Abstract

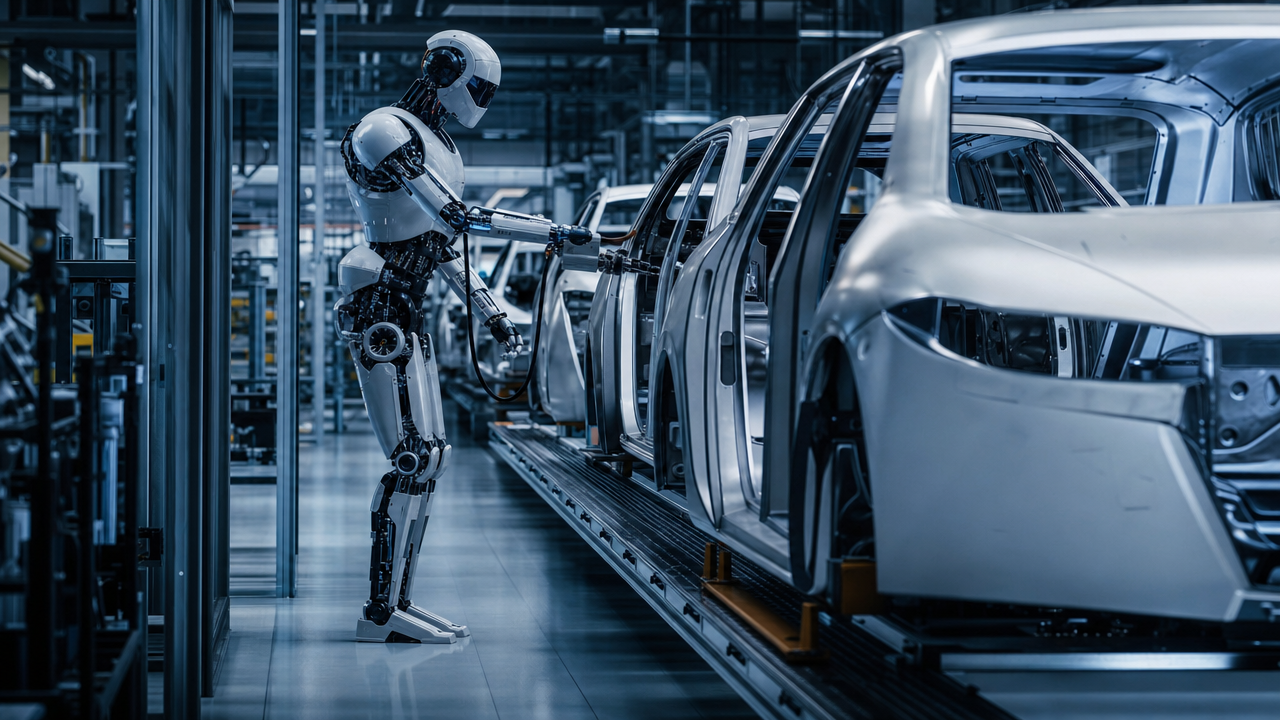

2026 is the mass-production year for humanoid robots. This is not a prediction — it is fact: by end of 2025, global humanoid robot shipments exceeded 17,000 units, with Chinese manufacturers contributing approximately 14,400 units (84.7% of global share); Unitree Robotics surpassed 11,000 cumulative units of a single bipedal model, ranking first globally; Agibot reached 5,000 cumulative units across three product lines; UBTech's Walker S1 completed multiple rounds of scale deployment in BYD, Zeekr, and Geely factories, and secured a single order worth CNY 250 million — the largest humanoid robot commercial order on record. Meanwhile, Tesla Optimus runs around the clock at Fremont, Figure AI's Figure 02 supported production of over 30,000 BMW X3 vehicles at Spartanburg, and Apptronik Apollo entered Mercedes-Benz's Berlin Digital Factory Campus.

Three forces drive this mass-production wave. First, US players led by Tesla and Figure AI, leveraging end-to-end AI and manufacturing ecosystem advantages, pulled humanoid robots into automotive production lines. Second, China's core trio — Unitree, Agibot, and UBTech — completed the critical leap from "prototype showcase" to "batch delivery" in 2025, backed by cost advantages and integrated supply chains. Third, warehouse-first player Agility Robotics established the first quantifiable commercial loop in logistics — Digit moved over 100,000 tote bins at GXO, setting the industry benchmark.

The technological foundation of this wave is the explosive development of embodied intelligence foundation models. NVIDIA released Isaac GR00T N1 at GTC 2025 in March — the world's first open-source humanoid robot foundation model; Figure AI's Helix system achieved zero-shot generalization for bimanual tasks; Agibot released GO-1, covering its Expedition A2 and Lingxi X1 product lines. Rising model capability is driving humanoid robots from "teach-and-replay" toward "language-driven open-task execution."

On the supply chain side, China's domestic substitution accelerates. Levo Harmonic (688017) shipped 425,200 harmonic reducers in FY2025, +72.48% YoY, with net profit doubling; Bestec (300580) planetary roller screws approach mass production; Inovance (300124) holds 27.6% of domestic servo motor market share, ranking first. From reducers to lead screws, motors to sensors, humanoid supply chains are rapidly completing a structural shift from import dependence to domestic dominance.

Key metrics summary:

- China 2025 humanoid robot shipments: ~14,400 units, 84.7% global share; 2026E: ~62,500 units (TrendForce), +94% YoY.

- China 2030 humanoid robot market expected ~CNY 870 billion (CAEI); global shipments may reach 1.2 million units, China >85%.

- Price curve accelerating down: 2025 industrial units ~CNY 300,000–650,000; 2026 target ~200,000–300,000; 2028–2030 may break below 100,000.

- Primary market activity: China humanoid track raised ~CNY 20 billion in 2025; Unitree Science-tech IPO filed March 2026, raising ~CNY 4.2 billion at ~CNY 42 billion valuation.

- Unitree FY2025 revenue: CNY 1.699 billion, adj. net profit CNY 590 million; ~32.4% global market share, No. 1 worldwide.

- Levo Harmonic FY2025 revenue: CNY 571 million, +47.31% YoY; net profit doubled.

Core conclusions:

- The central challenge of mass-production year 2026 is not "can we build it" but "can we drive costs through at scale." Embodied AI model generalization remains the largest uncertainty, determining whether humanoid robots can cross from "fixed workstations" to "flexible production lines."

- China's structural advantage lies in cost and supply chain, not model capability. The US leads China by roughly 12–18 months on foundation model capability, but China is building irreversible competitive moats in component localisation, manufacturing cost, and vertical application scenarios.

- The four-tier application path — "factory fixed workstations → warehouse logistics → commercial services → home services" — remains the dominant narrative. 2026–2028 core battlegrounds are automotive/3C factories and warehouse logistics; home scenarios can form scale markets no earlier than 2030.

Chapter 1 Definitions, Taxonomy and Full Industry Chain Overview

1.1 Definition and Essence of Humanoid Robots

A humanoid robot is defined as a robotic system with a morphology resembling humans — head, torso, dual arms and legs — capable of autonomous movement and task execution in environments designed for humans. Two core requirements: first, human-like morphology; second, scenario generalisation — the ability to act autonomously in unstructured human environments, not merely execute preprogrammed tasks at fixed workstations.

The human form is a means, not an end. Existing factory automation — robotic arms, AGVs, collaborative robots — can efficiently automate specific structured scenarios but cannot handle tasks requiring coordinated dual-arm operation, free movement through human-scale spaces, or working alongside humans. The humanoid form naturally fits environments designed for humans: operating human tools, using door handles, climbing human-designed staircases, executing collaborative tasks beside human workers.

From an engineering perspective, three technical challenges define modern humanoid robots: (1) Mechanical structure — full-size humanoids typically have 20–40 degrees of freedom (DOF), requiring many joint actuators to meet torque, speed, weight and power constraints while maintaining high reliability; (2) Perception systems — real-time 3D sensing of pose, obstacles and manipulation targets, using RGB-D cameras, LiDAR, six-axis force/torque sensors, and tactile sensor arrays; (3) Embodied intelligence — the core technical bottleneck, enabling robots to learn new tasks from observation and generalise learned knowledge to new scenarios.

1.2 Taxonomy

By morphology: Full bipedal (Unitree H1/H2, Tesla Optimus, Figure 02, UBTech Walker S1, Agibot Expedition A2, Fourier GR-1); Wheeled humanoid (Agibot A2-W, CloudMinds HARIX wheeled); Fixed/mobile-base dual-arm (Agibot Sprite series, ABB YuMi).

By size: Full-size (160–180 cm, 50–80 kg) — industrial main force; Mid-size (120–150 cm) — safer for service scenarios; Desktop/Education (30–80 cm) — algorithm verification.

By application: Industrial manufacturing; warehouse logistics; commercial service; home service; research/development.

By joint drive: Harmonic reducer drive (compact, high precision, lightweight — wrists, elbows, shoulders); RV reducer drive (high load, high rigidity — hips, knees, ankles); Planetary roller screw linear drive (high-efficiency linear actuation — leg joints on wire-driven designs like Optimus/Figure); Frameless torque motor direct drive (fast response, backdrivable — Unitree H1/H2 selected joints).

1.3 Full Industry Chain

Upstream (core components): Joint actuators (harmonic/RV reducers, planetary roller screws, frameless motors); sensing systems (depth cameras, LiDAR, force/torque sensors, tactile arrays, IMU); computing platforms (NVIDIA Jetson Thor/Orin); power systems (Li-ion battery packs); structural members (CFRP, aluminium die-cast, titanium 3D-printed).

Midstream (integration and software): Complete machine R&D and manufacturing; embodied foundation models (Isaac GR00T N1, Helix, GO-1, Tesla E2E); simulation platforms (Isaac Sim, Genesis, MuJoCo); operating systems and middleware (ROS 2).

Downstream (system integration and application): Automotive factory integration; warehouse logistics integration; commercial service scenarios; Robot-as-a-Service (RaaS).

1.4 Key Commercial Model Benchmarks (2025)

| Model | Company | Height (cm) | Weight (kg) | Payload (kg) | Total DOF | Hand DOF | Price (CNY) | Primary Use |

|---|---|---|---|---|---|---|---|---|

| Optimus Gen 2 | Tesla | 173 | 57 | 20 | 28 | 11/hand | Internal | Auto factory |

| Figure 02 | Figure AI | 167 | 70 | 25 | 32 | 16/hand | Custom | Auto factory |

| H1 | Unitree | 180 | 47 | 30 | 19 | 12/hand | ~650,000 | Industrial/R&D |

| H2 | Unitree | 176 | 50 | 30 | 40+ | 20+/hand | ~500,000 | Industrial mass |

| G1 | Unitree | 127 | 35 | 15 | 23 | 10/hand | 99,000 | Dev/Research |

| Walker S1 | UBTech | 171 | 70 | 40 | 41 | 11/hand | <300,000 | Auto factory |

| Expedition A2 | Agibot | 175 | 63 | 35 | 50 | 14/hand | ~450,000 | Auto/Mfg |

| GR-1 | Fourier | 165 | 65 | 50 | 40 | 12/hand | ~700,000 | Industrial/Rehab |

| PM01 | EngineAI | 164 | 60 | 25 | 35 | 12/hand | From 88,000 | Dev/Service |

| Apollo | Apptronik | 173 | 73 | 25 | 28 | Swappable | Custom | Auto factory |

| Digit | Agility | 175 | 65 | 16 | 16 | Gripper | RaaS | Warehouse |

1.5 Industry Chain Key Economic Indicators (2025)

Whole machine level: Global shipments ~17,000 units; China ~14,400 (84.7% share); China market ~CNY 1.55 billion; Unitree revenue CNY 1.699 billion (net profit CNY 590 million, 32.4% global share); UBTech revenue ~HKD 1.62 billion.

Joint actuator level: Harmonic reducer domestic substitution rate ~65%; Levo Harmonic FY2025 harmonic reducer sales 425,200 units, average price ~CNY 1,320/unit; RV reducer domestic rate ~55%; planetary roller screw domestic rate ~15% (Bestec advancing); frameless motor domestic rate ~70% (Inovance largest supplier).

Sensor level: 6-DOF force sensor import dependency ~60%; depth camera domestic rate ~75% (Orbbec leading); solid-state LiDAR domestic rate ~80% (RoboSense, Hesai leading).

Capital market: China humanoid track primary market 2025 fundraising ~CNY 20 billion; Unitree IPO plans to raise CNY 4.2 billion (filed March 2026, ~CNY 42 billion valuation); Agibot valuation >CNY 15 billion; Levo Harmonic FY2025 net profit CNY 124 million (doubled YoY).

1.6 Historical Analogies and Industry Lifecycle

The closest historical analogy is the NEV (new energy vehicle) industry (2015–2025): from prototype to scale production over ~8–10 years, with hundreds of early entrants, domestic component substitution (battery/motor/BMS), and 90%+ cost reduction (battery packs). The deep structural similarity: both are "mechatronics + AI software" complex systems; both rely on domestic component localisation to compress costs; both face the reliability gap from "showcase" to "mass production"; both benefit from China's complete manufacturing ecosystem. The key difference: humanoid AI software complexity (embodied foundation models) far exceeds NEV software complexity, suggesting a longer evolution cycle.

Chapter 2 Global Competitive Landscape and Key Overseas Players

2.1 Global Landscape Overview

As of early 2026, the global humanoid robot market shows a three-dimensional structure: US players dominate AI capability and ecosystem; China dominates production scale; European players seek vertical scenario breakthroughs. China shipments ~14,400 in 2025 (84.7% global), but US retains advantages in model capability, single-round funding scale, and downstream ecosystem influence.

2.2 Tesla Optimus: The Largest Variable

Tesla Optimus remains the most closely watched humanoid robot project globally. Gen 2 debuted in late 2024 with frameless motor-driven fingers (11 DOF/hand), 2-DOF ankle design, and Newton physics-engine-based simulation training. FY2025 data: ~5,000 units deployed internally at Fremont for battery pack and wire harness assembly. Q4 2025 announcements: Tesla is converting Fremont Model S/X production capacity (halting both models Q2 2026) to Optimus manufacturing; a dedicated Optimus line at Gigafactory Texas targets remote annual capacity of 10 million units (far term). 2026 target: 50,000–100,000 units, with some external customer deliveries.

Optimus' core differentiation: FSD end-to-end visual AI migration capability (world's largest real-drive video dataset, Dojo compute cluster) plus Tesla's proven mass manufacturing cost engineering from Model 3 ramp.

2.3 Figure AI: Industrial Pioneer

Figure AI (San Jose) raised USD 935 million total, with investors including OpenAI, Microsoft, NVIDIA, and Jeff Bezos's Bezos Expeditions. Figure 02: 167 cm, 70 kg, 25 kg payload, 32 DOF total (16 body + 16 hands). BMW Spartanburg deployment over ~11 months in 2025: 1,250 operating hours, supporting >30,000 BMW X3 vehicles, moving >90,000 components and ~1,200,000 steps. BMW subsequently expanded to Leipzig plant (Europe's first humanoid robot deployment in production). Figure 03 redesigned the wrist architecture — the highest failure point at BMW — eliminating distribution boards and dynamic cabling, with each wrist motor controller communicating directly with the main computer. Figure 03 introduces the Helix AI system: a VLA (vision-language-action) model enabling zero-shot bimanual task execution.

2.4 Boston Dynamics: Motion Control Benchmark

Electric Atlas (2024) abandoned hydraulics for full electric joint actuators, with running speed >4 m/s. Completed demonstrations at Hyundai's Ulsan plant in 2025. Spot (quadruped) remains core revenue source with 1,500+ commercial customers globally.

2.5 Agility Robotics: Warehouse Pioneer

Digit is the world's first humanoid robot to achieve commercial scale deployment. Warehouse-first design: bipedal walking with gripper optimised for tote handling (not dexterous fingers), ~175 cm, ~16 kg payload. 2025 milestone: >100,000 totes moved at GXO Flowery Branch — the first independently verifiable commercial-scale humanoid robot operation count. Amazon testing Digit for empty tote recycling. The RaaS model (pay-per-tote) has industry demonstration value: converting CapEx to OpEx, providing predictable recurring revenue.

2.6–2.8 Other Key Players

1X Technologies (Norway): OpenAI-backed, Neo Gamma full-size bipedal targeting home service. Core philosophy: "data density over data volume." 2025: Neo Beta pre-commercial test version released.

Sanctuary AI (Canada): Phoenix with ~20 DOF/hand — industry's highest commercial hand DOF. Targets fine manipulation in retail and manufacturing. 2025 commercial orders from Japan and North American auto component firms.

Apptronik (Austin, TX): Apollo (173 cm, 73 kg, 25 kg payload). Key feature: modular serviceability (target part replacement time <30 min). 2025: Mercedes-Benz MBDFC Berlin testing; Mercedes invested USD 403 million Series A; Jabil manufacturing partnership. 2027 commercial scale delivery target.

2.9 Global Supply Chain: Overseas Supplier Landscape

US: Exlar (planetary roller screws), ATI Industrial Automation (6-DOF force sensors), Harmonic Drive US, NVIDIA (edge AI), Qualcomm (Snapdragon robotics platform), Intrinsic (Google Alphabet robot software), Covariant (Amazon Robotics AI subsidiary).

Japan: Harmonic Drive (harmonic reducers), Nabtesco (RV reducers), Fanuc (servo motors + CNC), Yaskawa (servo motors), NSK/THK/NTN (precision bearings and lead screws).

Germany/Europe: Schaeffler (precision bearings), Bosch Rexroth (drive systems), Heidenhain (high-precision encoders), Beckhoff (EtherCAT real-time motion controllers).

Chapter 3 Policy, Macro and Capital Environment (PEST Analysis)

3.1 Policy Environment — China

China's MIIT issued the "Guidelines for Innovative Development of Humanoid Robots" in November 2023, targeting: 2025 — preliminary innovation system established, batch production in manufacturing and service scenarios, 2–3 globally influential ecosystem enterprises; 2027 — world-class technology capability; 2035 — world-leading comprehensive strength.

2025 policy highlights: "揭榜挂帅" (challenge programme) targeting whole machine, joint actuators, and embodied foundation models; preparation for national humanoid robot standardisation committee; January 2026 MIIT announcement of forthcoming "Humanoid Robot and Embodied Intelligence Comprehensive Standardisation System Construction Guide."

Local government actions: Beijing Yizhuang (CNY 1 billion fund, backing Galaxy Robotics, Robot Era); Shanghai Zhangjiang AI Island (embodied intelligence industrial belt); Shenzhen Nanshan (embodied intelligence support fund); Suzhou Industrial Park (land and tax incentives for component firms including Levo Harmonic).

3.2 International Policy

US: Continued AI chip export controls (NVIDIA H100/H800, Blackwell B100/B200 to China); DARPA and DOE fund robotics basic research. NIST advancing humanoid robot performance evaluation standards.

EU: AI Act (effective 2024) classifies industrial collaborative robots as "high-risk AI," requiring transparency, explainability, human oversight, and CE certification. Horizon Europe funds EU domestic robotics R&D.

3.3 Economic Environment

Manufacturing labour cost increases (Chinese manufacturing average wages +7–9%/year 2015–2025) provide the fundamental economic driver. With full-size industrial humanoid prices targeting CNY 200,000–300,000 by 2026–2027, 5-year TCO of CNY 350,000–600,000 compresses ROI to 2–3 years, entering the zone that triggers factory procurement decisions.

Primary market: China humanoid track CNY 20 billion fundraising in 2025 (record high). Unitree IPO valuation ~CNY 42 billion; Agibot valuation >CNY 15 billion; Fourier completed >CNY 1 billion Series C; Galaxy Robotics raised >CNY 700 million.

3.4 Social Environment

Structural labour shortage: China's working-age population (15–64) has declined since peaking in 2013, with an estimated 70 million fewer by 2035 vs. 2020. "Recruitment difficulty" in Pearl River Delta and Yangtze River Delta manufacturing is a structural norm, particularly for high-temperature, high-noise, hazardous workstations.

3.5 Technology Environment

NVIDIA Isaac GR00T N1 (launched March 2025): world's first open-source humanoid robot foundation model, multimodal input (language + images), dual-system architecture (System 2 slow reasoning + System 1 fast action), 780,000 synthetic trajectories generated in 11 hours improving performance by 40%. Jetson Thor (800 TOPS) enables on-device inference of 1–7B parameter embodied models. Genesis simulator (MIT, ~430,000× faster than MuJoCo) and NVIDIA Cosmos world model enable high-volume synthetic data generation.

Chapter 4 China Market Scale and Price Curve

4.1 2025 Market Scale

FY2025: China humanoid robot shipments ~14,400 units (multiples growth YoY), 84.7% global share, market ~CNY 1.55 billion. By end-use: industrial manufacturing ~55%, R&D ~25%, commercial service ~12%, warehouse logistics ~8%. Top players: Unitree ~5,500 units (32.4% global share #1), Agibot >5,000 cumulative units, UBTech >500 unit intent orders plus CNY 250M mega-order.

4.2 2026 Outlook

TrendForce: 2026 China shipments ~62,500 units, +94% YoY. Supply drivers: Unitree targeting 75,000 units annual capacity (Hangzhou new plant); Agibot targeting tens of thousands (A2 + X1 parallel); UBTech Walker S1 targeting 10,000+ capacity; Fourier GR-1 scaling to thousands; EngineAI PM01 at CNY 88,000 accelerating developer ecosystem.

Key 2026 verification milestones: MTBF breakthrough to 1,500 hours in batch-production models; ROI recovery period compressed to <2 years at price <CNY 250,000; at least one OEM achieving >1,000 units quarterly delivery; cross-workstation migration time shortened to <3 days.

4.3 2027–2030 Medium-Term Forecast

| Year | Global Shipments | China Shipments | China Avg Price (Industrial Full-Size) | China Whole-Machine Market |

|---|---|---|---|---|

| 2025 (Actual) | ~17,000 | ~14,400 | ~CNY 450,000 | ~CNY 1.55B |

| 2026E | ~70,000 | ~62,500 | ~CNY 280,000 | ~CNY 14B |

| 2027E | ~200,000 | ~160,000 | ~CNY 200,000 | ~CNY 32B |

| 2028E | ~500,000 | ~400,000 | ~CNY 140,000 | ~CNY 56B |

| 2030E | ~1.2M | ~1M | ~CNY 90,000 | ~CNY 90B |

Bull case (technology breakout ahead of schedule): 2027 global shipments 300,000–400,000 units. Bear case (technology/production delays): 2026 global shipments 20,000–30,000 units.

4.4 Price Curve and Cost Reduction Pathway

2024: CNY 800,000–1,200,000 (extreme early-adopter pricing). 2025: CNY 300,000–650,000 (-50% in two years). Drivers: harmonic reducer domestic price from CNY 2,400 to ~1,320 (-45%); frameless motor domestic rate +30%; structural CFRP costs -20%; scale learning curve effects. 2026–2027 target CNY 180,000–300,000. 2028–2030: industrial units <CNY 150,000; home units potentially <CNY 80,000. The single biggest cost lever: planetary roller screw domestic mass production (Bestec, Hengli Hydraulics advancing).

Chapter 5 Supply Chain Deep Dive

5.1 Joint Actuators: Core Cost Lever

Joint actuators represent 35%–50% of BOM cost. A full-size humanoid has 20–60 actuator DOF, each comprising drive motor, reduction mechanism, and position/torque sensor.

Harmonic reducer market: Levo Harmonic (688017) — FY2025 revenue CNY 571M (+47.31%), net profit CNY 124M (doubled); harmonic reducer sales 425,200 units (+72.48%); product price ~CNY 1,320/unit (55–60% below Harmonic Drive Japan); main supplier for Unitree (63% of demand), exclusive planetary reducer for Agibot Expedition A2 hip/waist, 50,000-unit Agibot order in 2025. Competitors: Harmonic Drive (Japan, global benchmark), Nidec (Japan), China: Zhongda Lide (002896).

RV reducer market: Leading: Nabtesco (Japan, ~60% industrial robot RV global share). Domestic: Dual Ring Transmission (002472), Zhongda Lide (002896).

Planetary roller screws: Bestec (300580) subsidiary Yuhua Precision has completed sample development; targeting batch supply 2026; partnership with Sanhua. Hengli Hydraulics (601100) and Qinchuan Machine Tool (000837) also advancing. Currently 85%+ import dependent — the most impactful single localisation event ahead.

5.2 Frameless Torque Motors and Servo Drives

Inovance (300124): ~27.6% domestic servo market share #1; launching one-piece joint module products (motor+driver+encoder+reducer integrated). Powtran (603160): servo motors, direct-drive torque motors, in multiple humanoid robot supply chains. Leisai (002979): motion controllers for multi-axis synchronous control. Sanhua (related to 003137): core Tesla Optimus thermal management actuator supplier — thermal management valves and flow control modules, leveraging auto thermal management depth to enter humanoid.

5.3 Sensors: 6-DOF Force, Tactile and Vision

6-DOF force sensors: ATI (US, ~40% global share), Kistler (Switzerland) lead high end. Domestic: Kunwei Technology (Shenzhen), Yuli Instruments (Harbin), Xinjingcheng (Shanghai), Keli Sensor (603662). Import dependency ~60%.

Tactile sensors: Lowest maturity in humanoid sensor system. Startups: Pacini Sensing, Touch Think (domestic); BeBop Sensors, SynTouch (overseas). Commercial density approaching 500–1,000 points/cm² on advanced prototypes.

Vision/depth perception: Orbbec (9069.HK) — domestic #1 structured-light depth camera, used in Unitree H1/H2 and Agibot heads. RoboSense (2498.HK) and Hesai (HSAI.US) solid-state LiDAR for outdoor mapping and global localisation.

5.4 Embodied Foundation Models and AI Computing

NVIDIA Isaac GR00T N1 (launched March 18, 2025): open-source, multimodal (language + images), dual-system architecture (large LLM + fast action network), trained with 780,000 synthetic trajectories (+40% performance vs. real data only). Jetson Thor (800 TOPS) enables on-device real-time inference. GR00T N1.5 and N2 followed in H2 2025 with improved open-world generalisation.

Figure Helix: Vision-language-action (VLA) architecture; zero-shot bimanual task execution demonstrated at BMW Spartanburg; <1% task failure rate over 10-hour shifts.

Agibot GO-1: Multi-task end-to-end learning; 50–200 demonstrations for new task generalisation; distributed multi-robot cooperative scheduling. First full-platform adaptation across Expedition A2 and Lingxi X1.

5.5 Batteries, Structural Parts and Other Components

Battery: 0.5–1 kWh, high-nickel NCM preferred; CATL (300750) and EVE Energy (300014) providing custom battery modules. Carbon fibre CFRP frames: Zhongfu Shenying (688295), Guangwei Composites (300699). Aluminium die-cast: Wencan (603348), Tuopu (601689). Precision bearings: SKF, FAG, NSK import-dependent (~80% for P4/P2 grade).

5.6 Humanoid vs. Industrial Robot Supply Chain Synergies and Competition

Synergies: joint drive motors, servo drivers, precision castings, safety sensors. Competition: humanoid robots will primarily replace workstations currently done by human workers, not highly automated mechanical arm workstations. The most impactful supply chain shift: harmonic reducer demand growing in both industrial robot AND humanoid markets simultaneously. Six-axis force sensors represent a near-zero base incremental humanoid market — no established industrial robot market to compete with.

Chapter 6 Key Company Deep Analysis

6.1 Unitree Robotics

Headquartered Hangzhou; CEO Wang Xingxing 23.82% stake; Tencent and Alibaba strategic investors. FY2025: revenue CNY 1.699B, adj. net profit CNY 590M; ~5,500 humanoid units shipped, 32.4% global market share #1. Cumulative H1 series production >11,000 units by May 2026.

Products: H1 (~180 cm, ~47 kg, ~CNY 650,000, 19 DOF, 3.3 m/s max speed, exported to 30+ countries); H2 (upgraded torque density, ~4-hour battery, 20+ DOF hands); G1 (127 cm, 35 kg, CNY 99,000 — breaks global price floor, 300+ universities worldwide); Go2 and B2 (quadruped lines). IPO: Science-tech board filed March 2026 (raised CNY 4.2B), approved June 1, 2026 — 73 days from filing to approval, fastest on record.

6.2 UBTech Robotics (HK 9880)

Founded 2012, listed HKEX (9880). FY2025 revenue ~HKD 1.62B; industrial humanoid >40% revenue. CNY 250M global largest single humanoid order in September 2025. Walker S1 (41 DOF, 11-DOF hands, >80% domestic component rate, -25% cost vs. predecessor) deployed at BYD (2× efficiency improvement), Zeekr (world's first multi-machine multi-scenario multi-task collaborative deployment), Geely (smart warehouse), Nio (quality inspection). Intent orders >500 units.

6.3 Agibot (Zhiyuan Innovation)

Founder "Peng Zhihui" (former Huawei genius youth programme). Founded February 2023, Shanghai. Cumulative production >5,000 units by end 2025 across three lines (Expedition A1/A2: 1,742; Lingxi X1/X2: 1,846; Sprite G1/G2: 1,412). Investors: Goldman Sachs, JD.com, Shanghai Embodied Intelligence Fund; valuation >CNY 15B. Products: Expedition A2 (full bipedal, industrial, GO-1 model); Expedition A2-W (wheeled); Lingxi X1/X2 (lightweight bipedal); Sprite series (mobile dual-arm table). GO-1 model achieved multi-task autonomous switching in automotive factory customers.

6.4 Galaxy Robotics (Galbot)

Founded by Prof. Wang He (Tsinghua), LLM-robotics integration focus. Galbot G1: wheeled mobile + dual humanoid arms. 2025: raised >CNY 700M; warehouse partnerships with SF Express and Cainiao. Differentiation: open-world natural language task decomposition.

6.5 Fourier Intelligence

Founded 2015, Shanghai. GR-1: 165 cm, 65 kg, 40 DOF, ~CNY 700,000. Dual strategy: rehab exoskeleton (mature cash flow) + general humanoid (high growth). 2025: completed >CNY 1B Series C; deliveries to auto Tier 1 suppliers and vocational training institutions. GR-1 was first Chinese humanoid demonstrated at major international tech events (Tokyo 2023).

6.6–6.10 Additional Players

EngineAI Robotics (众擎): PM01 at CNY 88,000 — lowest commercial full-size price globally; DJI-alumni team; Shenzhen-based.

LimX Dynamics (逐际动力): Extreme motion robustness (CL-1); Tsinghua control background; outdoor complex terrain leader in China.

CloudMinds (达闼): Cloud-centric model; HARIX service robots deployed in hotels, malls, museums.

Robot Era (星动纪元): Tsinghua AI embodied lab spin-off; XBot-L first deliveries to universities and auto Tier 1.

Leco (乐聚机器人): Shandong University spin-off; Kuavo series targeting factory deployment.

Tsinghua ecosystem cluster (星动纪元, 穹彻智能, 逐际动力): High research density; model-first or motion-first specialisation; backed by Beijing Yizhuang fund. Collectively represent China's highest academic output in embodied AI.

Key upstream suppliers extended: Qinchuan Machine Tool (000837, magnetic gear, precision grinding, advancing roller screws); Dual Ring Transmission (002472, RV reducers for humanoid); Leisai (002979, multi-axis motion controllers); Zhongda Lide (002896, harmonic and RV reducers); Sanhua thermal management systems.

Chapter 7 Industrial Belt Map and Manufacturing Clusters

7.1 Shenzhen Nanshan/Longhua — Embodied Intelligence Hardware Hub

Unitree Shenzhen R&D, EngineAI (HQ), Orbbec, RoboSense, Inovance manufacturing. Complete consumer electronics + industrial automation supply chain ecosystem. Sanhua, BYD Electronics, Luxshare, Tripod Technology manufacturing ecosystem enables rapid humanoid structural component iteration.

7.2 Beijing Haidian/Yizhuang — Policy and Science Dual Engine

CNY 1B Yizhuang humanoid fund. Galaxy Robotics (Tsinghua), Robot Era (Tsinghua), Qiongtian Intelligence backed. R&D density highest in China; embodied AI model research centre.

7.3 Shanghai Zhangjiang/Minhang — Industry-Academia Manufacturing Core

Agibot (Zhangjiang HQ, ~600 staff), Fourier Intelligence (Songjiang), Unitree Shanghai R&D, CloudMinds. Shanghai AILAB and Shanghai Embodied Intelligence Fund. Mature manufacturing service ecosystem (precision casting, mechatronics integration, precision testing).

7.4 Suzhou Industrial Park — Component Manufacturing Core Base

Levo Harmonic (688017, Xiangcheng) — >500,000 units/year capacity target; Inovance (SIP manufacturing base); Powtran (603160, SIP); large precision machining ecosystem. Suzhou is the city with highest human robot joint actuator component value in China.

7.5 Guangdong Dongguan/Foshan — Densest Industrial Application Zone

3C electronics (Huawei, OPPO, vivo supply chains) and automotive components. Dense demand market for humanoid robot industrial applications. One-piece die-cast capabilities (Tuopu, Wencan) and electronics manufacturing ecosystem for rapid structural and control system iteration.

In Tianxia Gongchang's platform, hundreds of suppliers from these industrial belts have been certified, covering harmonic reducers, servo motors, precision bearings, carbon fibre structural members and sensors, providing standardised sourcing channels for humanoid OEM domestic procurement.

7.6 Overseas Manufacturing Clusters

California (Silicon Valley/Bay Area): Figure AI (San Jose), 1X R&D, NVIDIA (Santa Clara), Google DeepMind (Mountain View), highest VC density globally.

Texas (Austin): Tesla Gigafactory Texas (dedicated Optimus line, far-term million units/year target), Apptronik HQ.

Norway (Oslo): 1X Technologies R&D and embodied learning data accumulation centre.

Germany (Leipzig/Berlin/Stuttgart): BMW Leipzig (Figure, Europe's first production deployment), Mercedes-Benz MBDFC Berlin (Apptronik), Volkswagen evaluating wire harness/welding applications. KUKA and Bosch Rexroth integrating humanoid capabilities.

Chapter 8 Vertical Segment Deep Studies

8.1 Industrial Manufacturing Humanoid Robots

Factory fixed workstation is the core battlefield for 2025–2028. Automotive factories — standardised processes, sufficient OEM margins for POC costs, strategic driver for digitalisation. 2025 quantifiable milestones: Figure 02 at BMW Spartanburg 1,250 hours / 30,000+ BMW X3 / 90,000+ components; UBTech Walker S1 at Zeekr (world's first multi-machine multi-scenario multi-task); Tesla Optimus at Fremont (internal, ~5,000 equivalent units); Apptronik Apollo at Mercedes-Benz Berlin (commercial pilot).

3C electronics manufacturing: next largest potential market after automotive. Core requirements: dexterous hand precision and visual accuracy. First-tier EMS (Foxconn, Luxshare) and brand OEMs (Huawei Terminal, Xiaomi) starting systematic workstation assessments. First batch purchase orders expected 2026–2027.

Key 5 workstation types by economic value: (1) material delivery (most mature, highest ROI ~1–3yr); (2) machine loading/unloading (second most common); (3) quality inspection (high value but requires 15+ DOF hands + high generalisation); (4) precision assembly (highest value, highest difficulty, 2027–2028 limited deployments); (5) end packaging and boxing (medium difficulty, 2026–2027 batch viable).

8.2 Warehouse Logistics Humanoid Robots

Agility Digit / GXO: 100,000+ totes benchmark. RaaS (Robot-as-a-Service) model: pay-per-move, converts CapEx to OpEx. Domestic: Agibot A2-W at JD.com warehouses; Galaxy Robotics Galbot G1 POC with SF Express and Cainiao. Wheeled humanoids have 3–5× energy efficiency advantage over full-bipedal for flat-floor warehouses.

Key SKU diversity challenge: Amazon's 400M+ SKUs require open-world object generalisation — unsolved until 2027–2028 for full-scale pick-and-pack. Near-term deployments favour standardised-bin tasks (Digit model).

8.3 Commercial Service and Other Scenarios

Commercial service: humanoid form premium highest (Hilton Hotels, malls, airports, museums). CloudMinds HARIX and UBTech Walker service variants in steady commercial deployment. Market scale limited vs. industrial in 2025–2027. Home service: 2030+ earliest scale market — requires open-home-environment generalisation + sub-CNY 50,000 price.

8.4 Dexterous Hands: Core Fine Manipulation Module

Figure 02/03: 16 DOF/hand, ~500g, linkage+micro-motor design. UBTech Walker S1: 11 DOF. Unitree H2: 20+ DOF. Domestic dexterous hand startups: Lingxin Qiaoshou (Chengdu, flexible tendon), Yinshi Robotics (Beijing, pneumatic+tendon), Songyan Power (Shanghai, micro-actuator integration). 2026–2027 target: 24–28 DOF, tactile >1,000 points/cm², single hand <400g.

8.5 Dual-Arm Collaboration and Foundation Model Intersection

Fixed/mobile-base dual-arm systems: lower cost vs. full-size humanoid, faster deployment for fine manipulation workstations. Agibot Sprite series, AUBO dual-arm. With embodied AI, these are qualitatively different from traditional teach-and-play dual-arm cobots — language-driven task flexibility.

Chapter 9 Technology Evolution Pathway

9.1 Embodied Foundation Models: From "Action Cloning" to "Generalised Reasoning"

Three-level roadmap: (1) Behavioural cloning — replicates taught tasks, proven in fixed workstations (Figure 02 at BMW); (2) Weak generalisation — transfers to similar tasks and similar environments; (3) Strong open-world generalisation — fully novel tasks from language description, target ~2027–2028.

Three key research streams: VLA (Vision-Language-Action) models — NVIDIA GR00T N1, Figure Helix; Diffusion Policy — action generation as denoising, excels at bimodal action distributions; World model + RL — train physical intuition in virtual worlds (NVIDIA Cosmos, DeepMind Genie 2).

Data quality over data quantity: NVIDIA 780,000 synthetic trajectories in 11 hours = 6,500 hours real demo equivalent, +40% performance. Genesis simulator (MIT, 430,000× faster than MuJoCo) democratises large-scale RL training.

9.2 E2E vs. Modular Control

Tesla Optimus: aggressive E2E (direct pixel-to-joint, FSD-style). Modular (UBTech, Fourier): layered sensing-planning-execution. Hybrid (industry mainstream): LLM/VLM for task planning + trajectory optimisation + classical joint control. Hybrid provides engineering reliability + intelligence; limits maximum generalisation capacity.

9.3 Joint Actuator Technology Evolution

Rotary joint paradigm (Unitree H1/H2, UBTech Walker S1): frameless torque motor + harmonic reducer. Mature supply chain (Levo Harmonic domestic), space-efficient. Linear drive paradigm (Tesla Optimus Gen 2, Figure 02/03): frameless motor + planetary roller screw. Simpler leg structure, higher efficiency, but supply chain (planetary roller screws) more challenging. No absolute advantage between paradigms — tradeoff of supply chain maturity vs. control architecture preference.

9.4 Bionic Leg Structure and Gait Control

WBC (Whole-Body Control): 500–1,000 Hz real-time QP optimisation, simultaneous satisfaction of floating base constraints, contact constraints and task objectives. Unitree H1 uses WBC + RL locomotion: complex terrain (stones, ramps) outdoor walking >10 km without falling (Shenzhen Nanshan field tests).

RL locomotion policy: ANYmal (ETH) and subsequent work demonstrated robustness exceeding hand-crafted controllers; Unitree H1's "wild" walking uses RL-trained policy.

9.5 Chinese Embodied AI Research Progress

Shanghai AI Lab's RoboTwin: 500,000 synthetic + 50,000 real teleoperation trajectories open dataset. BAAI Emu3-Body: VLA-architecture foundation model. Tsinghua groups: multi-modal manipulation, low-shot transfer. Gap vs. global frontier (CLIPort/RLBench benchmarks): 8–15 percentage points in 2025, down from 20–30 points in 2023.

9.6 Training Data Collection and Teleoperation

Teleoperation: 30–60 effective trajectories/hour (skilled operator), main data bottleneck. Synthetic generation (Isaac Sim + Cosmos): 1,000–100,000× faster but Sim-to-Real gap exists. Human video: extracting "hand-object interaction" knowledge from YouTube/factory videos (pretraining direction). Key domestic teleoperation platforms: BIGAI whole-body teleoperation kit, Tsinghua RoboFleet dual-hand exoskeleton.

9.7 AI Safety and Explainability

Safety filters on action outputs; constrained RL for safety-embedded training; interpretability for fast fault diagnosis in industrial settings (avoiding pure E2E for production). OTA updates: phased grey release (5% → 100%), integrity verification, mid-update interruption protection. FSD OTA engineering experience directly transferable to Optimus.

9.8 Energy Efficiency and Sustainability

Full-size humanoid at normal operation: 800–1,500 W vs. human metabolic power ~200–400 W at similar workload (2–5× less efficient due to electromechanical vs. biochemical). With passive dynamics and gait optimisation: projected 30–50% efficiency improvement by 2028–2030. "Dark factory" benefit: robots work without lights/air conditioning, partially offsetting energy premium. Lifecycle carbon footprint: ~30 MT CO₂e per unit per 5-year cycle (dominated by electricity consumption).

Chapter 10 Key Risks

10.0 Risk Landscape Overview

Risk matrix: High probability + high impact (core risks): embodied AI generalisation bottleneck delayed (60% probability, -40–60% market vs. expectations if delayed 2+ years); mass-production MTBF below target (50%); planetary roller screw localisation delay before 2027 (40%). Medium probability + high impact: Tesla Optimus major delay; expanded US export controls; factory safety incident causing OEM procurement pause. Tail risks: AGI breakthrough accelerating timelines (upside); humanoid robots sanctioned like Huawei 5G (downside); major public safety accident triggering industry-wide regulatory tightening (downside).

Core conclusion: The greatest systemic risk is not "can it be done" but "how much slower than expected." The key uncertainty is the timing of breakthroughs, not whether they happen.

10.1 Embodied AI Generalisation Bottleneck

Out-of-distribution generalisation: performance degrades on unseen object shapes/lighting/occlusion variations. Each new workstation still requires 100–500 demonstrations, limiting humanoid economics to high-value, high-repetition fixed workstations. If unresolved by 2027: potential market at 30%–50% of optimistic predictions.

10.2 Mass-Production Yield and Manufacturing Consistency

High-DOF assembly precision consistency; software-hardware co-calibration (currently 4–8 hours/unit, labour-intensive bottleneck); MTBF target 5,000 hours vs. current 500–2,000 hours typical; Figure 02's wrist cable failure (highest failure mode at BMW) driving Figure 03 redesign.

10.3 Cost Reduction Pace and Supply Chain Risk

Planetary roller screw localisation delay risk; import dependency on precision encoders (70%), P4/P2 bearings (80%), precision IMUs (~60%); currency risk on USD-denominated imports.

10.4 Safety Liability and Legal Framework Gaps

Robot-caused injury responsibility allocation (OEM vs. AI developer vs. system integrator vs. operator) has no global legal framework. Factory data security: production process data, product design features and production cycle information captured by robots — industrial IP protection requires governance frameworks.

10.5 Geopolitics and Tech Competition

NVIDIA Blackwell export controls increase China humanoid AI training infrastructure costs. IPO risk: Unitree's ~71× PE valuation could face secondary market pressure if growth slows, creating reverse pressure on primary market comps.

10.6 Application Timeline Misjudgment

Home service (2030 earliest, 2032–2035 most realistic scale market); SME factory penetration limited until generalisation breakthrough; family service safety certification and consumer acceptance building require 5–10 years.

Chapter 11 2026–2030 Trend Forecast

11.1 Shipment Curve and Market Scale Base Case

See table in Chapter 4.3. Bull case: 2027 global 300,000–400,000 units if AI generalisation breakthrough by 2026–2027; China 2028 whole-machine market >CNY 100B. Bear case: 2026 global 20,000–30,000 units if major production/technology delays.

11.2 CR5 Concentration Evolution

2025 global CR5 ~75% (Unitree ~32%, Tesla internal ~15%, Agibot ~12%, UBTech ~10%, Figure ~6%). 2027 expected: Unitree ~20%, Tesla ~18%, Agibot ~12%, UBTech ~8%, Figure ~7%; total ~65%. China share: from 84.7% in 2025 declining to ~65–75% by 2030 as Tesla Optimus scales, but China's absolute volumes continue rapid growth.

11.3 Model Iteration Roadmap

Unitree: H3 (2027, 22+ DOF hands, MTBF >3,000 hr, <45 kg); G1 price to ~CNY 60,000–70,000. UBTech: Walker S2 (5× faster workstation migration, 5-hr battery). Agibot: Expedition A3 (2027, <20 demo new workstation adaptation, 4-hr migration). Tesla: Optimus Gen 3 (2027, FSD V14-equivalent robot E2E system). Figure AI: Figure 04 targeting second vertical (warehouse or healthcare).

11.4 Application Scenario Penetration Pace

Tier 1 (factory fixed workstations, 2025–2028): main battlefield. By end 2027: estimated China auto + 3C factory cumulative humanoid deployment >100,000 unit-instances. Tier 2 (warehouse logistics, 2026–2029): rapid growth; domestic RaaS pilots expected H2 2026. Tier 3 (commercial service, 2027–2030): steady penetration in premium hotels/airports/malls. Tier 4 (home service, 2030+): 2030 before market; 2032–2035 realistic scale.

11.5 Supply Chain Critical Path

Node 1 (2026–2027): Planetary roller screw domestic mass production (Bestec/Hengli >5,000 units/month stable supply → -30–50% linear actuator cost). Node 2 (2026–2027): 6-DOF force sensor domestic breakthrough (Kunwei/Yuli → -60% sensor BOM). Node 3 (2027–2028): Dedicated frameless motor magnetic encoder domestic rate up. Node 4 (2027–2028): Dexterous hand tactile sensor mass production.

11.6 Investor Framework

Tier 1 (highest certainty): joint actuator suppliers — Levo Harmonic (688017), Bestec (300580). Confirmed humanoid volume correlation with domestic substitution share gain. Tier 2 (high elasticity): frameless motors (Inovance, Powtran, Leisai), 6-DOF force sensors (Kunwei awaiting IPO), vision (Orbbec). Tier 3 (longest monetisation path): OEM equity (Unitree, Agibot), warehouse/factory system integrators. Risk: early-stage OEMs without production records (high cash burn, unproven yield); ultra-high-multiple valuations pricing in optimistic AI generalisation scenarios.

Key monitoring indicators: Levo Harmonic quarterly reducer shipments; Unitree/Agibot/UBTech quarterly unit disclosures; Tesla Optimus annual production guidance; embodied AI generalisation benchmark scores; major OEM humanoid procurement budget announcements.

11.7 Humanoid Robots and Frontier Technology Intersections

AGI: humanoid robots as the physical substrate for "physical world AGI." If AGI breakthrough arrives before 2030, humanoid will be its most important physical manifestation. Digital twin: NVIDIA Omniverse + Isaac GR00T integration enables large-scale pre-deployment simulation of new workstations, reducing real-world demonstration requirements. Advanced manufacturing (AM): factory redesign will progressively optimise for "human-robot coexistence" (wider corridors, standardised rack sizes, unified workpiece interfaces), further lowering humanoid deployment barriers in a positive feedback loop.

Chapter 12 Conclusions and Outlook

2026 marks an exact, quantifiable inflection point in the humanoid robot industry. Global shipments of 17,000 units already exceed the comparable market scale of industrial robots in the early 2000s; Unitree H1 pricing dropped from CNY 1.2M to CNY 650,000 in two years; Figure 02 operated 1,250 hours in BMW production — not a demo but production records for a mass-production vehicle. Agility Digit moved 100,000 tote bins at GXO — the first independently verifiable commercial-scale operation count in humanoid robot history.

The deep logic of this mass-production wave is the historic intersection of manufacturing cost curves and humanoid robot price curves. When a full-size industrial humanoid's 5-year total cost of ownership falls below the 5-year comprehensive employment cost of a human worker (Chinese manufacturing ~CNY 600,000–900,000), economics triggers the critical threshold for replacement demand. Current China mainstream industrial models target CNY 200,000–300,000 (2026–2027), with 5-year TCO ~350,000–600,000, meaning ROI recovery of ~2–3 years — entering the range that influences factory financial decision-makers.

Three forces determine this competition's direction over the next five years:

The first force — embodied foundation model generalisation capability determines market boundaries. Whether robots can tomorrow complete electronic connector precision insertion without prior teaching, and the day after manage household cooking in unfamiliar kitchens, ultimately depends on whether embodied models break the out-of-distribution generalisation barrier. NVIDIA GR00T, Figure Helix, Tesla's E2E pathway, and Agibot GO-1 all assault the same technical ceiling. 2027–2028 may be the critical window where this barrier develops real cracks, triggering non-linear expansion in coverable workstations and market scale.

The second force — China's supply chain localisation speed determines the cost curve slope. Levo Harmonic's FY2025 net profit doubling, Bestec's planetary roller screw mass production approaching, Inovance's servo market share steady at domestic #1 — Chinese component manufacturers are iterating at a 2–3 year per generation pace catching up to international standards. When harmonic reducers, planetary roller screws, frameless torque motors, and six-axis force sensors all achieve scale domestic production (projected 2027–2028), the pace of whole-machine cost decline will exceed most institutional forecasts.

The third force — Tesla Optimus's actual mass-production pace is the global structural variable. Converting Fremont capacity from Model S/X to Optimus is the largest single production line transformation from "car manufacturing" to "robot manufacturing" in automotive industry history. If Optimus reaches 50,000 units in 2026 and begins external customer deliveries, it will simultaneously reshape: global market structure (US players retake production share), global supply chain structure (more Chinese component manufacturers enter Tesla supply chain), and overall industry confidence threshold (Tesla production endorsement's market education effect).

Tianxia Gongchang covers 4.8 million active factories, of which automotive manufacturing, 3C electronics, and precision machinery together account for over 1.8 million — the most important potential procurement cluster for humanoid robots over the next 5–10 years. From the factory procurement decision perspective, supplier screening efficiency directly affects the conversion cycle from POC to batch orders, and this is precisely the core value of a B2B platform built on active factory data.

Mass-production year has arrived. The technical inflection point, supply chain maturity, and capital concentration direction already point to the same coordinate in 2025–2026. The competition of 2026–2030 is a competition of speed (who reaches 100,000 units/year scale fastest), precision (who makes robots "run without teaching" in new workstations fastest), and cost (who drives whole-machine price below CNY 100,000 fastest). These three competitions unfold simultaneously, collectively composing the most compelling industrial evolution narrative in the post-mass-production year of humanoid robots.

Data Sources

Company Official Documents

- Unitree Robotics Science-tech Board IPO Prospectus (March 2026, Shanghai Stock Exchange filing 002178; proposed raise CNY 4.2 billion)

- UBTech Robotics FY2025 Annual Report (HKEX 9880; revenue ~HKD 1.62 billion)

- Levo Harmonic Transmission Science 2025 Semi-Annual Report / FY2025 Annual Report (688017; revenue CNY 571M +47.31%, net profit doubled)

- Tesla FY2025 Q4 Earnings and 2025 Investor Day Materials (Fremont + Texas Optimus production plans)

- Figure AI official blog and BMW Spartanburg deployment announcement (figure.ai/news/production-at-bmw)

- BMW Group press releases (press.bmwgroup.com): Figure 02 supporting 30,000+ BMW X3 at Spartanburg; Leipzig plant first European humanoid production deployment

- Mercedes-Benz Group official news (group.mercedes-benz.com): Apptronik Apollo Berlin MBDFC deployment; Mercedes USD 403M Series A investment

- NVIDIA official press releases and technical papers: Isaac GR00T N1 launch (nvidianews.nvidia.com); GR00T N1 open foundation model paper; 780,000 synthetic trajectory efficiency and 40% performance improvement data

- Agility Robotics official announcement: Digit moved 100,000+ totes at GXO (agilityrobotics.com/content/digit-moves-over-100k-totes)

Industry Research Reports

- TrendForce humanoid robot market quarterly tracking (Q4 2025/Q1 2026): 2026 China ~62,500 units, +94%

- IDC "2026 Humanoid Robot Commercial Deployment Research Report"

- CAEI "Humanoid Robot Ecosystem Report 2025": 14,400 units, mass-production year judgment, 2030 market ~CNY 870 billion

- Huaan Securities "From Sci-Fi to Reality: Humanoid Robot Industry 2025 Annual Strategy"

- Goldman Sachs "Global Humanoid Robot Market Outlook 2025"

- MIIT "Guidelines for Innovative Development of Humanoid Robots" (November 2023)

- MIIT January 2026 policy notice: "Humanoid Robot and Embodied Intelligence Comprehensive Standardisation System Construction Guide" (forthcoming)

Media and Information Sources

- 36Kr "After Mass-Production Year: China Humanoid Robots Move to 'Value War'" (2026)

- Huxiu "Unitree Science-tech Board IPO to Be Reviewed June 1"

- Sina Finance: Agibot reaching 5,000 units milestone (December 2025)

- IEEE Spectrum, The Robot Report: ongoing coverage of Agility Digit, Figure 02 BMW project, Apptronik Apollo

- MIT Technology Review: NVIDIA GR00T N1 world's first open-source humanoid robot foundation model

- Fortune: Figure AI and BMW collaboration details (April 2025)

Supply Chain Data

- Tianxia Gongchang platform humanoid robot supplier database (covering harmonic reducers, servo motors, sensors, precision bearings, LiDAR, robots supplier categories)

- East Money, Tonghuashun financial platforms: FY2025 data and research reports for Levo Harmonic (688017), Bestec (300580), Inovance (300124), Powtran (603160), Dual Ring Transmission (002472), Zhongda Lide (002896), Leisai (002979)

Data cut-off: June 4, 2026. All market forecasts in this report are research interval estimates and do not constitute investment advice.