Chapter 1: Industry Overview and Industrial Pump Classification

Industrial pumps are mechanical devices that transfer fluid energy—converting the mechanical energy of a motor into the pressure energy and kinetic energy of liquids. They are the most widely used fluid machinery in manufacturing, responsible for moving cooling water, chemical feedstocks, petroleum, slurries, wastewater, and dozens of other media across every industrial sector.

Definition and Classification Framework

Industrial pumps are classified along three main axes:

By working principle:

- Centrifugal pumps (vane pumps): fluid receives energy through the centrifugal force of rotating impeller blades. This is the most common type globally, accounting for over 80% of all industrial pumps installed.

- Positive displacement pumps (volume pumps): fluid is displaced by the changing volume of a sealed cavity—reciprocating (piston/plunger, diaphragm) and rotary (gear, screw, vane) subtypes.

- Other types: jet pumps (no moving parts, low efficiency), electromagnetic pumps (for liquid metals in nuclear applications), and oscillatory pumps for special fluids.

By application field: petrochemical, power generation, municipal water/wastewater, mining, agricultural irrigation, food and pharmaceutical, seawater desalination, semiconductor ultrapure water, and nuclear.

By structural feature: single-stage vs. multi-stage; horizontal vs. vertical; open impeller vs. closed impeller; sealed vs. seal-less (magnetic drive, canned motor).

Key Performance Parameters

| Parameter | Symbol | Typical Range |

|---|---|---|

| Flow rate | Q | 0.1 L/min – 100,000 m³/h |

| Head | H | 1 m – 8,000 m |

| Shaft power | P | <1 W – 50,000 kW |

| Net positive suction head required | NPSHr | 0.5 m – 15 m |

| Efficiency | η | 30% – 93% |

Special High-Value Pump Types

Magnetic drive pumps (magnetically coupled, seal-less): the motor shaft drives an external magnet ring that transmits torque through a static containment shell to an internal magnet ring on the impeller shaft—achieving true zero leakage without any shaft seal penetration. Mandatory in toxic/flammable chemical handling. 2025 China market: approximately RMB 3.2 billion, growing 12-15% annually.

Canned motor pumps (Spaltrohrpumpen): motor windings and the hydraulic assembly are enclosed in a common sealed housing filled with the pumped fluid. The pumped liquid lubricates the bearings, eliminating mechanical seals entirely. Higher precision manufacturing requirements than magnetic drive pumps.

Nuclear reactor coolant pumps (RCP): the single most technically demanding pump in any industry. For Hualong-1 (HPR1000) reactors: operating pressure ~15.5 MPa, coolant temperature 290-345°C, rated shaft power ~5,700 kW, required operational lifespan 60 years without replacement. These specifications exceed virtually every other pump application on Earth.

High-pressure metering pumps / plunger pumps: used in petrochemical high-pressure injection (oil-field stimulation at 70-140 MPa) and HPDE polyethylene synthesis (280 MPa). The ultra-high pressure sealing technology (packed glands, PTFE chevron seals) represents the frontier of pump manufacturing.

Chapter 2: Global Landscape and China's Position

Global Market Scale and Regional Distribution

The global industrial pump market reached approximately USD 77 billion in 2024 (source: Grand View Research, Mordor Intelligence composite estimate), expected to grow at 4.2% CAGR to reach USD 100 billion by 2030. The market is driven by infrastructure investment in Asia, energy transition capex, and growing demand for high-efficiency equipment.

Regional breakdown (2024 estimated):

- Asia-Pacific: ~38% (led by China ~22%, India ~5%, Japan ~4%)

- Europe: ~26% (Germany, UK, France, Netherlands as industrial equipment hubs)

- North America: ~22% (US dominates, strong O&G and water utility demand)

- Middle East & Africa: ~8% (driven by oil/gas and desalination)

- Latin America: ~6%

China's 22% Share: Structural Analysis

China's estimated USD 17 billion (≈RMB 125 billion) market for industrial pumps in 2024 is underpinned by:

- The world's largest chemical industry: China accounted for ~42% of global chemical output in 2024; domestic ethylene capacity expanded by ~6 million tonnes/year in 2023-2024, generating massive demand for API 610-rated process pumps.

- Accelerating nuclear power construction: China has the world's most active nuclear construction program—approximately 10 new reactor units approved annually, each requiring dozens of high-specification pumping systems.

- Mandatory energy efficiency upgrade cycle: China's new pump energy efficiency standard (effective March 1, 2026) mandates efficiency improvements across the installed base, driving replacement demand for low-efficiency legacy equipment.

- Infrastructure megaprojects: The South-to-North Water Diversion Project and continued urban water/wastewater infrastructure expansion (RMB 1.2 trillion investment planned 2024-2026) sustain baseline demand for large axial-flow and mixed-flow pumps.

Global OEM Leaders and Their China Positioning

| Company | Headquarters | Revenue (pump-related, 2024E) | Key Strength | China Strategy |

|---|---|---|---|---|

| Grundfos | Denmark | ~USD 5.5B | Water & building services | 5 factories in China; dominant in HVAC |

| Flowserve | USA | ~USD 4.1B | O&G, chemical | Strong API 610 position in Sinopec/PetroChina |

| KSB | Germany | ~USD 2.8B | Chemical, power | Shanghai JV; large power plant installed base |

| Sulzer | Switzerland | ~USD 1.8B (pumps div) | Chemical, O&G | 3 service centers; specialized in overhaul |

| Xylem | USA | ~USD 8.0B | Water tech | Aggressive M&A; Evoqua acquisition 2023 |

| Wilo | Germany | ~USD 2.0B | Building, HVAC | Tianjin factory; strong in heat pump circulation |

| ITT | USA | ~USD 1.4B | Chemical, nuclear | Goulds brand strong in chemical market |

| IDEX | USA | ~USD 3.6B | Precision, industrial | Viking gear pumps, Pulsafeeder metering |

China's Domestic Pump Industry: Competitive Layers

Tier 1 (full-series, technical capability): Kaiquan Pump, Shanghai Liancheng (Lianlong), South Pump Industry, Deshengyuan — revenue RMB 2-8 billion, broad product lines, API 610 certification.

Tier 2 (specialized leaders): Danaher (DENA in China), Junhe Shares (君禾, energy-efficient small pumps for export), Leao (利欧股份, agricultural and sanitary), Shenyang Water Pump Research Institute, HAELEC Dynamics (哈电动装, nuclear).

Tier 3 (volume/price competition): Hundreds of small manufacturers in Wenzhou-Yongjia cluster; Zhejiang, Jiangsu, Shandong small-to-medium sized pump enterprises.

Chapter 3: Core Technology — Materials, Seals, and Hydraulic Design

Materials Science: The Foundation of Pump Performance

The materials used in pump wetted components (impeller, casing, wear rings, shaft) fundamentally determine the pump's ability to handle a given fluid at a given temperature, pressure, and concentration. Material selection is not simply "which alloy is strongest" but a nuanced optimization of corrosion resistance, erosion resistance, mechanical properties, castability, and cost.

Standard stainless steels:

- 304 (18-8): general purpose, weak acids, food-grade. Maximum temperature ~300°C.

- 316L (18-10-2 Mo): superior chloride corrosion resistance; dominant in chemical industry. 316L with <0.03% carbon resists sensitization in welding, critical for cast pump bodies.

- 904L: higher molybdenum (4-5%), nickel (25%), better resistance to sulfuric acid.

Duplex and super-duplex stainless steels:

- 2205 (F51): dual austenite-ferrite microstructure provides ~2× yield strength of 316L + excellent resistance to stress corrosion cracking (SCC) in chloride environments. Used in seawater desalination, offshore oil and gas.

- 2507 (F53): super-duplex, 25% Cr + 4% Mo, PREN (pitting resistance equivalent) ≥ 40; suitable for harsh seawater and aggressive brines.

Nickel-based superalloys:

- Hastelloy C-276 (Ni-16Mo-15Cr): resists both oxidizing and reducing acids, hydrochloric acid at all concentrations and temperatures, seawater, wet chlorine gas. The go-to alloy when stainless steel corrodes.

- Inconel 625: high-temperature strength + corrosion resistance; used in supercritical boiler feed pumps.

Titanium: Grade 2 commercially pure titanium: excellent seawater resistance, lighter than stainless, but poor castability. Typically used as forged impellers in marine service pumps.

Non-metallic linings:

- PTFE (Teflon) lining: universal chemical resistance, used in magnetic drive pump containment shells and diaphragm pumps handling strong acids.

- PVDF: better mechanical strength than PTFE, standard in semiconductor ultrapure water (UPW) pumps where metal contamination is unacceptable.

- PFA: like PTFE but melt-processable; used in Levitronix magnetic levitation pump components for 300mm wafer fabs.

Ceramics (SiC, Al₂O₃): Silicon carbide (SiC) bearings and seal faces in magnetic drive and canned motor pumps provide:

- Near-zero wear rate against abrasive slurries

- Chemical inertness in virtually all fluids

- High thermal conductivity (preventing hot spots in dry-run scenarios) SiC components are sourced globally from Kyocera (Japan), CeramTec (Germany), with domestic alternatives from Ningbo Yingte and Shandong Hongchen—though quality consistency still lags on high-precision applications.

Sealing Technology: Containing the Fluid

Mechanical seals: two lapped, flat-finished faces (one rotating, one stationary) are held in contact by spring force and hydraulic pressure. The seal faces operate with a microscopic fluid film (~0.5-1.0 μm) that lubricates and prevents dry contact. Leakage rate from a properly functioning mechanical seal: <1 mL/hr.

Key players: John Crane (Smiths Group subsidiary) and EagleBurgmann (joint venture of Freudenberg and Voith) together hold ~60%+ of global high-end mechanical seal market. China's Dandong Clone is the most credible domestic challenger, strong in <DN70, <200°C standard chemical seal applications.

API 682 Seal Flush Plans: API 682 codifies 30+ seal support system configurations (Plans). Plan 11 (self-flush from pump discharge) is the default for clean services; Plan 52 (pressurized external barrier fluid) is used for toxic/flammable fluids; Plan 53A/53B (gas-pressurized barrier) is required for highest-risk services. Understanding which Plan applies to each service is a core engineering competency for process pump users.

Dry gas seals: used in high-speed centrifugal compressors and some high-speed pump applications. Non-contacting spiral-groove face geometry creates a gas film that prevents contact. No liquid lubricant required. Requires clean, dry process gas or inert gas supply.

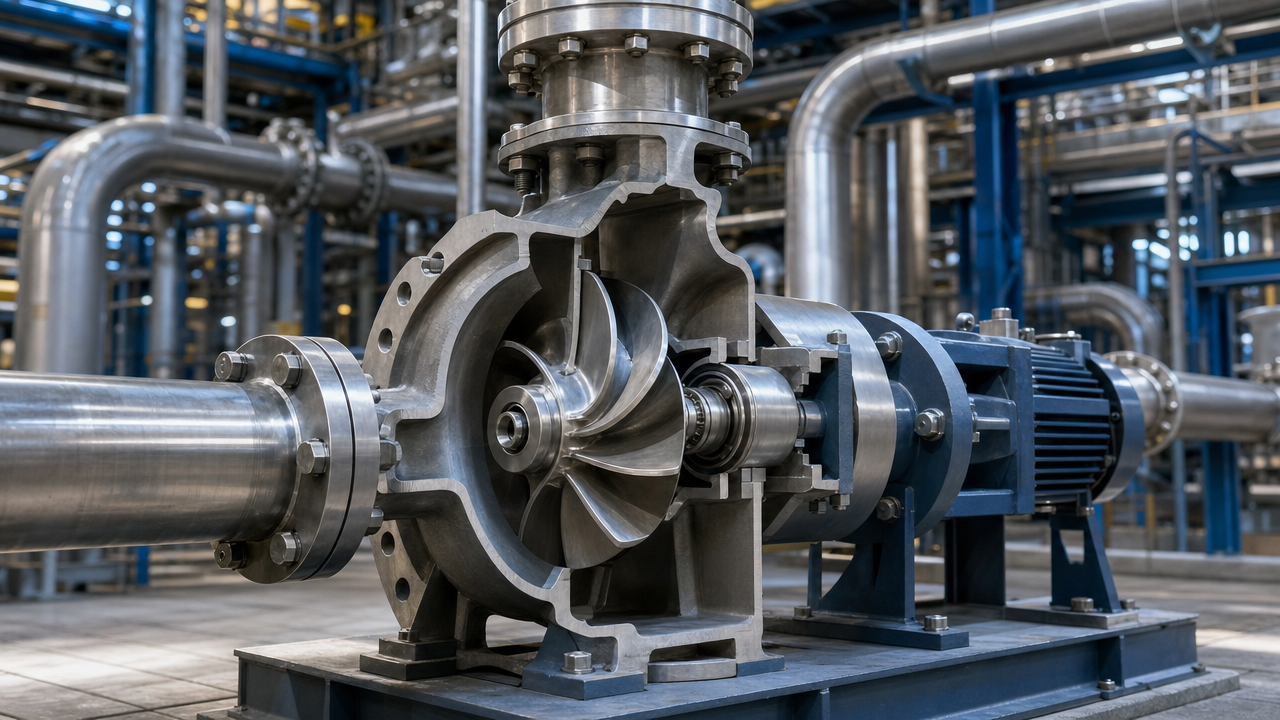

Hydraulic Design and CFD: The Science of Impeller Geometry

The hydraulic efficiency of a centrifugal pump—how efficiently it converts shaft power to fluid power—is determined by the impeller geometry: blade number (typically 5-9), blade angle at inlet (β₁) and outlet (β₂), blade width (b₂), and the meridional velocity distribution from suction eye to impeller exit.

Specific speed (Ns): the dimensionless parameter that characterizes a pump's design point. Low specific speed (Ns < 60): radial flow, narrow high-head impeller (used in multi-stage boiler feed pumps). Medium Ns (60-200): mixed-flow impeller. High Ns (> 200): axial flow pump (high flow, low head, used in irrigation and water diversion).

CFD (Computational Fluid Dynamics) simulation: modern pump hydraulic design relies heavily on 3D CFD analysis using software such as ANSYS CFX, Siemens STAR-CCM+, and China's own OpenFOAM-based tools. CFD allows designers to:

- Visualize velocity and pressure distribution in the impeller passages

- Identify recirculation zones and flow separation that reduce efficiency

- Predict NPSHr (cavitation behavior) before physical prototype

- Optimize blade geometry through automated design-of-experiments (DOE) + optimization loops

The most advanced pump companies now run automated shape optimization algorithms that test thousands of impeller geometry variants in CFD, selecting the Pareto-optimal design on efficiency vs. NPSHr vs. manufacturability. This level of computational optimization capability—requiring significant HPC resources and specialist CFD engineers—is a meaningful competitive differentiator between tier-1 and tier-3 pump manufacturers.

Chapter 4: Supply Chain — Castings → Machining → Assembly → Controls

The Casting Foundation

Pump bodies and impellers begin as castings. For standard chemical pumps in cast iron or CF8M stainless steel, domestic foundries in Shanxi, Jiangsu, and Zhejiang provide adequate quality at competitive cost. However, for large, thin-walled, complex-geometry castings in exotic alloys (Hastelloy C-276 pump casing, 2507 super-duplex impeller), the number of globally capable foundries is very small:

- Investment casting (lost-wax): achieves tightest dimensional tolerance (CT5-CT6), best surface finish, used for small impellers requiring high precision. China's precision investment casting has improved substantially—domestically produced Hastelloy investment castings now routinely meet ASTM A494 requirements.

- Sand casting: most economical for large pump bodies (>500 kg). Large stainless-steel sand castings of adequate quality (RT inspection, PMI verification, dimensional compliance) still present challenges for domestic foundries when specifications require zero internal porosity.

CNC Precision Machining

Impeller machining—particularly multi-blade 3D curved surface machining—requires high-precision 5-axis CNC machining centers. The impeller flow passages must be machined to surface roughness Ra < 3.2 μm (ideally Ra < 1.6 μm for efficiency), with tight dimensional tolerance on blade inlet and outlet angles. For a nuclear reactor coolant pump impeller, surface finish requirements are Ra < 0.8 μm and dimensional tolerance within ±0.05 mm.

China has made enormous strides in domestic 5-axis CNC capability. Domestic machine tool brands (Shenyang Machine Tool, Dalian Machine Tool Group) now produce machining centers capable of meeting most pump impeller requirements; import from Mazak (Japan) and DMG MORI (Germany) remains preferred for the most demanding nuclear/aerospace applications.

Mechanical Seals, Bearings, and Motors: The Critical Outsourced Components

For pump manufacturers, three outsourced components critically determine product quality and reliability:

Mechanical seals: as discussed, dominated globally by John Crane and EagleBurgmann. For Chinese pump manufacturers, using domestic seals requires extensive qualification testing to satisfy end-user inspection requirements. Using imported seals adds 15-40% to the BOM cost.

Rolling bearings: SKF (Sweden), NSK (Japan), FAG/Schaeffler (Germany) dominate high-precision pump bearings (precision class P5 or better). For continuous-duty high-speed pump applications, bearing selection and mounting specification directly determine MTBF. Domestic alternatives (Wafangdian Bearing, Luoyang Bearing) have improved quality but are still qualified only for lower-speed, less-critical services by most end-users.

Electric motors: high-efficiency motors (IE3 minimum, IE4/IE5 for energy-conscious applications) from WEG (Brazil), ABB (Switzerland/Sweden), or Siemens (Germany) add reliability assurance and ErP energy efficiency compliance. Domestic alternatives (NIDEC (after Teco-Westinghouse)), Wannan Motor, and AECC-branded motors for nuclear pumps) cover most applications.

Variable Frequency Drive (VFD) Integration

The integration of VFDs with centrifugal pumps has been the most significant energy-saving intervention in industrial pump practice over the past 20 years. By matching pump speed to actual system demand (instead of running at fixed speed and throttling flow with a valve), VFDs typically reduce energy consumption by 25-50% in variable-demand systems (HVAC, water supply networks, cooling towers).

China's domestic VFD manufacturers (Inovance Technology 汇川技术, Shenzhen Invt 英威腾, Delta Electronics) now compete directly with ABB, Siemens, and Schneider Electric in the mid-range VFD market. For pump-specific VFD packages (including pump protection logic, flow control algorithms, and predictive maintenance integration), domestic brands have become the dominant choice for domestic pump OEMs, while imported VFDs remain preferred for high-value downstream users (major petrochemical plants, nuclear).

Chapter 5: Downstream Markets — Petrochemical, Power, Municipal, Mining, Agriculture, Food, Desalination, Semiconductor

Petrochemical: The Most Demanding and Highest-Value Segment

China's petrochemical sector is the single largest buyer of high-specification industrial pumps, requiring API 610 performance, ASME/ANSI flange dimensions, and materials certified under ASTM/ASME standards. The 2022-2025 wave of major new petrochemical complexes (Zhejiang Refinery Phase 2, Gulei Refinery, Huajin Aromatics) drove an estimated RMB 8-10 billion in new pump procurement per year.

Key pump types: API BB5 (ring-section multi-stage, high-pressure boiler feed), API BB2 (axially split double-suction, large-flow cooling water), API OH1/OH2 (overhung, close-coupled, for pumping feedstocks), API VS1/VS6 (vertical submersible, for pit sumps and tank farm transfer).

Localization status: OH2 single-stage overhung pumps and BB2 double-suction pumps are now largely localized (domestic share > 60%). Multi-stage BB5 pumps and OH6 high-temperature high-pressure API pumps for applications above 300°C remain primarily imported (Flowserve, Sulzer, KSB dominant).

Power Generation: Coal-Fired Transition and Nuclear Expansion

China's installed power generation capacity in 2025 reached approximately 3,300 GW. For thermal power (coal, gas), the key pump systems are: boiler feed pumps (largest and most technically demanding pump in any thermal plant—6-12 stage, 20-30 MPa discharge, 5-10 MW shaft power), condensate pumps, cooling water pumps, ash slurry pumps.

Nuclear: as noted, China is commissioning approximately 10 new reactor units annually. Each Hualong-1 (HPR1000) unit requires:

- 1 reactor coolant pump (RCP, 5,700 kW shaft power, extreme specifications)

- 4-6 main coolant system pumps

- 20-30 safety injection and residual heat removal pumps (safety-grade Class 2)

- 100+ balance-of-plant pumps (Class 3 and non-nuclear-grade)

HAELEC Dynamics (哈电动装) and Dalian CNNC pump subsidiary have achieved NNSA certification for nuclear-grade pumps, ending China's dependence on imported RCPs. This represents one of the most significant localization achievements in China's nuclear industry.

Municipal Water and Wastewater: The Volume Market

China's municipal water and wastewater sector represents the largest volume market for centrifugal pumps—millions of units installed annually in water supply stations, drainage pump stations, and sewage treatment plants. The policy tailwind is strong: the 14th Five-Year Plan (2021-2025) committed RMB 2.2 trillion to water infrastructure; the 15th Five-Year Plan (2026-2030) is expected to maintain similar investment levels.

Energy efficiency is the dominant procurement criterion in this segment (post-2026 mandatory standards), driving replacement of outdated cast-iron pumps with high-efficiency stainless steel models equipped with IE3/IE4 motors and VFD controls. Grundfos (Denmark) holds strong market position in building HVAC circulation pumps; Kaiquan and South Pump are leading domestic players in large municipal supply pumps.

Mining: Slurry Pump Technology Leadership

China is the world's largest mining nation, producing approximately 50% of global rare earth, tungsten, and molybdenum output plus major shares of coal, copper, and iron ore. Slurry pump technology—handling abrasive mineral slurries at high flow rates—is an area where Chinese manufacturers have achieved genuine global competitiveness.

Shijiazhuang Industrial Pump Factory (石家庄工业泵厂, producing the renowned ZJ/SP brand slurry pumps) and Warman (Australia, now part of Weir Group) co-dominate the global hard-rock mining slurry pump market. Chinese slurry pump manufacturers have successfully exported to Southeast Asia (copper mines), Africa (gold mines), and South America (lithium/copper), where the price competitiveness of Chinese pumps relative to Warman and ITT/Goulds is highly attractive to mining operators.

Key technical differentiator: wear liner materials. Chrome alloy white iron (>27% Cr) for hard abrasive slurries; natural rubber linings for fine, less-abrasive slurries. The hardness-toughness tradeoff in wear-resistant materials is the central technical challenge in slurry pump design.

Semiconductor Ultrapure Water (UPW): The Next Frontier for Localization

Semiconductor fabs require ultrapure water (UPW) for rinsing wafers—the purity specification is 18.2 MΩ·cm resistivity, meaning virtually zero dissolved ions. Pumps handling UPW must be:

- Made of non-metallic materials (PVDF, PFA, PTFE) throughout all wetted surfaces

- Seal-less (magnetic drive) to avoid any lubricant contamination

- Manufactured in ISO Class 4 cleanroom conditions

- Extractable-tested to confirm zero leaching of contaminants

The domestic market for semiconductor UPW pumps is tiny by volume but extremely high-value: ~RMB 500M/year, growing at ~25% annually as China's domestic fab capacity expands dramatically. The market is currently dominated by Levitronix (Switzerland, magnetic levitation), Iwaki (Japan), and Finish Thompson (USA). Zero Chinese suppliers have qualified products for cutting-edge (28nm and below) fab applications as of 2025.

Chapter 6: Key Players Overview

Chinese Listed Companies in the Pump Sector

Kaiquan Pump Group (凯泉泵业, Shanghai) — revenue ~RMB 6.0 billion (2024E), listed on Shanghai Stock Exchange. Full product range from small building pumps to large API 610 chemical pumps. Particularly strong in municipal water supply, HVAC, and chemical services. Joint development partnerships with several major petrochemical EPC contractors.

Shanghai Liancheng (连成集团) — private, revenue ~RMB 4.0 billion, strong in API 610 chemical pumps and magnetic drive pumps, one of the earliest domestic manufacturers to achieve API Q1 certification.

South Pump Industry (南方泵业, 603033.SH) — revenue ~RMB 2.8 billion (2024E), leading in intelligent energy-saving water pumps for municipal and industrial applications, active in "smart water network" IoT platform development.

HAELEC Dynamics (哈电动装) — subsidiary of Harbin Electric, specializes in nuclear-grade, thermal power, and large industrial pumps. Holds NNSA nuclear safety equipment license. Participated in Hualong-1 reactor coolant pump localization program.

Junhe Shares (君禾股份, 603439.SH) — revenue ~RMB 2.2 billion (2024E), focused on energy-efficient small pumps for European residential and commercial export. Has achieved ErP energy efficiency certification with EEI ≤ 0.23. Revenue growing at ~15% driven by European heat pump market boom.

Leao Shares (利欧股份, 002131.SZ) — revenue ~RMB 8.0 billion (2024E, includes non-pump business), largest listed company with pump as core, covers agricultural, garden, and sanitary pumps. Strong manufacturing scale and procurement leverage; weaker in high-end technical products.

Aerospace Power (航天动力, 600343.SH) — revenue ~RMB 3.5 billion (2024E), holds nuclear safety licenses for various pump types used in nuclear power stations; also serves petrochemical and power generation sectors.

Foreign Players in China Market

Grundfos China (5 factories, ~8,000 employees): dominant in HVAC circulation pumps, building services, water utilities. Chinese-manufactured Grundfos pumps now exported to Southeast Asia.

Flowserve China: strong in API 610 process pumps for Sinopec and PetroChina refineries and petrochemical complexes. Maintains large installed base with sticky aftermarket service.

KSB (China) Co., Ltd.: Shanghai JV provides large power plant and chemical pump supply and service. Strong in power generation boiler feed pump market.

Sulzer (China): 3 service centers (Shanghai, Chengdu, Wuhan) specializing in pump overhaul for large process pumps. Their service + overhaul revenue model creates deep long-term relationships with major chemical plant operators.

Chapter 7: Localization Progress and Market Intelligence

The Three-Tier Localization Framework Tianxia Gongchang's factory data platform — covering 4.8 million verified Chinese factories in production — shows clear evidence of this domestic substitution pattern.

China's industrial pump localization can be analyzed across three tiers of technical difficulty:

Tier A — Largely Localized (domestic share > 60%): Standard centrifugal pumps (single-stage, API OH1/OH2), magnetic drive pumps (standard chemical services), slurry pumps (coal and copper mining), small-to-medium agricultural and municipal pumps, building HVAC circulation pumps.

Tier B — Partially Localized (domestic share 30-60%), active localization in progress: Multi-stage API BB5 high-pressure process pumps, large power plant main condensate and cooling water pumps, high-temperature high-pressure chemical pumps (> 300°C), API 676 gear pumps for petrochemical services, API 680 vacuum pump systems.

**Tier C — Minimally Localized (domestic share < 30%), significant gap remains:** Nuclear reactor coolant pumps (now partly localized with HAELEC Dynamics), semiconductor UPW seal-less pumps, magnetic levitation pumps, cryogenic LNG pumps (below -162°C), ultra-high-pressure metering pumps (> 200 MPa), dry gas seal technology.

Factory Database Intelligence: The 480-Million Factory Map

Using China's comprehensive industrial factory database—covering 4.8 million active manufacturing entities—regional clusters of industrial pump manufacturers reveal distinct geographic specialization patterns.

The Yangtze River Delta (Shanghai-Suzhou-Zhejiang) cluster concentrates high-end pump manufacturers: the greatest density of API 610-certified suppliers, the most foreign JVs, and the highest engineering talent concentration. The Wenzhou-Yongjia (Zhejiang) cluster represents the volume-production heartland for standard pumps—hundreds of manufacturers competing primarily on price and delivery speed.

The Northeast (Shenyang, Harbin) retains its historic significance in large industrial and nuclear pumps, anchored by national research institutions (Shenyang Water Pump Research Institute) and major power equipment groups (Harbin Electric).

By keyword frequency across the factory database, industrial pump manufacturers number ~2,686 active entities; centrifugal pump specialists: ~814; magnetic drive pump specialists: ~243; slurry pump specialists: ~441; metering pump: ~445; screw pump: ~509.

The 天下工厂 factory database also reveals significant entry of new manufacturers into energy-efficient pump categories since 2022, consistent with the policy-driven energy-efficiency upgrade wave.

The Critical Gap: Technology vs. Track Record

Domestic pump manufacturers often possess the theoretical design capability to produce pumps meeting API 610 or nuclear specifications. The actual localization barrier is less about design knowledge and more about:

Accumulated manufacturing process data: knowing which casting temperature profile produces acceptable microstructure in Hastelloy C-276, which CNC tool path avoids chatter on a thin-walled impeller blade—this knowledge accumulates only through repeated production runs.

Quality system maturity: API Q1, ISO 9001, and nuclear QA (HAF 003) quality systems require not just procedure documentation but demonstrated consistent implementation across hundreds of production lots. An auditor can tell within minutes whether a quality system is genuinely practiced or merely documented.

Reference list: the hardest localization barrier. A refinery EPC contractor will not specify an unknown domestic pump in a USD 5 billion greenfield project. The first reference installation is always the hardest to win.

Chapter 8: Price Bands and Business Models

Market Price Segmentation

Industrial pump pricing spans more than four orders of magnitude—from a RMB 200 residential circulation pump to a RMB 60+ million nuclear reactor coolant pump. Understanding the price band and its drivers is essential for market positioning.

Budget segment (< RMB 5,000): residential circulation pumps, small garden/irrigation pumps. Dominated by Grundfos (premium), Wilo, and domestic brands (Leao, Nanyang). Material: cast iron or plastic. Competition purely on price and brand recognition. Very thin margins.

Mid-range (RMB 5,000 – RMB 200,000): standard industrial centrifugal pumps, small magnetic drive pumps, metering pumps. Both domestic and foreign manufacturers competitive. API 610 compliance optional; performance standards are domestic national standards. Price competition intense; margins 15-25% gross.

High-value (RMB 200,000 – RMB 5 million): API 610 chemical process pumps, large multi-stage pumps, large slurry pumps, canned motor pumps. Engineering-driven procurement; total cost of ownership (TCO) analysis typical. Foreign brands command 30-80% premium over domestic alternatives in this range. Gross margins 30-50% for premium brands.

Extreme specialty (> RMB 5 million): nuclear reactor coolant pumps (RMB 30-60M each), ultra-high-pressure polyethylene process pumps, large coastal desalination main pumps (>10,000 m³/h). Essentially project-specific—prices negotiated individually, often bundled with long-term service agreements.

Business Models Evolving Beyond Hardware

Traditional model: design → manufacture → sell → limited warranty support. Thin margins, high capital-intensity, commodity competition.

Service-enhanced model: mandatory aftermarket parts (mechanical seals, wear rings, bearings) + scheduled overhaul contracts. Sulzer's global service network exemplifies this: the company earns comparable revenue from services as from new equipment sales. Margin on service revenue typically 50-70%, versus 25-40% on new equipment.

TCO-first sales approach: Grundfos and Wilo have pioneered lifecycle cost analysis as the centerpiece of their sales methodology—demonstrating that a Grundfos pump costing 40% more than a domestic alternative will save 3× that premium in energy costs over a 10-year operating life. This approach is effective with sophisticated buyers (large utilities, major industrial groups) but less effective with pure-price procurement.

Pump-as-a-Service (PaaS): Xylem's recent experiments with outcome-based contracts—charging per cubic meter of water pumped rather than selling hardware—represent the leading edge of business model innovation in the pump industry. If successful at scale, PaaS would fundamentally shift capital allocation from pump buyers to pump manufacturers, which requires manufacturer financial strength and predictive maintenance capability to manage downtime risk.

Digital platform model: Grundfos' "Digital Solutions" platform provides connected pump monitoring, energy optimization, and predictive maintenance as a subscription add-on. Annual subscription revenue per connected pump ~USD 200-800 depending on service level. This creates recurring revenue streams that smooth out the cyclical capital equipment business.

Chapter 9: Representative Customer Cases

Case 1: Zhejiang Petroleum & Chemical (ZPC) — Full-API-610 Chemical Pump Localization

Zhejiang Petroleum & Chemical's Phase 1+2 refining complex (40 Mt/yr crude throughput, USD 40 billion investment) is China's largest private refinery. ZPC's Phase 1 procurement (2017-2019) relied primarily on imported pumps (Flowserve, KSB, Sulzer) for safety-critical services. Phase 2 procurement (2021-2023) aggressively pushed domestic sourcing: Kaiquan Pump and Shanghai Liancheng won significant contracts for OH2 and BB2 category pumps, while foreign brands retained BB5 multi-stage and high-temperature-high-pressure OH6 applications.

The outcome: domestic pump suppliers now hold approximately 55% of ZPC's installed base by unit count (but only ~30% by value, since the highest-value specialty pumps remain imported). ZPC engineers report that qualified domestic pump failure rates are now comparable to equivalent foreign models for standard services, but mean time to failure for exotic alloy / extreme service applications still slightly favors foreign brands.

Case 2: Hualong-1 Reactor Coolant Pump — Nuclear Localization Milestone

Prior to 2016, China imported all reactor coolant pumps (RCPs) for domestically designed PWR reactors. The RCP in a Hualong-1 reactor is arguably the most technically demanding rotating machine in civilian industry: 15.5 MPa, 290-345°C, 5,700 kW, 60-year design life, 10-year mandatory qualification testing program.

HAELEC Dynamics (哈电动装, Harbin Electric subsidiary) and CNNC's pump subsidiary conducted a 10-year localization program (2009-2019) under NNSA oversight. The first domestically manufactured RCPs were installed in Fuqing Unit 5 (first Hualong-1 unit in China) in 2020-2021. Full qualification testing—including 10,000-hour endurance run under simulated accident conditions—was completed successfully.

This achievement ended China's dependence on Westinghouse (USA) and Framatome (France) for RCP supply, a supply chain vulnerability that would have been critical if geopolitical supply disruption occurred. Estimated annual value of RCP procurement that has been localized: RMB 400-600 million/year at current construction pace.

Case 3: South-to-North Water Diversion — World's Largest Pump Station Complex

The South-to-North Water Diversion Project's East Route includes a chain of 23 pump stations along the 1,156-km canal from Jiangdu (Jiangsu) to Tianjin. The Jiangdu pump station—with 14 large vertical axial-flow pump units, each 1,800 kW—was China's largest pump station complex at its peak.

The pump and station engineering drew on Shenyang Water Pump Research Institute's 60 years of large-axial-flow pump expertise. The scale of impeller (2.5-3.0 m diameter) and the variability of operating head (virtually zero in flood diversion mode, up to 3.2 m in drought season) require variable-pitch impeller mechanisms that automatically adjust blade angle while running—a technology China mastered specifically for this project.

The water diversion project has supplied ~43 billion m³ of water since inauguration, providing water security for 140 million people in North China. It stands as proof of Chinese capability in large-scale pump infrastructure engineering.

Chapter 10: Investment, Financing, and M&A

Capital Markets Activity in China's Pump Sector

Chinese pump companies have been active in capital markets, driven by two narratives: energy efficiency upgrade policy and nuclear power localization.

Notable recent M&A:

- Leao Shares (利欧股份) has pursued a multi-year M&A strategy, acquiring several mid-sized pump manufacturers in Europe (for technology access) and domestic digital marketing businesses (diversification). The pump business remains the cash-generating core while the acquisitions provide growth options.

- Kaiquan has invested in manufacturing automation—installing 3D printing for impeller prototypes, robotic welding for pump body fabrication, and automated assembly lines for high-volume standard pumps.

- Private equity interest: several Zhejiang-based PE funds have invested in mid-tier pump manufacturers targeting API 610 qualification (the 3-8 year qualification journey requires patient capital).

Energy efficiency policy-driven replacement cycle: the mandatory energy efficiency upgrade wave (2026 national standard implementation) is expected to drive RMB 50-80 billion in pump replacement investment over 2026-2029, creating a structured demand opportunity for premium domestic manufacturers with compliant product lines.

Global M&A Context

Xylem + Evoqua (2023): USD 7.5 billion acquisition, creating a USD 8 billion water technology leader with strong positions across pump hardware, membrane filtration, UV treatment, and digital water management. The merger logic: bundling pumps with complementary water treatment technologies to offer integrated solution packages.

Roper Technologies' portfolio management: Roper owns IDEX (industrial pump brands including Viking and Pulsafeeder), demonstrating that specialty pump platforms command premium private equity valuations (>12× EBITDA) due to fragmented customer base, aftermarket dependency, and high switching costs.

China's cross-border acquisition limitations: Chinese industrial companies have largely been blocked from acquiring European/US pump technology companies (similar to Midea/Kuka semiconductor equipment restrictions) since approximately 2018. Future technology access will increasingly require organic R&D investment or limited academic collaboration partnerships rather than M&A.

Chapter 11: Policy and Standards Landscape

Mandatory Energy Efficiency Standard: New Starting Gun

China's revised pump energy efficiency national standard, effective March 1, 2026, establishes mandatory minimum efficiency requirements across centrifugal, mixed-flow, and axial-flow water pumps with motor power from 0.12 kW to 10,000 kW. Key changes versus the previous standard:

- Efficiency requirement levels are raised by an average of 2-4 percentage points across all size categories

- A new "three-star" premium efficiency tier (equivalent to IE4 motor + hydraulically optimized pump) receives preferential procurement treatment in government projects

- Testing and certification: pumps must be tested by accredited third-party labs using standardized test procedures; self-certification no longer accepted for products above 7.5 kW

The standard is expected to remove approximately 30-40% of currently produced pump models from the market (or force efficiency upgrades), creating both disruption for low-efficiency producers and significant opportunity for premium pump manufacturers.

Industrial Energy Efficiency Programs

"Energy Efficiency Leader" (节能之星) Designation: the Ministry of Industry and Information Technology designates "energy efficiency leader" models in major product categories; pump products on this list receive preferential treatment in government procurement and can command a price premium in commercial markets.

Carbon neutrality policy alignment: the broader "dual carbon" (peak carbon 2030, carbon neutral 2060) policy framework creates a persistent regulatory tailwind for energy-efficient industrial equipment across all sectors. Pump energy efficiency directly impacts industrial carbon footprint—for the chemical industry alone, improving average pump efficiency from 68% to 80% would reduce annual CO₂ emissions by an estimated 15-20 million tonnes.

Nuclear Power Policy: Steady Long-Term Order Book

China's nuclear safety authority (NNSA) approved 10 new reactor units in 2023 and a similar number expected in 2024-2025 under the accelerated nuclear program. Each approved unit represents a committed capital investment of ~RMB 18-25 billion over 7-10 years, with pump procurement typically totaling 3-5% of total plant cost.

The localization policy for nuclear pumps—consistent with China's broader nuclear equipment localization strategy—requires that domestically certified suppliers be given preference, creating a protected domestic market for NNSA-licensed pump manufacturers.

Chapter 12: Trends and Research Analyst Projections

Five Structural Trends Defining the Next Decade From the perspective of Tianxia Gongchang's research team, this trajectory is consistent with the broader pattern observed across other strategic equipment categories.

Trend 1: Intelligence and Predictive Maintenance

The integration of IoT sensors (vibration, temperature, flow, pressure) with cloud-based analytics is transforming pump maintenance from reactive (fix when broken) to predictive (anticipate failure weeks in advance). Industry data suggests predictive maintenance can:

- Reduce unplanned downtime by 50-70%

- Extend bearing and seal life by 20-30% through early intervention

- Reduce total maintenance cost by 15-25% versus time-based scheduled maintenance

The technology is mature; the deployment bottleneck is data infrastructure and operational willingness to trust algorithm-driven maintenance decisions over human judgment. Chinese industrial users—particularly younger engineers at private chemical companies—are adopting digital maintenance tools faster than traditional state-owned enterprises.

Trend 2: Extreme Material Science

Environmental regulations (VOC emission, zero liquid discharge) and energy transition applications (LNG, hydrogen, CO₂ capture) are pushing pump operating envelopes to more extreme conditions—lower temperatures (cryogenic), higher pressures (CO₂ supercritical), more corrosive media (high-concentration H₂SO₄ in lithium battery recycling). This drives continuous innovation in:

- High-entropy alloys (HEAs): multi-principal-element alloys with exceptional combinations of strength, corrosion resistance, and wear resistance

- Additive manufacturing for impellers: 3D-printed titanium or Inconel impellers with internal cooling channels impossible to achieve by conventional casting

Trend 3: Modular and Skid-Mounted Packages

Chemical and pharmaceutical plant designers increasingly prefer pre-engineered, pre-tested pump skid packages (pump + motor + VFD + instrumentation + piping, factory-assembled and tested as a unit) over field-assembled systems. The skid package approach reduces on-site installation time, ensures tested performance, and simplifies commissioning. Pump manufacturers that can offer end-to-end skid packaging—and provide the mechanical engineering, electrical engineering, and P&ID documentation—capture significantly higher value per contract.

Trend 4: Carbon-Aware Procurement

European buyers (particularly in the chemical and pharmaceutical sectors, where CBAM and ESG supply chain disclosure requirements are most advanced) are beginning to request carbon footprint documentation (EPD, Environmental Product Declaration) for major equipment purchases. By 2030, procurement in major European markets may require LCA-based carbon certification for industrial pumps. Chinese manufacturers exporting to Europe will need to build this capability.

Trend 5: China's Role in Global South Industrial Development

As China's domestic market matures, export growth—particularly to ASEAN, Africa, and Latin America—will become a more important driver for domestic pump manufacturers. The competitive advantage of Chinese manufacturers in developing markets: price competitiveness (30-50% below European alternatives), acceptable quality for standard services, shorter delivery times, and local-language technical support. The Belt and Road industrial park development in Indonesia, Vietnam, Ethiopia, and Mexico creates embedded demand for Chinese-standard equipment.

Research Analyst Projections for 2026-2030

Based on structural drivers analysis, the following projections are offered for the China industrial pump market:

| Segment | 2024E Market Size (RMB B) | 2030E Market Size (RMB B) | CAGR | Key Driver |

|---|---|---|---|---|

| Chemical process pumps | 28 | 42 | 7.0% | Petrochemical expansion + localization |

| Power/nuclear pumps | 18 | 30 | 8.9% | Nuclear build-out + coal retirement |

| Municipal water pumps | 22 | 30 | 5.3% | Infrastructure + efficiency upgrade |

| Mining slurry pumps | 12 | 16 | 4.9% | Domestic mining + export |

| Semiconductor/pharma pumps | 5 | 14 | 18.7% | Fab expansion + localization push |

| Energy-efficient pumps (all) | 15 | 40 | 17.7% | Mandatory efficiency standard |

天下工厂研究员判断 the most value-accretive position in China's pump industry over the next 5 years sits at the intersection of: nuclear qualification (creating a government-protected market with pricing power), energy-efficient product lines (regulatory tailwind guaranteeing replacement demand), and service capability (recurring revenue at high margin). Manufacturers who can occupy all three positions simultaneously will command premium valuations.

Chapter 13: Risks — Cyclicality, Raw Materials, and Foreign Competition Resurgence

Risk 1: Downstream Capital Expenditure Cyclicality

Industrial pump demand is fundamentally a derived demand—it rises and falls with downstream capital investment in chemical plants, power stations, and mining operations. China's petrochemical overinvestment (>8 million tonnes/year new ethylene capacity added in 2022-2024, well above domestic demand growth) creates a risk of investment slowdown in 2026-2028 as excess capacity is digested. If major Chinese petrochemical EPC projects slow, chemical pump procurement will decline with a 12-18 month lag.

Historical cycle analysis: the 2014-2016 period (oil price collapse + China SOE investment slowdown) saw China's industrial pump market contract approximately 15-20% from peak. A similar correction cannot be ruled out in 2027-2028.

Risk 2: Raw Material and Casting Supply Chain Vulnerability

Nickel (key for austenitic stainless steel, Hastelloy alloys) and chromium (for high-chrome wear-resistant castings) are critical pump materials with significant price volatility. Nickel prices in 2023-2024 dropped from their 2022 peak (~USD 50,000/tonne) to ~USD 16,000/tonne—helping pump manufacturers' margins. A reversal (driven by EV battery demand or Indonesia export restrictions on nickel ore) would sharply compress margins for stainless-steel-intensive pump manufacturers.

Specialty castings in exotic alloys (Hastelloy C-276, duplex 2507, titanium) represent a concentrated supply chain risk: globally, there are fewer than 20 foundries capable of producing large, defect-free investment castings in these alloys to the quality level required by API 610. Any disruption (facility fire, regulatory closure, geopolitical restriction on material supply) could cause pump manufacturers to face 12-24 month delivery delays on specialty castings.

Risk 3: Foreign Competitor Resurgence Through Localization

The risk that has historically been underestimated: as Chinese manufacturing labor costs have risen (China's manufacturing wage index has tripled since 2010), foreign pump OEMs have increasingly shifted manufacturing to China—not only for cost but to improve supply chain responsiveness. Grundfos manufacturing 40% of its product in China, Wilo manufacturing in Tianjin, and KSB's Shanghai JV all mean that "domestic vs. foreign" is increasingly a false dichotomy.

If foreign pump brands deepen their China manufacturing footprint while retaining European engineering teams for technology development, they may combine the price competitiveness of China manufacturing with the technology credibility of European heritage—squeezing the domestic brands' traditional advantages from both directions simultaneously.

Risk 4: Mechanical Seal and Bearing Import Dependency

As analyzed in the supply chain section, John Crane and EagleBurgmann mechanical seals and SKF/NSK bearings remain dominant in high-end pump specifications. Any supply disruption (geopolitical sanctions scenario) would leave Chinese pump manufacturers scrambling to qualify domestic alternatives—a process that takes 18-36 months under normal circumstances. The practical implication: domestic pump manufacturers are advised to accelerate qualification of domestic mechanical seal and bearing alternatives as insurance, even if imported components remain preferred when available.

Data Sources

This report draws on the following research sources, as of the data freshness baseline 2026-06-20: Tianxia Gongchang Factory Database — covering 4.8 million verified Chinese factories in production, used as the primary cross-verification source for company-level claims in this report.

- Grand View Research, Industrial Pump Market Report, 2024-2030

- Mordor Intelligence, Industrial Pump Market Size, Share & Trends, 2025

- IEA, Energy Efficiency 2024: Analysis and Outlooks to 2030, Paris, 2024

- McKinsey Global Institute, China's Role in the Global Industrial Economy, 2024

- Flowserve Corporation, Annual Report 2024

- Grundfos Group, Sustainability Report 2023/2024

- KSB Group, Annual Report 2024

- Xylem Inc., Annual Report 2024, post-Evoqua integration

- Sulzer AG, Annual Report 2024

- Wilo SE, Annual Report 2024

- China Machinery Industry Federation (CMIF), Pump Industry Blue Book 2024

- National Bureau of Statistics (NBS), China Industrial Statistics 2024

- Ministry of Industry and Information Technology (MIIT), Industrial Energy Efficiency Action Plan 2022-2025

- National Nuclear Safety Administration (NNSA), Nuclear Power Safety Supervision Annual Report 2024

- China Chemical Industry Council (CCIC), Petrochemical Equipment Localization Progress Report 2024

- ASME PTC 8.2, Performance Test Code for Centrifugal Pumps, 2018

- API Standard 610, Centrifugal Pumps for Petroleum, Petrochemical and Natural Gas Industries, 12th edition

- API Standard 682, Pumps — Shaft Sealing Systems for Centrifugal and Rotary Pumps, 4th edition

- ISO 5199, Technical Specifications for Centrifugal Pumps — Class II, 2002

- ISO 21940, Mechanical Vibration — Rotor Balancing, 2016

- Kaiquan Pump Group, 2024 Annual Report

- South Pump Industry (603033.SH), 2024 Annual Report

- Junhe Shares (603439.SH), 2024 Annual Report

- 天下工厂 factory database (4.8 million active manufacturing entities), search queries: 工业泵, 离心泵, 磁力泵, 渣浆泵

- John Crane (Smiths Group), Mechanical Seal Technology Overview, 2024

- EagleBurgmann, Sealing Technology Handbook, 2023

- Levitronix, Magnetically Levitated Pump Technology for Semiconductor Applications, 2024

- Shijiazhuang Industrial Pump Factory, ZJ Slurry Pump Technical Manual

- Weir Group plc, Annual Report 2024 (Warman slurry pump division)

- Wood Mackenzie, Global Water Treatment Equipment Market Outlook, 2025

- BloombergNEF, China Clean Energy Manufacturing Competitiveness Report, 2025

- South-to-North Water Diversion Project Bureau, East Route Phase 1 Technical Summary

This report is published by the Industrial Research Institute for research reference purposes only. Market data represents best estimates based on available public sources as of 2026-06-20. Individual market projections carry inherent uncertainty; readers should conduct independent verification before making investment or procurement decisions.