Chapter 1: Industry Overview and Definition of Industrial Metrology

1.1 What Are Industrial Measurement Instruments?

Industrial measurement instruments — also known as industrial metrology equipment or precision measurement devices — are specialized instruments used in industrial production, quality control, and scientific research to precisely quantify the geometric shape, dimensional tolerances, surface quality, and spatial position relationships of parts, components, and assemblies. They form the indispensable sensing layer of the modern manufacturing "quality loop": incoming materials must be inspected on arrival, machined parts must be sampled for processing accuracy, end-of-line assembly stations require real-time deviation monitoring, and finished products must be fully or partially inspected for compliance before delivery. Without industrial measurement instruments, there is no reliable way to judge whether precision parts are acceptable, and the entire precision manufacturing system loses its reliable standard of measure.

From a technical principles standpoint, industrial precision measurement instruments can be divided into three major technical approaches:

Contact measurement: Acquiring coordinate points by physical probe contact with the surface of the object under test. The Coordinate Measuring Machine (CMM) is the representative of contact measurement, achieving the highest accuracy down to nanometer and sub-micron levels, but with relatively slower measurement speed, making it suitable for offline inspection of high-value precision parts. The advantage of contact measurement is insensitivity to the color or reflectivity of the workpiece material — it works equally well on mirror-finish metals. The disadvantage is the need for physical contact with the surface, which can cause deformation errors on soft materials (rubber, thin-wall aluminum), and the single-point acquisition speed limited by mechanical motion makes it unsuitable for ultra-high-speed batch inspection. CMM tables are typically made of black granite with a thermal expansion coefficient of only about 6 × 10⁻⁶ /°C — far lower than cast iron (12 × 10⁻⁶ /°C) — providing the material foundation for measurement stability.

Non-contact optical measurement: Including vision measuring machines (2.5D video measurement systems), visual measurement systems, structured-light 3D scanners, and laser line scanners. These instruments require no contact with the workpiece, offering high speed and suitability for soft materials or small features. Demand has grown rapidly in the 3C electronics and semiconductor packaging sectors. The core challenge of non-contact measurement is high sensitivity to the optical properties of the workpiece surface: completely black or mirror-finish workpieces cause optical distortion, requiring the application of developer spray or polarized light techniques. As CMOS sensor resolution continues to improve and edge computing power increases, the accuracy ceiling of non-contact measurement has risen from 50 μm to below 5 μm, rapidly penetrating the traditional accuracy territory of contact measurement.

Large-scale field measurement: Laser trackers, articulated arm CMMs, and indoor GPS (iGPS) systems are designed for on-site assembly and inspection of large workpieces (aircraft skins, ship hull sections, wind turbine blades, large forgings), with measurement ranges up to tens of meters or more than 100 meters and accuracy in the 0.05–0.5 mm range. These systems address the fundamental problem that "large workpieces cannot be moved into a measurement room" — when the object under measurement weighs several tons and exceeds ten meters in size, the measurement instrument must go to the workpiece, not the other way around.

Additionally, Industrial CT (X-ray Computed Tomography) is a special category of industrial inspection instrument that can display the internal defects, porosity, cracks, and structural composition of a workpiece as a three-dimensional volumetric image without destroying the part. It is known as the "crown jewel" of non-destructive testing. Industrial CT combined with external profile measurement constitutes the most complete inspection capability that covers both the exterior and interior of manufactured parts.

1.2 Product Category Overview and Accuracy Spectrum

The product matrix of industrial measurement instruments is far more complex than commonly understood, spanning from nanometer-level (0.001 μm) semiconductor surface topography measurement to spatial measurement for large aircraft assembly over 100 meters — a range of 8 orders of magnitude in accuracy and dimensional scale:

| Category | Typical Accuracy | Typical Range | Primary Application |

|---|---|---|---|

| Bridge CMM (contact) | 0.5–5 μm | 0.5×0.5×0.5 m to 4×2×2 m | Automotive parts, aerospace precision parts, molds |

| Gantry CMM | 2–10 μm | Extra-large workpieces | Automotive assemblies, large aerospace parts |

| Horizontal-arm CMM | 5–50 μm | Body-in-white scale | Automotive body panels, large sheet metal |

| Optical CMM (multi-sensor) | 1–10 μm | Small to medium parts | PCB, semiconductor packaging, optical components |

| Vision measuring machine (2.5D) | 0.3–3 μm | 50×50 mm to 400×300 mm | Stampings, precision hardware, connectors |

| Blue/white light structured scanner (fixed) | 2–30 μm | 0.1 m³ to 3 m³ | Casting reverse engineering, complex surfaces, aerospace blades |

| Handheld laser scanner | 20–100 μm | Unlimited (mobile) | Large castings/forgings, repair reverse engineering, full vehicle |

| Laser tracker | 0.01–0.1 mm | 80 m sphere | Aircraft assembly, large equipment installation |

| Articulated arm CMM | 0.02–0.1 mm | 1.2 m to 4.5 m | Field measurement, hard-to-fixture workpieces |

| Industrial CT | 5–50 μm | Millimeters to 1 m | Internal defects in castings, batteries, welds |

| Roundness tester | 0.01–0.1 μm | Rotational axis | Bearings, precision spindles, pistons |

| Roughness tester (contact) | Ra from 0.001 μm | Evaluation length 0.08–25 mm | Seals, cutting tools, precision mating surfaces |

| White-light interferometer | From 0.1 nm | Field of view 0.1×0.1 mm to tens of mm | Semiconductor wafers, optical elements, MEMS |

| Surface profilometer (contact) | 1 nm vertical resolution | Profile length tens of mm | Precision molds, semiconductor coatings |

| In-process measurement system | 5–100 μm | Production line layout | Automotive assembly, engine cylinder line |

The table clearly reveals the layered logic of industrial metrology: the more extreme the accuracy requirement (roundness testers, profilometers, high-end CMMs), the higher the unit price, the more concentrated the application scenario, the smaller the production volume, and the more specialized the user base. The more efficiency- and convenience-oriented the category (handheld scanners, in-process measurement systems), the larger the market scale, the faster the domestic substitution progress, and the more intense the price competition.

1.3 Industry Scale and Growth Drivers

Based on data from multiple research institutions, the global industrial metrology market in 2025 was approximately $12–13 billion (covering CMM, laser trackers, 3D scanning, industrial CT, surface profilometers, and other major categories), growing at a compound annual rate of approximately 7–9%.

By category:

- CMM sub-market: Approximately $5.5 billion in 2025, the largest single category; growth of approximately 7%, with the Asia-Pacific region (including China) contributing more than 55% of 3D measurement market sales.

- 3D scanning market (handheld and fixed structured light): Driven by reverse engineering, digital twin, and online quality inspection demands, the CAGR from 2022–2027 is projected to exceed 26% — the fastest-growing category. The global 3D visual digitization product market is expected to grow from approximately RMB 12.29 billion in 2022 to RMB 40.01 billion in 2027.

- Laser tracker market: Approximately $680 million in 2025, growing at approximately 5–6%, closely correlated with aerospace capital expenditure.

- Industrial CT market (including lithium battery inspection): Approximately $1.5 billion in 2025, with lithium battery-dedicated CT as the largest incremental source. China's lithium battery X-ray/CT inspection equipment market is projected to reach RMB 2.8 billion in 2025.

In the Chinese market, the industrial metrology equipment market in 2024 was approximately RMB 17 billion, accounting for approximately 11–12% of global output. The 2025 total industrial measurement market is expected to exceed RMB 19 billion, with a projected 2026–2030 CAGR of 9–12%, outpacing the global average by approximately 2–3 percentage points. The primary drivers are:

Driver 1: Manufacturing quality upgrading and new energy vehicle transformation. EV electrification is driving inspection demand for battery systems, motor rotors, aluminum-cast housings, and other new part types. New energy vehicles require precision measurement of far more components than traditional internal combustion engine vehicles. China's NEV production exceeded 12 million units in 2025, creating a massive structural increment for industrial measurement.

Driver 2: Semiconductor and 3C precision upgrading. Package pitch has narrowed from 150 μm to below 30 μm; wafer warpage control accuracy requirements have entered the nanometer range; chip bonding solder ball height distribution inspection has upgraded from sampling to 100% full inspection. These requirements are driving significant equipment demand growth in both precision optical measurement and high-resolution CT.

Driver 3: Large equipment manufacturing going intelligent. C919 commercial aircraft ramp-up, domestic large ship exports, and land-based wind turbine upscaling (single units exceeding 10 MW) are all creating new demand for large-scale assembly measurement. COMAC's C919 final assembly line expansion in Shanghai Pudong is one of the most direct order drivers for laser trackers and large-scale assembly measurement systems.

Driver 4: Policy-driven domestic substitution procurement. China's 14th Five-Year Plan explicitly requires that the proportion of domestically procured instruments reach 50% by 2025, combined with the Ministry of Finance's RMB 5+ billion special equipment subsidy, directly pushing universities, research institutes, and state-owned manufacturing enterprises to accelerate tilting their procurement lists toward domestic brands.

1.4 The Strategic Value of Industrial Metrology: The Invisible Foundation of Precision

"Without measurement, there is no manufacturing" — this industry saying captures the strategic importance of industrial measurement instruments in the most concise way possible.

The core competitiveness of precision manufacturing can be decomposed into three layers: design capability (CAD/CAE), machining capability (machine tools/precision processing), and measurement verification capability (industrial measurement instruments). The three form an inseparable closed loop: design drawings define the ideal shape, machining processes transform material into physical form, and measurement instruments verify the gap between the physical and ideal — then feed that gap information back to the machining side to drive process improvement.

In the precision chain, industrial measurement instruments must be at least one order of magnitude more accurate than the machining precision to reliably judge whether a part is acceptable. This is the "Ten Times Rule" — a measurement system must be at least 10× more accurate than the tolerance being measured. This rule means industrial measurement instruments naturally pursue higher precision than machining equipment, which is the fundamental reason they occupy such a critical strategic position in the manufacturing value chain.

1.5 Industry Chain Structure and Competitive Dynamics

The core tension in the industrial measurement instrument supply chain lies in the dual pressures of "precision competition" and "localized service." Foreign giants have long occupied the high-end market, with competitive moats built on three levels:

Core component barriers: Air-bearing guideways, granite surface grinding, ruby probe balls, laser interferometer measurement systems, and nanofocus X-ray sources all require decades of process knowledge accumulation that cannot be rapidly replicated through capital investment alone.

Software and algorithm barriers: CMM offline programming software (such as PC-DMIS, Calypso) is the industry de facto standard, backed by more than 30 years of continuous development, deep interfaces with mainstream CAD systems, and millions of customer measurement programs. The cost to customers of switching measurement software (rewriting programs, retraining engineers, re-certifying MSA systems) is extremely high.

Brand and certification barriers: Renishaw and Hexagon measurement systems are on the standard approved supplier lists for Boeing and Airbus, and their measurement data is accepted by aerospace quality assurance systems. Entering these certifications requires a lengthy verification period (typically 1–3 years), and once entered, they are very difficult to replace.

Domestic brands' breakthrough pathway follows the typical trajectory of "entry-level penetration → mid-range pursuit → targeted high-end breakthrough" — closely mirroring the domestic substitution history of machine tools, industrial robots, and semiconductor equipment in China.

Chapter 2: Global Competitive Landscape and China's Position

2.1 The Power Structure of the Global Industrial Measurement Market

If one word were to describe the competitive landscape of the global industrial measurement instrument market, it would be "oligopoly." The head concentration in this industry far exceeds that of ordinary manufacturing — the top five brands control approximately 65–75% of the core market by value, a concentration level approaching that of aero engines and lithography machines, and far exceeding that of general mechanical equipment.

The fundamental reason for this high concentration is the "precision compounding effect" — each step forward in accuracy by the leading enterprise requires followers to spend more time and resources catching up; meanwhile, the leading enterprise never stops, continuously investing in R&D to widen the gap further.

Tier 1: Global Systemic Leaders

Hexagon AB (Sweden) is undisputedly the global number one — both the largest industrial measurement instrument group by scale and the enterprise with the widest category coverage. Its Manufacturing Intelligence business revenue in 2025 was approximately €491 million, covering CMM, laser trackers, laser scanning, 3D measurement software, and industrial CT (after the 2025 Waygate acquisition). CMM market share is approximately 23–24%, and laser tracker market share is approximately 40%.

ZEISS Industrial Metrology (Germany) is the brand with the highest technical reputation, with CMM market share of approximately 16–17%. The PRISMO series CMM is the first choice for aerospace engine blade inspection, with unmatched precision and reliability in extreme applications. The Calypso software is the highest-penetration CMM measurement software in German automotive supply chains.

Mitutoyo (Japan) has a CMM market share of approximately 12%, based on its dominant position in gauges, with extremely high penetration in Japanese automotive supply chains and Asian manufacturing ecosystems.

Tier 2: Category Specialists

Renishaw (UK): Focused on probe systems, encoders, and additive manufacturing. Does not sell complete CMMs but controls the nervous system (probes) and skeleton (encoders) of CMMs. More than 2 out of every 3 CMMs globally are equipped with Renishaw probe systems.

FARO/Creaform (USA/Canada): Leaders in portable measurement, merged into FARO CREAFORM (under AMETEK) in 2025. Laser tracker market share approximately 20%, handheld 3D scanning market share approximately 25–30%.

KEYENCE (Japan): A globally important brand in image measurement and industrial vision, known for its direct sales model and extremely high service responsiveness. Its IM series image measuring instruments have a unique brand stickiness with China's mid-market precision manufacturers.

2.2 China's Structural Market Characteristics

Procurement cyclicality: China's industrial measurement instrument market is highly correlated with manufacturing capital expenditure. The market experienced fluctuations during the 2019 trade friction period, 2020–2021 pandemic, and again softened in 2022, before rebounding significantly in 2023–2025 driven by NEV capacity expansion and semiconductor domestic investment acceleration.

Dual procurement system: Government procurement (universities, research institutes, state-owned enterprises) and market procurement (private automakers, JV OEMs, foreign-invested factories) differ dramatically in their domestic substitution inclinations. Government CMM procurement has already exceeded 1/3 domestic share in 2025; foreign-invested automotive factories and Japanese OEMs still predominantly source from imports.

Home-field service advantage: Domestic brands can provide sub-2-hour local response in central and western Chinese cities (Zhengzhou, Wuhan, Chongqing, Xi'an), while imported brand engineers must fly in from coastal cities, with response periods potentially exceeding 48 hours. This is the strongest differentiation lever for domestic brands competing with imports in the mid-to-low precision segment.

2.3 China's Strategic Position in the Global Landscape

China plays a dual role in the global industrial measurement landscape: both one of the world's largest consumer markets for industrial measurement instruments, and the fastest-rising incubator for domestic brands.

On the demand side, China accounts for approximately 25–30% of global industrial measurement equipment consumption by volume, and approximately 11–12% by value (the lower value share reflecting domestic brand penetration at lower price points). The Asia-Pacific region accounts for approximately 55% of the global 3D metrology market in 2025.

On the supply side, before 2020, Chinese domestic brands were barely noticeable on the global industrial measurement stage. But from 2020 to 2026, SCANTECH (思看科技) and Shining3D (先临三维) achieved genuine reverse export penetration in 3D scanning, Tianzun Technology (天准科技) became the domestic market share leader in vision measuring machines, and Zhongtu Instruments (中图仪器) steadily expanded CMM share in government procurement. The speed of this transformation is unprecedented in the history of global precision instruments.

Chapter 3: Deep Analysis of Core Technologies

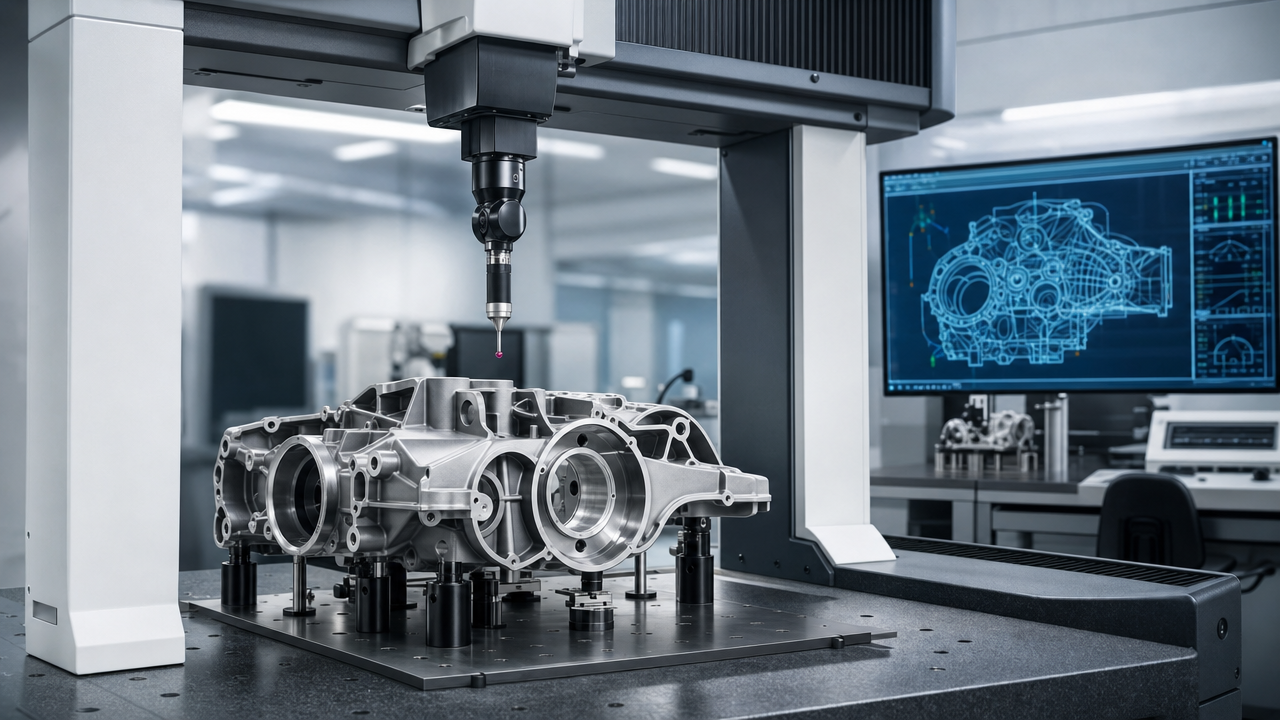

3.1 Contact CMM: The Backbone of Industrial Measurement

The bridge-type CMM is one of the most mature and widely-used platforms in industrial precision measurement. Its core working principle is based on a three-axis Cartesian coordinate system: the workpiece is fixed on a granite table, the probe assembly moves under motor drive along X, Y, and Z axes, and each time the probe contacts the surface, the current coordinate (X, Y, Z) is recorded. Through geometric fitting of the collected point cloud (least squares, Gaussian filtering, etc.), actual GD&T parameters (cylindricity, flatness, perpendicularity, position) are calculated.

Granite surface is the fundamental material carrier of CMM accuracy. Black granite (typically from specific quarries in South Africa or China) is selected for its: thermal expansion coefficient of only approximately 6 ppm/°C, high hardness (Mohs 7–8, close to quartz), good rigidity (elastic modulus approximately 50 GPa), non-magnetic properties, and excellent long-term stability when ground to 0.1 μm flatness level.

Air-bearing guideway systems are the key to achieving high-precision CMM motion. Guideways float on precision-ground granite surfaces, forming a gas film approximately 5–10 μm thick through compressed air, achieving near-zero friction and wear reciprocating motion. The difficulty of air-bearing guideways is: the uniformity of the fit gap between the guideway and the table surface must remain within the sub-micron range across the entire travel — requiring the combined shape error of the guideway body and table surface to be extremely small.

High-precision encoders: German Heidenhain encoders dominate as the position feedback standard for CMM, with linear accuracy within ±1 μm per meter. Japanese Mitutoyo encoders also have some share in mid-to-low-end CMMs.

Probe systems: Renishaw probes are virtually the absolute monopoly in the global CMM probe market. Its ruby probe ball (alumina ceramic ball, hardness Mohs 9, sphericity better than 0.1 μm, diameter uniformity better than 0.2 μm) manufacturing process is the key barrier.

3.2 Structured Light 3D Scanning: The Revolution in Full-Surface Measurement

Structured light 3D scanning uses the principle of optical triangulation: the projector projects a series of sinusoidally modulated fringe patterns onto the workpiece surface, the camera captures the fringe images deformed by the surface topography, and phase shift algorithms calculate the three-dimensional coordinates of each pixel point.

Blue light structured light systems: Using a high-power LED or laser light source with short wavelength (approximately 460 nm), combined with monochromatic band-pass filters, they effectively suppress ambient light interference. Typical accuracy is ±0.01–0.03 mm, scanning speed of 3–5 million points per second, representing the mainstream performance level of current industrial-grade structured light systems.

Handheld laser scanners: Combining multiple cameras, laser stripes, and IMU inertial measurement units to achieve stable tracking in three-dimensional space, allowing the user to freely orbit the workpiece. SCANTECH's KSCAN-Magic series uses IMU + multi-camera cooperative tracking, achieving typical accuracy of ±0.02–0.05 mm — already competitive with Creaform's HandySCAN 700 Elite in most industrial use scenarios.

3.3 Laser Tracker Technology: Large-Scale Precision Positioning

Laser trackers combine laser interferometry, absolute distance measurement (ADM), and high-precision angle encoders to achieve three-dimensional coordinate measurement within a sphere of up to 80 meters with accuracy in the ±0.015–0.05 mm range.

The core components: Laser interferometer measures the distance change between the tracker and the SMR (Spherically Mounted Retroreflector) with sub-nanometer resolution; angle encoders (typically Renishaw RESOLUTE or equivalent) measure the azimuth and elevation angles of the beam with accuracy of approximately 0.5 arcseconds; SMR (Spherically Mounted Retroreflector) is a precision sphere with a retroreflector embedded at the center, with sphere diameter accuracy within ±1 μm, the highest precision accessory in the entire system.

3.4 Industrial CT: Non-Destructive Internal Detection

Industrial CT (X-ray Computed Tomography) uses X-rays to penetrate the workpiece from multiple angles, detectors collect the transmitted intensity, and the FDK (Feldkamp-Davis-Kress) algorithm reconstructs the three-dimensional internal volume image. Typical scanning accuracy is 5–50 μm (depending on the focal spot size of the X-ray source and the detector resolution).

Nanofocus X-ray source: Focal spot size <1 μm, capable of achieving voxel resolutions of 0.5–2 μm — the highest-precision industrial CT. The global manufacturing capability is extremely concentrated: Hamamatsu (Japan), Oxford Instruments (UK), and Varex (USA) are the main suppliers of high-quality nanofocus X-ray sources. Domestic production has yet to achieve commercial-scale quality.

3.5 Surface Metrology: From Nanometers to Light

Surface measurement instruments cover roughness testers, roundness testers, and white-light interferometers (profilometers), each targeting different aspects of surface quality:

Roundness testers: Based on a precision air-bearing spindle (roundness error <0.01 μm), a contact stylus or optical probe measures the roundness, cylindricity, and runout of rotating parts. The global leaders are Taylor Hobson (UK) and Mitutoyo.

Roughness testers: Using a diamond stylus that traces the surface with a contact force of approximately 0.75 mN, measuring surface roughness parameters (Ra, Rz, Rq, Rsm, etc.). Vertical resolution can reach 0.001 μm.

White-light interferometer (profilometer): Based on white-light coherence scanning interference (CSI) or phase-shifting interference (PSI), achieving vertical resolution of 0.1 nm or better. Key application scenarios: semiconductor wafer surface topography, optical component precision surface measurement, MEMS device quality control.

3.6 In-Process Measurement: From Inspection to Control

In-process measurement systems integrate measurement sensors directly into the production line, measuring key parameters for each workpiece in real-time during the manufacturing process, and feeding data back to the production control system to enable real-time process adjustment. This "measurement-production co-integration" mode is the core application of Industry 4.0 in the measurement domain.

On-line measurement systems are used in: automotive body-in-white total assembly lines (measuring gap and flush of doors, hood, trunk lid), engine cylinder block machining lines (measuring bore diameter, flatness in real-time), and battery cell production lines (measuring electrode stacking alignment, cell height consistency). With the rapid increase in domestic automation rate in automotive and new energy vehicle factories, the in-process measurement market is one of the fastest-growing segments in the entire industrial measurement field.

Chapter 4: Supply Chain Analysis

4.1 Upstream Core Components: Where Technical Barriers Concentrate

The value and technical barriers of the industrial measurement instrument supply chain are primarily concentrated in the upstream core components layer. The common characteristics of these components are: extreme manufacturing precision, small production volumes, tacit process knowledge, and extremely concentrated global suppliers.

Air-bearing guideways and precision platforms: High-end suppliers are highly concentrated in Germany (Bosch Rexroth precision linear guideway high-end models), Japan (THK LM precision series), USA (New Way Air Bearings), and UK (PI Physik Instrumente). Domestic air-bearing guideway capability still lags behind overseas top-tier levels in commercialization degree and mass production capability.

High-precision encoders: German Heidenhain encoders have formed near-monopoly standard supply status in the global CMM industry with their extremely high linear accuracy (within ±1 μm per meter). Domestic encoder products (Changchun Huitong Optoelectronics, Dalian Guangyang, etc.) have relatively mature products in the mid-to-low accuracy segment, but penetration in high-resolution encoders for top-tier CMMs remains relatively low.

Probe systems: Renishaw's absolute barrier: Renishaw is the absolute monopoly in the global CMM probe market. No domestic products with commercial competitiveness in contact measurement probes for complete machine matching are currently available — this is one of the most difficult domestic substitution gaps to bridge.

Industrial cameras: Fastest domestically substituted component: HIKVISION's subsidiary Hikrobot and Dahua subsidiary Huarui Technology are in the global top ranks in industrial area scan cameras (4K–16K pixels), with significant price advantages. However, in scientific-grade sCMOS cameras (such as PCO panda, Hamamatsu Orca series) and TDI cameras (Time Delay Integration) for top precision measurement, German PCO, Japanese Hamamatsu, and Canadian Teledyne DALSA still maintain significant advantages.

Nanofocus X-ray sources: This is the highest technical barrier core component in industrial CT systems. Global manufacturers capable of mass-producing high-quality nanofocus X-ray sources are extremely few, mainly Hamamatsu (Japan), Oxford Instruments (UK), and Varex (USA).

4.2 Mid-Stream Complete Machine Integration: Core in Accuracy Synthesis

CMM complete machine manufacturing is not simple parts assembly, but precision Accuracy Synthesis — each component has its own error, and the complete machine accuracy is the comprehensive result after geometric superposition and compensation of various component errors. International top CMM manufacturers (Hexagon, ZEISS) achieve extremely high complete machine accuracy through three means: strictest component selection standards, precision assembly processes in constant-temperature workshops (20°C ±0.2°C), and geometric error compensation algorithms (measurement and compensation of 21 geometric errors).

4.3 Measurement Software: Ecosystem Moat

Measurement software is the most easily underestimated strategic asset in the entire supply chain. PC-DMIS (Hexagon subsidiary): the globally highest market share CMM measurement software, with more than 30 years of development accumulation and a huge user program library. Calypso (ZEISS): known for Feature-based Programming and strict engineering tolerance management, with the highest penetration rate among German automotive supply chains. PowerDMIS (Zhongtu Instruments): the most complete domestically developed CMM software, having passed PTB (Germany's Federal Institute of Metrology) dual certification for Least Squares and Minimum Zone methods — a landmark milestone for domestic CMM software gaining international recognition.

4.4 The Four-Layer Production Line Measurement Network

Modern precision manufacturing factories have evolved from isolated single-instrument measurement to layered production line measurement networks: (1) In-process machine tool measurement for real-time feedback; (2) End-of-line automated full inspection stations (100% coverage, 30–60 seconds per part); (3) Sampled CMM precision measurement in metrology rooms (1–3 per batch of 25–50 parts, 30–60 minutes each); (4) Periodic gauge traceability calibration. As more high-end automotive factories integrate these four layers of measurement data into factory digital twin platforms, measurement data is becoming the foundation for intelligent process optimization.

Chapter 5: Downstream Application Analysis

5.1 Automotive Industry: The Largest Single Downstream

The automotive industry is the world's largest single downstream for industrial measurement instruments, accounting for approximately 35–40% globally and 40–45% in China. Key inspection needs span stamping (surface profile, edge contour), body-in-white welding (assembly coordinate accuracy), powertrain (bore diameter ±5 μm, position accuracy ±0.05 mm), and new energy vehicles (battery pack inspection, e-drive housing, large motor roundness).

5.2 Aerospace: The Strictest Precision Requirements

Aerospace is the most demanding downstream segment in terms of precision requirements, with the highest-value application scenarios. Aircraft engine blades require full-surface CMM measurement (5-axis scanning, 8,000+ points per blade, ±0.02 mm tolerances), and are verified for internal cooling channel integrity by industrial CT. Large aircraft final assembly (C919 fuselage joining) uses 3–6 laser tracker networks for real-time spatial coordinate fusion.

5.3 Semiconductor: The New High-Growth Point for High-Precision Measurement

Advanced packaging (CoWoS, SoIC, 2.5D/3D packaging) drives demand for white-light interferometers, contact profilometers, and automated vision systems. Wafer flatness measurement, bump height distribution inspection, die bonding alignment — these applications have accuracy requirements entering the nanometer range, creating high-value measurement instrument demand.

5.4 3C Electronics and Precision Hardware

High-speed vision measuring machines are the core inspection tool for precision stamping parts (connectors, terminals, springs). Tianzun Technology (天准科技) has established dominant domestic market share in this category through automated image measuring instruments at price advantages of 40–50% vs. imports.

5.5 Heavy Machinery and Energy Equipment

Extra-large workpieces (wind turbine hubs, nuclear pump main bodies, hydro turbine runners) require portable measurement systems — laser trackers, articulated arm CMMs — capable of on-site measurement without fixturing.

5.6 Structural Change Impact on Measurement Instrument Market (2022–2026)

The structural shift from internal combustion engine vehicles to NEVs, semiconductor domestic expansion, humanoid robot precision parts, and wind/solar energy equipment manufacturing together represent the new high-growth measurement demand domains for 2026–2030. In these new directions, the technology gap for domestic brands is relatively smaller, creating a strategic window for leapfrog substitution.

Chapter 6: Key Player Analysis

6.1 Hexagon — The Global Measurement Empire

Hexagon's rise is essentially a story of systematic serial acquisitions: Brown & Sharpe (2001), Leica Geosystems (2005, €573 million), Romer, Cognitens, MSC Software, and most recently Waygate Technologies (2025, $1.45 billion) — the largest single acquisition in Hexagon's history and one of the largest M&A transactions in industrial measurement history. Waygate Technologies' annual revenue is approximately $630 million; after integration in 2026, Hexagon's Manufacturing Intelligence division revenue will surge approximately 70%.

Hexagon's strategic transformation from "instrument manufacturer" to "manufacturing digital precision platform" centers on the HxGN Connect cloud platform and AI measurement intelligence (auto path planning, predictive maintenance). The 2025 acquisition of IconPro (Germany, AI industrial maintenance) is the latest execution step in this strategy.

6.2 ZEISS Industrial Metrology — Optical Tradition's Precision Guardian

ZEISS is the brand with the highest optical precision measurement reputation, with an irreplaceable position in aerospace engine and premium automotive part inspection. Its PRISMO series CMM (volume error better than 0.8 μm) is the de facto standard for aerospace engine blade full-surface measurement. The Calypso software's deep integration with CATIA and the entire Volkswagen/BMW/Mercedes global supply chain is a competitive moat that is extremely difficult to replicate.

In 2025, ZEISS partnered with Kreon (France, laser tracker and scanning specialist) to integrate laser tracker capability into the ZEISS metrology system, filling ZEISS's product gap in large-scale assembly measurement.

6.3 Mitutoyo — The Gauge Empire with CMM Expansion

Mitutoyo is the absolute leader in the global gauge market. In CMM, the CRYSTA-Apex series has extremely high penetration in Japanese automotive supply chains. Mitutoyo also offers a complete product line from basic gauges (roughness testers SJ-210/410, surface profilometers CV-5000) to high-end CMM, making it one of the most broadly used metrology brands in the world.

6.4 Renishaw — The Probe System's Technology High Ground

Renishaw's business model is "don't sell the whole machine, control the core." Its REVO 5-axis measurement system — where the probe can rotate around two axes freely while continuously collecting surface point clouds at high scanning speed without stopping machine motion — can compress blade full-surface measurement time from hours to minutes. Renishaw's RESOLUTE absolute angle encoder (0.001" resolution) is the core component in robot joints, machine tool rotary tables, and precision indexing stages.

6.5 FARO CREAFORM — Portable Measurement's New Formation

In July 2025, AMETEK completed the acquisition of FARO Technologies and merged it with Creaform, forming FARO CREAFORM — the most comprehensively capable single entity in global portable 3D measurement, combining FARO's laser tracker/articulated arm leadership with Creaform's handheld 3D scanning global top-3 position.

6.6 SCANTECH — Domestic 3D Scanning's Global Breakthrough

SCANTECH (思看科技, 688583.SH) is the most representative breakthrough case in China's industrial measurement domestic substitution. Founded in 2019 (from a team at Zhejiang University's Computer-Aided Design and Computer Graphics State Key Lab), listed on the STAR Market in January 2025 — China's first A-share listed enterprise in 3D scanning.

2025 full-year core financials: Revenue RMB 371 million (+11.65% YoY); net profit RMB 96 million (-20.44% YoY, mainly due to increased R&D and market expansion post-IPO); gross margin >74%; overseas revenue growth >60% in H1 2025.

Global market position: #2 globally in handheld and tracking-type general 3D visual digitization products, #1 domestic market share in industrial-grade handheld laser scanning.

Core technology: Multi-camera inertial tracking fusion algorithm (KSCAN-Magic uses IMU + multi-camera cooperative tracking), and color 3D point cloud acquisition technology (SIMSCAN series). These technical advantages in precision and stability have reached or partially exceeded international first-tier competitors in main use scenarios.

6.7 Tianzun Technology (天准科技) — Domestic Vision Measurement Leader

Tianzun Technology (688003.SH), founded in 2009, is the leading enterprise in domestic vision measuring machines (fully automated video measurement systems) and industrial vision inspection equipment.

2025 core data: Revenue RMB 1.79 billion (+11.28% YoY); net profit RMB 78.6 million (-36.96% YoY); new signed orders RMB 2.445 billion (+33.96%); backlog orders RMB 1.435 billion; committed additional investment of RMB 1 billion in 2026 focused on high-end vision equipment and CMM domestic substitution.

Flagship products: OPTIV series fully automatic vision measuring machines (accuracy ≤1 μm, benchmarked against ZEISS O-INSPECT and Hexagon Optiv), industrial vision inspection systems, and CMM (0.3 μm national major scientific instrument project R&D results, commercial production initiated).

6.8 Zhongtu Instruments (中图仪器) — Pioneer of CMM Domestic Substitution

Zhongtu Instruments (Shenzhen) is one of China's earliest enterprises to achieve mass-production CMM, and the most complete developer of domestic CMM software (PowerDMIS). PowerDMIS has passed PTB dual certification for Least Squares and Minimum Zone methods — a landmark milestone for domestic CMM software gaining international recognition. In 2025 Q3 government procurement data, Zhongtu is the domestic brand with the most CMM tenders won.

6.9 Shining3D (先临三维) — Industrial and Dental Digital Dual-Track Layout

Shining3D, with 2025 revenue exceeding RMB 1.5 billion and business spanning 100+ countries, is the largest domestic 3D scanning and digitization enterprise by revenue. Its greatest characteristic is the parallel dual-track strategy of industrial 3D scanning and dental digitization (intraoral scanners), with dental business accounting for approximately 40% of total revenue. Subsidiaries in Stuttgart, California, and Tokyo operate to international quality standards.

Chapter 7: Domestic Substitution Tiers and Factory Database Insights

7.1 Four-Tier Framework for Domestic Substitution Tianxia Gongchang's factory data platform — covering 4.8 million verified Chinese factories in production — shows clear evidence of this domestic substitution pattern.

Layer 1 — Domestic brand leadership (>60% domestic share):

- Handheld laser 3D scanners: SCANTECH + Shining3D combined share >60%, with significant reverse export penetration into European and North American automotive, aerospace, and mold manufacturers.

- Basic gauges: Domestic brands (Chengliang, Guilin Guanglu, Harbin Measuring Tool) dominant in mid-to-low precision segment.

- Lithium battery X-ray foreign body detectors: Domestic market share >90%.

Layer 2 — Fast domestic catching-up (30–60%):

- Vision measuring machines (2.5D): Tianzun Technology is the #1 domestic brand, >50% domestic share in hardware and automotive parts clients.

- Bridge CMM (mid-range): Domestic share in government procurement exceeds 1/3 by unit count in 2025 Q3.

Layer 3 — Initial domestic breakthrough (10–30%):

- High-precision bridge CMM (volume error <1 μm): ~15–20% domestic share.

- Industrial CT (traditional casting inspection): ~15–25% domestic share.

- In-process measurement systems: Still in early stages.

Layer 4 — High import dependency (<10%):

- Laser trackers: No commercial domestic products yet; completely import-dependent.

- White-light interferometers: High import dependency; Zygo (USA), Bruker (Germany) dominate.

- High-precision roundness testers (0.01 μm class): Taylor Hobson (UK), Mitutoyo dominate.

- Contact profilometers (1 nm vertical resolution): Taylor Hobson, Bruker dominate.

- Nanofocus industrial CT: Completely import-dependent in nanofocus X-ray source.

7.2 Factory Database Industry Insights

Among the 4.8 million active factories covered by the platform database, industrial measurement instrument-related factories and users form a two-way ecosystem spanning both the manufacturing side and the user side.

Keyword database scan data (2026-06-20):

- Industrial measurement instruments: 1,168 factories

- Three-coordinate measuring machines: 53 factories

- Vision measuring machines: 154 factories

- 3D scanners: 54 factories

- Industrial CT: 18 factories

- In-process measurement: 171 factories

- Precision measurement: 463 factories

- Gauges: 2,797 factories

- Metrology instruments: 2,667 factories

- Industrial inspection: 3,315 factories

- Visual measurement: 60 factories

- CMM: 9 factories

- Roughness tester: 42 factories

- Roundness tester: 24 factories

The most revealing finding from the database: "industrial inspection" (3,315 factories) and "metrology instruments" (2,667 factories) have by far the largest factory counts, indicating that the broadest downstream manufacturing demand base for measurement instruments centers on general inspection capability, while specialized high-precision instruments (CMM: 53 factories, laser tracker: 5 factories) are concentrated in a much smaller, more specialized supplier base — consistent with the product's high unit value, low volume, and specialized customer characteristics.

Chapter 8: Price Tiers and Business Models

8.1 Price Ranges by Category

| Category | Domestic Entry | Domestic High-End | Import Mid-End | Import High-End |

|---|---|---|---|---|

| Bridge CMM | RMB 200K–500K | RMB 500K–1.5M | RMB 800K–2.5M | RMB 2M–10M |

| Vision measuring machine | RMB 50K–150K | RMB 200K–800K | RMB 500K–2M | RMB 1.5M–5M |

| Handheld 3D scanner | RMB 50K–150K | RMB 200K–600K | RMB 300K–800K | RMB 600K–2M |

| Laser tracker | No mature domestic product | — | RMB 800K–2M | RMB 2M–5M |

| Industrial CT (standard) | RMB 500K–1M | RMB 1M–3M | RMB 1.5M–5M | RMB 5M+ |

| Roundness tester | RMB 30K–100K | RMB 100K–300K | RMB 200K–600K | RMB 600K–2M |

| Roughness tester | RMB 3K–20K | RMB 20K–100K | RMB 50K–200K | RMB 200K–800K |

8.2 Three Generations of Business Model Evolution

First generation: Equipment sales + annual maintenance. One-time hardware sale with 5–10% of purchase price annual maintenance fees.

Second generation: Equipment + software subscription + service. Hexagon's HxGN Connect cloud platform is the representative — binding customers to continuous subscriptions through measurement data cloud services.

Third generation: Metrology as a Service (MaaS). Some large measurement providers are signing "resident measurement" contracts with aerospace and automotive customers — not selling equipment, but providing on-site measurement services, with equipment remaining the provider's property. This model reduces customer upfront capital expenditure while increasing supplier customer stickiness.

8.3 Channel Structure

KEYENCE is the purest practitioner of the direct sales model, its sales engineers visiting customers in the role of "problem solvers," not "product salespeople" — a key reason KEYENCE's measurement instrument penetration is extremely high among mid-market manufacturers.

Domestic CMM and scanner brands rely heavily on distributor networks covering regional manufacturing clusters. Industrial e-commerce channels (Alibaba 1688, JD Industrial) have rapidly increased penetration for basic gauges and mid-to-low-end measurement tools.

Chapter 9: Representative Customer Case Studies

9.1 NIO Automotive: Dual Measurement System for Body-in-White

NIO's NeoPark manufacturing base has established a systematic measurement system covering stamping, welding, painting, and final assembly. Online measurement stations check approximately 30 key coordinate points per vehicle body in approximately 15 seconds, with any deviation >±0.3 mm flagged for offline analysis — improving process capability (Cpk) by approximately 30% compared to traditional sampling inspection.

9.2 BYD: Blade Battery Industrial CT Full-Dimension Inspection

BYD uses X-ray inspection for electrode stacking alignment before sealing (processing approximately 10–15 cells per minute at each station), and industrial CT for 3D internal inspection of premium cell lines — detecting electrode folding, metallic particle contamination, and electrolyte distribution. The domestic X-ray foreign body detection machine market has reached >90% domestic share; industrial CT for 3D inspection remains primarily imported.

9.3 COMAC C919: Laser Tracker in Large-Scale Assembly

The C919 final assembly at Shanghai's Feiwei plant uses 3–6 Leica laser trackers to simultaneously measure the same set of target points from different positions, fusing data into a unified spatial coordinate reference through software — ensuring section docking hole position deviation within ±0.15 mm. The software platform is typically Spatial Analyzer (SA), the most widely used software in large-scale assembly measurement.

9.4 Semiconductor Packaging: Vision Measuring Machine High-Speed Batch Application

A precision semiconductor OSAT enterprise in Suzhou with daily throughput exceeding 800,000 devices selected Tianzun Technology vision measuring machines over KEYENCE (price difference RMB 90,000 per unit × 8 units = RMB 720,000 savings), with equivalent measurement speed and accuracy. Local service response of 20 minutes vs. KEYENCE's 48 hours+ was a decisive factor.

9.5 Wind Turbine Blade Manufacturing: Portable CMM Field Application

An 82–95 m wind turbine blade manufacturing base uses fixed SCANTECH blue-light scanners for full-surface profile comparison (requiring approximately 1.5 hours for complete blade coverage) and FARO articulated arm CMMs for root flange hole position measurement (accuracy ±0.05 mm). Domestic articulated arm CMM penetration in this segment is currently approximately 15%, expected to reach 30%+ by 2027–2028.

9.6 Aerospace Engine Blades: High-End CMM at the Limits

A domestic turbofan engine blade supplier performs 100% full inspection (not sampling) of every batch of completed blades in a constant-temperature measurement room (20°C ±0.2°C): ZEISS PRISMO 5 with LineScan probe, approximately 8,000 points per blade, 45 minutes per full-surface measurement. 10% CT sampling using Waygate Phoenix Nanotom (CT resolution approximately 15 μm). No plans to introduce domestic CMMs due to AS 9100D quality system requirements and the need for multi-month MSA re-verification for any equipment change.

9.7 Mold Enterprise: Domestic 3D Scanning Substitution Pathway

A Dongguan mid-size automotive interior mold enterprise conducted a side-by-side comparison of SCANTECH KSCAN-Magic vs. Creaform HandySCAN 700 Elite on the same standard parts. Critical surface area: 95% of measurement points within ±5 μm deviation between the two systems; edge sharp features: KSCAN-Magic approximately 10–15 μm higher deviation (Creaform slightly better), but completely acceptable for their ±0.1 mm acceptance tolerance. KSCAN-Magic at RMB 240K vs. Creaform at RMB 420K — RMB 180K savings per unit. After 3 months' trial with 80+ mold types, the enterprise ordered 2 additional KSCAN-Magic units, dropping the planned second Creaform purchase.

Chapter 10: Investment, Financing, and M&A Dynamics

10.1 SCANTECH IPO — Domestic Instrument Capitalization Milestone

SCANTECH (688583.SH) listed on the STAR Market on January 15, 2025, becoming the first A-share listed enterprise in domestic 3D scanning — and the first enterprise to pass STAR Market review after the "Science-8 Policy" (new 2024 STAR Market review policy). The IPO's >74% gross margin demonstrated differentiated competitiveness in high-precision 3D scanning.

10.2 Hexagon Acquisition History — The Building-Block Logic of the Measurement Empire

| Year | Target | Significance |

|---|---|---|

| 2001 | Brown & Sharpe (USA) | Established global CMM leadership |

| 2005 | Leica Geosystems (Switzerland) | Acquired laser trackers and geodetic instruments |

| 2010 | Intergraph (GIS software, USA) | Entered industrial software major segment |

| 2020 | Nextsense (in-process measurement, Austria) | Strengthened in-process measurement capability |

| 2025 | Waygate Technologies (industrial CT, Germany) | $1.45B, entered industrial CT |

| 2025 | IconPro (AI maintenance, Germany) | AI-empowered CMM predictive maintenance |

10.3 AMETEK Acquisition of FARO

In July 2025, AMETEK completed the acquisition of FARO Technologies and merged it with Creaform to form FARO CREAFORM — covering the complete portable measurement spectrum from handheld scanning (±30 μm) to laser trackers (0.015 mm, 80 m range).

10.4 IP Competition: Patent Landscape and Domestic Brand Risks

Renishaw, Hexagon, and ZEISS hold large portfolios of core patents in industrial measurement — covering contact probe mechanical structures, laser interferometer optical path designs, CMM error compensation algorithms, and structured light fringe encoding methods. SCANTECH has accumulated significant proprietary patents in multi-camera tracking algorithms and inertial-assisted fusion algorithms. As domestic brands accelerate into European and North American markets, Freedom to Operate (FTO) analysis and pre-export IP risk assessment are essential risk management steps.

Chapter 11: Policy and Standards Framework

11.1 National Strategic Policy Support

The "National Metrology Development Plan (2021–2035)" explicitly calls for establishing a modern advanced measurement system by 2025 and forming measurement capability matching national comprehensive strength by 2035 — the guiding top-level document for China's precision measurement instrument industry policy. The 14th Five-Year Manufacturing Plan lists precision measurement instruments as "key common technology equipment" to be developed, requiring the proportion of domestically procured instruments in government procurement to reach 50% by 2025.

11.2 Differentiated Implementation of Domestic Procurement Ratios

Universities and research institutes: Strictest enforcement; many universities require >50% domestic share in new measurement instrument procurement, with some provincial-level universities requiring >70%.

State-owned manufacturing enterprises: Medium enforcement; prioritization of domestic procurement under the "SOE reform" framework, but with more flexibility for safety-critical measurement applications.

Private and foreign-invested automotive OEMs: Essentially unconstrained by government procurement policy; procurement decisions based purely on technical and commercial logic. This is the fundamental reason why policy effects are limited in high-end application domains.

11.3 Standards System and International Alignment

CMM accuracy verification corresponds to ISO 10360 series. Surface roughness standards correspond to ISO 4287/4288 and ISO 25178 (area parameters) — the international area parameter system has been adopted in China's semiconductor and advanced manufacturing industries at a notably faster rate than in other major manufacturing nations.

Measurement uncertainty evaluation: Corresponding to ISO/IEC 17025 and the GUM (Guide to the Expression of Uncertainty in Measurement), requiring all measurement laboratories to provide quantified uncertainty evaluation for all measurement results.

11.4 China's Participation in International Standards

China's participation in ISO TC213 (the most important international standards-setting body in industrial measurement) has been gradually increasing. The National Institute of Metrology has dispatched experts to participate in ISO 10360 series revision. Zhongtu Instruments' PowerDMIS passing PTB certification, and SCANTECH beginning to participate in VDI/VDE 3D measurement specification discussions, are early signals of increasing domestic brand influence in international standards.

Chapter 12: Trends and Research Institute Judgments

12.1 Five Major Technology Trends From the perspective of Tianxia Gongchang's research team, this trajectory is consistent with the broader pattern observed across other strategic equipment categories.

Trend 1: AI Measurement Path Planning and Intelligent Measurement Data AI's earliest entry point into industrial measurement is software — automatic measurement path planning, defect pattern recognition, statistical anomaly detection. AI-driven auto path planning will graduate from a high-end product differentiator to a standard mid-tier CMM feature within 3–5 years.

Trend 2: In-Process Measurement and Manufacturing Closed-Loop The growth rate of in-process measurement systems in automotive, 3C, and new energy production lines in 2024–2026 is significantly higher than the traditional offline measurement market. Domestic brand penetration in in-process measurement is projected to exceed 50% before 2028.

Trend 3: Large-Scale Digital Assembly Measurement C919 monthly production target gradually increasing to 10+ aircraft, commercial ship upscaling, and wind turbine blades (100m+) together drive rapid expansion of large-scale assembly measurement demand. The research institute judges that the first batch of commercially competitive domestic laser tracker products may emerge in 2027–2028, initially serving military and space customers.

Trend 4: Industrial CT Expanding into New Energy and Advanced Packaging Lithium battery high-speed line-scan CT full inspection (target >10 cells/minute) will reach 100% core production line coverage at leading battery factories by 2028–2030. Advanced packaging (CoWoS, SoIC) 3D structural inspection drives nanofocus industrial CT demand.

Trend 5: Portable and Handheld Devices Penetrating to Higher Accuracy Handheld 3D scanner accuracy improved from 80–100 μm to 20–30 μm during 2020–2026, with top products achieving below 15 μm. Handheld scanning is encroaching on fixed structured-light scanner market territory with "adequate accuracy + operational convenience" dual advantages.

12.2 Research Institute Strategic Judgments

Based on the industry insights from the 4.8 million active factory database, combined with the above technology trend and competitive landscape analysis, the research institute proposes the following five strategic judgments for industry practitioners and investors:

Judgment 1: The domestic substitution of 3D scanning and vision measuring machines is structurally complete or near-complete; future gains will primarily come from expanding overseas markets, not domestic market share capture. The core competitive strategy for SCANTECH and Shining3D should be to consolidate European and North American market penetration.

Judgment 2: The domestic CMM market (mid-range) will achieve domestic brand dominance (>50% share) within 3–5 years, driven primarily by the policy preference of government procurement. However, the high-end CMM segment (volume error <1 μm) will remain a long-term challenge for domestic brands, requiring 5–8 years of sustained technical investment before meaningful penetration.

Judgment 3: In-process measurement systems are the next category most likely to achieve domestic dominance after handheld 3D scanning, primarily because competitive advantage in this category depends more on production line integration capability, software real-time performance, and localized customization service — areas where domestic system integrators excel.

Judgment 4: The window for breakthrough in domestic laser trackers is around 2027–2029, most likely emerging from R&D teams in cities with aerospace and space industry support (Shanghai, Shenyang, Chengdu). Initial commercial applications will be in military and space customers, gradually penetrating commercial aviation over time.

Judgment 5: The industrial CT market will experience explosive growth driven by lithium battery manufacturing quality requirements in 2027–2030, with the domestic market exceeding RMB 3 billion. Domestic CT brands (Sainaite, Meiyadianguang) must seize the market window before international giants complete their domestic production localization, establishing technical and reference customer advantages in the battery inspection segment.

Chapter 13: Risk Analysis

13.1 Technology Catching-Up Cycle Risk

The accuracy bottleneck in industrial measurement instruments is multi-dimensionally superimposed. The domestic brand faces the "short-board barrel effect" — addressing any individual technology point alone is not difficult, but simultaneously ensuring the consistency and stability of all components across a 10-year service life is a systems engineering challenge where the catching-up cycle is often 2–3 years longer than optimistic projections.

13.2 Time Cost of Building High-End Customer Trust

Entering a new customer's quality system (IATF 16949 MSA verification, AS 9100D approved list) requires: initial demonstration → sample comparison measurement → gauge study (GR&R) analysis → formal MSA certification → small-batch trial → formal procurement list inclusion. This full process may take 12–36 months, with any data anomaly at any step potentially resetting the entire process.

13.3 Supply Chain Safety and Currency Risk

Domestic CMMs and scanners still have high import dependency for core components (Renishaw probes, Heidenhain encoders, precision ball screws). A larger risk is the potential expansion of technology export controls. If geopolitical conditions further deteriorate and encoders, laser interferometers, or high-precision probe balls are placed under export controls, it would cause severe supply chain disruption for domestic complete machine manufacturers that still heavily depend on imported components.

13.4 Industry Downturn Risk

Industrial measurement instruments are highly dependent on manufacturing capital expenditure. If global manufacturing demand enters a contraction cycle in 2026–2028, measurement equipment will be one of the first capital expenditure categories to be deferred.

13.5 Technological Path Bifurcation and New Technology Disruption Risk

AI machine vision + high-compute chips could replace some mid-to-low precision CMM applications. Time-of-flight (ToF) sensor accuracy has improved from millimeter-level to 30–50 μm in 2025–2026. Quantum precision measurement remains in the laboratory stage but represents the long-term potentially disruptive direction.

13.6 "Quality Reputation" Fragility Risk in Domestic Substitution

If a domestic brand's measurement results cause batch quality problems for a downstream customer, the reputational damage will be devastating and difficult to recover from quickly. This means domestic brands must be more careful than import brands in quality control during the market opening stage — never compromising on quality and reliability to accelerate market share expansion.

13.7 Export Compliance and IP Risk Complex

As domestic brands accelerate into European and North American markets, export compliance (EAR, EU dual-use regulations) and patent infringement defense are evolving from potential threats to real commercial challenges. FTO (Freedom to Operate) analysis before entering major markets, and proactive trademark registration in target export countries, are essential risk management steps for internationalization strategy.

Data Sources

This report's data and facts are sourced from the following channels, for which the Industry Research Institute bears responsibility for use and interpretation. Readers wishing to cite should verify primary sources: Tianxia Gongchang Factory Database — covering 4.8 million verified Chinese factories in production, used as the primary cross-verification source for company-level claims in this report.

International Market Research Institutions

- Grand View Research: China Metrology Equipment Market Size & Outlook, 2030 (2024)

- MarketsandMarkets: Industrial Metrology Market Size, Share, Industry Report, 2025 to 2030

- Market Research Future: 3D Metrology Market Report Size, Share and Industry Trend 2035

- Allied Market Research: Coordinate Measuring Machine Market Size, Share — 2026 (2024)

- Future Market Insights: Laser Trackers Market Size, Share & Forecast 2025 to 2035

- GGII (High-Tech Industry Research Institute): China Lithium Battery X-ray/CT Detection Equipment Market Forecast (2025)

Corporate Announcements and Annual Reports

- SCANTECH (688583.SH): 2025 Annual Report Summary (Shanghai Securities News, 2026-04-28)

- Tianzun Technology (688003.SH): 2025 Performance Express and Q1 Report (Securities Star, 2025)

- Hexagon AB: Year-End Report 1 January – 31 December 2025 (Hexagon website, 2026-01-29)

- AMETEK/Creaform: FARO acquisition completion and FARO CREAFORM business merger announcement (2025-07)

Industry Media and Professional Information

- Instrument Information Network: Tianzun Technology continuous innovation, accelerating domestic CMM substitution progress (2024-07)

- Sina Finance: Domestic brands exceed one-third — 2025 Q3 CMM procurement 103 units (2025-12)

- 36Kr, Finance.com: SCANTECH IPO coverage (2025-01)

- Securities Times (STCN): SCANTECH market share #1 domestic, #2 global (2025-01)

- Aerospace Testing International: Hexagon to buy Waygate Technologies (2025)

- Engineering.com: FARO expands 3D scanning portfolio with Creaform (2025)

Policy Documents

- State Administration for Market Regulation: National Metrology Development Plan (2021–2035)

- Ministry of Industry and Information Technology: Action Plan for Development of Intelligent Inspection Equipment Industry (2023–2025)

- Ministry of Finance: Major Scientific Instruments and Equipment Special Support Policy (2024)

Platform Factory Database Data

- Internal keyword scan data (2026-06-20): Distribution statistics of industrial measurement instrument-related keywords in the 4.8 million active factory database, covering coordinate measuring machines (53 factories), vision measuring machines (154 factories), laser trackers (5 factories), industrial CT (18 factories), in-process measurement (171 factories), industrial inspection (3,315 factories), metrology instruments (2,667 factories), and other category factory distributions. Data sourced from the 天下工厂 platform internal database scan (2026-06-20, internal).