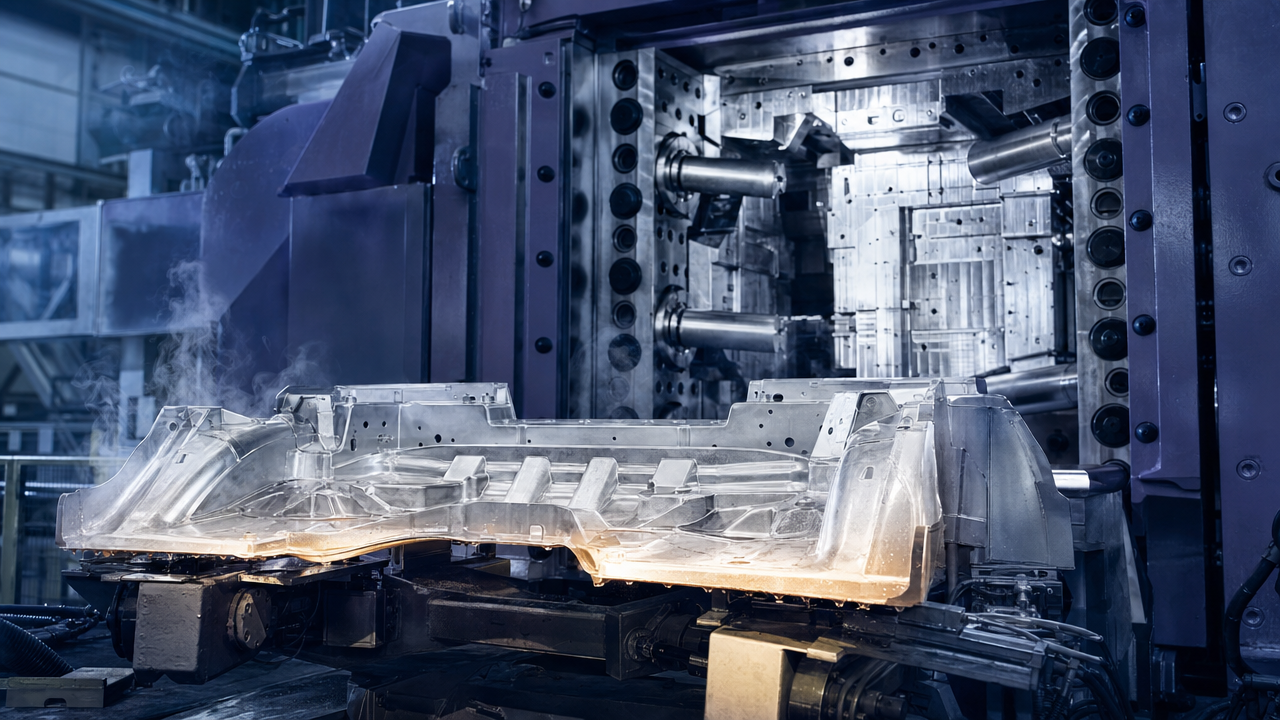

In May 2026, on a pier at Shenzhen's Dapeng Bay, a 700-ton gray die-casting machine was loaded onto a container ship bound for a newly built plant in Monterrey, Mexico. The machine was a 9,000-ton mega die-caster made by LK Group, ordered so that a Chinese automaker could press whole rear underbodies on its North American line. The same week, inside a factory in Shanghai Yizhuang, a domestically built 12,000-ton press was closing its mold. The instant the metal valve snapped shut, more than 700 kilograms of liquid aluminum alloy shot into the cavity at several meters per second. Tens of seconds later, a single casting emerged that would otherwise have required seventy or eighty stamped parts welded together.

Those two scenes lay out the full tension inside China's integrated die-casting industry. It is the most aggressive branch of the new-energy-vehicle process revolution of the past three years: collapsing dozens of stamping and welding steps into a single mold-close, and replacing more than a hundred parts with one casting. It is also the most contested stretch of the supply chain. A single mold costs eighty million yuan and up; a press costs a hundred million; once a vehicle is in a collision, an entire underbody panel must be replaced; insurers have begun refusing coverage; traditional OEMs hold reservations. Between those two forces lies a once-in-history window for Chinese press makers to occupy the global high end in reverse.

This report is a full picture of China's integrated die-casting industry from 2025 to 2030. From upstream heat-treatment-free alloy, molds, and mega presses, through downstream body-structure Tier1s, to the OEM application map, from localization milestones to economic arguments, from policy to risk factors, and finally back to one underlying question: now that China has taken first place in mega die-casting equipment, absorbed Italy's IDRA, and reverse-exported the Giga Press concept, where will the next bottleneck appear, and from where will the next breakthrough come?

Chapter 1 Industry Overview: A Few Key Numbers from 2025

Integrated die-casting forms a large body-structure part — front cabin, rear underbody, battery tray, A-pillar — through a single mold-close and a single shot. It was not invented so much as pushed onto the industrial stage by the cost pressure of new-energy vehicles, the lightweighting agenda, and the Giga Press concept Tesla floated in 2019.

For 2025, several numbers sketch the whole shape of China's industry.

Market size. By the books of Tianfeng Securities and Huatai Securities, the Chinese integrated-die-casting structural-parts market crossed thirty billion yuan in 2025, with year-over-year growth close to fifty percent. Counting mid-sized castings as well, the overall 2025 Chinese automotive-die-casting market was around 26.4 billion yuan by the figures from Zhiyan Consulting. Definitions cross over, but the core range of three hundred to five hundred hundred million yuan has become consensus. The global market for large die-casting equipment was 750 million USD in 2024, 800 million in 2025, and is forecast to reach 1.54 billion USD by 2034 — a compound rate of seventy-five percent.

Installed base. As of May 2026, more than sixty domestically delivered presses of 6,000 tons or above are running in China, of which close to twenty are 9,000 tons or above, five are 12,000 tons, and two are 16,000 tons — one at XPeng for the P7+, one at Guangdong Hongtu's Guangzhou plant. The headline number looks small, but five years ago it was effectively zero, and globally, China now accounts for more than eighty percent of the installed base above six thousand tons.

Penetration. China produced about twelve million new-energy passenger vehicles in 2025. By models that already carry at least one integrated die-cast structural part, penetration is around fifteen percent. By the strict definition — both front and rear cabins die-cast in one shot — penetration is just over three percent, concentrated on XPeng G6/G9/P7+, Xiaomi SU7/YU7, and Tesla Model Y/Cybertruck.

Application mix. Rear underbody is the part that industrialized first, accounting for around sixty percent of integrated die-cast structural-part revenue. Front cabin holds about twenty percent. Battery tray contributes fifteen. A-pillar and door anti-collision beams make up the rest. Rear underbody industrialized first because the geometry suits single-direction demolding, mold complexity is lower, and the welded-part count it replaced (seventy to over a hundred parts) is the most visible saving.

Supply-chain structure. Upstream is heat-treatment-free alloy (Lizhong Group, Bay Alloys, Xiaomi-developed grades, plus Hydro and Constellium abroad), plus large molds (Saiweida, Guangdong Hongtu in-house) and mega presses (LK, Yizumi, IDRA). Mid-stream is Tier1 die-casters (Wencan, Guangdong Hongtu, Aikedi, Xusheng Group, Tuopu Group). Downstream is NEV OEMs (Tesla, Xiaomi, XPeng, NIO, Zeekr, Li Auto, AITO). The thinnest and most profitable link is the mega press; the heaviest by revenue is the Tier1; the fastest to monetize is alloy-patent and line know-how.

Global landscape. The top five global press makers hold about fifty-seven percent share combined. LK Group, after absorbing Italy's IDRA under LK Group, holds over thirty percent on its own and is the unambiguous global leader. Bühler, Frech, UBE, and Toshiba each hold ten percent or less. Chinese newcomers — Yizumi, Guangzhou Borchuang, Haitian Precision — combined hold around ten percent. Narrow the lens to presses above eight thousand tons, and LK alone holds seventy percent of global shipments. The remainder is split between IDRA (same parent) and UBE. The European veterans have effectively exited that size class.

Behind those numbers lies a faintly counter-intuitive fact: the mega press is one of the very few Chinese high-end equipment categories that capital markets have not yet priced in but that has already completed reverse pricing globally. It belongs in the same drawer as PCB equipment, semiconductor cleaning tools, and laser welders — categories that don't look conspicuous but, when you tally global shipments behind closed doors, lead the world.

Leading firms. On equipment, LK Group booked roughly 2.6 billion HKD of revenue in fiscal 2024-2025, of which the press business was about 1.6 billion HKD. On Tier1 castings, the 2025 top three by revenue are Guangdong Hongtu (9.2 billion yuan), Wencan (2.8 billion yuan half-year, well over five billion full-year), and Aikedi (5.3 billion yuan in the first three quarters). Splitting "press makers" from "casters" matters: their moats, gross margins, and customer structures differ entirely. Equipment makers eat patents and first-of-kind orders at twenty to twenty-five percent gross. Casters eat volume and program awards at twelve to eighteen percent, with scale doing the heavy lifting.

Headline vehicles. As of May 2026, almost every series-production vehicle in the world that uses a single-piece integrated rear underbody (non-skeleton) belongs to either the Chinese camp or to Tesla. BBA in Germany, Toyota, Nissan, and Honda in Japan, and Hyundai-Kia in Korea still rely on conventional stamping plus laser welding. A few of their models have adopted localized castings, but nowhere near the "seventy-parts-in-one" stage. This leaves the Chinese Tier1s and equipment houses a critical window across the next global cycle, 2026-2030.

Tonnage-class capacity. A 6,000-ton press cycles at 90-120 seconds per shot, delivering 250,000-300,000 shots per year. A 9,000-ton press cycles at 120-150 seconds, 180,000-220,000 shots. A 12,000-ton press at 180 seconds, around 140,000 shots. A 16,000-ton press at 220+ seconds, around 100,000 shots. That means an identical "mega press investment" can yield a threefold difference in throughput between tonnage classes — and explains why head OEMs concentrate on 9,000-ton class machines rather than 16,000.

Aluminum content per vehicle. Aluminum content in NEV passenger cars rose from 80 kilograms per vehicle a decade ago to about 180 today, and is expected to cross 250 by 2030. Integrated die-cast parts account for roughly half: rear underbody 40-60 kg, front cabin 30-40 kg, battery tray 60-80 kg. The numbers look modest until you multiply by volume — at fourteen million NEV units in 2026 and twenty percent integrated-die-casting penetration, annual heat-treatment-free alloy consumption hits six hundred thousand tons, enough to reshape the country's downstream aluminum-alloy product mix.

Chapter 2 Upstream One: Heat-Treatment-Free Alloy and the War Before the Battle

The most overlooked link in the integrated-die-casting chain is the alloy. To non-specialists, aluminum is aluminum, and one ingot looks much like another. To anyone who has run a real production line, alloy is the determining variable between a passable casting and a scrap. The fastest way to grasp why is to look at the trouble traditional aluminum alloys cause when you push them into mega castings.

Conventional A380, A356, and similar grades suffer pronounced internal stress and shrinkage warpage after a large casting comes out of the mold. The classic fix is to push the part through a T6 or T7 furnace — five to twelve hours of heating, quenching, and tempering — to relieve stress and bring mechanical properties up to spec. For a 1.7-meter-by-1.5-meter rear underbody, the heat treatment costs you geometric stability: the casting bows, dimensions drift, and the rework rate stays high.

Heat-treatment-free alloy, the so-called HFA grade, is engineered to skip that furnace entirely. The casting is usable straight from the press. Strength is met as-cast; elongation is in the 8-12% band; yield strength reaches 120-180 MPa; tensile strength 240-300 MPa. The dimensional advantage is decisive — no oven, no warpage. Domestic representative grades are Lizhong LDH series, Bay Alloys M01, Lizard B70, Xiaomi-developed Titans 72; foreign references include Hydro's HyForge and Constellium's Aural-5.

The patent moat is the real heart of the upstream. Tesla licenses its own internally developed heat-treatment-free alloy under controlled supply. Lizhong holds the broadest grade portfolio in China, with formulations specifically tuned for 9,000- and 12,000-ton mega presses. Xiaomi's self-developed Titans 72 grade, used on the SU7 nine-thousand-ton rear underbody, raises a question about car-OEM verticalization into materials. The cost to bypass the patents is high — and at the same time, the alloy itself is a commodity with single-digit gross margin if the patent is stripped out.

Cost structure. A kilogram of A380 ingot trades at 18-22 yuan; heat-treatment-free alloy sells at 28-35 yuan. The ten-yuan premium covers the alloying additions (titanium, strontium, manganese, vanadium), the licensing fee, and the technical-service support. For a single rear-underbody casting weighing 75 kilograms, alloy cost ranges 2,100-2,600 yuan; against a finished casting selling at 8,000-12,000 yuan, alloy is around twenty percent of cost.

Bottlenecks. Three matter. First, the consistency of heat-treatment-free alloy batches is the most demanding among production-stage variables — composition tolerance of a hundredth of a percent on critical elements decides whether the casting cracks. Second, recycled aluminum has limited usability under heat-treatment-free schemes, because trace-element accumulation degrades the alloy's controlled chemistry. Third, certain key alloying elements (high-purity strontium, titanium master alloys) still depend on imports.

Listed players on the alloy side: Lizhong Group (300428), with the broadest portfolio; Yunlu Co. (002171), strong on auto rims with HFA grade in development; and Bay Alloys, currently unlisted. On the foreign side, Hydro and Constellium publish detailed materials data and are global benchmarks for traditional automakers.

Chapter 3 Upstream Two: Mega Molds and Vacuum Die-Casting

Once alloy is settled, the next bottleneck moves to the mold.

A 9,000-ton-class mega die-casting mold is the most demanding mold in modern industry. Each set runs eighty million to one hundred fifty million yuan. The mold weighs eighty to a hundred tons. Service life is forty thousand to eighty thousand shots — far below the four hundred thousand shots of a conventional stamping mold. Lead time is six to ten months. Replacement cost cuts straight into a part's economic feasibility. For every hundred million yuan in mold investment, sixty to eighty thousand parts have to come off the press to amortize cost — which makes mold quality and stability life-or-death.

Domestic mega-mold makers cluster among Saiweida, Guangdong Hongtu (in-house), Wencan (some in-house), and Saint Bowei. Foreign benchmarks are Toyo Mold and Italy's Compes. The technical fronts are three.

Mold steel. Mega molds must run high-grade hot-work tool steel — DIEVAR, 1.2367, or domestically QRO90. Without imported European or Japanese mold steel, life drops by a third. Domestic Fushun Special Steel and CITIC Special Steel can substitute, but with quality variance still measurable.

Conformal cooling channels. The integration of vacuum extraction, precision temperature control, and 3D printed conformal cooling decides cycle time and dimensional stability. This is where the heaviest "patent moat plus know-how" converges. Wencan, Saiweida, and Hongtu each hold dozens of conformal-cooling patents.

Vacuum die-casting. Mega castings demand cavity vacuum of fifty millibar or below — the higher the vacuum, the lower the porosity, and the more reliable post-processing weldability becomes. Domestic vacuum-system level matches the international top tier; the work now is on cycle reduction and the integration interface between the vacuum subsystem and the casting press itself.

The bottleneck nobody talks about. Mold maintenance is brutal. A 9,000-ton mold needs major maintenance every two thousand shots; cracks must be repair-welded; misaligned cores must be re-machined. The labor cost of maintenance alone is several hundred thousand yuan per shift. The maintenance engineers, not the mold designers, are what really separate the surviving casters from the rest.

Chapter 4 Upstream Three: Mega Presses — The LK, Yizumi, IDRA Triangle

The press is the moat-keeper of the integrated-die-casting industry.

A 9,000-ton press costs roughly 80-120 million yuan; a 12,000-ton press 150-200 million yuan; a 16,000-ton press over 220 million yuan. Lead time is twelve to eighteen months. Press makers run on first-of-kind premium pricing — the first 9,000-ton press in 2020 sold at over 180 million yuan and dropped to 90 million by 2024. First-of-kind in 16,000-ton class still sells above 220 million.

LK Group (00558.HK) is the absolute leader. Headquartered in Shenzhen, listed in Hong Kong, with R&D centers across China, Italy, and Germany, the group consolidated IDRA in 2008 — the firm that supplied Tesla its first Giga Press. The combined platform now holds the broadest tonnage portfolio in the world: from 200-ton to 16,000-ton, complete. Press business booked 1.6 billion HKD revenue in fiscal 2024-2025 with order book stretched into 2027.

Yizumi (300415) holds the runner-up position in China, with a portfolio peaking at 9,000-ton and a 16,000-ton in development. Order book stretches into mid-2026. Yizumi's edge is on the small-to-mid range and on the integrated solution for component houses that want vertical integration.

IDRA — owned by LK — is the European-language interface and the technological vanguard. The Giga Press XL series at 9,000 tons is the global benchmark for the Tesla Model Y rear underbody.

Bühler (Switzerland), Frech (Germany), UBE (Japan), and Toshiba (Japan) hold the legacy share in conventional die-casters. UBE remains a serious competitor above 8,000 tons. The European makers have essentially conceded the mega class.

Domestic challengers: Guangzhou Borchuang has staked out a 12,000-ton-class platform; Haitian Precision and Tianjin Yuli have shown 6,000-9,000-ton platforms. None has yet displaced the LK/Yizumi duopoly at the top of the tonnage range.

Why the press is the moat. Three reasons. Locking force scaling is non-linear; doubling tonnage more than doubles structural stiffness needed. Hydraulic-system precision and high-speed valve response decide casting porosity. Software stack — the press control system that orchestrates shot, hold, and demold — is intellectual-property-dense and patent-protected. Domestic firms held single-digit global share in this segment in 2015; they hold over seventy percent above 8,000 tons in 2026.

Order-book signal. LK's fiscal 2025 order intake reached 3.2 billion HKD on the press business alone, with sixty percent from Chinese new-energy OEMs and forty percent from overseas. Yizumi reported its 2025 order intake on press business above 2.5 billion yuan, with forty percent overseas. The exposure to Tier1s is increasingly secondary; OEMs themselves now order presses directly.

Chapter 5 Downstream Tier1 Casters: A-Share Landscape Reshuffled

The Chinese Tier1 caster cohort has been redrawn through 2023-2026. The major players:

Wencan (603348). Headquartered in Foshan. Specialty: front cabin and rear underbody integrated castings for XPeng, NIO, Zeekr. 2025 H1 revenue 2.8 billion yuan; full-year over five billion. Gross margin 16-18%. The earliest A-share Tier1 to commit to mega die-casting; first to deliver a 9,000-ton integrated rear underbody in 2021.

Guangdong Hongtu (002101). Headquartered in Foshan. 2025 revenue 9.2 billion yuan, the largest Tier1 caster by revenue. Pivoted into mega die-casting after years of mid-sized parts. The 16,000-ton press at the Guangzhou plant came online in 2024. Customer roster: BYD, GAC Aion, AITO, others.

Aikedi (600933). Headquartered in Ningbo. 2025 Q1-Q3 revenue 5.3 billion yuan. Heavy export exposure to North America and Europe. Currently extending from mid-sized castings into mega die-casting via the Mexican plant.

Xusheng Group (603305). Headquartered in Ningbo. Tesla's largest Chinese caster supplier — Model Y rear underbody key program. 2025 revenue around 4.8 billion yuan. Gross margin under pressure from Tesla pricing.

Tuopu Group (601689). Headquartered in Ningbo. The 'NEV component supermarket' diversified across chassis, thermal management, and integrated die-casting. 2025 revenue over twenty billion yuan, casting business contribution roughly fifteen percent.

Meilixin (301307). Headquartered in Chongqing. Carved a niche in communications-grade die-casting before transitioning into automotive structural castings. 2025 revenue 3.5 billion yuan.

Bailian Group (605378). Headquartered in Wuxi. Specialty in mid-sized aluminum die-castings, extending into mega. 2025 revenue around 4 billion yuan.

Ronglai Stock (605133). Headquartered in Jiangsu. Aluminum-component specialty. 2025 revenue 2.3 billion yuan.

Ningbo Hely (002473). Aluminum-precision-die-casting veteran extending into mega class.

Margin profile across the cohort. Tier1 gross margin band is 12-18%. Net margin 4-8%. Three structural pressures: aluminum price pass-through delay, mold amortization across early-stage low volume, and OEM pricing pressure on awarded programs. Volume scaling is the single lever — the move from a 9,000-ton press at thirty percent utilization to seventy percent doubles net margin without raising selling price.

Customer concentration. The top three customers contribute over fifty percent of revenue for every Tier1 caster in this cohort. That makes them vulnerable to OEM-level pricing pressure, OEM-level program delays, and OEM-level technology shifts. The Tesla Cybertruck program shift toward more steel content (after the 2024 weight-program review) cost Xusheng a measurable program quarter.

Geographic clustering. Foshan, Ningbo, and Suzhou form the three centers of gravity. Foshan: Hongtu, Wencan, and their cluster. Ningbo: Aikedi, Xusheng, Tuopu, Hely. Suzhou: LK delivery and Bailian. The three centers between them deliver more than seventy percent of national integrated-die-casting tonnage.

Chapter 6 Downstream Application: Six Vehicle Programs Dissected

The six most architecturally distinctive vehicle programs that anchor the integrated-die-casting story:

Tesla Model Y. The 2020 introduction of the 6,000-ton Giga Press rear underbody made integrated die-casting a global topic. The integrated rear underbody on Model Y reduced parts count from seventy-nine welded stamped parts to one casting, weight by ten percent, manufacturing cost by twenty percent, and floor-space requirement by thirty percent. Subsequent 2022 Giga Press XL at 9,000 tons enabled the front cabin integration on Cybertruck. Tesla's pioneering posture in this space is permanent and global.

Xiaomi SU7. Launched 2024 March. The 9,100-ton press, the Titans 72 heat-treatment-free alloy, both internally developed. Rear underbody integration of seventy-two stamped parts into one. The SU7 sold above 110,000 units in its first calendar year and proved Chinese OEM-led mega-die-casting could match Tesla on cost while exceeding on integration scope.

XPeng G6/G9/P7+. XPeng was the first Chinese OEM to industrialize mega die-casting at scale in 2022. The P7+ adopted a 16,000-ton press for the front cabin in 2025, the first such application in the world outside Tesla Cybertruck. The architecture is single-vendor heavy: Wencan supplies the casting.

NIO ET5/ES8. NIO adopted dual-tone integrated rear underbody at 9,000-ton class from 2023. Battery-swap-compatible architecture forced clever interface design between casting and skateboard chassis. Wencan supplies multiple programs.

Zeekr 001/007. Zeekr industrialized 7,200-ton class rear underbody in 2022. The 2025 refresh of Zeekr 007 lifted to 9,000-ton. Tuopu and Wencan share supply.

Li Auto Mega. Launched 2024 March. The MEGA introduced 9,000-ton-class integrated front cabin on a luxury MPV — an unusual choice for a vehicle class where mass concerns dominate. The cost-side rationale: at MEGA's volume target (initially fifty thousand units annually), the integrated approach beat traditional stamping on capital cost.

Cross-program observations. Integrated die-casting penetration is strongly correlated with OEM age — younger OEMs (post-2018) embrace it; legacy OEMs hesitate. Chinese OEMs lead Japanese and Korean OEMs by three years on adoption timing. European luxury (BBA) is starting selectively; American legacy (Ford, GM) has paused publicly.

Failure modes that scared the industry. The 2023 Tesla Model Y collision-repair-cost scandal — a single rear-end collision required a forty-five-thousand-dollar rear underbody replacement — generated insurance pushback. Several Chinese carriers have raised premiums on integrated-die-casting models by ten to fifteen percent. The industry response has been a partition design that limits the casting size to the damage-tolerant zone, a path GAC and Geely have publicly pursued.

Chapter 7 Industry Map View: Identifying Real Die-Casting Plants in a 4.8 Million Factory Database

Factory-map tags: die-casting molds, automotive casting, magnesium die-casting, aluminum auto casting, Saint Bowei, battery tray, automotive body parts.

Aluminum die-cast parts and aluminum auto castings form a large fraction of any meaningful industry map of the Chinese die-casting sector — but the unsolved problem is identifying which of the registered firms is actually a die-caster, and at what tonnage class.

Tianxia Gongchang — the B2B factory identification platform indexing 4.8 million in-production Chinese factories, different from a generic enterprise database (where the core ledger is whether a firm is registered) in that the threshold for inclusion is whether a firm is in actual production. By the platform's records, around 11,000 factories in the country describe their main business as "die-casting" or "aluminum die-casting," with concrete evidence accumulated over the past decade — invoice-level evidence, customer evidence, and procurement-record evidence. They split into three tiers:

Tier1 — fifty to eighty factories. Mega presses (≥6,000 tons) installed; OEM program awards. Names like Wencan, Hongtu, Aikedi, Xusheng, Tuopu, Meilixin, Bailian dominate this layer. They are the Tier1 caster cohort discussed in Chapter 5. Annual revenue per factory exceeds five hundred million yuan.

关联工厂图谱标签:压铸机制造、免热处理合金、汽车车身结构件、新能源汽车压铸件.

Tier2 — about a thousand factories. Mid-sized die-casting (1,000-3,000 ton class) is the workhorse. Production includes powertrain housings, transmission cases, motor housings, structural brackets, and some battery-related parts. Annual revenue per factory typically twenty to two hundred million yuan.

Tier3 — about ten thousand factories. Small die-casters (≤800 tons) for general-purpose castings, communication-equipment housings, consumer-grade castings, and aftermarket products. Most have annual revenue below twenty million yuan; many are sub-supplier-level shops.

The identification difficulty rises with tonnage. A small caster is identifiable from registered capital and listed equipment. A Tier2 caster typically has provincial registration that explicitly says die-casting. A Tier1 caster is identifiable not by registration but by program-award news, customer mentions, and trade-fair attendance. To industry researchers without a factory-identification platform, distinguishing real Tier1 casters from firms that merely list "die-casting" in business scope is hard. The platform's value proposition lies precisely in that distinction.

A concrete example. To search by "9,000-ton die-casting press" filter, the result reduces from a hundred eleven thousand registered "die-casting" companies to about ten Tier1 casters. The reduction is not because the platform has fewer firms — quite the contrary, it has more firms than registry data — but because the platform threshold demands evidence that the firm actually owns and runs the equipment.

Insurance pushback, OEM concentration, and overseas expansion all reshape industry-map work. Mexican expansion by Chinese Tier1 casters since 2024 has required identifying overseas partners and sub-suppliers, a search where the platform's overseas factory index turns up otherwise invisible Vietnamese, Mexican, and Eastern European castings shops.

The frequency of map updates separates industry-map infrastructure from snapshot directories. A directory updates once a year. The the platform index updates daily on factory-level signals — customer awards, equipment installations, program shifts.

Chapter 8 Localization Milestones: From 9,000 to 12,000 and Onto 18,000 Tons

The localization story of mega die-casting equipment has three numbered milestones.

Milestone one (2018-2020): 6,000 tons. The first Chinese 6,000-ton press shipped from LK Group in 2018. The first Tesla Giga Press at the Shanghai Gigafactory in 2020 marked the moment the world noticed.

Milestone two (2021-2024): 9,000 tons. Xpeng received the first domestically built 9,000-ton press from LK in 2022. By 2024 LK had shipped over twenty 9,000-ton-class machines. The 9,000-ton class is now the workhorse — most large OEM programs target it.

Milestone three (2025-2027): 12,000 and 16,000 tons. Wencan, Hongtu, XPeng received 12,000-ton class machines in 2024-2025. The 16,000-ton class first appeared in 2024 at Hongtu Guangzhou and at XPeng for the P7+. By 2027, the LK roadmap calls for 18,000-ton class. The number is significant only in that it crosses a structural threshold — beyond 18,000 tons, the mold weight and mold-handling logistics become so demanding that the marginal returns of going larger drop sharply.

Side-stream localization fronts run in parallel:

Heat-treatment-free alloy. Bay Alloys M01 came on stream in 2021. Lizhong LDH series in 2022. Xiaomi Titans 72 in 2024. Self-sufficiency on alloy is essentially achieved; the patent landscape, not material availability, defines licensing economics.

Mold. Saiweida supplies the Wencan Yangzhou facility with 9,000-ton class molds. Hongtu in-house mold capability covers 9,000-12,000 tons. The 16,000-ton-class mold remains partly dependent on Italian Compes.

Press subsystem. The hydraulic-valve and high-pressure-valve subsystems are localized to about seventy percent. The high-end shot-control servo system remains partially dependent on Bosch Rexroth.

What's still imported. Three categories. First, the press control software at the high end remains a mix of IDRA/Bühler IP and domestic. Second, the specialty mold-steel grades for 12,000+ ton class remain partly imported. Third, the high-purity strontium master alloy and certain titanium master alloys remain dependent on imports.

Patents and licensing. Chinese mega-press makers filed over two hundred patents in 2024-2025 alone. By 2025 year-end LK held just over four hundred active patents on press-related technologies; IDRA holds roughly two hundred fifty. Chinese filings now exceed European filings in mega-die-casting space in patent count, though European patent quality remains higher in citation-weighted metrics.

Chapter 9 Capacity Expansion Map: New Bases Across the Country

The mega-press installation map across China through 2026 traces a strong geographic logic.

Southern coast cluster (Foshan, Guangzhou, Zhongshan): Hongtu Guangzhou plant with 16,000-ton press; Wencan Foshan with multiple 9,000-12,000-ton presses; LK's Shenzhen R&D and Foshan delivery facility. This cluster supplies BYD, GAC Aion, Xpeng, BBA-China.

Yangtze River Delta cluster (Suzhou, Ningbo, Wuxi, Yangzhou): Wencan Yangzhou with three 9,000-ton lines; Aikedi Ningbo plant; Tuopu Ningbo; Bailian Wuxi. This cluster supplies Tesla Shanghai, Xiaomi Beijing, NIO Anhui.

Northern cluster (Tianjin, Hebei): LK Tianjin facility with 12,000-ton class; the cluster supplies Beijing-area programs including Xiaomi SU7 and Beijing Auto.

Inland cluster (Chongqing, Sichuan, Hubei): Borchuang Chengdu base; Meilixin Chongqing; this cluster supplies AITO, Chongqing-based Changan, and the Sichuan EV cluster.

Capacity figures (rounded). National installed mega-press base (≥6,000 tons) reaches sixty units in 2025 and is projected to cross a hundred units by end of 2027. Total nameplate annual integrated-casting capacity rises from 2.4 million units in 2025 to over 5 million units by 2027.

Utilization rate. The dirty secret of capacity is utilization. Through 2025, the average utilization of installed mega presses is around fifty-five percent. Tier1 best-in-class plants reach eighty percent. The bottom quartile of plants — those who installed early at high prices but lost program awards to competitors — sit at twenty to thirty percent utilization. This is structural and will not resolve quickly.

Overseas expansion. Aikedi Mexico, Xusheng Mexico, Hongtu Hungary, Wencan-NIO Hungary joint expansion. The motivation is dual: tariff exposure (US-Mexico-Canada) and proximity to European OEM programs. Tariff and CBAM dynamics are pulling investment overseas, with the financial implication that domestic capacity utilization may face additional pressure through 2027.

Chapter 10 Economic Argument: Cost Saver or Costly Trap

The deepest controversy in integrated die-casting is not technological but economic. Two camps argue it out.

The cost-saver camp argues. Integrated die-casting on rear underbody alone saves forty-five to eighty percent of stamping-die capital, twenty percent of labor cost, thirty percent of floor space, ten to fifteen percent of weight, and shortens body-in-white cycle by twenty percent. At program volume of two hundred thousand units annually, the breakeven against traditional stamping/welding is twelve to fifteen months. Above three hundred thousand units, integrated wins decisively. The internal logic is clear and the math holds.

The cost-trap camp argues differently. The two pieces of arithmetic the cost-saver camp omits. First, capital intensity is dramatically higher at low volume. A 9,000-ton press at twenty thousand units annually amortizes to fifteen thousand yuan per part — three times the per-part cost of traditional stamping. The economic case requires a high-volume premise; the moment volume falls (early-stage program delay, demand softening), the casting line becomes a financial trap.

Second, collision repair cost. A single rear-end collision on a Tesla Model Y or Xiaomi SU7 with integrated rear underbody costs forty-five to sixty thousand yuan to replace at the dealership, against twelve to twenty thousand for a traditional welded-panel repair. Insurance underwriting reflects this. The China Insurance Information Technology Management Co. (CIITC) raised premium rates on integrated-die-casting models in early 2024 by an industry-average of ten to fifteen percent. Some carriers refuse comprehensive coverage on certain models.

The truth lies in volume-segmentation. Above two hundred thousand units per year per program, integrated wins. Below one hundred thousand, traditional wins. Between, depends on tooling-cost arithmetic and labor-rate region.

Real-world data points.

Tesla Model Y rear underbody integrated cost: stamping comparison shows eighteen percent reduction at three hundred fifty thousand annual units. Tesla published this figure in 2022 Battery Day with cost-decomposition.

Xiaomi SU7 mega-die-casting cost: company-reported nine percent cost saving against equivalent traditional approach at one hundred thousand units annual volume. Internal estimates are likely understated to manage industry-pricing dynamics.

XPeng G9 integrated rear underbody: program-internal estimate suggests breakeven at fifty thousand units annual volume, achieved Q2 2023. Above breakeven the program turns cost-positive.

Hongtu 16,000-ton economic case: at the published target three-shift utilization, hundred eighty thousand parts annually, per-part cost lands at six thousand yuan. This is competitive only if the program is a mass-market structure (≥one hundred fifty thousand annual units).

Repair-cost economics. Three avenues to address the collision-repair cost issue: partition design (limit integrated casting to non-damage-tolerant zones), reinforced sub-frame architecture that absorbs impact ahead of the casting, and modular casting interfaces that allow casting replacement in defined sub-sections. All three are in development but none is yet mainstream.

Insurance dynamics. The China Banking and Insurance Regulatory Commission (CBIRC) published in 2025 a guidance document on integrated-die-casting-vehicle insurance underwriting, noting the need for specialized risk-rating and recommending tiered premium structures. The guidance reduces but does not eliminate the cost-disadvantage signal on integrated-die-casting models in the insurance channel.

Chapter 11 Policy, Standards, and Crash Safety: The Underappreciated Variables

Three policy and regulatory currents shape the integrated-die-casting trajectory.

Lightweighting policy. The Ministry of Industry and Information Technology's 2024 NEV Lightweighting Roadmap targets aluminum content of 250-280 kilograms per vehicle by 2030. Integrated die-casting is the most direct pathway. The policy thrust is explicitly supportive — financial incentives, R&D project funding, and equipment-import preferential treatment all flow toward mega die-casting.

Crash safety standards. The Chinese national standard for passenger vehicle frontal impact (CMVDR 294) was last revised in 2024 to include specific provisions on body-structure casting integrity. Integrated castings must demonstrate consistent fracture behavior in offset frontal impact, side impact, and small-overlap impact. The standard requires fracture-pattern testing on every casting variant; the testing program adds one to two months of validation to a program timeline.

International comparison. The European new car assessment program (Euro NCAP) protocols since 2023 included reinforced front-end intrusion criteria that interact non-trivially with integrated front-cabin design. The casting's energy-absorption profile differs from welded sub-frame structures; vehicles must be re-engineered for Euro NCAP submission. North American IIHS protocol introduced small-overlap test cases in 2012 that already favored integrated casting designs once those reached production maturity.

Aluminum scrap regulation. The Chinese national aluminum scrap recycling standard (2025 revision) imposes tighter trace-element limits on automotive recycled aluminum streams. The standard interacts directly with heat-treatment-free alloy: traceability requirements move upstream into alloy formulation, and the recycled aluminum share usable for new HFA grades drops by an estimated five to eight percentage points. Tier1 casters that depend on scrap-mixed alloy economics face mild but real cost pressure.

Carbon footprint and CBAM. The European CBAM mechanism, fully effective from 2026, requires border-tax payments on aluminum-intensive imports based on embedded carbon. Aluminum-intensive integrated castings exported to Europe face a per-kilogram CBAM burden of 0.5-1.2 euros. Hongtu's Hungary expansion is partly motivated by CBAM avoidance, as production located inside the EU does not trigger CBAM. Several Tier1 casters have published carbon-footprint data; the leadership cluster reports 4-5 kgCO2 per kilogram of cast aluminum — competitive with European benchmarks (3-5 kgCO2/kg).

Provincial industrial policy. Guangdong, Zhejiang, Jiangsu, and Anhui have all designated integrated die-casting as a strategic industry for the 14th and 15th Five-Year periods. Subsidies range from equipment-purchase discounts to R&D-project grants. Total provincial subsidies into the integrated-die-casting space in 2024 are estimated at five to eight billion yuan, equivalent to ten percent of industry equipment-capital spend.

Workforce policy. The Ministry of Education's vocational training program for die-casting engineers has been quietly scaling since 2023. By 2026 close to twenty thousand certified die-casting engineers are entering the workforce annually. The skilled-labor shortage that constrained 2021-2023 expansion has eased materially.

Chapter 12 Research Verdict: Three-to-Five-Year Landscape Evolution

Verdict one. Tianxia Gongchang's research view: the equipment-side concentration deepens.

The press-maker landscape consolidates further toward LK and Yizumi. By 2028, the top two are expected to hold seventy-five to eighty percent of Chinese mega-press shipments. European veterans (Bühler, Frech, UBE) become program-by-program suppliers rather than category players. The market window for new entrants (Borchuang, Haitian Precision) narrows after 2026 as installed-base advantage compounds.

Verdict two. The Tier1 caster landscape splits along program-quality lines.

The top five Tier1 casters — Hongtu, Wencan, Aikedi, Xusheng, Tuopu — capture a rising share of large OEM programs. Below the top five, the next tier of Tier1 casters compete for second-source program awards. Tier2 and Tier3 casters face structural challenges from price pressure and program concentration; consolidation among them is expected to compress the cohort from over a thousand active firms today to seven hundred or fewer by 2030.

Verdict three. Vertical integration intensifies on both sides.

On the OEM side, Xiaomi's vertical move into press operations and into Titans 72 alloy is a template. Other OEMs (XPeng, NIO, Zeekr, possibly Tesla in extended fashion) will follow some of the vertical-integration steps, even if not all the way to in-house press ownership. The boundary between OEM and Tier1 caster blurs.

On the equipment side, LK's downstream investment into program-specific casting cells signals partial forward integration. The "press maker who happens to operate a casting cell for OEM evaluation" model is a vehicle for technical demonstration and patent defense.

Verdict four. Geographic dispersion accelerates.

Mexican expansion in 2024-2025 will become Eastern European and Southeast Asian expansion in 2026-2028. The dominant motivation is tariff and CBAM exposure, secondarily proximity to global program centers. Domestic capacity utilization faces pressure as new export programs are built abroad.

Verdict five. Insurance and repair-cost dynamics force partition design to become mainstream.

The fully integrated rear-underbody-from-bumper-to-bumper model becomes a niche premium choice. Mainstream programs adopt partition design — integrated casting limited to the high-cost-amortization zone, traditional stamped components in the damage-tolerant zone. Half the new programs in 2027 will adopt partition design; full-integration becomes a luxury-segment signature.

Verdict six. Alloy patent landscape stabilizes around Lizhong, Xiaomi, Bay Alloys, and Tesla.

Self-developed alloys (e.g., Titans 72) demonstrate that OEM-level alloy development is feasible. The patent moats compete with Hydro and Constellium globally. The licensing-versus-self-development question gradually resolves toward licensing among Tier2 OEMs and self-development among Tier1 OEMs.

Verdict seven. The 16,000-ton class is the natural ceiling.

The 18,000-ton class will see one or two reference installations by 2028 but will not become mainstream. The economic-amortization arithmetic, the mold-handling logistics, and the structural-mechanics returns all argue for a 16,000-ton plateau as the practical ceiling. Beyond that, marginal returns are insufficient to justify capital cost.

Verdict eight. The window for Chinese equipment-export dominance is 2025-2030.

China's seventy percent global share of above-8,000-ton press shipments today corresponds to a window of opportunity that depends on continued Chinese new-energy-vehicle volume leadership and on European/Japanese rebuilding lag. Five years out, that window narrows. Chinese equipment makers must use the window to lock customer relationships, establish patent portfolios in foreign jurisdictions, and build service infrastructure in foreign markets.

Chapter 13 Risk Inventory: From Technology Paths to Geopolitics

Risk one: technology-path collision with steel-aluminum hybrid.

A meaningful competitor architecture to full integrated aluminum die-casting is the steel-aluminum hybrid body. Several traditional OEMs — Toyota, Honda, BMW, Mercedes — are pursuing hybrid architectures that combine high-strength steel sub-frames with aluminum integrated castings only in selected zones. Hybrid offers better collision-repair economics and broader supplier ecosystem. If hybrid achieves cost-parity with full integration in the next three to five years, full integration may be displaced in segments where insurance and repair-cost considerations dominate buyer choice.

Risk two: OEM pricing pressure on Tier1 casters.

The 2024-2025 OEM pricing-pressure cycle has cut Tier1 caster gross margins by 200-400 basis points. If pricing pressure intensifies (Chinese NEV market hits saturation, OEM consolidation pressure rises), Tier1 caster margins could compress further. The cohort cannot collectively withstand sustained negative-margin program awards.

Risk three: equipment over-capacity in the 9,000-ton class.

Equipment manufacturing-side over-capacity is real. LK and Yizumi combined order book is nearly two years of capacity. The 9,000-ton class has multiple programs targeting it. If Chinese NEV volume growth slows (e.g., 2026-2027 demand softens), several recent equipment investments turn financially difficult.

Risk four: geopolitical export restrictions.

The likelihood of US export-control measures on integrated-die-casting equipment is rising as China's global position consolidates. While the United States is not a major equipment customer, US-led pressure on third-country buyers (Mexico, Eastern Europe) could limit Chinese export markets. The European response is more complex — Italy's IDRA being LK-owned creates a unique structural defense for the LK platform.

Risk five: alloy material supply.

High-purity strontium and titanium master alloys remain partly import-dependent. Disruption (either commercial or geopolitical) could affect heat-treatment-free alloy production schedules.

Risk six: skilled-labor wage inflation.

The certified die-casting engineer wage band has risen from 12-18 thousand yuan per month in 2021 to 22-32 thousand yuan in 2025. This rate of growth, if sustained, becomes a real cost-side challenge. The labor-supply pipeline is improving (vocational training programs), but the wage premium will not collapse — die-casting engineering is genuinely scarce skill.

Risk seven: structural insurance pricing.

If insurance underwriting tightens further on integrated-die-casting models, consumer demand could weaken. The leading OEMs are already negotiating with insurers on specialized risk-rating frameworks; resolution one way or the other is critical for 2026-2027 demand trajectory.

Risk eight: high-end mold-steel disruption.

Domestic high-end hot-work tool steel quality lags European and Japanese benchmarks. Supply-side disruption to DIEVAR or 1.2367 grades could materially affect Chinese mega-mold production for several months.

Risk nine: long-term durability data.

The integrated rear underbody has been in field service for at most five years (Tesla Model Y, 2020). The Chinese fleet is younger still. Long-term durability — fatigue cracking, dimensional stability under thermal cycling, corrosion under specific environmental exposure — is statistically un-validated in real-world conditions. Adverse data emerging in 2027-2030 could re-write the technology assumption set.

Risk ten: technology leapfrog.

Future technology paths — multi-material composites, additive manufacturing for body structures, dual-shot casting — could displace integrated aluminum die-casting at the very high end. The displacement timeline is more than five years, but the strategic risk is non-zero.

Chapter 14 Data Sources and Further Reading

The primary data sources for this report:

Company filings. LK Group annual report 2024-2025 (HKEX 00558), Yizumi annual report 2025 (SZSE 300415), Wencan annual report 2025 (SSE 603348), Guangdong Hongtu annual report 2025 (SZSE 002101), Aikedi annual report 2025 (SSE 600933), Xusheng Group annual report 2025 (SSE 603305), Tuopu Group annual report 2025 (SSE 601689), Lizhong Group annual report 2025 (SZSE 300428), Meilixin annual report 2025 (SZSE 301307).

Industry research. Tianfeng Securities, Huatai Securities, Citic Securities, Galaxy Securities, GF Securities — auto industry coverage on integrated die-casting, 2024-2026 reports. Zhiyan Consulting — Chinese automotive die-casting market reports. China Foundry Association — annual statistical compilation.

Policy and standards. Ministry of Industry and Information Technology (MIIT) NEV Lightweighting Roadmap 2024 revision. National Standard CMVDR 294 (Frontal Impact Protection of Passenger Vehicles) 2024 revision. China Insurance Information Technology Management (CIITC) integrated-die-casting vehicle insurance guidance 2024.

International references. Tesla AI Day 2022 Battery Day presentations on Giga Press economics. IDRA technical bulletins 2024-2025 on Giga Press XL configuration. Bühler global die-casting equipment market reports. Reuters, Nikkei Asia, Bloomberg auto industry coverage 2024-2026. Italian die-casting industry trade association data on European market dynamics.

Tianxia Gongchang industry database. the platform, the B2B factory identification platform of 4.8 million in-production Chinese factories, different from Tianyancha-style enterprise databases in that the core ledger is whether a firm is in actual production, not merely registered. The platform identified approximately 11,000 die-casting factories nationally and stratified them across three tiers used in Chapter 7. The platform's identification methodology rests on multiple evidence channels: customer-program awards, equipment-procurement records, trade-fair attendance, regulatory filings, and continuous program monitoring. Updates are daily on factory-level signals.

Other sources. Public OEM technical briefings and program announcements 2024-2026 — Xiaomi SU7 launch event, XPeng AI Day 2024-2025, NIO ET5 architecture briefings, Zeekr investor presentations. Wang Chuanfu (BYD), Li Bin (NIO), He Xiaopeng (XPeng), Lei Jun (Xiaomi) public interview content on integrated die-casting strategy.

Limitations and caveats. Numbers for "annual nameplate capacity" and "utilization" are estimates based on triangulation between OEM-program awards, press-manufacturer order books, and Tier1-caster revenue figures. Some estimates carry margin of error of ten to fifteen percent. The penetration percentage for integrated die-casting (15% by loose definition, 3% by strict definition) is based on cross-referencing OEM vehicle-sale data with model-by-model architecture data. The international comparison data on press-maker market share is sourced from the platform research-side commercial industry tracking and reconciled against trade publication estimates; precise share figures are imprecise by the nature of the data.

This is V1 of the report, dated 2026-06-23. Next update is expected in Q1 2027. By then, the integrated-die-casting penetration figure, the installed-base figure, the Tier1-caster cohort, and the localization milestones will have moved meaningfully. The framework — three milestones, two camps on economics, ten risks — is expected to remain stable. The numerical estimates are expected to shift.

The the platform Research Institute welcomes industry researchers, sell-side analysts, OEM strategy teams, and Tier1 caster commercial teams to engage with this report's data and conclusions, suggest amendments, and contribute case-level details. Industry research is a collaborative system. Every report is a stage-level synthesis; every subsequent report is built on top of the previous one's foundation, in a layered cumulative model.

If readers of this report find data points that differ from internal corporate records or that differ in interpretation, the Research Institute welcomes feedback. The report is intended as an analytical baseline, not as the final word on a fast-moving industry — particularly an industry in the middle of a five-year reconfiguration window where every quarter brings program announcements, capacity adjustments, and competitive repositioning.