passivation treatment (typically with nitric acid solution) to remove free iron from the surface and establish a stable chromium oxide passivation film.

VI. New Materials and Frontier Processes in Valve Applications

Additive manufacturing (metal 3D printing): Additive manufacturing technology is beginning to show application potential in high-end industrial valves, particularly for complex structures such as non-standard valve bodies and integrally formed sealing seats that are difficult to achieve with traditional processes. Flowserve has disclosed using laser powder bed fusion (LPBF) to produce Hastelloy fittings for control valve internals.

Ceramic material valves: In strongly corrosive and abrasive media (such as phosphoric acid, hydrochloric acid, high-temperature slurries containing solids), alumina ceramic (Al₂O₃) and silicon carbide (SiC) valves show excellent corrosion and wear resistance, with service life potentially more than ten times that of metal valves.

Shape memory alloys in micro-valves: In biomedical and specialty precision instrument fields, the superelasticity and shape memory effect of nickel-titanium alloys are used for automatic response control of micro-valves, using temperature changes to drive valve switching without external electric power.

VII. Deep Analysis of Control Valve Flow Characteristics Technology

The core of industrial control valve flow characteristic curves: Linear characteristic: Flow changes linearly with valve opening, Δq/Δl = constant. Equal-percentage characteristic (logarithmic): Under the same change in opening, the relative change (percentage) in flow remains constant — this is the most widely used industrial control valve characteristic because it matches the characteristics of most industrial processes. Quick-opening characteristic: Used for rapid shut-off applications.

High-precision control valves must control the deviation of the actual measured flow characteristic curve from the design value within ±5%. Domestic companies such as Chuan Yi and Zhejiang Sanfang have achieved stable characteristic accuracy within ±5% through precision CNC milling and per-unit flow calibration.

VIII. Noise and Cavitation Control: The Technical Core of High-Differential-Pressure Control Valves

At high differential pressure (such as 5–8 MPa across a refinery high-pressure fractionator bottom), ordinary control valves produce severe cavitation and flashing phenomena. Anti-cavitation control valves use "multi-stage pressure reduction" flow path design, distributing the total pressure differential across multiple throttling stages to ensure that the throttling pressure differential at each stage is below the medium's vaporization pressure. Representative products such as Emerson Fisher Cavitrol III series, Flowserve Mark100, and IMI CCI DRAG series all use proprietary multi-channel multi-stage pressure reduction designs.

IX. Technical Certification System and Test Requirements for Nuclear-Grade Valves

Seismic qualification testing: Nuclear-grade valves must pass IEEE 344, RCC-M F7700, and other specifications through actual vibration table testing to demonstrate that under specified seismic wave spectrum excitation, the valves can maintain structural integrity and functional effectiveness.

Thermal aging and radiation aging qualification: Non-metallic materials in nuclear-grade valves (seals, packing, valve seats) must pass accelerated thermal aging and radiation aging (gamma-ray cumulative dose to design service life) tests.

High Energy Line Break (HELB) condition qualification: Valves in the containment must maintain function during steam jet and high-temperature, high-pressure mixed environmental conditions.

X. Cryogenic Superconducting and Ultra-Low Temperature Valves: Emerging Technology Track

Quantum computing and high-temperature superconductor (HTS) commercialization is generating a new niche market — ultra-low temperature valves (operating temperature below -196°C, approaching absolute zero in some cases):

Liquid helium (LHe) systems: MRI superconducting magnets, particle accelerator superconducting magnets (such as the LHC's 4.2K liquid helium), and future quantum computers' dilution refrigeration systems need micro-valves and fluid control elements that work at 4.2K (liquid helium boiling point) or even lower temperatures.

Liquid nitrogen (LN₂) systems: High-temperature superconducting (HTS) transmission cables, superconducting transformers, and superconducting energy storage systems work at 77K (liquid nitrogen temperature range), creating demand for high-reliability cryogenic valves in liquid nitrogen cooling systems.

Chapter 4: Supply Chain Overview: From Castings and Forgings to Assembly and Testing

I. Upstream Raw Materials and Castings/Forgings

The starting point of the industrial valve supply chain is specialty metals and castings/forgings, the dual determinants of valve quality and cost.

Specialty steels and alloys: Nuclear-grade stainless steel must meet low-cobalt requirements (typically Co < 0.1%); USC coal power P91/P92 steel requires strict Cr, Mo content control; LNG cryogenic valve 316L must pass cryogenic impact toughness testing (Charpy V-notch impact value at -196°C must be ≥27 J). Domestic Baosteel, CITIC Pacific Special Steel, and Dongbei Special Steel can supply nuclear-grade and specialty stainless steel, but the largest electroslag remelting (ESR) and vacuum induction melting (VIM) castings and forgings still have a certain proportion coming from Japan and Germany.

Casting and forging processes: Valve castings are the mainstream forming method for most mid-to-low-end valve bodies. The domestic valve casting supply chain is highly concentrated around Wenzhou, Ningbo, and Shanghai. Wenzhou's Longwan and Ouhai districts are China's largest valve casting industrial clusters, with annual output accounting for approximately 40% of the national total.

Seals and packing: Valve seals and packing are among the highest-value technical categories in upstream support. Domestic production of graphite seals and PTFE packing has basically matured, but nuclear-grade dedicated seals and semiconductor-grade polymer seals still need continuous benchmarking against international standards for consistency and long-term reliability.

II. Midstream: Valve Body Processing, Valve Core Manufacturing, and Precision Assembly

Valve body processing: The valve body is the structural framework of the valve. High-end valve bodies must go through rough machining, semi-finish machining, finish machining, and sealing surface lapping, with full-process coordinate measuring machine (CMM) inspection, with key dimensional tolerances typically controlled within IT6 class. Nuclear-grade valve bodies require 100% radiographic and magnetic particle/penetrant inspection records with full quality documentation archived with the product.

Valve core manufacturing: The valve core (including ball, disc, flap, plug) is the core action element for sealing and control. Ball sphericity error must be controlled at the micron level, sealing surface roughness must be lapped to Ra 0.2 μm or below. Jiangsu Shentong's nuclear-grade ball machining uses five-axis CNC machine tools with laser tracker real-time monitoring, achieving sphericity accuracy to IT4 class.

Valve stem processing: The valve stem must have sufficient torque capacity and bending stiffness, with the surface undergoing precision grinding and nitriding treatment. For nuclear-grade valves, the valve stem must use ferritic-free austenitic stainless steel to prevent magnetic field interference with nuclear instrumentation systems.

Precision assembly: High-end valves must be assembled in constant-temperature (20°C ±1°C), clean environments (Class 100,000 cleanroom or above; semiconductor valves must reach Class 100).

III. Downstream Support: Actuators and Control System Integration

Actuators: Domestic actuator companies include Suzhou Neway (under Zhongmi Holdings), Chongqing Chuan Yi actuators, and Shanghai Automation Instrumentation. Mid-to-low-end actuators are basically localized, but SIL 2 certified smart electric actuators still have substantial Rotork imports.

Smart positioners: Emerson Fisher's FIELDVUE DVC6200, ABB's TZIDC, and Yokogawa's YVP are mainstream high-end products. Domestic Chuan Yi Automation is actively catching up with its complete instrumentation support capability and localized technical service.

Digital integration: With industrial internet and DCS/SCADA system upgrades, smart valve integration is becoming mandatory for large installation procurement. Smart valve components supporting HART, Profibus-PA, Foundation Fieldbus, and 4G/5G wireless connectivity are seeing rapid demand growth.

IV. Geographic Distribution of Industrial Clusters

- Wenzhou (Valve Capital): China's largest valve industrial cluster, mainly mid-to-low-end cast iron and copper alloy valves, with over 2,000 valve factories, annual output accounting for approximately 40% of national total.

- Shanghai: Center for high-end control valves and electric valves, with Chuan Yi, Shanghai Automation Instrumentation, and other state-owned enterprises and foreign-capital manufacturing bases.

- Jiangsu Suzhou/Wuxi: Important production area for nuclear-grade valves (Jiangsu Shentong), LNG valves (Neway Valve), and high-end industrial valves.

- Chengdu: Home base of Chuan Yi Automation, featuring control valves and smart instrumentation valves.

- Wuhan: Mainly power valves and pressure vessel accessories, with Harbin Electric Valves (ultra-supercritical power) and other companies.

- Harbin: Deep tradition of heavy industrial valve manufacturing, with rich technical accumulation in high-temperature, high-pressure fields.

V. Weak Links in the Supporting System: Special Raw Materials and Precision Inspection

Special metallurgical raw materials: Nuclear-grade low-cobalt austenitic stainless steel's domestic supply has long faced problems with composition consistency and batch stability. P91/P92 high-temperature steel processing accuracy and heat treatment uniformity for extra-large specifications remain directions for continuous optimization.

Precision inspection instruments: High-precision coordinate measuring machines, flow calibration equipment, and ultrasonic automatic testing systems are largely dependent on imports from Zeiss (Germany), Hexagon (Sweden), and Renishaw (UK).

Cryogenic sealing materials: Specialty PTFE sealing rings for LNG cryogenic service have limited domestic suppliers with specification consistency lagging Japanese and French products.

Software tools and simulation capabilities: Domestic companies universally use imported software such as ANSYS, ABAQUS, and Fluent for valve flow characteristic calculations (CFD fluid simulation), sealing contact analysis (FEM), and thermodynamic simulation.

VI. Supply Chain Resilience and Strategic Inventory Strategies

High-end industrial valves, particularly nuclear-grade ones, have extremely long procurement lead times (typically 12–24 months, with some Class 1 nuclear categories exceeding 36 months). For nuclear power as an example, each reactor must maintain a certain quantity of specific specifications of safety valves, check valves, and globe valves as spare parts on site to handle unplanned emergency repairs.

VII. Valve Testing and Certification Institution System

National-level testing institutions: Hefei General Machinery Research Institute (HGMRI) is the most important national-level testing institution in the domestic industrial valve field.

Industry association certification: The China General Machinery Industry Association Valve Branch is the industry organization responsible for industry statistics, standard management, and industry integrity assessment.

International certification bodies: TÜV SÜD, Bureau Veritas, Lloyd's Register, and other international certification institutions have local certification service organizations in China, whose certificates are cross-verifiable in their international networks.

Nuclear-grade specific certification: The ASME N-stamp certification is the core qualification for entering the U.S. and international nuclear power markets, with extremely limited domestic valve companies holding it (fewer than 10 nationwide). RCC-M certification (managed by AFCEN) domestic participation is equally sparse.

VIII. Frontier Progress in Valve Testing Technology

Computational Fluid Dynamics (CFD) simulation testing: Before physical prototype manufacturing, high-precision CFD simulation predicts valve flow field distribution, pressure loss, flow characteristics, and cavitation risk under different openings and conditions.

Acoustic emission (AE) monitoring: High-end valve sealing performance testing incorporates acoustic emission monitoring technology to identify the location and size of leakage channels.

Digital QA document systems: Digital quality assurance document systems (electronic QA management platforms) significantly reduce documentation management costs while improving audit traceability efficiency.

IX. The Reshaping Role of Material Innovation on the Valve Supply Chain

Additive manufacturing (3D printing): Metal additive manufacturing (SLM/DMLS) is changing the manufacturing approach for complex valve cores and valve body internal flow paths.

High-entropy alloys (HEA) and amorphous alloys: High-entropy alloys show performance exceeding conventional alloys in wear resistance and corrosion resistance, with application potential in the sealing surface materials field for valves exposed to extremely corrosive media.

Flexible graphite and composite sealing materials: Flexible graphite (Expanded Graphite, EG) is an important material for industrial valve packing, combining high temperature resistance, self-lubrication, and compressible sealing performance. China is the world's largest natural flake graphite producer and has formed a complete flexible graphite processing chain.

Radiation-resistant polymers: Radiation-resistant polymers (such as special polyimides and polyphenylene sulfide composite materials) for nuclear-grade valve seals inside containment structures are a key supporting area for nuclear-grade valve localization.

X. Digital Reconstruction of the Supply Chain: From ERP to Valve Full Lifecycle Platform

The digital transformation of the industrial valve supply chain is evolving from single-point tools toward comprehensive digital platforms covering the entire lifecycle:

Design end: CAD/CAM/CAE tools (CATIA, SolidWorks, ANSYS) are already widely adopted in leading valve companies.

Manufacturing end: MES adoption rate in leading valve companies is approximately 60%–70%, but less than 30% in small and medium enterprises.

Service end: Digital management of the valve full lifecycle (from factory delivery, installation, operational monitoring, to repair and refurbishment) is currently mainly led by foreign companies such as Emerson and ABB.

Chapter 5: Downstream Applications: Petrochemicals, Power, LNG, Semiconductors, and Emerging Sectors

I. Petrochemicals: The Largest Single Downstream, Entering the Equipment Renewal Cycle

Petrochemical valves are the largest single downstream market for Chinese industrial valves, accounting for approximately 35%–40% of total demand. The three major groups — CNPC, Sinopec, and CNOOC — have annual valve procurement estimated conservatively at RMB 30–50 billion, covering the full supply chain of refining, ethylene cracking, polyolefins, aromatics, and fine chemicals.

The 2024–2025 "dual renewal" equipment policy became an important catalyst for petrochemical valve demand. Sinopec confirmed advancing equipment renewal plans at its national refineries, with valve replacements at major refineries expected to bring tens of billions of yuan in incremental orders.

Notably, the major overhaul cycle (typically once every 4–5 years) for high-end ethylene and aromatics integrated plants has a marked pulse-like characteristic. The 2025–2026 period coincides with a concentrated overhaul year for multiple large refinery installations.

II. Nuclear Power: The Crown Segment of High-End Valves

Nuclear power is the downstream application with the highest technical content and largest unit value for industrial valves. A standard pressurized water reactor nuclear island uses approximately 18,000 valves, with procurement of approximately RMB 200–300 million per unit, and the total valve value of an entire nuclear power plant (including the conventional island and nuclear auxiliary systems) can exceed RMB 1 billion.

In 2025, China has approximately 26 nuclear power units under construction, with the scale of approved units under construction ranking first globally. According to China's nuclear power development plan, the target nuclear power installed capacity is 70 GW by 2025 and 110 GW by 2030.

Nuclear power valves are divided into three safety classes: Class 1 nuclear (1E class, directly affecting nuclear safety), Class 2 nuclear (auxiliary systems connected to safety systems), and Class 3 nuclear (general systems in the nuclear island). The higher the class, the longer the certification cycle, higher technical barriers, and more expensive unit price.

The domestic localization rate for nuclear power valves has improved significantly. In "Hualong One" units, the overall localization rate has reached approximately 88%–95%. Jiangsu Shentong covers more than 90% of the domestic market in nuclear power ball valves, while CNNC Sufa holds an important position in Class 1 and 2 nuclear butterfly valves, globe valves, and safety valves, with 2024 revenue of approximately RMB 1.84 billion.

The localization battle for the "crown" categories has not yet been completed. The main steam isolation valve (MSIV) must close within milliseconds and withstand high-temperature, high-pressure steam impact, making it technically extremely demanding. Pilot-operated pressurizer safety valves, which must guarantee precise opening pressure and reliable re-seating under multiple accident conditions, still rely on imports domestically.

III. LNG: From Sole Reliance on Imports to Domestic Breakthrough

LNG (liquefied natural gas) is the most important downstream market for cryogenic valves. LNG receiving terminal valve conditions are extremely harsh: storage tank area valves must operate long-term at -162°C, seawater vaporizer outlets require frequent opening and closing, and all valves must meet DNV GL or Det Norske Veritas certification requirements.

In 2024, China added approximately 22.3 million tons/year of LNG receiving capacity, with 31 operating LNG terminals nationwide and total receiving capacity of approximately 157 million tons/year.

LNG valve demand shows typical "batch concentration, high single-purchase price" characteristics. A 4-million-ton/year LNG terminal has valve procurement of approximately RMB 300–500 million, of which cryogenic ball valves and cryogenic butterfly valves account for more than 60% of the value.

On the localization front, the Longkou LNG project achieved engineering application of a complete series of 42-inch (DN1050) domestically produced cryogenic ball valves, a milestone in China's LNG large-bore cryogenic valve localization. Neway Valve's LNG cryogenic valve products have entered multiple domestic terminals, with continuously expanding market share in medium-bore (DN150–DN600) cryogenic ball valves. However, the overall localization rate for large-bore (DN900 and above) cryogenic ball valves is still approximately 40%, with substantial product volumes from Neles Metso and Velan imports.

IV. Semiconductors: The Largest "Blank Slate" Segment for Domestic Valves

Semiconductor process requirements for valves are the most stringent of all industrial scenarios. For 14nm and below processes, fluid control in etching, deposition, and cleaning process steps imposes extreme demands: internal surface roughness (Ra < 0.1 μm after electropolishing), metal ion contamination (< 0.1 ppb), particle generation rate (<1 particle/cycle @ ≥0.2 μm), pressure stability (< ±0.1%), dead-volume-free design, and chemical resistance (HF, H₂O₂, O₃, etc.).

The global semiconductor UHP valve market is approximately USD 1.2 billion (2024), projected to exceed USD 2 billion by 2030. Switzerland's VAT Group holds approximately 75% global market share in vacuum valves, with Japan's Fujikin and U.S. Swagelok dominating process fluid valves. Domestic chip manufacturers (SMIC, Yangtze Memory, Hua Hong) source virtually 100% of their valves from imports.

Domestic vacuum and UHP valve companies such as Donghui Valves, Shenhe Valves, and Hualiu Technology have started R&D, with some products entering customer verification stages, but the overall technology maturity level is approximately 5–8 years behind VAT and Fujikin.

V. Municipal Water Supply, Mining, and Other Downstream Markets

Municipal water supply is one of the largest downstream markets for butterfly valves and gate valves, with a localization rate approaching 100%, but extremely fierce competition and gross margins typically in the 20%–30% range.

The hydrogen energy supply chain is the most closely watched emerging downstream for 2025–2030. Hydrogen refueling station valves (35 MPa/70 MPa pressure reducing valves, high-pressure globe valves, safety valves) are at the frontier of domestic substitution battles.

VI. The Evolution of Refined Demand from Petrochemical Plants for Valves

From 2024 to 2025, the petrochemical industry's demand for valves has evolved from simple "pipeline switching control" to "process system intelligent operations." Owners are increasingly inclined to procure "smart valve components" that include intelligent actuators, positioners, and fieldbus modules, or even "full lifecycle service packages" covering valve management software and remote diagnostic services.

This shift from "single-item procurement" to "service bundling" is a double-edged sword for domestic valve companies. On one hand, full lifecycle service capability has become an important plus in new procurement by large refineries; on the other hand, companies that rely purely on product manufacturing capability and cannot provide integrated services will see their win rates in high-end project bids continuously decline.

VII. Synergistic Growth Effect of Nuclear Power and LNG Downstream

Nuclear power and LNG, the two main downstream sources of high-end valve demand, are showing an unprecedented simultaneous growth trajectory in 2025–2030. Moreover, the high-end valve capabilities required for these two tracks have high technical correlation (both requiring cryogenic/high-pressure material certification systems, precision sealing technology, and stringent quality assurance systems).

VIII. Structural Impact of the New Power System on Valve Demand

Since 2025, "new power system" construction (large-scale new energy + energy storage + smart grid) is reshaping the valve demand structure in the power industry. While photovoltaic and onshore wind power basically do not use traditional fluid control valves, large energy storage systems (flow batteries, compressed air energy storage) and coal power flexibility renovation are sources of incremental valve demand.

IX. Metallurgical Industry Valve Demand: Special Scenarios for High-Temperature, Wear-Resistant Valves

Blast furnace gas and converter gas systems: Metallurgical industry produces large amounts of blast furnace gas (containing CO, H₂S, dust) requiring large quantities of dust-wear-resistant sealing valves.

Continuous casting and rolling systems: Steel continuous casting systems have stable demand for hydraulic control valves and large-flow water valves.

Non-ferrous metal hydrometallurgy: Copper, nickel, and cobalt hydrometallurgy involves high-concentration acidic solutions, requiring highly corrosion-resistant valves (rubber-lined butterfly valves, Hastelloy globe valves).

X. Hygienic Valve Demand in Pharmaceutical and Food Industries

The pharmaceutical (GMP certification) and food (FDA certification) industries have unique "hygienic grade" requirements. Core characteristics of sanitary valves: no dead-zone flow path design; precision internal surface polishing (Ra ≤ 0.8 μm); full stainless steel material (316L mainstream); Clean-In-Place (CIP) and Sterilize-In-Place (SIP) capability; no lubricants. The estimated 2025 domestic market size is approximately RMB 5–8 billion, with annual growth approximately 10%–15%.

XI. Coal Chemical Industry and New Materials: Special Battlefield for High-Temperature, High-Pressure Valves

China is the world's largest coal chemical producer. Coal chemical installations have extremely stringent demands for high-temperature, high-pressure valves:

Coal gasification units (operating temperature 1200–1500°C, pressure 2.5–6.5 MPa): Slurry valves must achieve precise throttling in high-temperature, high-pressure fluid containing solid particles. The number of enterprises globally that can produce valves for these conditions can be counted on one hand.

Fischer-Tropsch synthesis units (coal-to-liquid route): reactor temperature 180–350°C, pressure 2–4 MPa, with wax and catalyst dust, requiring forged steel valves with special surface treatments.

Hydrocracking and hydrotreating units: Must meet NACE MR0175 (hydrogen sulfide stress corrosion resistance standard) requirements.

XII. Municipal and Water Supply: High Volume, Low Price, the Domain of Scale Economics

Municipal water supply (drinking water, wastewater treatment, stormwater management) is one of the largest "high volume, low price" sub-markets for industrial valves:

Products: Mainly gate valves and butterfly valves, primarily DN50–DN2000 in size, mainly cast iron valves (ductile iron) or low-carbon steel rubber-lined.

Policy drivers: "Sponge City" initiatives, urban aging pipe network renovation, and water supply network leakage control (the national "14th Five-Year Plan" requires water supply network leakage rate to drop below 8% by 2025) are important drivers.

Chapter 6: Profiling the Key Players

I. Domestic Leading Enterprise Profiles

Jiangsu Shentong (A-share 002438)

Jiangsu Shentong is the most representative private enterprise in China's nuclear power valve field, headquartered in Suzhou, Jiangsu, specializing in nuclear-grade valve development and production. In the domestic nuclear power valve sub-market, particularly nuclear-grade ball valves, market share exceeds 90%, and it is a core supplier for mainstream nuclear power models such as Hualong One and CAP1000.

The company's core barriers are: over twenty years of nuclear QA system accumulation, stable full-process manufacturing capability for nuclear-island-class valves, and deep strategic synergy established with nuclear power groups such as CNNC and CGN.

Jiangsu Shentong's growth logic is highly tied to the pace of Chinese nuclear power construction: every newly approved Hualong One unit corresponds to potential ball valve orders of more than RMB 100 million.

Neway Valve (A-share 603699)

Neway Valve is one of the most comprehensive listed industrial valve companies in China, covering multiple high-end industrial scenarios including oil and gas pipelines, LNG, petrochemicals, coal chemicals, and marine. 2024 revenue was approximately RMB 6.24 billion, up approximately 12.5% year-on-year.

Neway Valve's advantage lies in product line breadth and global footprint. The company's exports account for approximately 40%, with products sold to more than 70 countries, one of the few Chinese valve companies that has entered the supply chains of international oil companies (IOCs) and international LNG companies.

CNNC Sufa (A-share 000777)

CNNC Sufa is a nuclear valve holding listed company under CNNC, specializing in nuclear power valves and industrial valves, with 2024 revenue of approximately RMB 1.84 billion. Relying on CNNC's dominant position in nuclear power general contracting, the company has unique strategic resource advantages with extremely stable orders.

Chuan Yi Automation (A-share 603100)

Chuan Yi Automation is China's largest industrial instrumentation and smart control valve manufacturer, with 2024 revenue of approximately RMB 7.59 billion. The company's Chongqing Chuan Yi Automation Instrumentation division is a leading domestic control valve supplier, serving multiple industries including petrochemicals, chemicals, power, and metallurgy.

Chuan Yi invested earliest in smart valves and is one of the first domestic companies to launch control valve smart positioners and valve management systems (VMS). Its product matrix covers instruments (temperature, pressure, flow measurement), control valves, actuators, and control systems, forming a "complete chain" in industrial automation instrumentation.

Harbin Electric Valves

Harbin Electric Group's valve division deeply cultivates ultra-supercritical coal power and large hydropower industrial valves. In the ultra-supercritical coal power valve field (600°C/30 MPa main steam globe valves, control valves), Harbin Electric Valves holds approximately 70% domestic market share. In large hydropower valve configurations — including Baihetan and Wudongde giant hydropower stations' large-bore electric butterfly valves (DN3000 and above), spherical valves, and hydraulically controlled globe valves — Harbin Electric Valves has important supply records.

Kaiquan Pump Industry's valve division, mainly pump-matched valves and municipal water valves, is a leading domestic municipal and building industrial valve brand.

Zhejiang Sanfang Control Valve Co., Ltd. is a representative enterprise in the domestic professional control valve field, focused on high-performance control valves, serving petrochemical, power, and chemical customers.

Ziyi Automation

Shanghai Automation Instrumentation Co., Ltd. (Ziyi Automation) is a representative enterprise in China's instrumentation-type smart control valve field, deeply cultivating smart control valves and industrial automation control elements.

II. Foreign Brand China Market Landscape

Emerson Fisher: Global leader in control valves and smart valves, with approximately 30%–40% market share in China's high-end refineries and chemical installations, firmly occupying the top customer group with FIELDVUE series smart positioners and AMS valve management software.

Flowserve: Global pump-valve integrated giant, FCD division focused on control valves and industrial valves, mainly serving large Sinopec and CNPC refineries and chemical plants, with significant advantages in corrosion-resistant specialty alloy valves and high-differential-pressure control valves.

Crane Co: American century-old valve company, with products covering steam, chemical, and nuclear power fields.

IMI Critical Engineering: UK IMI Group subsidiary, focused on ultra-high-pressure, high-temperature, high-differential-pressure extreme condition control valves, a high-end player in nuclear power, hydrogen compression, and LNG.

Velan: Canadian nuclear power specialist valve company, with approximately 50 years in the global nuclear power market, 2024 revenue of approximately USD 347 million, with China nuclear power market contributing approximately 15%–20%.

III. Deep Analysis of Foreign Enterprise Technical Barriers: Why They Are Hard to Imitate

Tacit knowledge non-replicability: A considerable proportion of high-end valve manufacturing technology is "tacit knowledge" — the feel of precision lapping, experiential judgment in control valve flow characteristic tuning, recognition of abnormal sounds in LNG cryogenic testing. This knowledge cannot be fully obtained through patent documents or technical manuals and can only be formed through long-term practical accumulation and mentoring.

Irreplaceability of global service networks: Emerson and Flowserve's global service networks (technical support centers, field engineers, spare parts warehouses) cover all major industrial nations, providing 24-hour response service at any location.

First-mover advantage of standard-setting authority: Many parameter settings in major valve technical standards such as API, ASME, and ISO (such as the formula for calculating the flow coefficient Cv and leakage class classifications) actually originate from the technical practices of companies like Emerson and Flowserve, invisibly embedding their product design optimization directions into standard texts.

Self-reinforcing effect of customer stickiness: Once a large installation selects a valve brand, subsequent maintenance, upgrades, and expansion tend to maintain the same brand to ensure spare parts compatibility and operator familiarity.

IV. Summary of Competitive Landscape by Sub-Segment

| Category | Domestic Leader | Foreign Dominant Brands | Localization Rate (2026) |

|---|---|---|---|

| Nuclear power ball valve | Jiangsu Shentong | Velan, IMI | 90%+ |

| Nuclear power butterfly/globe valve | CNNC Sufa | Velan, L&T | 85%+ |

| Main steam isolation valve (Crown) | In progress | Velan, IMI | <50% |

| LNG medium-bore cryogenic ball valve | Neway Valve | Neles Metso | 60%+ |

| LNG large-bore cryogenic ball valve | Few companies breaking through | Neles Metso, Velan | 40% |

| Control valve (standard grade) | Chuan Yi, Zhejiang Sanfang | Emerson, ABB | 55% |

| Control valve (high end) | Chuan Yi, Ziyi | Emerson, Flowserve | 30% |

| Petrochemical general | Neway Valve etc. | Crane, Flowserve | 80%+ |

| Semiconductor vacuum valve | Early stage | VAT, Swagelok | <10% |

| Hydrogen refueling station 35MPa | Qipan etc. | GFI, OMB | 50%+ |