China Precision Bearings & Ball Screws 2026 — The Precision Lifeline of Machine Tools, Robots, and EV Drivetrains

Industrial Research Institute | 2026-06-18

Chapter 1 Industry Overview: The Iron Triangle of Precision Bearings, Ball Screws, and Linear Guides

I. Three Components, One Precision System

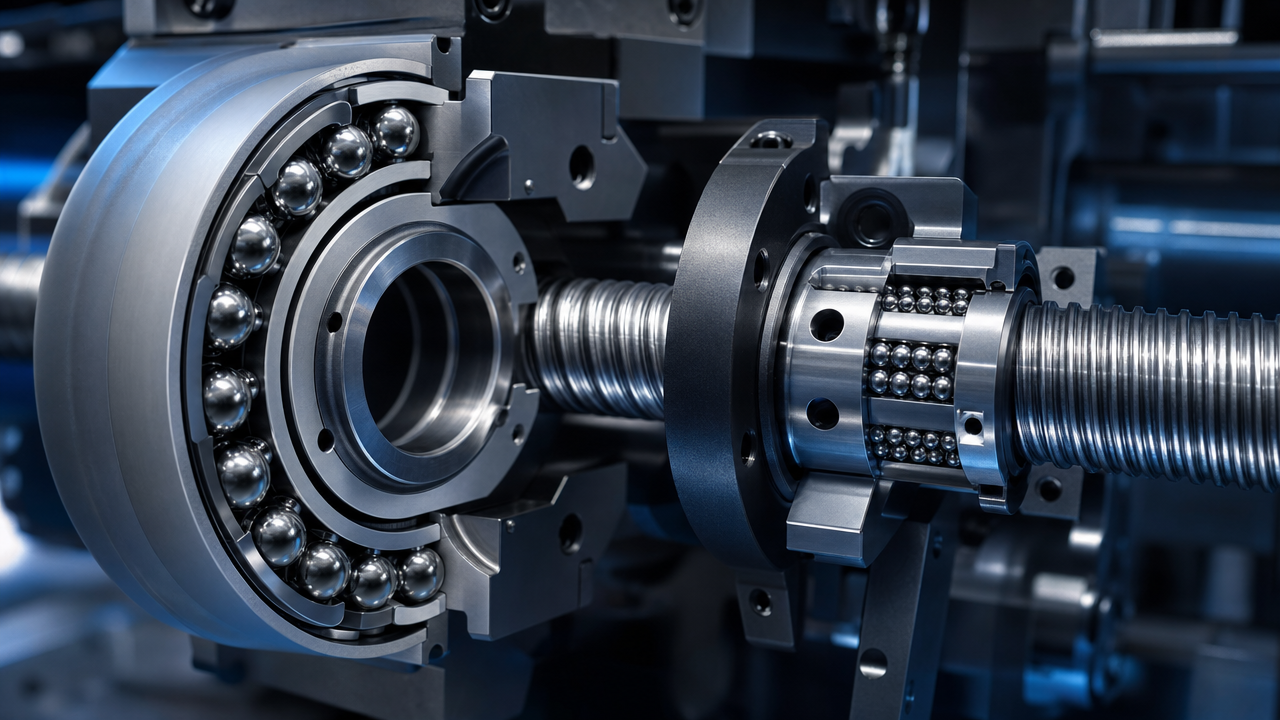

Among all core components of mechanical transmission, precision bearings made from precision bearing steel, ball screws, and linear guides form the "precision iron triangle" of modern manufacturing. Each plays a distinct role yet they are mutually interdependent: precision bearings support rotary motion, ball screws convert rotation into high-precision linear motion, and linear guides provide precise directional constraint for that linear motion. Together, the three components form the core of a CNC machine tool spindle system, the lifeline of an industrial robot joint, and the foundation of a precision platform in semiconductor lithography equipment.

Without precision bearings, a spindle cannot rotate smoothly at tens of thousands of revolutions per minute; without high-accuracy ball screws, a worktable cannot repeatedly position itself at the micrometer or even sub-micrometer level; without rigid linear guides, any lateral force will cause linear motion to deviate from its path. The technical level of these three types of components directly determines the precision ceiling of a country's machine tool industry, robotics sector, and semiconductor equipment industry.

From a product standpoint, the manufacturing logic of all three component types is highly consistent: precision grinding is a common key process step; bearing steel and high-strength alloy steel form a shared material foundation; stringent heat treatment is a common means of ensuring dimensional stability; and a clean manufacturing environment is a shared prerequisite for controlling contour error. It is precisely for this reason that the world's top suppliers — whether Japan's NSK and THK, Germany's Schaeffler, or Sweden's SKF — almost universally supply all three product types, forming an integrated linear motion solution of "bearings + screws + guides." This integrated supply capability is not only a comprehensive demonstration of technical ability but also a major negotiating advantage in procurement discussions with machine tool manufacturers and automation equipment makers.

Why does a single supplier need to make bearings, screws, and guides at the same time? Because all three product types share nearly identical foundational process DNA: high-purity specialty steel, sub-micron precision grinding, stringent heat treatment for dimensional stabilization, ultra-clean assembly environments, and nanometer-level precision measurement capabilities. Once a company establishes this capability base in one product category, the marginal cost of extending to the other two is far lower than building from scratch. This also explains why European and Japanese giants such as SKF, NSK, and Schaeffler can maintain leadership across all three product lines globally, while no Chinese company has yet reached a comparable scale in full-category precision transmission.

II. The Sub-Segment Landscape of Precision Bearings

In the broad context of the overall bearing market, precision bearings represent a sub-segment of relatively limited scale but with significantly higher technical barriers and profit margins. The global precision bearing market exceeded USD 20 billion in 2025, with ultra-precision grades (P4/P2 and above) accounting for approximately 35%, or roughly USD 7 billion. By comparison, the global total bearing market is approximately USD 120 billion; though the ultra-precision segment accounts for less than 6% of the total, its profit contribution exceeds 20%.

Within China, measured by downstream application, precision bearings can be roughly divided into six major sub-market battlefields:

Machine tool spindle bearings: This is the oldest and most classic application scenario for precision bearings. High-speed precision spindles require angular contact ball bearings or precision cylindrical roller bearings, with precision grade requirements of P4 or even P2, inner and outer ring roundness errors controlled to within a few micrometers, and rotational accuracy (radial runout RRIR) below 1 to 2 micrometers. Representative suppliers include NSK (ROBUST series), Schaeffler/FAG (BSBO/BSBL series), and Shanghai Tianjie. In 2025, China's machine tool spindle bearing market was approximately RMB 5 to 6 billion, with foreign brands accounting for approximately 70% to 80%.

Robot bearings and harmonic reducer bearings: The flexspline-rigid gear-wave generator structure of harmonic reducers requires ultra-thin cross-section bearings, especially crossed roller bearings and thin-wall deep groove ball bearings. These bearings have extremely thin cross sections (wall thickness of only 5 to 8 mm, outer diameter to cross-section height ratio typically exceeding 10:1), making precision grinding extremely difficult. This is one of the sub-categories with the fastest improvement in domestic substitution rate. Domestic companies such as ZYS (Suzhou, Chinese Academy of Sciences system) and Cixing Group (Zhejiang Cixi) have achieved some breakthroughs in the robot harmonic reducer matched bearing market, with domestic substitution rates rising from less than 10% in 2018 to around 30% in 2025.

Wind turbine main shaft bearings and pitch bearings: This is the precision bearing category with the most significant domestic substitution results in recent years. Companies such as LYC (Luoyang Bearing), ZWZ (Wafangdian Bearing), Xinqianglian (Luoyang Xinqianglian Slewing Bearing), Tianma Co., and Hengrun Co. have deeply entered this market. By 2025, the domestic substitution rate for main shaft bearings of major domestic wind turbine brands has exceeded 60%, and the rate for yaw and pitch bearings (slewing bearings) approaches 80% — the highest domestication rate among all precision bearing sub-categories.

High-speed rail bearings: This is one of the bearing categories with the lowest domestic substitution rate to date and also the most difficult technical fortress to break. The lifespan requirements for EMU axle box bearings (350 km/h grade) exceed 2.4 million kilometers (equivalent to 60 laps around the Earth), operating under severe vibration, impact, and extreme temperature differentials, with any premature failure being unacceptable as it means a safety accident. Currently, LYC (Luoyang Bearing) and ZWZ (Wafangdian Bearing) have completed bench verification of high-speed rail bearings and are advancing on-vehicle real-world verification, but it will still take several more years to reach mass supply.

EV/new energy vehicle bearings: With the rapid proliferation of NEV electric drive systems (motor + reducer + power electronics), EV-specific bearings have grown into the fastest-growing sub-category of China's bearing market. Core challenges include anti-electrical corrosion (electrochemical corrosion caused by shaft current) and high-speed operation (drive motor speeds exceeding 20,000 rpm under 800V high-voltage systems). Domestic companies such as C&U, ZWZ, and Cixing are conducting dedicated R&D to address the special demands of EV bearings.

Semiconductor equipment bearings: The ultra-precision category with the highest accuracy requirements, currently with a domestic substitution rate of less than 1% and almost entirely dependent on imports — the final frontier in the precision bearing domain.

III. The Strategic Position of China's Ball Screw Industry

The strategic position of ball screws within the precision transmission components system has risen sharply with the industrialization of humanoid robots. Before 2025, ball screws were primarily viewed as "basic functional components for machine tools," with market size of approximately RMB 3 to 5.5 billion and moderate growth. After 2025, the expected demand for planetary roller screws (PRS) from humanoid robots has pushed this track to the forefront of strategic competition.

Why do humanoid robots need large quantities of ball screws and planetary roller screws? The joint drive of humanoid robots requires converting the rotational motion of motors into linear motion of limbs. Compared with hydraulic and pneumatic actuation, the combination of ball screws and motors offers advantages of high precision, small size, light weight, and simple control, making it the mainstream solution for humanoid robot linear actuation. A single humanoid robot requires 15 to 20 sets of ball screws or planetary roller screws, with a per-unit value of approximately RMB 15,000 to 30,000 — one of the highest-value precision transmission components by single-machine value.

The key difference between a planetary roller screw (PRS) and a standard ball screw is: PRS replaces steel balls with multiple threaded rollers, dramatically increasing load capacity and rigidity through increased contact area while allowing a more compact form factor, making it the optimal solution for humanoid robot joint actuation. The current domestic substitution rate for PRS is approximately 20%, with per-unit value of approximately RMB 20,000 — the category with the lowest domestic substitution rate and highest value density among all precision transmission components, and the most urgent domestic substitution target from 2026 to 2028.

The full lifecycle service value of ball screws: Compared with the one-time purchase nature of bearings, the full lifecycle commercial value of ball screws is more complex, encompassing the following layers: initial purchase cost (precision ground screws: RMB 3,000 to 30,000 per set); periodic lubrication maintenance (grease replenishment every 1,000 to 3,000 operating hours); staged adjustment of preload level (reducing preload grade as wear progresses to extend usable life); and replacement cost at end of life. For CNC machine tool users, the wear curve of the screw directly affects machining precision — once backlash exceeds the allowable value (typically 3 to 8 micrometers), the machine's circular interpolation accuracy declines and "quadrant glitches" appear on workpiece surfaces, requiring screw replacement. This means the aftersales service and MRO (maintenance, repair, and overhaul) market for screws is an important source of stable revenue for screw manufacturers, with full lifecycle revenue approximately 1.5 to 2 times the initial purchase price.

Capacity expansion capability assessment for domestic screw companies: Under the anticipated demand explosion from humanoid robots, domestic screw companies are all accelerating capacity expansion, but the expansion speed is constrained by three critical bottlenecks:

First, procurement of precision thread grinding machines: global high-end precision thread grinding machines (such as KAPP-Niles and STUDER) typically have lead times of 12 to 24 months, and some models have begun to attract export control attention. The physical upper limit of capacity expansion depends on the number of grinding machines that can be procured.

Second, training skilled operators: an operator who can independently operate a precision thread grinding machine and meet C3 grade or above precision requirements needs at least 18 to 24 months of hands-on training — a human capital bottleneck on the speed of capacity expansion.

Third, synchronized expansion of quality systems: capacity expansion must be accompanied by a synchronized expansion of quality inspection capability (coordinate measuring machines, laser interferometers, ball bar testers, etc.); otherwise, production volume increases while quality control fails, creating the risk of mass returns — a fatal blow to the cash flow of screw companies.

Taking all three bottlenecks together, our research institute judges that the actual upper limit of annual capacity expansion for leading domestic screw companies (NJPE, Hanjiang Tool, and Yintai Technology) is approximately 20% to 30%, insufficient to support demand explosions of 100 times or more from the humanoid robot market — this means that if humanoid robots truly achieve mass production in 2027 to 2028, screws will become one of the tightest bottlenecks in the supply chain, and the bargaining power of leading suppliers will increase significantly.

IV. Precision Linear Guides: The Real Logic Behind Hiwin's Dominance in the Mid-Range Market

Compared with precision bearings and screws, the linear guide market landscape has one distinctive feature: Taiwan's Hiwin has become the world's number-one linear guide market share holder (approximately 30%), surpassing inventor THK (approximately 22%). Understanding how this came to be has important implications for understanding the future path of mainland Chinese precision transmission component companies.

Hiwin's linear guide products (precision grades H/SP/UP, corresponding to standard/precision/super-precision) have already basically matched THK's LM guides in technical specifications, at approximately 60% to 70% of the price of equivalent THK products. This price-performance ratio has enabled large-scale substitution of THK in machine tools, automation equipment, and other standardized applications. Currently, the procurement strategy of domestic precision machine tool manufacturers is universally "use Hiwin for standard grades, use THK for extremely precise applications," which has allowed Hiwin to establish extremely strong market share in the mainland China market.

Mainland domestic linear guide companies (Yintai Technology, Precision Drive, Taisheng Precision, etc.) hold some low-end market share in C5/C7 grades (ordinary industrial grade), but in SP/UP precision markets, the gap with Hiwin remains significant. Hiwin has production bases in Suzhou and Kunshan on the mainland, with supply capability and response speed essentially equivalent to a "local supplier," further squeezing the living space for mainland brands.

V. The Industrial Cluster Structure of China's Precision Bearings

China's precision bearing manufacturing is highly concentrated in a few industrial clusters. This concentration is not only historically formed but also a productive reality — in the precision bearing industry, the supporting industrial ecosystem (steel, heat treatment, grinding machines, calibration, technical worker training) can only be obtained at the lowest cost within a cluster:

Henan Luoyang: The city with the most concentrated precision bearing R&D and manufacturing capability in China, centered on LYC (Luoyang Bearing Group), radiating dozens of supporting SMEs covering ring forging, precision grinding, cages, precision grinding oil stones, and other supporting processes. It also hosts the country's only national key laboratory in the bearing industry.

Liaoning Wafangdian: Centered on ZWZ (Wafangdian Bearing Group), this is an important industrial base for large engineering machinery bearings, railway bearings, and large tapered roller bearings, and one of the most densely populated regions of China's traditional bearing industry.

Zhejiang Cixi/Ningbo: Cixing Group and surrounding supporting companies, focused on small precision bearings (miniature bearings, thin-wall bearings) and new energy vehicle bearings, forming an "East Zhejiang Bearing Cluster" that has rapidly expanded into the robot bearing market in recent years.

Jiangsu Suzhou/Changzhou: ZYS Suzhou Institute (Chinese Academy of Sciences system), Leader Drive, and multiple robot-matched bearing companies have gathered here, forming an emerging industrial cluster centered on robot precision bearings. The density of bearing-related companies in Suzhou Industrial Park is unrivaled nationally.

Shandong Linqing: A traditional ordinary bearing industrial cluster with huge annual output, mainly consisting of medium and low-end products. It is China's "quantity contributor" to bearings, but with a relatively lower level of precision manufacturing; its role in the precision bearing domestic substitution process is primarily to provide ring blanks and other support elements.

The formation mechanism of precision bearing industrial clusters: The formation of precision bearing industrial clusters is not random geographic distribution but follows several core industrial-economics logics:

Infrastructure-driven: The bearing clusters in Luoyang and Wafangdian fundamentally rely on the strategic layout of the bearing manufacturing industry among the "156 Soviet aid projects" in the early years of the People's Republic — these two cities possess a complete bearing manufacturing infrastructure accumulated over seventy years (specialized colleges, research institutions, equipment repair shops, raw material dealers, heat treatment contractors, precision instrument calibration agencies). New entrants to the bearing business in these two cities can obtain these supporting services at extremely low external transaction costs, significantly lowering the barriers and operating costs of starting up.

The positive feedback loop of talent density: Once a bearing industrial cluster forms in a region, large numbers of experienced bearing manufacturing engineers and technicians gather there, further reducing the cost for new companies to recruit talent and also accelerating the intra-regional dissemination of technical knowledge and process know-how (through talent mobility). This mechanism is particularly evident in Xinchang: the technology DNA of Xinchang's precision miniature bearing industry mainly derives from one source (a pioneer company founded by a core group of engineers from a Wanxiang Group bearing division); over subsequent decades, the resignations to start new businesses and the cross-flowing talent mobility of these engineers formed the technology family tree of Xinchang's hundreds of miniature bearing companies today.

Regional brand effect: "Luoyang bearing" and "Wafangdian bearing" as place-of-origin brands have created a first-mover impression among procurement personnel — bearings from "Luoyang" carry an inherent credibility bonus in the eyes of buyers, even though individual company brands vary in quality. This regional brand effect reduces the market development cost for companies within the cluster and is an important externality of cluster economies.

Conversely, industrial clustering also has negative effects: intense competition leads to frequent talent and technology outflow, low-end price wars erode overall profit margins, and there is a "bad money drives out good" risk (low-quality suppliers pull down the product reputation of the region as a whole). How to enjoy the cluster dividends while avoiding intra-cluster involution is a common management challenge facing the upgrade of bearing industrial clusters in Luoyang, Xinchang, and similar regions.

VI. The Technology Generation Gap in Precision Bearings and Screws: Why It Is Difficult to Catch Up Quickly

Understanding the true nature of the gap between China's precision bearings and ball screws and international leaders is a prerequisite for formulating the correct industrial strategy. This gap is not simply a matter of "insufficient funding" or "missing technology," but rather a generational gap of "accumulated time," manifesting in the following dimensions:

Metallurgical database of materials: Japanese bearing steel producers such as Sanyo Special Steel and Daido Steel have undergone more than 80 years of bearing steel smelting process optimization, accumulating massive databases of "bearing steel composition — heat treatment parameters — bearing performance" correlations. This database cannot be built through pure laboratory research alone; it must be accumulated through large numbers of batches in real industrial production — the composition of each batch of bearing steel varies slightly, and the corresponding bearing performance has subtle differences; only after accumulating thousands or even tens of thousands of batches of data can smelting engineers precisely control key process parameters to achieve predictability of bearing lifespan. China's steel companies are 20 to 30 years behind Japan in the depth and breadth of this database.

Tacit knowledge of process: A large part of the process knowledge in precision grinding and superfinishing is "tacit knowledge" — the combined control of grinding force, feed rate, coolant flow, and wheel dressing timing depends on the intuition and experience of process engineers, and cannot be fully reduced to written technical manuals. The tacit knowledge accumulated by veteran process engineers at NSK's Japanese factories is a core advantage that domestic companies cannot replicate from literature or patents in the short term. This is especially prominent in the superfinishing process: the most subtle quality gap between domestic and imported ultra-precision bearings often originates precisely in this step.

Equipment precision generational gap: Japan's Yasda YMC430 ultra-precision coordinate grinding machine has spindle radial runout of only 0.05 micrometers and positioning accuracy of ±0.5 micrometers — the apex of commercially available precision grinding machine specifications today. Domestic precision grinding machines have approximately 0.5 to 1 micrometer radial runout on equivalent metrics, a difference of about 10 times. This means that even if process engineers fully catch up to Japanese standards in skill, as long as domestic grinding machines are used, the ceiling on product precision is limited by the equipment to a lower level.

Time accumulation of brand and customer trust: Customers in precision bearings (especially ultra-precision spindle bearings and aviation bearings) prioritize "how many years this company's bearings have been running and how much usage verification data has accumulated" when selecting a supplier. NSK has been supplying bearings for a certain type of engine for more than 20 years, with cumulative data sufficient to prove long-term reliability under extreme operating conditions. Domestic suppliers newly entering these tracks, even if their product design is fully compliant, must still go through years or even decades of time accumulation before they can establish equivalent customer trust. This is an accumulation of brand assets that cannot be quickly compensated for through marketing spending or pricing strategies.

VI (cont.). Mass Production Consistency: The True Engineering Threshold for Precision Bearings

Producing one set of P4-grade sample bearings in a laboratory environment, versus producing tens of thousands of P4-grade bearings of equal precision with stable batch-to-batch consistency on a production line, are two engineering challenges of completely different magnitudes. Mass production consistency of precision bearings is the fundamental dividing line between "able to make a sample" and "able to deliver a product."

Statistical control of batch consistency: The precision machine tool spindle bearing production lines of Japan's NSK and Germany's Schaeffler have established statistical process control (SPC) systems centered on the process capability index (Cpk). Key quality characteristics (ring roundness, groove curvature, axial clearance) must have Cpk values ≥ 1.67, meaning the process variation range does not exceed 60% of the tolerance range, leaving sufficient safety margin. Domestic precision bearing companies typically only require Cpk ≥ 1.33. This difference appears small, but its meaning in mass production is: NSK producing 1 million P4-grade bearings would have a theoretical defect rate of approximately 0.6 ppm (0.6 per million); under domestic standards the defect rate is approximately 63 ppm — a difference of about 100 times. This is the deep statistical reason why, even when a domestic factory's equipment and process levels are close to NSK's standards, a perceptible gap in batch consistency and outgoing yield remains.

Ongoing compliance in cleanroom management: Cleanroom (class 100 to class 1,000) management for precision bearing assembly is not a "build it once and you're done" matter, but a systems engineering effort requiring continuous maintenance and personnel training investment. The core challenge of a cleanroom is not the physical facility but the ongoing enforcement of personnel behavioral standards: every opening of a door, every person entering or exiting, every material transfer must strictly follow cleanroom procedures; otherwise, microscopic particles can enter the assembly area and contaminate the bearing. Domestic precision bearing factories have basically met cleanroom physical facility standards, but there is still room to improve in the consistent execution of personnel behavioral standards — this is a cultural and management problem that is harder to solve quickly than a purely technical problem.

Precision of environmental temperature control: Assembly of ultra-precision bearings (P4/P2 grade) must be conducted in a constant-temperature environment (within ±0.5°C), because the thermal expansion of steel (linear expansion coefficient of GCr15 approximately 12×10⁻⁶/°C) causes bearing ring dimensions to change with temperature — a 1°C temperature change causes a 100 mm bore ring to change by approximately 1.2 micrometers, which is non-negligible compared with P4-grade tolerances (approximately 2 to 4 micrometers). The ability to maintain a stable constant-temperature assembly environment year-round 365 days (especially at peak summer cooling loads and winter heating demands) is an important indicator of the true authenticity of a precision bearing factory's production conditions.

Multi-batch performance consistency: For high-reliability applications (wind turbine main shaft bearings, high-speed rail axle boxes), batch-to-batch performance consistency is more important than single-set performance. Procurement parties typically require suppliers to provide outgoing inspection data for more than 30 consecutive batches (rotational accuracy, vibration values, axial clearance) to evaluate inter-batch performance stability. Domestic precision bearing companies, because of their relatively short production histories, still have insufficient data accumulation in this dimension of "completeness of historical data," affecting the purchase confidence of high-reliability customers.

From a statistical perspective, the essence of the mass production consistency problem is "the steady-state control capability of the manufacturing system" — the ability to maintain all process parameters within a narrow target range over the long term, excluding disturbances from equipment wear, personnel variability, and material batch differences. Building this capability requires at least 5 to 10 years of continuous improvement accumulation and cannot be rapidly leapfrogged through one-time technology transfer or capital injection.

VII. Bearing Typology: The Product Spectrum from Deep Groove Ball to Crossed Roller

When discussing domestic substitution and technical specifications of precision bearings, different bearing types face completely different technical challenges and degrees of difficulty in domestic substitution. Understanding the characteristics of major types helps to more precisely understand the competitive landscape of each sub-category.

Deep groove ball bearings (DGBB): The most common bearing type, capable of bearing both radial and axial loads simultaneously, the most common configuration in industrial motors, automobiles, and household appliances. The domestic substitution rate for precision deep groove ball bearings (P4-P5 grade) is relatively the highest; domestic companies such as C&U and Cixing have been supplying new energy vehicles and industrial robot markets in volume. The main difficulty in precision deep groove ball bearings lies in steel ball precision (roundness, diameter consistency) and the arc accuracy of ring grooves, where domestic products have made substantive breakthroughs.

Angular contact ball bearings (ACBB): Designed specifically for high-speed applications that must bear both radial and axial loads simultaneously, with 15° or 25° contact angles respectively adapted to different force balance requirements — the core bearing type for precision spindles. The manufacturing difficulty of precision angular contact ball bearings (P4-P2 grade, for high-speed spindles) lies in contact angle precision (contact angle deviation affects axial rigidity), light preload design (excessive preload generates overheating at high speed, while too little preload means insufficient rigidity), and consistency of matched-set installation (usually installed in pairs or sets of four, with axial clearance of each bearing highly consistent). This is one of the most difficult categories for domestic precision bearings to crack.

Cylindrical roller bearings (CRB): Load capacity is 3 to 5 times higher than ball bearings of the same specification, suitable for machine tool spindles bearing pure radial loads, and also the main bearing type for wind turbine gearboxes. The manufacturing key for precision cylindrical roller bearings is roller cylindricity (arc error in rollers leads to contact stress concentration) and ring flange precision. Domestic precision cylindrical roller bearings already have good mass production capability at P5 grade; P4 grade in major equipment applications still mainly relies on foreign brands.

Crossed roller bearings (XRB): Rollers are alternately arranged at 90° in a V-shaped groove, capable of simultaneously bearing axial, radial, and overturning moment loads in a single bearing — the core bearing type for precision turntables, robot joints, and coordinate measuring machines. Precision requirements for crossed roller bearings are extremely high — V-shaped raceway angle accuracy, roller dimensional consistency (diameter and length deviations both controlled to micrometer level) are critical. Domestic ZYS has significant accumulated expertise in crossed roller bearings, with some specifications achieving domestic substitution, but top precision specifications still mainly rely on THK and IKO imports.

Thin-wall bearings (Thin Section Bearings): Extremely thin cross sections (outer diameter to cross-section height ratio typically exceeding 6:1, even more than 10:1), the core configuration for harmonic reducers and precision turntables. The manufacturing difficulty of thin-wall bearings lies in the fact that rings are extremely prone to deformation during grinding and installation (roundness of thin rings cannot be guaranteed under clamping force), requiring dedicated non-clamping floating positioning grinding processes — one of the most technically challenging categories in domestic precision bearing development.

Four-point contact ball bearings: Contact between balls and grooves forms four contact points, capable of bearing bidirectional axial forces in a single bearing with compact structure; commonly used in wind turbine yaw bearings (replacing a combination of two angular contact ball bearings) and robot joint turntables. The key to precision manufacturing is the uniform spacing precision of the four-point contact grooves. Xinqianglian's pitch/yaw bearing products have extensive applications of this type and it is one of the bearing types with higher domestic substitution rates.

Chapter 2 Global Landscape and China's Position: Giant Territory and the Catch-Up Situation

I. Five Camps in the Global Precision Bearing Market

The global precision bearing and linear motion market is dominated by top-tier companies from Sweden, Germany, and Japan. As of 2025, the global bearing market size is approximately USD 120 billion, with the precision bearing sub-segment approximately USD 20 billion; the global linear motion product market (including linear guides, ball screws, and linear modules) is approximately USD 13.3 billion, expected to reach USD 22.4 billion by 2032, with a compound annual growth rate of approximately 7.7%.

First camp: Sweden's SKF

SKF is the century-old hegemon of the global bearing industry, founded in 1907, with brands including SKF and SNFA (ultra-precision bearings). SKF holds approximately 25% revenue share in the global precision bearing market — the highest share among single enterprises. Its ultra-precision bearings (SNFA brand) and spindle bearing product line are technologically leading, with deep presence in aerospace engines and semiconductor equipment. SKF's global revenue in 2025 was approximately SEK 98 billion (approximately RMB 63 billion), with industrial precision bearing business accounting for approximately 35% of total revenue.

SKF has five production bases on the Chinese mainland — in Shanghai (headquarters), Beijing, Dalian, Jinan, and Pinghu — with the mainland market contributing approximately 10% of its global revenue. In 2024, SKF completed the divestiture of its automotive wheel hub bearing business, focusing on industrial precision bearings and high-performance applications, further concentrating its product portfolio toward high precision and high added value. In the Chinese market, SKF's strategic focus is shifting from automotive bearings to precision industrial bearings, medical equipment bearings, and semiconductor equipment bearings.

Second camp: Germany's Schaeffler (FAG/INA brands)

Schaeffler Group was founded in 1946; its FAG brand (Friedrich Fischer invented the ball bearing in 1883; Fichtel & Sachs later became FAG) represents the highest standard of German precision machine tool bearing manufacturing. Schaeffler is Europe's largest bearing and linear motion product group. Its FAG BSBO and BSBL series ultra-precision spindle bearings are the industry standard configuration for five-axis machining center electric spindles, with installed quantities in the global high-end machining center market exceeding any other brand.

Schaeffler's Greater China revenue in 2025 was approximately RMB 22 to 24 billion (based on company annual reports and broker estimates), making it its second-largest single market globally. It has a dedicated ultra-precision bearing production line in Taicang, China, primarily supplying the Chinese market while also exporting to other Asia-Pacific markets. In 2024, Schaeffler completed the merger with Vitesco Technologies, gaining important system integration capability in new energy vehicle electric drive, further strengthening its strategic position in China's new energy vehicle supply chain.

Third camp: Japan's NSK

NSK (Nippon Seiko K.K.) was founded in 1916 and is Japan's largest bearing company, globally leading in precision machine tool spindle bearings. Its ROBUST-HC series ultra-precision spindle bearings can reach 120,000 rpm working speed (for precision grinding electric spindles), representing the world's highest-speed spindle bearing technology. NSK's fiscal year 2025 revenue (to March 2026) was approximately JPY 900 billion (approximately RMB 44 billion), with Greater China accounting for approximately 25%.

NSK is the primary supplier of axle box bearings (350 km/h grade) for China's EMU trains in high-speed rail — also one of the hardest links to break through in domestic substitution. In any single category, NSK's high-speed rail bearings are the hardest to replace because behind them lies a century-level accumulation of bearing lifespan verification data. NSK is also investing heavily in R&D resources in EV bearings; its world's highest-speed (2025 certification) ball bearings developed specifically for EV drive motors have industry-leading anti-electrical corrosion performance under 800V system high-speed operating conditions.

Fourth camp: Japan's JTEKT (Koyo brand)

JTEKT is Toyota's bearing company; the Koyo brand is globally top three in automotive bearings. Its precision spindle bearing products have also entered the machine tool market, but its precision bearing share in the Chinese market is relatively smaller than NSK/Schaeffler. JTEKT has deep ties with Japanese OEMs in automotive wheel hub bearings and steering system bearings; its share in China's precision industrial bearing market is approximately 5%.

Fifth camp: Three linear motion leaders (THK / NSK Precision / Hiwin)

In the ball screw and linear guide sector, Japan's THK is the global founder and the most authoritative technical standard setter — THK developed the world's first commercial linear motion guide in 1971, thereby founding the modern linear motion product industry. THK's fiscal year 2025 revenue was approximately JPY 470 billion (approximately RMB 23.5 billion); its LM guides (linear motion guides) are the de facto industry standard, and all followers (including NSK, Hiwin, PMI, etc.) produce products with dimensions and interfaces compatible with THK.

Hiwin as a Taiwan company has become the global linear guide market share leader through precise market positioning. Hiwin's global linear guide market share is approximately 30%; driven by the humanoid robot wave, the robotics business has become a new growth engine. In 2025, the robotics business accounted for approximately 7% of Hiwin Group revenue; it is expected to surpass 10% in 2026.

Ten-year evolution trends in the global precision bearing industry landscape: Looking back at the evolution of the global precision bearing industry landscape from 2015 to 2025, the following several trends are most notable:

First, mainland Chinese market share has expanded rapidly but with polarized quality distribution. In 2015, mainland Chinese companies held approximately 8% share of the global precision bearing market; by 2025, this has risen to approximately 15%, with significant quantitative growth. However, within this 15% share, approximately 85% is concentrated in P0 to P6 low-precision products, while the share of ultra-precision products at P4 grade and above is still less than 2%, reflecting a significant time lag between "quantitative catch-up" and "qualitative catch-up."

Second, European and Japanese giants have significantly increased their proportion of localized production in the Asia-Pacific region. SKF, NSK, and Schaeffler have all substantially increased their proportion of localized production in China and Southeast Asia; in 2025, NSK manufactures approximately 70% of its China sales in China (only approximately 30% in 2010), both hedging against exchange rate risk and accelerating delivery responsiveness. This trend continuously strengthens the cost competitiveness of foreign brands in the Chinese market, squeezing the price competition space of domestic brands.

Third, semiconductor equipment and medical robots have spawned new ultra-high-precision tracks. Before 2015, the highest-end applications for precision bearings were concentrated in machine tool spindles (P4/P2 grade) and aircraft engines (M50 steel). After 2020, new applications emerged — such as air-bearing bearings and guides for semiconductor lithography machine precision workpiece stages, thin-wall bearings for surgical robot joints, and ultra-low-friction miniature bearings for quantum computer cooling systems — pushing the technical ceiling of precision bearings higher once more. In these "ultra-high-end" applications, even NSK and SKF are in the R&D exploration stage, with domestic enterprise participation virtually at zero, but this also means there is no solidified competitive landscape in this field, and technological breakthroughs have greater strategic imagination space.

II. Mainland Chinese Companies: The Difficult Transition from Quantity to Quality

China is the world's largest bearing producer, with annual output exceeding 29.6 billion units, accounting for approximately 35% of global production. But in terms of output value, the average price of these bearings is extremely low — 29.6 billion units of bearings have an output value of approximately RMB 300 billion, equivalent to approximately USD 40 billion, while the global bearing market has output value of approximately USD 120 billion; China's quantity is approximately 35% of the global total, but its share of output value is less than 10%. This enormous gap between quantity and price clearly reveals the structural contradiction of China's bearing industry: world-first in production volume, while value creation capacity is far from matching.

In terms of company scale, the largest comprehensive bearing company on the Chinese mainland is the about-to-be-listed LYC (Luoyang Bearing Group Co., Ltd.), with 2025 operating revenue of RMB 6.034 billion and net profit of RMB 529 million, both all-time highs. ZWZ (Wafangdian Bearing Group) has annual output exceeding 8 billion units with revenues of approximately RMB 6 billion, with unique accumulation in large bearings. C&U Group (Shanghai, private), Tianma Co., Wuzhou Xinchun, and other companies together form the first tier of the domestic bearing industry, but the proportion of precision bearing products at these companies is relatively limited.

In the ball screw and linear guide sector, representative domestic companies include Nanjing Process Equipment (NJPE), Hanjiang Tool (under Hanjiang Machine Tool Group), Yintai Technology, and Jike Co., but the scale of these companies is relatively small (annual revenue mostly within RMB 500 million), mostly with C5 to C7 medium-to-low-end products as the main offering, and their combined market share in C3 grade and above precision does not exceed 10%.

III. The Historic Decline in Foreign Brand Market Share and Its Correct Interpretation

In 2018, foreign brands held approximately 79% of China's precision bearing (P5 grade and above) market. By 2025, this proportion has fallen to below 30%. This is a historic transformation, but it needs to be correctly understood to avoid overestimating the actual progress of domestic substitution.

This market share transfer has mainly occurred at the P5 grade (relatively ordinary precision level), i.e., in mid-to-high-end machine tools, automotive transmission, wind power, and other fields, where domestic bearings have achieved the leap from "not good enough" to "basically good enough" through large-scale capacity investment, continuous process improvement, and the push of "first-batch insurance" policies. At P4 grade and above (ultra-precision grade), especially in machine tool spindle bearings, semiconductor equipment bearings, and precision instrument bearings, the dominant position of foreign brands has basically not been shaken — NSK/FAG/SKF market shares in these categories are still above 80%.

The rational strategy is: actively advance domestic substitution in categories where domestic products have been proven reliable (wind turbine pitch bearings, mid-to-low-speed industrial robot joint bearings); maintain foreign procurement in categories not yet fully verified (high-speed spindle bearings, semiconductor equipment bearings) while launching verification projects to accumulate data.

Regional differences in the decline of foreign market share: The overall decline in the market share of foreign precision bearings shows significant differences across regions. In the North China heavy industry zone (Beijing, Tianjin, Hebei) and Northeast old industrial base (Shenyang, Dalian), domestic bearing substitution has progressed faster, because heavy machine tool and mining machinery OEMs in these regions have long-term matching relationships with local state-owned bearing enterprises (LYC, Harbin Bearing). In the Yangtze River Delta precision manufacturing cluster (Suzhou, Shanghai, Ningbo), high-precision machine tool and medical device OEMs that primarily export tend to retain foreign bearings to meet their downstream customers' quality certification requirements. In the Pearl River Delta electronics manufacturing cluster, Korean and Japanese precision bearings hold an absolute dominant position in the maintenance market for SMT placement machines and similar equipment. This regional difference suggests: national figures for precision bearing domestic substitution rates mask regional structural differences, and domestic substitution progress in different regions must be evaluated independently by industry and application scenario.

IV. Three Competitive Tiers in Global Precision Bearings

Top tier (P4/P2 ultra-precision, semiconductor, aviation, precision instruments): SKF, Schaeffler/FAG, and NSK form an absolute monopoly among European and Japanese giants, with combined market share exceeding 85%. The core competitive variable is precision grade certification capability and customer trust accumulation, not price. Domestic enterprises are basically absent from this tier and cannot form a substantive challenge in the short term (before 2030).

Middle tier (P4 to P5, high-end machine tools, industrial robots, high-speed rail): SKF/Schaeffler/NSK dominate, but Hiwin (linear motion products) and LYC (Luoyang Bearing) have made some breakthroughs. This tier is the most active battlefield for domestic substitution; foreign brand market share is contracting from approximately 75% in 2018 toward approximately 50% to 60% in 2025, but the contraction pace is slower than external expectations.

Bottom tier (P5 to P6, general industry, non-critical automotive parts, ordinary machinery): Domestic companies have basically completed substitution at this tier. LYC, ZWZ, C&U, Cixing, and others hold most of the market share; foreign brands retain share only in price-premium-sensitive situations.

The dividing lines between the three tiers are not fixed but continuously shift upward as domestic technological capabilities improve. Over the past 5 years, the dividing line has already moved upward from the P0/P5 boundary to the P5/P4 boundary — below P5 is already basically a domestic-dominated battlefield, P5 to P4 is the current most intense competition zone, and above P4 foreign brands still hold firm.

Historical evolution and future prediction of competitive tier dividing lines: Through historical data analysis, our research institute has plotted the evolution curve of precision bearing competitive tier dividing lines:

In 2010, the dividing line was near the P0/P6 boundary — below P6 grade (equivalent to the current ordinary industrial grade) there were domestic competitors; above P6 was almost entirely foreign territory.

In 2015, the dividing line moved up to near P5/P4 — domestic product share at P5 grade (mid-level industrial precision) broke 30%, marking the phased leap of domestic bearings from "basic industrial use" to "precision industrial use."

In 2020, the dividing line further differentiated within the P5 range — wind turbine pitch/yaw types (precision requirement P5/P6) saw domestic substitution rate exceeding 70%, while machine tool spindle types (also P5 grade but more demanding operating conditions) still had domestic substitution rates below 20%, reflecting sub-segment differences within the same precision grade but with different operating condition difficulty.

In 2025, the dividing line showed localized breakthroughs at the P4/P2 boundary — a few companies such as LYC passed verification by high-end machine tool manufacturers for specific models of P4-grade angular contact ball bearings, with domestic substitution rates rising from near zero to approximately 15%, but domestic substitution for P2-grade ultra-precision bearings remains near zero.

Our institute predicts that by 2030, the main dividing line of competitive tiers will advance to the P4/P2 boundary — i.e., the domestic substitution rate for P4-grade precision bearings (machine tool spindles) will break 40%, becoming the main competitive zone between domestic and foreign products, while P2-grade (ultra-precision, semiconductor and aviation) domestic substitution will rise from near zero currently to 5% to 10%. This pace of evolution (dividing line moving up one precision grade every 10 years) implies that the complete domestic substitution of precision bearings is a systemic project spanning at least 20 to 30 years, not a task that can be rapidly accelerated by short-term policy pushes.

V. Hiwin: A Successful Model for Asian Challengers

In the global precision transmission field, Hiwin is a rare case of an "Asian challenger successfully surpassing a Japanese leader." Founded in 1989, after 30 years of focused development, Hiwin achieved the feat of surpassing THK in global linear guide market share — extremely rare in the Japanese-dominated precision machinery field.

Hiwin's success strategy can be summarized in three points: first, providing products at 90% to 95% of performance with approximately 60% to 70% of the price of Japanese equivalents, precisely targeting the mass market of "good enough + reasonable price"; second, establishing large-scale production bases in Taiwan and Suzhou to control costs and guarantee delivery times through scale advantages; third, in product line expansion always following market demand rather than ahead-of-time positioning, gradually expanding from machine tool guides to high-end applications such as industrial robots, semiconductors, and medical equipment, with each expansion pulled by existing customer needs.

In 2025, Hiwin gained a new development opportunity in the humanoid robot wave. The company has entered the supply chains of Tesla's Optimus and multiple leading domestic humanoid robot companies, providing precision linear guides and some screw products, with the robotics business's proportion of group revenue rapidly increasing. Hiwin's coordinated operating model between its Taiwan headquarters and Suzhou factories gives it advantages in price, lead time, and customization capability over Japanese counterparts, which is an important advantage for entering high-growth tracks.

For mainland Chinese bearing and screw companies, Hiwin is a unique entity that is simultaneously both a competitor and a reference point — its development path shows that Asian companies, through specialized focus, scale, and cost optimization, can indeed compete with European and Japanese giants in precision machinery, but this requires decades of uninterrupted accumulation, not a leap that can be completed with one or two rounds of capital investment.

VI. Strategic Divergence Among Mainland Chinese Precision Transmission Companies

In 2025 to 2026, the strategic paths of mainland Chinese precision bearing and transmission component companies are diverging, with different types of companies choosing completely different development directions. This divergence will profoundly influence the industry landscape over the next 5 to 10 years.

Path A: Vertical specialization type (represented by LYC and Xinqianglian)

These companies choose to deeply accumulate in a single sub-category (wind turbine main shaft bearings, large slewing bearings), building hard-to-replicate moats through technical focus and scale effects. LYC's wind turbine main shaft bearings and Xinqianglian's pitch and yaw bearings are typical results of this path. The advantage of vertical specialization is fast accumulation and deep moats; the risk is that cyclical fluctuations in a single category have significant impacts on revenue (annual demand for wind turbine main shaft bearings is highly correlated with installed capacity in that year, with revenue differences between high and low installation years reaching 40% to 60%).

Path B: Robot new-track entry type (represented by Cixing Group and ZYS)

These companies use their existing precision bearing manufacturing capabilities as a technical foundation and proactively enter new application scenarios such as robot bearings. The attractiveness of this path lies in: robot bearings have high unit value (3 to 5 times that of same-specification industrial bearings), low domestic substitution rate (currently 25% to 35%), and strong growth potential. The risk lies in the uncertainty of the robotics industrialization timeline, and the development of new-track products (thin-wall bearings, crossed roller bearings) requires process accumulation somewhat different from traditional bearings.

Path C: Supporting service ecosystem extension type (represented by some SMEs)

Some smaller-scale precision bearing companies are choosing to evolve from pure manufacturers to composite service providers of "manufacturing + technical service + MRO parts," establishing specialized service ecosystems in specific industries (such as precision machine tool and semiconductor equipment maintenance). The commercial logic of this path is: high-end precision bearing manufacturing requires large amounts of capital and time accumulation, while providing professional services based on manufacturing knowledge is a path to reach high-value customer groups with lower capital investment.

Path D: Materials and process upgrade type (represented by upstream companies such as Xingcheng Special Steel)

At the very top of the precision transmission components industrial chain, materials companies are choosing to upgrade from providing qualified bearing steel to providing engineering materials solutions oriented toward specific applications: not just selling steel, but providing material heat treatment advice, bearing steel fatigue data support, and joint debugging services for materials and heat treatment processes, upgrading materials companies from raw material suppliers to precision manufacturing partners. This path requires materials companies to establish deeper data-sharing relationships with downstream bearing manufacturers and is an important direction for improving the value density of the entire industrial chain.

These four paths are not mutually exclusive, and successful companies often focus on their main path while moderately trying extensions into adjacent paths. But the core logic is consistent: under conditions of limited capital and technology accumulation, focused concentration is the optimal strategy; only after reaching a certain stage of accumulation is it the right time for moderate diversification and industrial chain extension.

Chapter 3 Core Technical System: Where Does Precision Come From?

I. Precision Grades: A Complete Mapping from ISO to Application

The precision system for precision bearings is jointly defined by the International Organization for Standardization (ISO) and national standard systems. In China, GB/T 307 series is implemented, dividing bearings into five precision grades P0/P6/P5/P4/P2, with smaller numbers representing higher precision: P0 is standard grade (general industrial bearings), P6 is high grade, P5 is precision grade, P4 is ultra-precision grade, and P2 is extreme precision grade (top ultra-precision, mainly used for ultra-precision machine tool spindles and aircraft engines).

Corresponding to international standards, ISO 492 divides bearings into Class Normal/6/5/4/2, Japan's JIS standard into JIS0/6/5/4/2, and US ABEC grades correspond to P0 through P2 as ABEC 1/3/5/7/9 respectively. The nominal equivalence relationship is: P5≈ISO Class 5≈ABEC 5, P4≈ISO Class 4≈ABEC 7, P2≈ISO Class 2≈ABEC 9.

It is worth particularly noting that the "nominal equivalence" of precision grades does not mean that same-grade products under different standards have completely identical technical performance. Due to differences in detailed tolerances, measurement methods, and evaluation conditions across standard systems, a product certified to P4 grade under one standard may only satisfy P5 grade requirements under the strict inspection of another standard. This is one of the technical challenges domestic precision bearings face when exporting to European and Japanese markets.

The correspondence between precision grades and application scenarios: P0/P6 grade is used for ordinary machine tool feed axes, wind turbine gearboxes, and general motors; P5 grade for ordinary CNC machine tool spindles, mid-to-low-speed industrial robot joints, and high-end household appliances; P4 grade for high-precision CNC machine tool spindles (precision milling/grinding), high-speed industrial robot joint axes, and medical CT scanner spindles; P2 grade for ultra-precision coordinate boring machine spindles, ultra-precision grinding machine spindles, optical instrument precision shafting, and some semiconductor front-end equipment precision motion axes.

The economics of precision grades: why tightening tolerances corresponds to exponential price jumps: The precision grade of precision bearings with each step up does not increase manufacturing difficulty and price linearly but shows exponential jumps, due to the following points:

First, non-linear increase in reject rate. The dimensional tolerance (ring roundness, groove curvature) for P4 grade bearing rings is approximately 50% stricter than P5 grade, but due to the tail effect of the normal distribution, the reject rate typically increases 3 to 5 times rather than 50%, directly pushing up the unit cost of P4 grade bearings.

Second, surging inspection costs. P4 grade and above precision bearings require high-precision measuring instruments (roundness instruments, coordinate measuring machines, laser interferometers); inspection time per bearing set is approximately 15 to 40 minutes, several times higher than P5/P6 grade (2 to 5 minutes); the proportion of inspection costs in manufacturing costs increases from approximately 5% at P6 grade to approximately 20% to 30% at P4 grade.

Third, environmental control costs. P4 grade and above assembly must be conducted in constant-temperature (±0.5°C) cleanrooms (10,000 to 1,000 class); cleanroom construction and operating costs translate to approximately RMB 20 to 100 fixed cost amortization per bearing set, significantly pushing up unit costs in small-batch production.

Fourth, grinding wheel and consumable costs. CBN superabrasive grinding wheels (diameter 200 to 400 mm) used for P4 grade precision bearing grinding have unit prices of approximately RMB 8,000 to 30,000 per wheel, with service life of approximately 50 to 200 bearing sets, translating to approximately RMB 50 to 200 per set in grinding wheel costs; compared with ordinary corundum grinding wheels used for P6 grade (RMB 500 to 2,000 per wheel, service life 2,000 to 5,000 sets), P4 grade grinding wheel costs are approximately 5 to 20 times higher.

The combination of the above four factors means that the manufacturing cost of P4 grade precision bearings is approximately 3 to 6 times that of same-specification P6 grade, while the market selling price is approximately 5 to 15 times, reflecting the dual effect of the premium space and technical barriers brought by precision grades.

II. In-Depth Analysis of the Ball Screw Precision System

The precision standard for ball screws differs slightly from bearings. Japan's JIS B1192 (China's corresponding GB/T 17587) divides ball screw precision into ten grades from C0 to C10, with smaller numbers representing higher precision. The core precision indicator is Lead Error — the deviation between the actual stroke and theoretical stroke of the screw:

| Precision Grade | Representative Lead Error (per 300 mm stroke) | Main Applications |

|---|---|---|

| C0 | ≤3.5 micrometers | Ultra-precision coordinate measuring machines, nanometer-level platforms |

| C1 | ≤5 micrometers | Precision machining centers, precision inspection equipment |

| C2 | ≤7 micrometers | High-end machining centers, precision grinding machines |

| C3 | ≤12 micrometers | Standard high-end CNC machine tools (largest volume demand) |

| C5 | ≤23 micrometers | Ordinary CNC machine tools, general automation equipment |

| C7 | ≤52 micrometers | Handling, simple positioning situations |

| C10 | ≤210 micrometers | Power transmission, low accuracy requirements |

C3 grade (12 micrometers/300 mm) is the mainstream demand specification for current precision machine tools and also the most fiercely contested dividing line for domestic substitution: below C5 grade domestic substitution has basically been achieved; C3 grade is the "main battlefield currently under siege"; and C2 to C0 grade almost entirely depends on imports (mainly THK and NSK Precision).

The precision standard for planetary roller screws (PRS) has not yet formed a unified international standard; manufacturers use their own specifications, mainly extending definitions with reference to the framework of ISO 3408 (ball screw standard). The precision currently required by humanoid robot applications roughly corresponds to the C3 to C5 level of ball screws, with more focus on repeatability and backlash than on pure cumulative lead error.

III. Material System: The Metallurgical Support Behind Precision

The material selection for precision bearings and ball screws is the physical foundation that constrains the manufacturing ceiling:

GCr15 (high-carbon chromium bearing steel): The most mainstream bearing steel material, with carbon content approximately 0.95% to 1.05% and chromium content approximately 1.3% to 1.65%. After heat treatment, hardness HRC 60 to 65, with good contact fatigue life and wear resistance, meeting all application requirements of P0 to P5 grade bearings, and also the mainstream material choice in P4 grade ultra-precision bearings. Ultra-pure GCr15 (oxygen content <5 ppm, non-metallic inclusions <0.5 mm²/dm²) produced by Xingcheng Special Steel represents the highest standard of domestic bearing steel.

GCr15SiMn/GCr15SiMo (improved bearing steel): Silicon, manganese, molybdenum, and other alloying elements are added on the basis of GCr15 to improve the hardenability of the steel, suitable for ring sections of large bearings (bore diameter >300 mm), the commonly used material for large wind turbine bearings and mining machinery bearings.

M50/M52 (high-speed tool steel): Used in aircraft engine bearings, maintaining high hardness (HRC 58+) above 200°C — the standard material for civil aviation engine main shaft bearings. Global major suppliers are Japan's Daido Steel and Sanyo Special Steel; domestic supply capability is limited.

Silicon nitride ceramic balls (Si₃N₄): Density is only 40% of steel balls, elastic modulus approximately 1.5 times that of steel, thermal expansion coefficient 25% of steel; at high speeds the centrifugal force generated is far lower than steel balls (at the same speed, centrifugal force is proportional to mass, and silicon nitride balls have centrifugal force only 40% that of steel balls), giving hybrid ceramic bearings (steel rings + ceramic balls) excellent performance under ultra-high-speed conditions. NSK's all-ceramic bearings and SKF's hybrid ceramic bearings are widely used in precision grinding spindles and semiconductor equipment. Domestic silicon nitride ceramic balls at G5 grade (diameter deviation ≤0.13 micrometers) can be supplied in volume, but G3 grade (≤0.08 micrometers) still relies on imports.

IV. Precision Grinding Process: The Critical Leap from Blank to Precision

The core process in precision bearing manufacturing is grinding, whose importance can be understood from the following perspective: the roundness error of bearing ring blanks (after forging + turning) is approximately 50 to 100 micrometers; after precision grinding and superfinishing, the roundness error of P4 grade rings must reach 0.5 to 1 micrometer — the grinding process needs to reduce roundness error by approximately 100 times.

Grinding processes are divided into: rough grinding (removing most of the allowance), semi-finish grinding (approaching target dimensions, leaving 0.1 to 0.3 mm allowance), finish grinding (reaching design dimensions, leaving minimal allowance), and superfinishing (reducing surface roughness from Ra 0.06 micrometers to Ra 0.006 to 0.01 micrometers). Each process step requires dedicated equipment: precision internal and external cylindrical grinding machines (supplied by Japan, Germany, Switzerland), groove grinding machines (Japan's Koyo Machinery, etc.), superfinishing machines (Germany's Supfina, etc.).

Key parameter control in grinding processes: grinding wheel grit selection (rough grinding P60, finish grinding P400 to P600, superfinishing P1500 and above), grinding speed (finish grinding spindle speed 15,000 to 25,000 rpm), feed rate (feed per revolution 0.001 to 0.005 micrometers), coolant (must have precision filtration to prevent grinding particles from causing surface scratches), workpiece temperature control (constant temperature ±0.5°C to prevent thermal deformation from causing precision drift). The comprehensive control of this series of parameters is where the core "tacit knowledge" of precision bearing manufacturing resides.

V. Precision Classification and Core Technology of Linear Guides

Linear guide precision classification (based on the THK system, widely adopted in the industry): Standard grade (Normal, H grade), Precision grade (P grade/SP grade), and Super Precision grade (SP/UP grade). THK's H grade guide straightness is approximately 12 micrometers/500 mm, SP grade approximately 3 micrometers/500 mm, and UP grade approximately 1.5 micrometers/500 mm — the precision ceiling of currently commercially available linear guides.

Key technologies for linear guides include: precision grinding of the hardened steel main body (guide rail straightness), raceway shape (circular arc raceway vs. double arc raceway, affecting contact rigidity and low-friction characteristics), preload grade (C0 no preload / C1 light preload / C2 medium preload — higher preload means higher rigidity but also greater friction), and circulation circuit design (affecting noise and high-speed smoothness). Hiwin's linear guides adopt a cross-section design fully compatible with THK's, and at C4 to C5 precision grades (corresponding to SP grade) have achieved the same level of specifications as THK at approximately 60% to 70% of THK's cost — currently the mainstream procurement choice for domestic machine tool manufacturers.

The supply landscape of the linear guide market (2025, Chinese market): THK approximately 15% (high-end precision, ultra-precision occasions), Hiwin approximately 30% (precision to ultra-precision), PMI approximately 10% (Taiwan, precision grade), mainland companies (Yintai Technology, Precision Drive, etc.) combined approximately 20% (standard grade to precision grade downstream), and the remaining approximately 25% scattered across other imported brands.

VI. Inspection and Certification System

Precision bearings must pass multiple strict inspection checkpoints before leaving the factory:

Dimensional accuracy inspection: Air gauges (resolution 0.01 micrometers) for inner and outer diameter inspection; roundness instruments (roundness measurement resolution 0.01 micrometer level) for inner and outer ring roundness inspection; contact profilometers for groove curvature inspection.

Rotational accuracy testing: Dedicated bearing rotational accuracy test stands measure inner ring/outer ring radial runout (RRIR/ORER) and axial runout (RAXR/OAER) under specified preload and speed conditions — the most critical test item for precision grade certification.

Vibration and noise testing (BVID): Bearing Vibration Instrument Detectors evaluate bearing vibration acceleration in three frequency bands (low, medium, high). For P4 grade and above bearings, vibration acceleration in the high-frequency band must be below extremely strict thresholds, directly related to bearing surface cleanliness and material uniformity.

Life bench testing: For high-reliability applications such as high-speed rail, wind power, and aviation, bearings must pass accelerated life tests under specified speed and load (usually equivalent to hundreds to thousands of hours of actual operating conditions) before shipment, verifying that bearing fatigue life reaches design targets.

China's bearing industry still lacks internationally recognized independent third-party inspection and certification agencies; most companies rely on self-built inspection rooms for outgoing inspection. Compared with Japan's mature JIS certification system (Japanese Bearing Industry Association) and Germany's third-party certification system (FAG/DIN standard certification system), this affects the trust-building of domestic precision bearings with international high-end customers.

The actual commercial value of international inspection certification: For precision bearing manufacturers, obtaining internationally recognized third-party inspection certification is not only an internal tool for quality management but also a commercial key to opening the door to high-end customers. Taking aerospace bearing certification as an example, obtaining AS9100D (Aerospace Management System Certification) requires approximately 18 to 24 months of system construction and third-party auditing, costing approximately RMB 500,000 to 2 million, but once certified, the company can enter the Qualified Supplier Database of the global aviation industrial chain (such as Boeing and Airbus supplier portals), showcasing qualifications to thousands of aviation manufacturers globally, with potential market value in the hundreds of millions.

The certification gap in Chinese precision bearing companies: The precision bearing industry in China has a clear "missing middle layer" in certification: the number of companies with basic ISO 9001 certification is large (thousands nationally), but companies with specific industry advanced certifications (AS9100D, IATF 16949, IRIS, etc.) are relatively scarce (hundreds), and precision bearing inspection agencies with international third-party laboratory mutual recognition capability (CNAS accreditation + ILAC mutual recognition) are even fewer (approximately 10 to 15 nationwide). This missing middle layer makes it difficult for many medium-sized domestic companies with actual precision manufacturing capabilities to enter the Qualified Supplier lists of multinational corporations due to lack of internationally recognized certification endorsement, creating a market predicament of "capable but lacking credibility." Building a more complete middle-layer certification system (especially specialized certification for robot and new energy vehicle bearings) is important infrastructure work for improving the overall international competitiveness of China's precision bearing industry.

VII. The Design Science of Precision Transmission Components: Hertzian Contact Theory and Engineering Boundaries

The performance limits of precision bearings and ball screws are fundamentally constrained by contact mechanics. A deep understanding of this underlying physical constraint is key to understanding why certain precision requirements cannot yet be met at current technology levels.

Application of Hertzian contact theory: The Hertzian contact theory established by British physicist Heinrich Hertz in 1882 describes the distribution of contact area and contact stress when two elastic bodies are in contact under force. In precision bearings, the contact between steel balls (or rollers) and ring raceways is a classic Hertzian contact problem: bearing steel balls (Young's modulus approximately 200 GPa) and rings (also approximately 200 GPa) produce extremely small elastic deformation under load, with the contact surface being an elliptical area (for ball bearings, area approximately 0.01 to 0.1 mm²), and peak contact stress approximately 1,500 to 3,000 MPa. This contact stress determines the theoretical upper limit of bearing steel fatigue life — when contact stress exceeds the fatigue limit of the steel (approximately 1,800 to 2,200 MPa), fatigue crack propagation begins on the raceway surface, ultimately leading to spalling failure.

This mechanism explains why the setting of bearing preload must be so precise: if preload is too large, contact stress increases and fatigue life shortens; if preload is too small, balls slip against the raceway (skidding) at high speeds, accelerating wear and causing precision to deteriorate rapidly. The preload window (the allowable ratio between maximum and minimum preload) for P4/P2 grade bearings is typically within ±5% to ±10%, placing extremely high demands on assembly processes (precision of preload application).

EHD lubrication theory and ball screw efficiency: The lubrication mode of precision bearings is elastohydrodynamic lubrication (EHD) — under high contact stress, lubricating oil in the contact zone is compressed into an extremely thin oil film (thickness 0.1 to 0.5 micrometers); oil viscosity increases significantly due to high pressure (piezo-viscous effect), forming an oil film of sufficient thickness to separate the contact surfaces and avoid direct metal-to-metal contact. EHD film thickness is highly sensitive to the base oil viscosity of the grease, bearing speed, and contact zone temperature: at ultra-high speeds (>20,000 rpm), contact zone temperature rise causes the base oil viscosity of the grease to drop sharply (viscosity-temperature effect), the EHD film thins and enters mixed lubrication or even boundary lubrication, friction coefficient increases sharply, bearing heat generation accelerates, forming a vicious cycle. This is the fundamental physical mechanism behind why high-speed precision spindle bearings have significantly shorter than designed service lives under extreme speeds, and also the theoretical basis for why grease formulation selection is so critical for P4 grade and above high-speed bearings.

Ball screw elastic deformation and positioning accuracy: In high-accuracy ball screw systems, the same Hertzian contact deformation exists between balls and screw spiral raceways. When axial load is applied, elastic displacement produced by contact deformation (at nanometer level) is superimposed on actual motion displacement, affecting actual positioning accuracy. High-precision machine tools in design need to quantify this elastic displacement through axial stiffness (unit N/μm) specifications; high-rigidity screw systems typically have axial stiffness in the range of 100 to 500 N/μm, meaning that under 100 N of axial force, the system elastic displacement is approximately 0.2 to 1 micrometer — still a non-negligible source of error for ultra-precision machine tools pursuing sub-micrometer positioning accuracy. Increasing preload can improve axial stiffness, but the trade-off is increased heat generation and shortened life — the eternal "preload triangle trade-off" (precision, life, rigidity) in precision screw design.

Mastering these contact mechanics theories and applying them in product design is the core knowledge leap for precision transmission component companies to evolve from "making by following examples" to "independent design optimization." Currently, the gap between domestic precision transmission component companies and European and Japanese giants in applied design capability for contact mechanics is an important constituent part of the "technology generation gap," no less important than the gap in grinding processes and materials.

VIII. Evolution of Bearing Life Prediction Theory and Engineering Challenges

Bearing life prediction is the core problem in precision bearing engineering applications and the ultimate test distinguishing bearing products of different technical levels.

L10 life basic theory: The bearing rated life (L10 life) defined by international standard ISO 281 refers to the theoretical number of hours that 90% of bearings can operate under given load and speed without fatigue spalling. Key parameters in the L10 life calculation formula are the ratio of rated dynamic load capacity (C) to actual load (P) (C/P), and the exponent determined by bearing type: 3 for ball bearings, 10/3 for roller bearings. From the formula, L10 life is proportional to a high power of (C/P), meaning that the impact of load on life is extremely sensitive: a 20% increase in load shortens ball bearing life by approximately 50%.

Engineering significance of the modified life factor (a₂₃ factor): The basic L10 life formula was established on data from the 1960s without considering the effects of material cleanliness, lubrication conditions, installation accuracy, and other factors. Modern ISO 281 introduces the modified life factor a₂₃ (or AISIM correction factor), incorporating material factor (am₁), lubrication conditions (aISO), and other factors into calculations, making life prediction closer to actual operating conditions. For high-end precision bearings using ultra-clean bearing steel (oxygen content ≤5 ppm) with optimized lubrication, the modified life factor a₂₃ can reach 15 to 50, meaning actual life is 15 to 50 times higher than basic L10 life. This is why top-tier precision bearings (NSK, FAG) can achieve far longer service lives than ordinary calculation predictions under specified operating conditions.

The statistical nature of fatigue life and engineering management: Bearing life is essentially a statistical quantity rather than a fixed value — even bearings from the same batch operating under exactly the same conditions will have actual failure times following a Weibull distribution; L10 is merely a certain quantile of this distribution (life corresponding to 10% failure probability). In practice, L50 (50% failure probability, median life) is typically approximately 5 times L10, while L1 (1% failure probability) is approximately 0.21 times L10. For high-reliability applications (aircraft engines, high-speed rail), engineers need to focus not on L10 but on Lna (extremely low failure probability, such as 0.1% or even 0.01%), which corresponds to the extreme small tail of the sample and requires far more test data than usual to accurately estimate — this is also the deep statistical reason why high-speed rail bearing certification cycles are so lengthy.

Complexity of operating condition effects: beyond simple load calculations: In actual operating conditions, bearing life is affected by the combined superimposition of load spectrum (complex variation history of load over time, not simple constant load), temperature history, lubrication state changes, installation precision, and shaft deflection. The load spectrum for wind turbine main shaft bearings is particularly complex: wind speed varies randomly, causing bearing loads to change simultaneously at two time scales — low-frequency (wind direction changes) and high-frequency (turbine speed). The traditional L10 life formula needs to be approximated using equivalent load methods, and this approximation may underestimate fatigue damage under extreme operating conditions (typhoons, turbulence). Mastering real-world operating load spectra and constructing accurate life prediction models is one of the core contents of deep technical cooperation between precision bearing manufacturers and OEMs, and also an important dimension of the gap between domestic bearing companies and foreign giants in high-end applications.