Executive Summary

China is the undisputed core of the global electric two-wheeler industry. In 2025, total new vehicle sales reached approximately 55–60 million units, accounting for more than 80% of global volume, with a fleet in service exceeding 400 million units — roughly one vehicle for every three to four citizens. The underlying logic of this industry is uniquely Chinese: it is not a "luxury good" trickling down from premium segments, but a "necessity" that has from its very inception served the most basic and indispensable short-distance mobility needs of ordinary Chinese households. This essential character provides the industry's robust volume foundation.

Four structural variables converged in 2025 to drive a new cycle of value re-rating in what might otherwise appear to be a mature market: the upgrade to new national standard GB 17761-2024, lithium battery penetration breaking through 40%, intelligent features diffusing from challenger brands to the leading incumbents across the board, and overseas expansion transitioning from "shipping goods" to "putting down roots."

From a competitive perspective, the industry is undergoing irreversible consolidation from fragmented to concentrated. Yadea Holdings (HK 1585) retained its position as the global sales leader with approximately 16.3 million units, with FY2025 net profit surging 128.8% year-on-year to approximately RMB 2.9 billion, and gross margin reaching a historic high of 19.1%. Emma Technology (A-share 603529) closed in with approximately 15.8 million units and net profit of approximately RMB 2.46 billion. Ninebot/Segway (A-share 689009) achieved a remarkable 64.5% growth rate, lifting electric two-wheeler sales to 4.09 million units, making it the industry's most dazzling growth standout. Tailg Technology's submission of a Hong Kong Stock Exchange listing application in January 2026 signals that the third tier of competitors is entering a phase of capital-driven consolidation. NIU Technologies (NASDAQ: NIU) saw 2025 sales dip modestly to approximately 1.2 million units, but maintains a distinctive position in international brand recognition and premium intelligent connectivity. The combined market share of the dual duopoly (Yadea + Emma) stands at approximately 55%, with CR5 at approximately 62%. Consolidation is clear and irreversible — by 2030, CR5 is projected to exceed 70%, with the total number of vehicle manufacturers contracting from approximately 100 in 2025 to fewer than 50.

From a technology and commercial standpoint, lithium electrification is the most certain structural trend. LFP (lithium iron phosphate) cell prices have fallen from approximately RMB 1.50/Wh at the 2021 peak to approximately RMB 0.40/Wh in 2025. Average selling prices have risen from approximately RMB 1,800 during the lead-acid era to approximately RMB 3,500–4,500 in the lithium-dominant era. Industry revenue growth (approximately 30%) far outpacing unit growth (approximately 12%) reflects the per-unit value expansion driven by lithium electrification and intelligent connectivity. By 2030, the ex-factory vehicle market is projected to expand from approximately RMB 190 billion in 2025 to approximately RMB 350 billion, with the full industry chain (including batteries, motors, charging and swapping infrastructure, and the aftermarket) exceeding RMB 1,200 billion.

On the overseas dimension, Southeast Asia (Vietnam, Indonesia, Thailand) is the international market offering the most certain volume increments for Chinese electric two-wheeler brands in 2025–2030. Yadea, Tailg, and Luyuan have all established local manufacturing in Vietnam, directly challenging the dominance of Japanese brands Honda and Yamaha in Southeast Asia's combustion motorcycle market. Europe's e-Bike component market (centered on Bafang) faces EU anti-subsidy investigation pressure, but the EU's 2035 combustion ban creates a historic opportunity window for Chinese manufacturing. In India, extremely high tariff barriers mean Chinese complete-vehicle brands are entering via the CKD components export model; direct complete-vehicle entry is unlikely in the near term.

This report represents the Research Institute's systematic deep-dive into China's electric two-wheeler industry in 2026, conducted on the basis of data from 4.8 million active factories on the platform, publicly disclosed financial data from multiple listed companies, and first-hand industry research. The research covers the complete supply chain from lithium mining to the end rider, integrating quantitative analysis and qualitative judgment to deliver authoritative research that is both globally panoramic and practically grounded for supply chain participants, investment institutions, and policy researchers.

Chapter 1 Definitions, Classifications, and the Full Industry Chain Panorama

I. Product Definitions and the Legal Classification System

Electric two-wheelers are electrically powered personal mobility vehicles with two wheels. Under China's current legal framework — the Road Traffic Safety Law and its accompanying technical standards — they are divided into three statutory categories, each with distinct administrative jurisdictions, technical parameter boundaries, and licensing requirements.

Electric bicycles (E-Bikes) constitute the largest-volume and broadest-user-base category. Under the new version of national standard GB 17761-2024, the core technical parameters are: maximum design speed not exceeding 25 km/h (with a tamper-proof device that cannot be bypassed by any means); complete vehicle mass (including battery) not exceeding 55 kg; motor rated power not exceeding 400 W; battery voltage not exceeding 60 V; and mandatory pedal-assist functionality with both human and electric propulsion. Electric bicycles are legally classified as "non-motor vehicles," requiring no driver's license, operating in non-motor vehicle lanes with the same road rights as bicycles. They are currently China's most numerous urban-rural commuting tool, contributing approximately 75% of total electric two-wheeler sales in 2025.

Light electric motorcycles occupy the space between electric bicycles and electric motorcycles, with a maximum design speed exceeding 25 km/h but not exceeding 50 km/h, or a motor rated power exceeding 400 W but not exceeding 4,000 W. They are classified as motor vehicles, requiring an F-class license, operating in motor vehicle lanes, requiring license plates and mandatory insurance. This category is an important choice for suburban commuters and professional delivery riders; its freedom from the 25 km/h hard cap makes it more versatile, and the majority of standard delivery platform rider vehicles belong to this category.

Electric motorcycles are the highest-specification, highest-priced category, with maximum design speed exceeding 50 km/h and motor rated power exceeding 4,000 W. As motor vehicles, they require D or E-class motorcycle licenses, motorcycle license plates, annual inspections, and enjoy the same road rights as combustion motorcycles. Electric motorcycles are the direct electrification replacement for combustion motorcycles, targeting consumers who demand riding performance and long-distance range, priced at RMB 8,000–40,000 per unit, and are the primary battleground for traditional motorcycle manufacturers such as CFMoto and Qianjiang Motor in their electrification transitions.

II. Scenario-Based Classification and User Profiles

From a usage-scenario perspective, the operational segmentation within the industry is more analytically valuable than the legal categories:

Commuter transportation: The most mainstream use case, covering 5–20 km daily commutes in urban and rural areas, contributing over 60% of sales volume. Users span a wide age range (18–65), with medium-high price sensitivity and primary requirements around range (60–100 km per charge), appearance (not embarrassing), and value-for-money (RMB 2,000–4,000 range). This scenario is the red ocean where Yadea, Emma, and Tailg fiercely compete, and the core driving scenario for lithium electrification.

Delivery and logistics: Professional food delivery riders (Meituan, Ele.me, JD Express, etc.) who ride 150–250 km daily, with requirements for battery capacity (over 120 km range), battery-swapping convenience, and vehicle durability far exceeding ordinary commuter users. Approximately 7 million professional riders constitute a B2B market of approximately RMB 15–20 billion per year.

Recreational and sporting: Mid-to-high-end electric mountain bikes and urban electric touring scooters targeting higher-income users seeking riding enjoyment, priced at RMB 8,000–30,000, with relatively small market volume (approximately 1–2 million units per year) but fast growth, serving as an important anchor for brands' premium strategies.

Shared mobility: Internet platform-operated shared electric bicycles (Hellobike, Meituan, DiDi Qingju) purchased in B2B bulk (RMB 2,000–3,000 per unit), characterized by high durability (3-year service life), full IoT connectivity, and 5–8 uses per vehicle per day. This is the most demanding segment for vehicle quality consistency and reliability.

Export and overseas sales: Complete vehicle exports and CKD kit exports to Southeast Asia, and e-Bike motor and mid-drive system exports to Europe. Though not serving Chinese consumers directly, this segment contributes considerable foreign exchange earnings and manufacturing capacity utilization to the industry chain.

III. Deep Technical Comparison: Lead-Acid vs. Lithium Batteries

The technological rivalry between lead-acid batteries and lithium-ion batteries is one of the most critical structural variables in the 2025 electric two-wheeler market.

Lead-acid battery technology: Lead-acid cells are based on reversible electrochemical reactions between lead (Pb) and lead dioxide (PbO₂) in a sulfuric acid (H₂SO₄) electrolyte, with a discharge voltage of approximately 2.0 V per cell. Electric two-wheelers typically use four 12 V modules in series (48 V system). Energy density is approximately 30–40 Wh/kg — versus lithium's 140–175 Wh/kg — meaning a lead-acid pack for equivalent range weighs approximately 12–14 kg, versus approximately 4–5 kg for an LFP pack, a critical difference for compliance with the new national standard's 55 kg vehicle mass limit.

Lead-acid cycle life is typically 300–500 charge cycles to 20% depth of discharge, requiring replacement approximately every 1–1.5 years. Lead-acid batteries do not tolerate over-discharge well, cannot support fast charging (requiring 6–8 hours for standard charging), and perform poorly in the city's frequent stop-start environment.

Lead-acid batteries' absolute advantages are: ① extremely low cost (48V/20Ah pack at approximately RMB 150–200 ex-factory, only 20–30% of equivalent LFP lithium); ② a mature nationwide repair ecosystem (county and township repair shops can replace without specialized tools); ③ safety (physical damage does not cause thermal runaway self-ignition, giving consumers a "no fire hazard" psychological safety advantage over lithium); ④ a mature recycling system (over 95% recycling rate for used lead-acid batteries).

LFP lithium battery technology: LFP cells use olivine-structured lithium iron phosphate (LiFePO₄) as the cathode, graphite as the anode, carbonate electrolyte, and polyolefin composite separator. Working voltage is approximately 3.2–3.3 V per cell. Energy density is approximately 140–175 Wh/kg (2025 mass production level), with a cycle life of 800–1,500 cycles at 80% DOD, and charging time of approximately 3–6 hours standard, with support for over 2C fast charging.

LFP's greatest advantage over NCM (ternary lithium) is safety: LFP's thermal decomposition temperature is 550°C (versus 210–280°C for NCM), with far lower thermal runaway tendency in abuse tests, making it ideal for the demanding environments of electric two-wheelers.

IV. The Nine-Link Full Industry Chain Panorama

The electric two-wheeler supply chain can be decomposed into nine major links forming a complete value chain from raw materials to consumers:

Link 1: Mining and basic raw materials. Lead-acid routes rely on lead (adequate domestic supply in Yunnan, Guangxi, Sichuan, with recycled lead accounting for approximately 60%); lithium battery routes depend on lithium concentrate (import-dependent on Australia and Chile, with domestic Four Chuan and Qinghai supplementing), phosphorus (abundant domestically), copper (for motor windings and circuit boards), and NdFeB (Inner Mongolia rare earths for high-performance permanent magnets in hub motors).

Link 2: Cell manufacturing. LFP cells are manufactured by coating, winding/stacking, injecting electrolyte, formation charging, and encapsulating into prismatic aluminum shell, cylindrical, or pouch formats.

Link 3: Battery module and PACK assembly. Cells are assembled into complete battery packs with BMS integration, encapsulated in aluminum or steel housings, with waterproof sealing. Two-wheeler dedicated lithium PACK must pass the six mandatory safety tests of GB 43854-2024. Shengxin Battery (Star Charge) is the world's largest specialized two-wheeler lithium PACK supplier, with over 50% domestic market share.

Link 4: Motor assembly. Hub motors (Rear Hub Motor) are the mainstream, covering 200W–8,000W+ power ranges. Brushless DC hub motors (BLDC) with FOC control have become standard for mid-to-high-end products. Bafang is the world's largest specialized e-Bike motor supplier, with approximately 30–40% market share in the European e-Bike mid-drive motor market.

Link 5: Electronic control assembly (controller + BMS). The motor controller is the vehicle's "brain," reading torque commands and motor Hall signals via MCU, calculating current commands in real time, and driving MOSFET power transistors to PWM-modulate motor stator windings. The BMS monitors cell voltage and temperature at millisecond resolution, executes multi-level protection logic, manages cell balancing, estimates SOC (within ±5% accuracy), and communicates with the charger and vehicle via CAN/UART.

Link 6: Body structural components. Includes frames (high-strength steel tube welding or aluminum alloy die-casting/extrusion welding), front fork shock absorber assemblies, wheel hubs (aluminum alloy die-cast rims plus bearings), brake systems, tires, seats, fenders, and body panels (ABS/PP injection molded).

Link 7: Functional accessories. Instrument clusters (from segment LCD to TFT color screens with integrated BeiDou positioning), full-LED lighting (headlights, DRLs, taillights, turn signals), chargers (lead-acid type RMB 15–30, smart lithium type RMB 50–200), helmets (new standard mandates delivery of a GB 811-compliant helmet with each vehicle purchase), anti-theft locks, BeiDou positioning modules, and IoT communication modules (4G Cat.1).

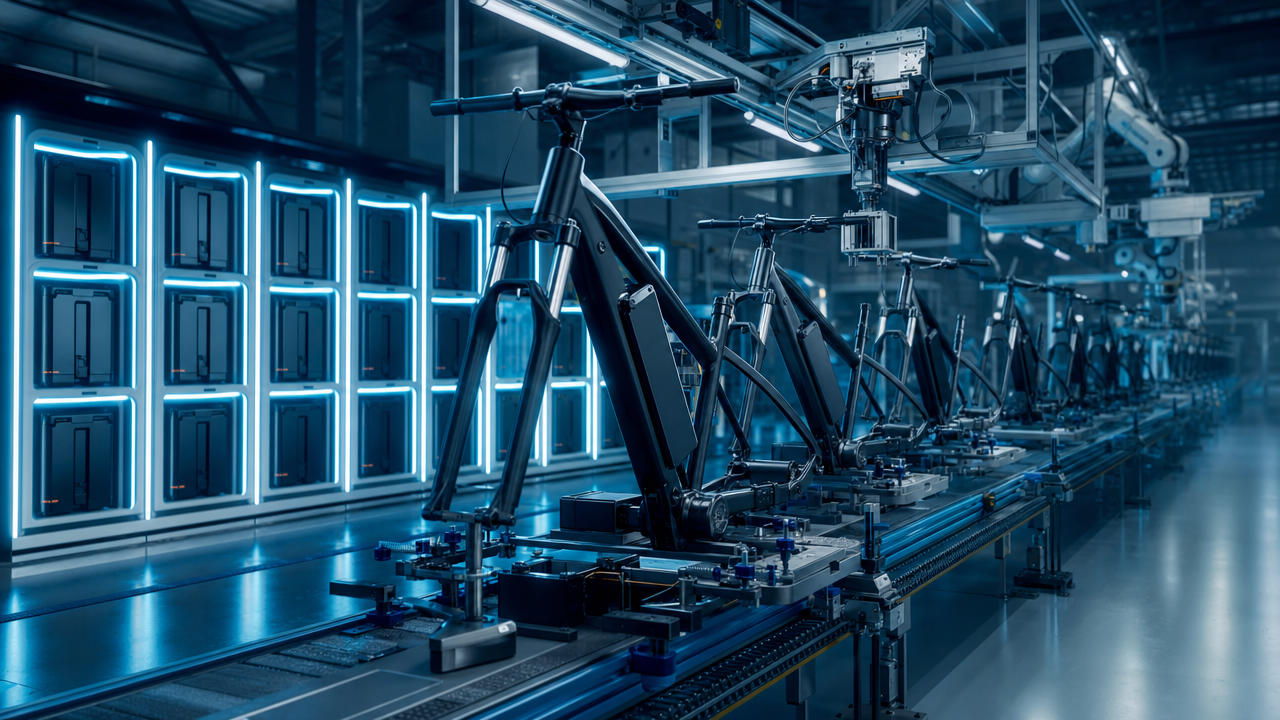

Link 8: Vehicle manufacturing and branding. OEM vehicle manufacturers integrate upstream components, perform frame welding/aluminum die-casting, electrophoretic painting, automated assembly line production (approximately 120–180 seconds per vehicle cycle time), ex-factory quality inspection, and manage brand building, channel management, and after-sales service systems.

Link 9: Distribution, charging/swapping operations, and aftermarket. The offline dealer network (approximately 300,000+ nationwide outlets) and online e-commerce platforms (approximately 15% penetration rate) form the distribution layer; charging pile operators and battery-swapping operators provide energy infrastructure; the aftermarket (parts replacement, used vehicle transactions, insurance, maintenance services) generates approximately RMB 40–50 billion per year based on the 400 million vehicle fleet.

V. Supply Chain Cost Structure Analysis

Using a 2025 ex-factory price of approximately RMB 3,500 for a mid-range lithium commuter electric bicycle as an example, the manufacturing cost breakdown is approximately:

| Cost Item | Cost (RMB) | % of Manufacturing Cost |

|---|---|---|

| Lithium battery pack (48V/20Ah LFP) | 480–530 | ~28–31% |

| Motor (350W rear hub) | 65–80 | ~4–5% |

| Controller (incl. BMS integration) | 90–120 | ~5–7% |

| Frame (steel tube welding + electrophoresis) | 180–240 | ~10–14% |

| Front fork shock assembly | 45–70 | ~3–4% |

| Hubs + tires (front and rear) | 60–90 | ~3–5% |

| Brake system (front disc + rear disc) | 40–65 | ~2–4% |

| Instrument cluster (color LCD/TFT) | 40–80 | ~2–5% |

| Lighting (full LED) | 20–35 | ~1–2% |

| Plastic body panels (ABS injection) | 80–120 | ~5–7% |

| Wiring harness and connectors | 25–40 | ~1–2% |

| Seat, luggage box, handlebar | 30–50 | ~2–3% |

| Charger (included with vehicle) | 50–100 | ~3–6% |

| BeiDou positioning module | 18–28 | ~1–2% |

| 4G IoT communication module | 18–28 | ~1–2% |

| Assembly labor and manufacturing overhead | 150–200 | ~9–12% |

| Total (manufacturing cost) | ~RMB 1,391–1,876 | 100% |

This cost structure reveals two key facts: ① the power battery (approximately 28–31%) is the single largest cost item, and every decline in cell prices directly improves vehicle gross margins; ② motor + controller combined represent approximately 9–12%, a relatively mature component category with limited cost reduction potential absent major technical changes, though integration into unified motor-controller modules can reduce assembly costs.

VI. Vertical Integration Trends in the Supply Chain

Leading vehicle manufacturers significantly deepened their vertical integration in 2024–2025, driven by dual imperatives of supply chain security and cost control.

Yadea's "VFLY Drive System" self-development: Yadea established the "VFLY Power Technology" subsidiary in 2024, focused on in-house development of the complete vehicle powertrain (motor + controller + BMS in one integrated module), aiming to reduce dependence on external suppliers and improve system efficiency through software-hardware co-optimization.

Emma's "AIMA Technology Research Institute": Emma established a approximately 500-person research institute in Tianjin covering battery technology research, vehicle dynamics simulation, and intelligent algorithms (OTA update systems, UBI telematics-based insurance data models). Emma's 2025 "AIMA Connect" intelligent platform integrates riding data, remote diagnostics, theft management, and OTA upgrades.

Dual supplier safety system: As Shengxin Battery's lithium PACK market share exceeded 50%, vehicle manufacturers' dependence risk on a single supplier became increasingly prominent, prompting Yadea and Emma to accelerate the introduction of secondary suppliers (CATL's two-wheeler division, Guoxuan High-Tech's two-wheeler PACK product line) as strategic backups.

Chapter 2 Global Electric Two-Wheeler Competitive Landscape

I. Global Market Size and Regional Distribution

In 2025, global electric two-wheeler annual sales (including electric bicycles, light electric motorcycles, and electric motorcycles) reached approximately 65–70 million units. Geographic distribution is highly concentrated: China accounts for over 80%, Southeast Asia approximately 5% (approximately 3.5 million units), South Asia (mainly India) approximately 2% (approximately 1.3 million units), Europe (including e-Bikes) approximately 8% (approximately 5–6 million units, mainly electric assist bicycles), with other regions (North America, Middle East, Africa, Latin America) combined at approximately 5%.

Key structural characteristics: China is the "dual core" of electric two-wheeler production and consumption; over 90% of global electric bicycle components (including motors, controllers, batteries, frames) are manufactured in China; Southeast Asia is the fastest-growing non-China market, projected to exceed 10 million units annually by 2030; Europe's e-Bike market is most mature in Western Europe, with the Netherlands (over 1 million units/year) and Germany (approximately 700,000 units/year) leading demand for high-quality, high-safety mid-drive systems, where Bafang is the primary beneficiary.

II. Japanese Legacy Giants: Honda and Yamaha's Electrification Dilemma

Honda (Tokyo 7267) exceeded 21 million units in FY2025 global motorcycle sales. Honda's electrification strategy reflects classic "supertanker transformation" characteristics: its vast combustion motorcycle R&D system, global dealer network, and manufacturing bases make the transition speed less nimble than Chinese challenger startups. Honda's two electrification directions: ① the Honda Mobile Power Pack e: swappable battery system (building battery-swap networks in Taiwan and India); ② plug-in electric product lines (Honda EM1 e: in Europe, approximately €3,500 RRP, approximately 3–4x premium over Chinese products of equivalent performance).

Yamaha (Tokyo 7272) was the most cautious among the Japanese Big Three on electrification pace in 2025, with limited production electric products and slow expansion plans. Yamaha was one of the earliest mid-drive motor suppliers in the e-Bike space (launching the world's first commercial e-Bike in 1993), retaining unique brand equity in the European and Japanese premium e-Bike markets, though market share has been significantly eroded by Bosch and Bafang.

III. European Electric Motorcycle Ecosystem in Depth

Europe is the world's most mature market for high-end electric motorcycle culture. Piaggio Group (PIA.MI) encompasses Vespa, Aprilia, Moto Guzzi, and Piaggio brands; the Vespa Elettrica is available in fully electric and hybrid versions across European markets. Zero Motorcycles (California, founded 2006) is North America's most influential pure electric motorcycle specialist brand, with 2025 products priced at approximately USD 16,000–22,000 and performance (46–67 kW power, 200–330 km range) comparable to mainstream combustion mid-to-large displacement motorcycles. Energica (Modena, Italy) represents European traditional motorcycle industrial culture's transition to electric; Energica Ego (100 kW, 0–100 km/h in approximately 2.6 seconds, over 400 km range) is technically the most extreme production pure-electric superbike, the designated vehicle for the MotoE World Championship. KTM's Freeride E-XC (18 kW, approximately 108 kg complete weight) is the brand's most commercially successful pure-electric off-road product.

IV. India: The World's Fastest-Growing New Battleground

India's 2025 electric two-wheeler (E2W) market saw approximately 1.28 million new registrations, growing approximately 28% year-on-year. TVS Motor led with approximately 300,000 iQube units sold (approximately 23% market share). Bajaj Auto's Chetak EV sold approximately 270,000 units (approximately 21% market share). Ola Electric experienced a dramatic collapse from approximately 410,000 units (approximately 35% market share) in 2024 to approximately 200,000 units (approximately 15%) in 2025 — a cautionary tale of insufficient after-sales service infrastructure failing a technically aggressive growth push.

V. Gogoro: Infrastructure as Business Model

Gogoro (Taiwan, NASDAQ: GGR) was the world's earliest company to build a complete business model around a city-scale battery-swapping network as its core competitive advantage, with the "Energy as a Service" logic: the vehicle (Smartscooter series) is the entry point to the swapping network; monthly battery rental subscription is the continuous profit source. Taiwan's GoStation network density has reached the world's highest: 2,700+ stations, 1.4 million+ smart batteries, 370,000+ daily swaps, 650,000+ active users; approximately 35% electric scooter market penetration in Taiwan.

VI. Southeast Asian Local Forces and the Rise of Vietnam

Vietnam's electric two-wheeler penetration is rising fastest in Southeast Asia. In 2025, approximately 350,000–450,000 electric motorcycles/scooters were newly registered, growing over 150% year-on-year. Indonesia, Southeast Asia's largest combustion motorcycle market (approximately 5 million annual sales), has only approximately 2% electric penetration, but enormous potential. Gojek's battery-swapping partnership with Gogoro and Honda's EM1 e: entry are two major potential market catalysts.

VII. European e-Bike Market Deep Analysis

Europe's Pedelec e-Bike market (maximum 25 km/h assist) is the world's most mature, highest-willingness-to-pay e-Bike segment, and the highest-value single international destination for Chinese motor and components exporters. In 2025, European e-Bike annual sales were approximately 5–5.6 million units, with a market size of approximately €20–25 billion. Germany is the largest single market (approximately 1.7 million units), followed by the Netherlands (approximately 1.1 million units).

Bosch's technological moat: Bosch eBike Systems' market dominance (approximately 42% share) rests on three core advantages: ① ergonomics (the cadence-assist linearity of its torque sensor is highly praised by European consumers); ② reliability (2-year or unlimited-mileage warranty, lowest failure rates in the industry); ③ software ecosystem (Bosch eBike Connect APP with ride tracking, navigation, battery status, and deep Garmin integration). Bosch OEM supply pricing at approximately €400–600 per mid-drive unit — approximately 1.5–2x Bafang's retail price — demonstrates the commercial logic of technical recognition translating to pricing power in mature markets.

Bafang's competitive strategy: Bafang's European strategy is "value as wedge, product upgrade as lever" — entry-level BBS series at approximately USD 150–200 build supplier relationships with smaller e-Bike brands; the high-end M600 series (peak 600W, 4.45 kg, torque-sensor control) directly targets Bosch Performance Line CX at approximately 60–70% of Bosch pricing.

2025 structural challenges: European e-Bike market growth was flat or slightly negative in 2025, impacted by softer consumer confidence and channel inventory digestion from the 2022–2023 over-ordering period. This dip is viewed as cyclical, not structural, given the long-term policy support for green mobility.

VIII. Middle East and Africa: The Next Frontier of Two-Wheeler Electrification

The combined annual motorcycle sales of the Middle East and Africa exceed 12 million units (predominantly combustion), with electric penetration near zero. The Middle East's extreme summer temperatures (45–50°C) impose stringent battery thermal management requirements — any market entry must be preceded by a robust high-temperature thermal management solution. Sub-Saharan Africa's "boda-boda" motorcycle transport economy (Kenya, Nigeria, Ethiopia combined over 2 million units/year) combined with improving solar power infrastructure creates a medium-term opportunity horizon for Chinese brands entering via their established combustion distribution channels.

Chapter 3 PEST Analysis

I. Policy Dimension

The comprehensive impact of new national standard GB 17761-2024

On September 1, 2025, the new version of mandatory national standard GB 17761-2024 (Electric Bicycle Safety Technical Specification) officially came into effect — the most systematic upgrade since the 2018 version. The standard maintains the three core parameters (25 km/h maximum speed, 55 kg maximum vehicle mass, 400 W motor power) while strengthening requirements in six technical dimensions:

First: Mandatory tamper-proofing. The vehicle electrical system must prevent any means of increasing maximum speed beyond 25 km/h through hardware (physical structure + electrical interlock), eliminating the previously tolerated practice of speed-limit removal via software parameter adjustment. Added BOM cost approximately RMB 50–150 per vehicle.

Second: Mandatory BeiDou/GPS positioning. All newly produced electric bicycles must include a satellite positioning system, uploading location information to a platform for "dynamic safety monitoring" (sudden acceleration and speeding behavior alerts). BeiDou module bulk procurement cost approximately RMB 15–30 per unit.

Third: Mandatory lithium battery safety certification under GB 43854-2024's six mandatory tests (overcharge protection, over-discharge protection, external short circuit, thermal abuse, nail penetration, crush). All lithium modules used in electric bicycles must obtain CCC certification.

Fourth: Upgraded flame-retardant material requirements. Body panels must pass GB/T 5169 flame-retardant tests; battery compartments must be designed with insulation layers and thermal runaway propagation prevention structures.

Fifth: Vehicle mass control clarification. The 55 kg limit now specifies precise measurement conditions preventing evasion by weighing without battery.

Sixth: Production consistency requirements. For the first time, manufacturers are required to establish production process control documents and accept regulatory spot inspections.

The 2025 trade-in subsidy program

Cumulative national trade-ins exceeded 8.46 million units by June 2025 (over 6x year-on-year growth), exceeding the annual target. The program released pent-up replacement demand, guided migration to lithium vehicles (subsidies specifically targeted new national standard-compliant lithium products), and reduced random disposal of old lead-acid batteries.

Charging and swapping infrastructure policy

The National Energy Administration and Ministry of Housing jointly issued charging facility construction guidelines requiring new residential developments to plan centralized charging areas (one charging spot per two vehicles) with monitoring, fire extinguishers, and ventilation. Financial support was provided for upgrading older residential developments. These policies are projected to drive new two-wheeler charging pile installations exceeding 5 million units in 2026, with cumulative installations exceeding 50 million by 2027.

II. Economic Dimension

Delivery economy expansion: Combined daily orders from Meituan, Ele.me, and JD delivery exceeded 150 million in 2025, with approximately 7 million active professional riders creating a stable B2B market of approximately RMB 15–20 billion/year with a 1–2-year replacement cycle.

Consumer stratification: High-net-worth consumers in tier-1 and tier-2 cities show increasing acceptance of premium smart electric motorcycles above RMB 9,999. Mass consumers in lower-tier cities and counties saw demand for RMB 2,000–3,500 lithium commuter vehicles concentrated and released through trade-in policies. The RMB 2,500–4,500 mid-range market is the most fiercely contested battleground.

ASP tailwind from lithium electrification: Industry overall ASP (ex-factory average selling price) reached approximately RMB 3,300 in 2025, up approximately 37% from approximately RMB 2,400 in 2022 — the primary driver of industry revenue (approximately RMB 190 billion) growing far faster than unit volumes (approximately 12%).

III. Social Dimension

Urbanization and the last-kilometer necessity: With China's urbanization rate at approximately 67.4% in 2025, the daily "last 3–15 km" trip in urban areas is the most irreplaceable demand source for electric two-wheelers. Electric two-wheelers outperform any alternative in the urban periphery where subways don't reach and bus wait times are too long.

Professional rider rights and compliance: 2025 saw increased policy attention to delivery rider labor rights, with "flexible employment protection" policies significantly raising workers' compensation coverage; platforms began incorporating electric vehicle compliance standards into platform rules, indirectly driving professional riders' vehicle replacement demand.

Generation Z's demands reshaping product design: The core consumer group for high-end smart electric two-wheelers in 2025, born 1995–2010, prioritizes aesthetics, strong technology feel (color screen + APP + OTA), personalization, and social sharing capability. Ninebot and NIU's product design language aligns precisely with Gen Z's aesthetic sensibilities.

IV. Technology Dimension

Semiconductor cost reductions enabling intelligent connectivity: 4G Cat.1 communication module costs fell approximately 70% from 2020 to 2025 (now approximately RMB 20–28 per unit); BeiDou positioning chips approximately RMB 15–25; FOC motor control MCU approximately RMB 12–20. Combined at approximately RMB 50–75, these enable intelligent features to permeate from premium NIU/Ninebot to mid-range Emma/Yadea products — when the smart hardware BOM is under 2–3% of vehicle cost, "smart" becomes standard rather than differentiator.

On-device AI inference capability: ARM Cortex-A55-class processors (approximately 1–2 TOPS computing) now cost approximately RMB 40–60 per chip, capable of running lightweight 1–2B parameter language models, establishing the technical foundation for "edge AI riding assistants" commercializing in 2026–2027 without cloud connectivity.

V2G technology outlook: With 400 million electric two-wheelers, the distributed storage potential is significant. At approximately 0.3–0.5 kWh dispatchable energy per vehicle, the 400 million fleet represents approximately 120–200 GWh of scheduling potential — equivalent to approximately 120–200 units of 100 MW utility-scale storage — though commercial realization requires unified communication protocols, benefit-sharing mechanism design, and user participation incentives, with small-scale V2G pilots expected in 2028–2032.

SiC power device technology diffusion: Silicon carbide (SiC) MOSFETs — widely adopted in EV main inverters for their high breakdown voltage, low on-resistance, and fast switching — are now penetrating high-end electric motorcycles (rated power over 5,000 W), reducing controller switching losses by approximately 30–50% and improving high-speed cruising efficiency by approximately 3–8%. Domestic SiC manufacturers (San'an Integrated, Xinyan, Tianke Heda) entered high-end electric motorcycle vendor qualification systems in 2025.

Digital twin technology in vehicle R&D: Digital twin technology significantly accelerated vehicle development in 2025 by simulating vehicle dynamics, thermal management, and vibration fatigue in virtual environments — shifting the majority of "physical testing" to "virtual testing," reducing product development cycles by approximately 30–40%.

Chapter 4 China Market Size, Structure, and Competitive Landscape

I. Comprehensive Market Decomposition

Sales and production: China's 2025 full-year new electric two-wheeler sales reached approximately 55–60 million units (midpoint approximately 58 million units); production (including exports) approximately 58–63 million units. At the 2025 ex-factory average selling price of approximately RMB 3,300 per unit, total ex-factory vehicle market size is approximately RMB 189–210 billion. Including the complete upstream value (batteries approximately RMB 70–80 billion, motors and controllers approximately RMB 30–40 billion, other components approximately RMB 60–80 billion) plus charging/swapping operations (approximately RMB 30–50 billion) and aftermarket (approximately RMB 40–50 billion), the full industry chain broad market is approximately RMB 500–600 billion.

The special context of the 2025 sales peak: The 2025 sales figures include a non-recurring factor — the GB 17761-2024 transition period (production allowed under old standards through August 2025, sales of old-standard inventory allowed through December 1, 2025) creating an approximately 6–8 million unit demand pull-forward in Q3, followed by a notably sharp Q4 decline (OVID Research data shows November down 28.7% year-on-year). Excluding this pull-forward effect, true 2025 demand is approximately 50–53 million units, and 2026 will gradually return to normal growth trajectories.

Category structure and price band distribution:

- Electric bicycles (GB compliant, ≤25 km/h): approximately 43 million units (74%), ex-factory average RMB 2,800

- Light electric motorcycles (>25 km/h, ≤50 km/h): approximately 9.5 million units (16%), ex-factory average RMB 3,800

- Electric motorcycles (>50 km/h): approximately 5.5 million units (10%), ex-factory average RMB 8,500

Price band distribution (at terminal retail price):

- Under RMB 1,500 lead-acid commuter: approximately 15% (~8.7 million units, rapidly shrinking)

- RMB 1,500–2,999 low-to-mid lead-acid/lithium mix: approximately 25% (~14.5 million units)

- RMB 3,000–4,999 mid-range lithium: approximately 35% (~20.3 million units, fastest-growing price band)

- RMB 5,000–9,999 high-end lithium: approximately 18% (~10.4 million units)

- Over RMB 10,000 smart electric motorcycles/premium scooters: approximately 7% (~4.1 million units)

II. Deep Competitive Landscape Analysis

Decoding the Yadea + Emma dual duopoly moat: The duopoly's market dominance rests on multiple structural pillars: ① channel density (Yadea 30,000+ stores, Emma 25,000+ stores, with completeness in tier-3, tier-4 cities and counties that no other brand can match); ② scale purchasing cost advantages (annual lithium battery procurement exceeding 6 million packs, achieving purchasing prices 15–25% below competitors); ③ complete price band coverage (from RMB 999 to RMB 15,999, preventing any foothold for targeted segment attacks); ④ brand "mindshare" (the default behavior of hundreds of millions of users is "when replacing a vehicle, go check out Yadea/Emma").

Ninebot's disruptive path: Ninebot's rise is a textbook case of "software product logic disrupting hardware manufacturing." Behind its 2025 sales of 4.09 million units with 64.5% growth: APP daily active users exceeding 1 million (industry high), OTA update frequency approximately once per quarter (far exceeding traditional brands' annual product cycle), user NPS approximately 62 (vs. industry average approximately 25), and industry-leading online channel sales. Ninebot proved that "premium consumers will pay RMB 2,000–5,000 extra for software experience."

NIU's defensive battle: NIU possesses two irreplaceable first-mover advantages: ① clear "China premium smart two-wheeler" brand recognition in overseas markets (Europe, Japan) with established local agent networks; ② user community operations ("NIU-oil tribe") achieving approximately 35% repurchase rate, far above the industry average. However, NIU's moat is being rapidly eroded by Ninebot, whose 2025 flagship products closely match NIU's products in features, range, and pricing.

III. Market Channel System Deep Analysis

Dealer network structure: Approximately 300,000 nationwide electric two-wheeler stores, structured as: ① brand primary dealers (provincial/regional representatives) — approximately 1,000–2,000, responsible for distributing to secondary dealers; ② secondary dealers (city/county stores) — approximately 150,000–200,000, directly facing end consumers; ③ repair service network (third tier) — approximately 100,000–120,000, providing warranty maintenance and after-sales service.

The "three ledgers" of store operations: A typical secondary dealer's economics: ① vehicle sales ledger (primary income source; a mid-range RMB 3,500 lithium vehicle yields approximately RMB 300–400 net profit, approximately 30 units/month = approximately RMB 9,000–12,000/month net); ② repair service ledger (pure profit business, approximately RMB 5,000–10,000/month revenue at over 70% gross margin); ③ trade-in ledger (acquiring used vehicles at RMB 200–800, reselling or parting out, approximately RMB 2,000–5,000/month net).

Online channel's role and limits: The 2025 online penetration rate of approximately 15% faces structural limits beyond 30% due to: large vehicle size precluding standard courier delivery; test-ride experience being irreplaceable online (especially for mid-to-high-end products); and after-sales service requiring offline dealer networks.

Ninebot and NIU's "DTC countertrend": With online sales ratios of approximately 25–30% and 20–25% respectively, far above the industry average, these brands succeed because: ① premium smart consumers research extensively online before purchasing; ② their user bases are concentrated in tier-1 and tier-2 cities where service networks are dense enough; ③ their product standardization reduces the need for physical experience before purchasing decisions.

Chapter 5 Supply Chain Deep Analysis

I. Power Battery Industry Chain Comprehensive Review

Lead-acid battery industry chain operating logic: Lead-acid battery production involves mature processes including lead ore smelting/recycled lead recovery, grid casting, active material preparation, electrode plate coating, formation charging, assembly, electrolyte filling, cap welding, and factory testing. Tianneng Stock's moat in lead-acid comes from scale (annual production exceeding 500 million Ah), its recovery system (partnering with thousands of nationwide recovery networks for low-cost recycled lead), and channel binding (long-term exclusive/preferred cooperation agreements with Yadea, Emma, Tailg).

Shengxin Battery's monopoly position in lithium PACK: Shengxin's dominant position rests on three moats: ① technical barrier (proprietary LFP two-wheeler cell formulations and BMS control algorithm patents optimized for the unique stop-start, high-temperature, vibration operating conditions of two-wheelers); ② customer binding (long-term strategic cooperation with Yadea and Emma prevents new entrants from quickly accessing leading customers); ③ channel effect (Shengxin also holds over 50% share in the Southeast Asian electric two-wheeler market, demonstrating "global small power lithium king" positioning as a co-internationalization partner with Yadea).

II. Motor Industry Chain

Fragmented domestic market: China's annual hub motor production exceeds 60 million units, with over 95% produced by small and anonymous manufacturers concentrated in Wuxi (approximately 30% of national output), Ningbo (approximately 20%), and Guangdong (approximately 15%). Entry-level 250W brushless hub motors are priced at approximately RMB 35–60 ex-factory; high-end 1,000W+ integrated-controller motors at approximately RMB 200–350.

Bafang's international technology moat: Bafang's European market strategy of "price-competitive entry, product upgrade as leverage" — entry-level BBS01/02D series at approximately USD 150–200 retail build supplier relationships; the high-end M600 series directly competes with Bosch Performance Line CX at approximately 60–70% of Bosch pricing, pulling some European mid-tier brands from Bosch to Bafang.

III. Body Structural Components and Lightweighting Trends

Frame material evolution: From iron tubing (lowest end) to high-strength steel (mainstream) to aluminum alloy (high-end), with correlation to vehicle price bands: below RMB 1,500 primarily iron/low-strength steel; RMB 2,000–4,000 primarily Q235/Q355 steel (approximately 70%), with aluminum approximately 30%; above RMB 5,000 primarily aluminum alloy die-casting (approximately 65%).

Aluminum alloy frame rapid adoption: Aluminum frames (primarily 6061-T6 or 6063-T5 alloy) offer key advantages over steel: ① 2–3 kg weight reduction (aluminum frame approximately 2.8–3.5 kg vs. steel frame approximately 4.5–5.5 kg); ② better corrosion resistance; ③ superior aesthetic integration enabling streamlined frame designs. Large integrated aluminum die-cast components — using 3,000–5,000 tonne large-scale die-casting machines to form entire rear frame sections in one piece — represent the cutting edge of 2025 manufacturing trends.

Brake system technology upgrade: GB 17761-2024's stricter braking distance requirements (from 25 km/h to complete stop, ≤4 meters) drove the shift from "low-grade drum brakes" to "disc/hydraulic brakes." In 2025, over 60% of lithium products above RMB 3,500 feature front and rear disc brakes ("dual disc" configuration), up from approximately 20% in 2022.

IV. Smart Hardware Supply Chain System Analysis

BeiDou/GPS positioning modules: Mandatory BeiDou positioning (new national standard requirement) drove a surge in positioning module demand. Two-wheeler BeiDou modules require small form factor, low power consumption, fast cold-start time, and strong vibration resistance. Pricing at approximately RMB 15–30 per unit, with annual new demand of approximately 50–60 million units.

4G IoT communication modules: Quectel EC21/EC25/MC60 series are mainstream choices, supporting 4G LTE Cat.1 (max 10 Mbps downlink, adequate for OTA updates and real-time position uploads). With annual demand of approximately 50 million units under new national standard mandatory connectivity requirements, BeiDou and 4G modules are trending toward SiP (System in Package) integration into a combined "BeiDou+4G dual-function positioning and communication module."

Color instrument clusters and in-vehicle displays: From traditional segment LCDs to color TFT touch screens (displaying maps, navigation, weather, and ride data visualization), instrument upgrades are the most visible pathway to improved "technology feel." Color screen penetration in products above RMB 5,000 reached approximately 80% in 2025; approximately 40% for RMB 3,000–5,000 products.

NFC and biometric anti-theft: Ninebot's 2025 flagship vehicles feature NFC key sensing (smartphone or NFC card replacing physical keys); NIU supports "fingerprint + NFC dual authentication" on some models. These anti-theft technologies address consumers' acute concern about electric bicycle theft (approximately 1 million stolen annually in China).

V. Aftermarket: The Vast Long-Tail Value Network

The aftermarket (parts retail, repair services, insurance, used vehicle circulation, battery recycling) generates approximately RMB 40–60 billion per year based on the 400 million vehicle fleet.

Parts retail backbone: Lead-acid battery replacement (approximately 3 years × 40 million vehicles/year × approximately RMB 350 per set ≈ approximately RMB 14 billion/year), tires (approximately 3 years × 150 million vehicles/year × approximately RMB 80/tire ≈ approximately RMB 12 billion/year), brake pads, chargers — these four items combined represent approximately RMB 38 billion/year in replacement parts driven purely by fleet size × replacement frequency.

Insurance: Electric bicycle insurance penetration reached approximately 25% in 2025, with mandatory insurance pilots rolling out in some cities. If 50% penetration × 400 million fleet × approximately RMB 200 average premium, annual premium scale would reach approximately RMB 40 billion, making it one of the largest new categories in China's non-vehicle insurance market.

Chapter 6 Key Enterprise Deep Analysis

I. Yadea Holdings (HK 1585): Deconstructing the Global Leader's Moat

FY2025 performance deep analysis: Yadea's approximately 16.3 million unit 2025 sales (electric bicycles 11.45 million units +26% YoY, electric scooters 4.81 million +22.5% YoY) demonstrate strong growth across both major categories. Revenue RMB 37 billion, gross margin 19.1% (up approximately 4 percentage points from 2024's 15.2%), net profit RMB 2.91 billion (net margin 7.9%) — net profit growing 128.8% YoY is the highest earnings elasticity in the A/H-share two-wheeler segment in 2025.

Three-tier overseas architecture: Yadea's international layout follows a progressive "export → local assembly → local sales" architecture. Layer one (most mature): complete vehicle exports to markets with low tariff barriers (Middle East, East Africa, Latin America). Layer two (strategic core): local factories in Vietnam, Indonesia, Thailand, bypassing import tariffs for competitive local pricing. Layer three (brand elevation): Japan direct-sales stores and European agent channels, using premium smart products to enter mature markets and strengthen the global premium brand image.

II. Emma Technology (A-share 603529): Channel + Technology Dual Drive

Emma's 2025 revenue of approximately RMB 28 billion and net profit of approximately RMB 2.46 billion, with the net profit gap versus Yadea's RMB 3 billion narrowing rather than widening — demonstrating Emma's profit margin improvement pace is comparable to Yadea's. Core competitive advantages: ① Tianjin manufacturing base cost advantages (lower labor and land costs versus Wuxi, high production worker proficiency from historical depth); ② electric tricycle differentiation (tricycles contributed approximately RMB 1.85 billion revenue, up 38% YoY, a segment where Yadea has no large-scale presence); ③ eVTOL collaboration research plan providing long-term "imagination space" for institutional investors.

III. Ninebot/Segway (A-share 689009): The Software-Defined Disruptor

Ninebot's "software-defined two-wheelers" model received powerful business-level validation in 2025: 4.09 million units sold (+64.5% YoY) + RMB 11.86 billion electric two-wheeler revenue (+64.5% YoY) + RMB 1.76 billion net profit (+62.2% YoY) — three "near-doubling" metrics in synchronized resonance.

Four dimensions of the technology ecosystem: ① Hardware platform: aluminum alloy integrated die-cast frame, high-precision BeiDou RTK positioning (centimeter-level precision), 77 GHz millimeter-wave forward radar (flagship B190C), and self-developed integrated electronic control unit. ② Software ecosystem: Segway-Ninebot Connect APP with over 1 million monthly active users, OTA updates approximately every 3 months including AI riding scores, intelligent route recommendations, and UBI insurance linkage. ③ Business model innovation: the industry's first electric two-wheeler software subscription service (Ninebot Cloud Plus, approximately RMB 9.9/month), with approximately 150,000 monthly paying subscribers in 2025 — a small but commercially significant proof of concept. ④ Internationalization: The Segway brand's "tech mobility" recognition in North America and Europe provides Ninebot's electric two-wheelers with an established brand credential in markets where NIU, Yadea, and others have no comparable pre-existing brand equity.

IV. NIU Technologies (NASDAQ: NIU): The International Premium Brand's Defensive Battle

NIU's 2025 performance (~1.2 million units, ~8% decline) reflects a strategic defense challenge: Ninebot's comprehensive smart catch-up is compressing NIU's differentiation space; NIU's domestic market share (approximately 2%) is difficult to expand further; international markets face European market softness. NIU's very limited strategic options: ① continue deepening technology leadership (next-generation products must maintain a 2–3 generation lead over Ninebot); ② accelerate internationalization (expand NIU Europe's retail network); ③ explore cross-category extension (premium electric motorcycle, electric bicycle adjacencies).

V. Supply Chain Partner Enterprise Deep Assessment

Tianneng Stock faces allocation tensions between deep defense in lead-acid and lithium strategy build-out. Lead-acid still contributes over 93% of revenue, but lead-acid's medium-to-long-term decline (2030 lead-acid two-wheeler penetration potentially only approximately 18%) means no transition is slow attrition. Tianneng's lithium transition path: ① minority stake/acquisition in quality LFP cell suppliers; ② leveraging existing lead-acid sales channels to push proprietary lithium PACK products; ③ finding new growth in ladder utilization (reuse of retired lead-acid/lithium batteries).

Chaowei Power faces similar transition pressure but is behind Tianneng in lithium layout, while differentiating on "safe lead-acid" technology iteration (Chaowei's premium black gold series shows significant improvements in low-temperature performance and high-current discharge) and exploring sodium-ion battery (Na-Ion) two-wheeler applications as a potential cost advantage.

VI. Emerging Vehicle Brand Survival Logic and Differentiation Paths

Xinri Stock (NIS): 2025 sales approximately 2.2 million units, breaking through under "dual brand aging" pressure via "high-end sporting electric motorcycle" (Xinri FROG series, RMB 8,000–25,000 sporting scooters) targeting performance-oriented riders.

Luyuan Group: Core moat is the "liquid-cooled lead-acid technology" patent system, extending motorcycle liquid-cooling technology to lead-acid battery management, improving high-temperature (above 45°C) cycle life by approximately 40–60%. Strong channel density in Southern China.

CFMoto's electric motorcycle strategy: CFMoto (A-share 603026), one of China's most internationally competitive motorcycle brands, launched ZEEHO as an independent electric motorcycle brand. The ZEEHO AE8/AE8S series (maximum 150 km/h, 160 km range) entered European markets (Germany, France, Italy) after obtaining e-Mark certification — the most mature case of Chinese brand internationalization in "high-performance electric motorcycles." ZEEHO's technical highlights include a self-developed "dual flywheel permanent magnet synchronous motor" and an integrated liquid-cooled motor + controller thermal management system.

Japanese brands' residual position in China: Honda, Yamaha, and Suzuki's electric two-wheeler offerings in China have failed to attract Chinese consumers — not due to technical incapability, but strategic resource allocation: Japanese companies prioritize their electric transition efforts in Southeast Asian markets (where they dominate combustion), with China effectively treated as a "strategically ceded" territory. This absence benefits Chinese brands' high concentration in the domestic market.

Chapter 7 Midstream Industrial Belts and Regional Competitive Landscape

I. Jiangsu Wuxi: The Global Electric Two-Wheeler Industry Heartland

Through a systematic analysis of distribution and operating data of tens of thousands of electric bicycle-related factories, the Tianxia Gongchang Industrial Research Institute finds Wuxi and the Suzhou-Wuxi-Changzhou region to be China's — and the world's — absolute core of the electric two-wheeler industry. From vehicle manufacturers (Yadea global headquarters + Wuxi manufacturing base, NIU main factories, Emma Suzhou base) to core components (Wuxi and Changzhou motor factories, controller factories, frame factories, instrument factories) to supporting industries (logistics, tooling, rapid prototyping services), a super-cluster with approximately 80 km diameter has formed. Supply chain response time within the cluster (from order to delivery to the vehicle manufacturer) typically does not exceed 4 hours — a competitive advantage no other region can replicate.

The policy dimension: Wuxi's city government has designated the electric two-wheeler industry a key development sector, providing research land subsidies (Yadea Technology Research Institute receives government land use incentives), talent attraction programs (Taihu Talent Program offering housing subsidies and research startup funds for senior technical talent), and green manufacturing upgrade subsidies (supporting the introduction of automated assembly lines and electrophoretic painting equipment).

II. Zhejiang Taizhou: Electric Motorcycle and High-End Components Base

Taizhou's comparative advantage rests on its strong combustion motorcycle manufacturing heritage. The 1990s–2000s Taizhou (centered on Luqiao and Wenling) era as the world's largest low-end combustion motorcycle manufacturing base built a complete supply chain for critical motorcycle components — engine casting, transmission gearboxes, suspension damper systems, brake systems, high-power driveline components. In the transition from combustion to electric motorcycles, these existing craft capabilities are directly reused. Taizhou is also China's most important production base for electric vehicle brake systems (disc and drum brakes), with annual shipments exceeding 100 million units, over 60% exported to Southeast Asia and Europe.

III. Tianjin: Northern Manufacturing Center and Historical Industrial Heritage

Tianjin is the earliest industrial origin of Chinese electric two-wheelers (China's first electric power-assisted bicycle was produced here in 1996), nurturing the early supply ecosystem for Tianneng, Chaowei lead-acid batteries, and a large number of body panel (plastics, seats) and low-to-mid-end accessory (wiring harnesses, switch components) suppliers. Emma Technology's Tianjin headquarters and primary manufacturing base is a continuation of this historical depth.

IV. Guangdong Shenzhen + Dongguan: Smart Hardware Supply Chain Highland

The Shenzhen-Dongguan metropolitan area is China's most dense electronics manufacturing region, and this advantage is fully leveraged by electric two-wheeler intelligent upgrades: controller MCU chips (GD32, N32 domestic ARM chips), IoT modules (Quectel MC60, EC20 4G Cat.1 modules), BeiDou positioning modules, LED driver chips, TFT color display modules, and NFC chips all have dense supplier presence in Shenzhen or Dongguan. Shenzhen's electronics manufacturing services ecosystem (PCB design/fabrication, SMT assembly, tooling rapid prototyping, IC selection evaluation) allows NIU and Ninebot new product development cycles from "drawings to production samples" in only approximately 6–8 weeks.

V. Vietnam: The Central Node of Southeast Asian Industrial Belts

Vietnam (centered on Hanoi's northern provinces and Ho Chi Minh City's surrounding areas) is rapidly becoming the dual role of most important overseas manufacturing base and sales market for Chinese electric two-wheeler brands. Yadea's Vietnam factory (Quang Nam Province, South Korea Industrial Zone) has annual capacity exceeding 1 million units, serving local Vietnamese market sales and exporting to other ASEAN members. Tailg has an assembly factory in an industrial park near Hanoi. Vietnam's government "manufacturing localization rate improvement plan" (LCR targets rising annually) will push Chinese suppliers to establish local production in Vietnam — most likely starting with labor-intensive processes such as frame welding and plastic parts injection molding.

Chapter 8 Segment Deep Research

I. Commuter Electric Bicycle: Core Competitive Logic

The typical commuter user's requirement priority order is: reliability ("can't run out of battery on the road") > price ("must be affordable") > appearance ("can't be too ugly") > smart features ("APP or no APP is fine"). This priority guides product design: commuter vehicles' core competitiveness is "doing the most important things (range, durability) to the fullest within budget," rather than stacking smart features.

In 2025, lithium electrification in mid-range commuter vehicles achieved a penetration rate leap from approximately 40% in 2024 to approximately 60%, catalyzed by the "trade-in subsidy + new national standard guidance" dual drivers. The core drivers of consumers switching to lithium commuter vehicles: ① lithium range (60–100 km) significantly superior to same-price lead-acid (40–60 km); ② trade-in subsidies directly covering the RMB 200–400 price premium, lowering the psychological threshold.

II. Food Delivery Rider Scenario: "Professional Grade" Requirements

Professional delivery riders represent China's most "professional" (daily riding over 10 hours, 150–250 km) and most "demanding" (any vehicle failure directly translates to income loss) user segment.

Range is the first requirement: Riders need to complete a single work segment (4 hours, approximately 80–100 km) without charging, requiring over 100 km usable range — demanding a lithium capacity of 48V/30Ah (approximately 1,440 Wh) or 96V/20Ah (approximately 1,920 Wh).

Battery-swap convenience is the second requirement: In 2025, leading battery-swap operators (Tower Energy, EasyGo) achieved swap station density of approximately one station per 200–300 meters in tier-1 city high-density delivery zones, with swapping time approximately 1–2 minutes — a complete victory over charging (4–6 hours) as a time solution.

Durability is the third requirement: Professional riders' annual mileage (approximately 50,000–80,000 km) is approximately 15–25x ordinary consumer mileage, demanding specialized reinforcement in frame welding precision, suspension travel, waterproofing, and wiring harness abrasion resistance.

III. Shared Mobility Platform Vehicle Technical Standards

Hellobike, Meituan Bike, and DiDi Qingju impose the market's most stringent B2B procurement specifications: 3-year/100,000 km service life requirement for main structural components; IoT module with GPS/BeiDou dual-mode positioning and OTA upgrade support; critical component replacement possible in 5 minutes with specialized tools; and anti-vandalism protection. These specifications concentrate supply to a handful of vendors — Yadea and Emma are the two primary suppliers.

IV. High-Power Electric Motorcycle Export Market Opportunity Matrix

European market: 2025 European electric motorcycle annual registrations approximately 300,000–400,000 units. Chinese-made high-power electric motorcycles have a compelling advantage: at equivalent performance, Chinese products cost approximately 30–50% of European domestic brands (Zero, Energica). CFMoto's CRX (e-Mark L3 certified for European road use) sells at approximately €8,000–10,000 versus Zero SR/F at approximately €16,000–18,000 — exceptional value.

Southeast Asian market: Vietnam, Thailand, Indonesia combined annual high-performance scooter sales exceed 8 million units (currently almost entirely combustion). Chinese brands' opportunity: use 75V/30Ah+ lithium, 3,000W+ motor high-performance electric scooters to target Honda PCX 125cc (Vietnam's best-selling scooter, approximately 500,000 annual units) at approximately 11,000–14,000 RMB equivalent pricing.

V. Business Model Innovation: From "Selling Vehicles" to "Mobility Service Subscriptions"

Traditional electric two-wheeler business models involve a single transaction at purchase, with no ongoing revenue relationship. This captures minimal lifetime value from users.

Ninebot's subscription exploration: Three-tier subscription plans — basic (free, basic APP + automatic OTA updates), enhanced (RMB 9.9/month, adding high-precision riding analysis + theft tracking priority response + UBI insurance discount linkage), professional (RMB 29.9/month, adding real-time navigation with RTK precision + road condition alerts + multi-vehicle family management + cross-city roadside assistance). Currently approximately 150,000 paying users (approximately 1.5% penetration), far below automotive SaaS rates (Tesla FSD approximately 15–20% paying penetration) but represents the industry's first validation of willingness to pay for software.

Battery-swap subscription income logic: Swap operators (Tower Energy, EasyGo, Hellobike Swap) offer monthly swap packages (approximately RMB 200–400/month depending on city and package level) for unlimited swaps — converting the hard demand for "vehicle charging" into a predictable monthly recurring revenue stream, the most mature commercial implementation of mobility service subscriptions.

Used vehicle trading platform opportunity: The approximately RMB 20–30 billion/year fragmented used electric two-wheeler market lacks professional evaluation standards, trading platforms, and quality guarantee systems. A specialized used vehicle platform offering professional "electrical inspection" reports (battery health, mileage records, collision records), platform warranty (90-day free repair after purchase), and standardized pricing represents a substantial commercial opportunity.

Helmet market policy and commercial linkage: New national standards require purchase-with-vehicle delivery of a GB 811-compliant helmet. In 2025, the mandatory helmet policy drove approximately 80–90 million units of accompanying helmet sales (estimated market size RMB 50–80 billion), growing approximately 3x from 2022. Brands' helmet strategies — Yadea's "V-series co-branded helmet" and Emma's "AIMA dedicated helmet" — transform compliance giveaways into brand extension products and mobile advertisement billboards.

Deep binding with the sharing economy: Hellobike, Meituan Bike, and DiDi Qingju collectively operate over 15 million shared electric vehicles in approximately 300 cities nationwide, serving over 10 billion rides annually. The relationship between shared platforms and vehicle manufacturers has evolved beyond simple B2B procurement into "strategic symbiosis," with vehicle manufacturers deeply participating in platform technical standard setting (remote lock communication protocols, OTA interfaces, battery swap standards) and platforms viewing manufacturers as technology partners.

VI. Special Application Scenarios: Industrial and Commercial Electric Two-Wheelers

Mining and factory internal commuting: Large mines and industrial parks generate stable B2B demand for specialized electric two-wheelers (factory specifications, no public road certification, maximum approximately 20 km/h, range approximately 40–60 km, emphasizing durability and load capacity), procured through project tendering (typically 50–500 units per procurement), with higher margins than consumer models.

Public safety patrol vehicles: Police electric motorcycles (maximum approximately 60–80 km/h, range approximately 100–150 km, equipped with emergency lights, radio communications mounts, body camera mounts) represent stable procurement with special requirements for reliability in the field.

Express delivery terminal distribution: Express couriers (SF Express, JD, STO, Yuantong, etc.) constitute a B2B market parallel to but distinct from food delivery — prioritizing cargo box/rear rack volume and high daily mileage durability, with less urgent battery-swap dependency given fixed station access for charging.

VII. Consumer Finance and Installment Purchase Market Impact

Installment penetration: In 2025, installment purchases account for approximately 20–30% of terminal retail (primarily for mid-to-high-end products above RMB 3,000). Installment makes "accepting a slightly more expensive lithium vehicle" psychologically easier — a RMB 3,500 vehicle in 12-month installments is approximately RMB 300/month.

Used vehicle residual value's effect on installment decisions: Ninebot and NIU premium products' resale value (approximately 40–60%) significantly exceeds Yadea/Emma entry-level products (approximately 15–25%). When users adopt a "2-year installment + trade-in" consumption path, the high residual value product's "effective ownership cost" (purchase cost minus trade-in residual) may actually be lower than the low-residual-value product, rationally driving selection toward premium brands.

Chapter 9 Technology Evolution Roadmap

I. Power Battery Technology Leap Paths

Path 1: Continuous LFP energy density improvement

LFP cell energy density will rise from 155–165 Wh/kg in 2025 to 175–185 Wh/kg by 2030 through: ① high-nickel LFP (LNFP/LFMP): introducing manganese/nickel atoms to raise working voltage from 3.2V to 3.5–3.7V, improving energy density while maintaining safety; CATL's "NREGS ultra-fast charging battery M3P" is the representative, with two-wheeler application verification completed in 2025; ② cathode particle engineering: carbon nanotube coating, single crystal treatment, optimized particle size distribution; ③ electrolyte system innovation: high-concentration electrolytes and fluorinated carbonate solvents offering superior thermal stability in high-temperature environments.

Path 2: Long-term solid-state battery breakthrough

All-solid-state lithium batteries (ASSB) theoretically eliminate lithium dendrite short-circuit safety risks while raising energy density above 300 Wh/kg. Commercial constraints for two-wheeler applications include: manufacturing cost (approximately 5–10x LFP currently), interface impedance, and poor low-temperature ionic conductivity. Small-batch solid-state two-wheeler flagship products (priced approximately RMB 15,000–25,000) are expected to debut in 2027–2028, with relatively mature mass production possible in 2030–2032.

Path 3: Standard battery-swap pack ecosystem integration

The Ministry of Industry and Information Technology's push for the D-series standard battery pack (D1: 48V/12Ah, D2: 60V/12Ah, D3: 72V/20Ah, unified exterior dimensions and interface protocols), if mandatorily implemented in 2026–2027, would break proprietary battery standards across brands, enabling truly cross-brand battery-swap service and significantly improving swap infrastructure utilization. Resistance from leading vehicle brands (whose proprietary packs serve as user lock-in mechanisms) suggests the D-series standard will advance with a "B2B first, B2C second" strategy.

II. Charging Technology Rapid Evolution

Slow charging evolution: Current mainstream chargers operate at 1C rate (approximately 4–6 hours to full charge, CC-CV two-stage strategy, Flyback Converter topology at approximately 85–88% efficiency). High-end 2025 lithium electric bicycles already include 1.5C smart fast chargers (~2.5–3 hours), with BOM cost approximately RMB 80–120 higher than standard chargers.

Fast charging standardization: China Automotive Engineering Research Center (CAERC) launched a "two-wheeler fast charging protocol standardization" research project in 2025, targeting publication of a recommended industry standard by 2027. This would enable brand-agnostic public fast charging stations to serve any brand's electric two-wheeler, similar to USB-C standardization's effect on smartphone charging convenience.

Wireless charging long-term potential: Inductive wireless power transfer (WPT) appeared as an optional feature on some premium electric motorcycles (above RMB 20,000) in 2025, but is limited by efficiency losses (approximately 4–5 percentage points below wired) and cost (approximately RMB 800–1,500 per vehicle-side receiver + ground transmitter set). Magnetic resonance wireless charging (5–15 cm transmission distance, 500–1,000 W power) maturing and cost reductions could enable "parking spot embedded wireless charging pads — park and auto-charge" experiences in some smart parking facilities by 2028–2030.

V2G coordinated storage potential: When public charging piles support bidirectional charging (V2G technology), electric two-wheeler battery packs can supply power back to the grid during non-riding periods, becoming part of distributed storage. With approximately 0.3–0.5 kWh dispatchable energy per vehicle, coordinating millions of vehicles offers significant grid peak-load management potential. Chinese electric two-wheeler industry V2G pilot applications are expected in 2028–2030 after bidirectional charging hardware standards and grid coordination mechanisms mature.

III. Smart Connectivity Security and Privacy Challenges

As intelligent connectivity deepens, cybersecurity and personal privacy protection become critical accompanying challenges.

Riding data privacy boundaries: Highly intelligent electric two-wheelers continuously record and upload precise riding trajectories (BeiDou centimeter-level precision, updated every second), riding speed and acceleration, parking location, and riding time and frequency. The Cyberspace Administration of China (CAC) applied its automotive data security regulations to intelligent electric two-wheelers in 2025, requiring: ① explicit disclosure of data collection content and purposes; ② user ability to query and delete personal riding data; ③ prohibition of riding data transmission overseas; ④ prohibition of using riding location data for targeted advertising without explicit user consent.

Cybersecurity attack surface: Remote lock/unlock functionality creates potential attack vectors; OTA update channels could be compromised to push malicious firmware. Security assessments showed Ninebot and NIU's OTA code signing verification, API authentication, and data transmission encryption (TLS 1.3) are relatively mature; some mid-range smart products from Yadea/Emma still have room for improvement in security coding standards, particularly regarding third-party IoT module firmware security quality.

"Data as asset" regulatory dynamics: The tension between the commercial value of riding big data (urban planning, insurance actuarial, targeted advertising) and personal privacy protection produced the industry's first systematic regulatory-industry debate in 2025. The CAC's draft regulations propose that "commercial use of riding trajectory data requires explicit user consent, revocable at any time" — if strictly enforced, this would significantly reduce the commercial potential of riding data.

IV. Electric Two-Wheelers and Urban Management: Riding Compliance and Enforcement

Smart enforcement technology: In 2025, Beijing, Shanghai, and Shenzhen piloted "AI camera + automatic electric vehicle violation recognition" systems, identifying violations (running red lights, wrong-way riding, speeding) in real time via AI vision algorithms. The technology substantially improves violation detection rates.

Systematic solution for rider professionalization and compliance: Regulators are exploring a "rider professional qualification + platform accountability" combined approach: delivery platforms must be responsible for their riders' riding compliance rates (platform receives connected warnings if riders violate rules), and establishing a "rider points system" (violations deduct points, depleting points leads to temporary delivery suspension). The Shanghai and Shenzhen pilot programs in 2025 saw food delivery rider red-light running rates fall approximately 40% year-on-year, demonstrating the "platform accountability + points" compound constraint's significant behavior correction effect.

Chapter 10 Comprehensive Risk Factor Assessment

I. New National Standard Transition Period Market Volatility

The GB 17761-2024 implementation timeline created a demand pull-forward in 2025 Q3 followed by a sharp Q4 decline (some months down over 25% year-on-year). This policy-driven "pull-forward → pullback" cycle has precedent in new national standard implementation history (GB 17761-2018 in 2019 triggered a similar pattern), with markets typically taking 2–3 quarters to return to normal growth trajectories.

Yadea and Emma, with their vast dealer networks and strong market control capabilities, completed old-standard vehicle channel digestion in Q3 2025 with manageable financial impact. Smaller brands face larger inventory write-down risks, further exacerbating market concentration divergence.

II. Lithium Battery Safety Incident Systemic Risk

A series of electric bicycle lithium battery charging fire incidents in 2024–2025 drove regulators to strengthen charging safety management, with cities issuing "no indoor or stairway charging" regulations.

Short-term: Some consumers delay lithium vehicle purchases due to outdoor charging inconvenience; lead-acid vehicles (safer, no fire risk from forgetting to unplug charger) regain relative advantage.

Medium-term: Large-scale public charging facility construction progressively resolves charging inconvenience in 2026–2027; leading suppliers' (Shengxin, Tianneng) high-safety BMS lithium products differentiate while low-quality lithium is cleared from the market.

Long-term: Lithium safety incident risks will continuously decline through technology upgrades and infrastructure improvements, not presenting a fundamental obstacle to the lithium electrification trend.

III. EU Anti-Subsidy Tariff Deep Impact

Impact on Bafang: Bafang's revenue is approximately 80% European-derived; a 10–20% EU anti-subsidy tariff on Chinese e-Bike motor imports would directly erode approximately 5–10 percentage points of Bafang's gross margin. Countermeasures: ① establishing European origin assembly factories in Eastern European non-EU members (Poland/Czech Republic); ② upgrading Chinese factory technology content (shifting to higher-end products to absorb tariff increases through pricing); ③ accelerating non-European market development (Southeast Asia, Middle East, Africa).

Impact on complete-vehicle brands: Yadea's European whole-vehicle exports of approximately 50,000–100,000 units/year and NIU Europe's approximately 30,000–50,000 units represent limited tariff exposure; if tariffs land, they would trigger retail price increases (approximately RMB 800–2,000 equivalent) in the price-sensitive European mid-range market, with local assembly as the primary countermeasure.

IV. Price War Risk and Systemic Threats to Industry Profitability

The 2024–2025 profitability improvement cycle's sustainability is a core investor concern. Historical price war patterns: Chinese manufacturing industry price wars typically follow "overcapacity → inventory buildup → market-share-for-price tradeoff → industry-wide price reduction → gross margin collapse → weaker capacity exits → industry reshuffle." The electric two-wheeler industry experienced one such cycle in 2018–2021.

Sustainability analysis: The 2025 improvement drivers (falling LFP cell prices → lithium electrification ASP uplift + cost reduction dual tailwind) continue in 2026–2027 if: ① LFP cells continue falling (to below RMB 0.30/Wh, enabling lithium vehicle average selling prices to decline while maintaining margins — beneficial lithium electrification acceleration rather than margin compression); ② leading brands maintain pricing discipline (resist Tailg post-IPO aggressive market share grab attempts); ③ post-new-standard demand decline depth doesn't trigger capacity utilization falls leading to defensive price competition.

Dual duopoly pricing system defense tools: Yadea and Emma have proactive tools to resist price wars: price band stratification (entry models absorb low-price competition, mid-to-high-end models don't compete on price), dealer incentive management (better channel partner margins than competitors), and product upgrades (maintaining high-end model pricing through new features and colors).

V. Service System Construction Challenges in Overseas Expansion