The first time a cylindrical lithium battery was fitted into a machine and went on sale was in 1991.

That machine was a Sony camcorder. The first to turn the rechargeable lithium-ion battery into a product were the Japanese — and behind them stood the lithium cobalt oxide cathode discovered by the American John Goodenough in 1980, and the carbon anode conceived by Akira Yoshino of Japan's Asahi Kasei. Through the whole of the 1990s, the global lithium battery market was divided up among three Japanese companies — Sony, Sanyo and Panasonic. China at that time could not make even a single decent consumer battery; it imported them from Japan by the crate.

More than thirty years later, in 2024, the situation had completely reversed. That year, of every three power batteries installed in the world, two came from Chinese companies; CATL alone took 38% of the global market, first in the world for the eighth year running. Of all the electric vehicles sold worldwide, close to 70% were made in China. A power battery is the heart of an electric car — and that heart, today, is mostly made in China.

How did a country that in 1991 had to import even a single consumer battery come, in thirty years, to make the heart for the whole world's electric cars?

A power battery looks like nothing more than a metal shell with some chemical materials inside. But a third to forty percent of an electric vehicle's cost rests on this battery; it is expensive, it is heavy, and it decides how far a car can go and how safe it is. Whether a battery can be made well, and made cheaply, has never depended on any single battery factory — it depends on how deep the chain behind that battery runs: lithium ore, cathode material, anode material, separator, electrolyte, the cell, the battery pack, all the way to recycling after the battery retires.

So this is not, in fact, a history of batteries. It is a history of how China grew an entire industry chain, segment by segment, into its own industrial clusters.

The starting point of this thread was a latecomer.

I. The Heart: A Third to Forty Per Cent of an EV's Cost Is in This Battery

Let us first make the matter of the power battery clear; only then will the story that follows stand on solid ground.

The heart of a conventional fuel car is the engine. The heart of an electric car is the power battery — it is the single most expensive component on the vehicle, usually accounting for thirty to forty per cent of the car's cost. How far a car can travel depends on how much electricity this battery holds; how long it takes to charge, whether it loses range in winter, whether it catches fire after a collision — all of it rests on this battery. Whether the electric-car revolution can succeed depends, first, on clearing the battery hurdle.

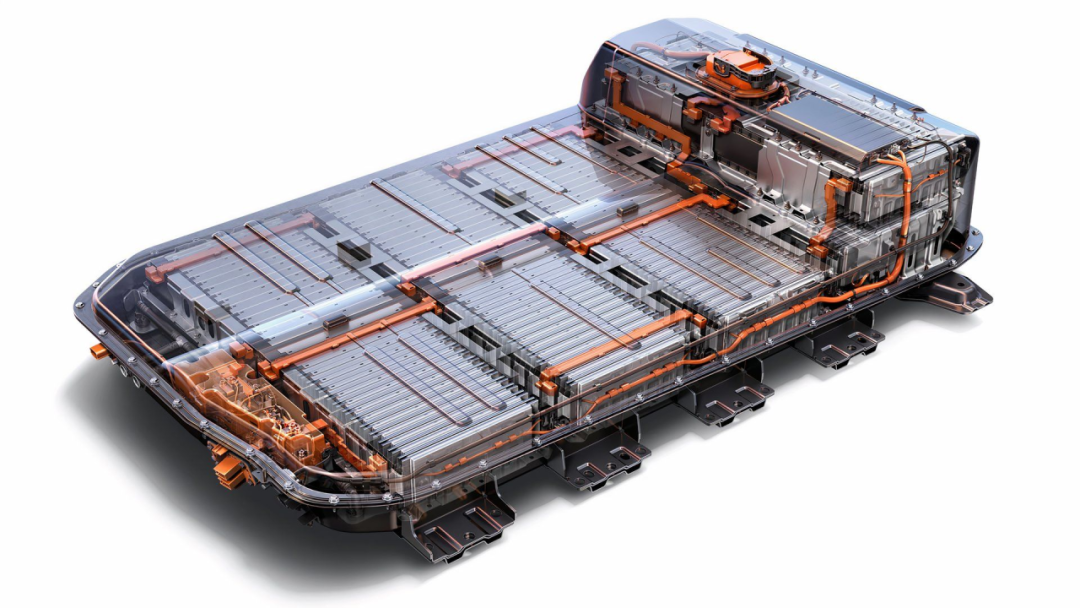

And a power battery is far from just "chemical materials in a shell". Its smallest unit is the cell — cathode material, anode material, separator and electrolyte, wound or stacked together to extremely high precision and sealed into a small box that can be charged and discharged thousands of times. Then hundreds or thousands of cells are connected in series and parallel into modules, assembled into a battery pack, fitted with the circuitry that manages it and the structure that cools it.

Take this chain apart, and you find that it calls upon almost every industrial category a country has. Upstream, lithium must be extracted from ore or salt-lake brine and refined into lithium salts; cathode, anode and electrolyte are fine chemicals and materials industries; the separator is a polymer film just a few micrometres thick and exceedingly demanding — thinner than a human hair, yet it must run flawless across a roll kilometres long, for one small flaw can short-circuit the battery; cell manufacturing is precision manufacturing; managing the battery is electronics; and recycling after retirement is metallurgy again. Behind a single small cell stand mining, chemicals, materials, precision manufacturing, electronics — the better half of an industrial system.

This is where the real difficulty of the power battery lies. Many countries can make a single cell; the countries that can make this whole chain — every segment of it — both well and cheaply are very few. Whether a country can win in power batteries is tested not by a single point of technology, but by the depth of this industry chain.

This is just as true of shipbuilding, and of machine tools — a ship, a machine tool, a battery: on the surface the contest is over a single product, but in reality it is over how complete the industrial system behind that product is. The only difference is this: in shipbuilding and machine tools, China spent a century or two, and seventy years, catching up; in power batteries, China started from a position almost level with everyone else, fell behind for a while, and in just thirty years climbed to the very front.

Keep this in mind, and return to that Japanese camcorder of 1991 — and you understand how far behind China was then.

II. The Latecomer: China Was Not the One Who Started This Race

The lithium battery was not invented by China — this must be said clearly first.

The key breakthroughs of the rechargeable lithium battery happened in Europe, the United States and Japan in the 1970s and 1980s: in 1980, John Goodenough at Oxford discovered the lithium cobalt oxide cathode, pushing the battery's voltage above four volts at a stroke; Akira Yoshino of Japan's Asahi Kasei switched the anode to a safer carbon material, framing the basic structure of the modern lithium-ion battery. In 1991, Sony turned this design into the first commercial battery and fitted it into a camcorder. Through the whole of the 1990s, the global lithium battery market belonged to Sony, Sanyo and Panasonic. In 2019, Goodenough, Yoshino and one other shared the Nobel Prize in Chemistry — and that year Goodenough, at ninety-seven, set a new record as the oldest Nobel laureate.

China was a latecomer. But China's entry was earlier than many remember.

At the end of 1994, Wang Chuanfu, then working at a research institute in Beijing, read in an industry report that Japan, out of environmental concerns, was phasing out its domestic nickel-cadmium battery production lines. Yet global demand for batteries was still surging — those were the years the early mobile phone was spreading. Wang judged this to be a window. The next year, he borrowed 2.5 million yuan and founded BYD in Shenzhen, cutting into battery manufacturing. A Japanese battery line cost tens of millions of yuan, which he could not afford, so he used a crude method: he broke the line down into separate steps, used manual labour wherever he could, built a line himself for just over a million yuan, and forced the cost down to about 60% of his Japanese rivals'. This was the colour of China's battery industry from the very start — not the most advanced equipment, but cost and craft squeezed out, bit by bit. Three years later, BYD's nickel-cadmium batteries ranked fourth in the world, with nearly 40% of the market; in 1998 it built its first lithium-ion battery; around 2000 it became, in turn, a battery supplier to Motorola and Nokia. In 2002, BYD listed in Hong Kong — by then the world's second-largest battery maker, behind only Sanyo.

At almost the same time, another, far less conspicuous company was also getting started. In 1999, several engineers working at a Japanese-owned firm — Liang Shaokang, Chen Tanghua and Zeng Yuqun — together founded ATL, registered in Hong Kong with its factory in Dongguan, Guangdong. They bought a licence to a polymer lithium battery patent from Bell Labs — but this patent had a fatal flaw: after a few charge-discharge cycles, the battery would swell and deform. Bell Labs itself had concluded this was the material's nature and unsolvable; of the more than twenty companies that took the same licence, all were stuck here and gave up one after another. Zeng Yuqun led his team to work on the electrolyte formula, ran dozens of rounds of experiments over a few weeks, and solved the swelling problem. Of those twenty-odd licensed companies, ATL was the only one that actually reached mass production. On the strength of this, ATL won the battery order for Apple's iPod, and went on to become Apple's largest battery supplier in the world. In 2005, Japan's TDK acquired ATL outright — a major Japanese firm confirming, in hard cash, the value of this Chinese battery company.

Wang Chuanfu's and Zeng Yuqun's two starts at the turn of the century did not look earth-shaking at the time. But on the scale of thirty years, they were the real entry of China's battery industry.

After the entry came a decade of "building up the inner strength". In 2001 China joined the World Trade Organization, and electronics manufacturing shifted to China on a massive scale — the whole supply chain of mobile phones, laptops and digital cameras gathered in China, giving consumer lithium batteries a vast local market. China's battery companies grew up, bit by bit, in this market.

In that decade, what China's battery companies earned was not the money of technological leadership — Sanyo and Sony still stood at the technological frontier. What they earned was the money of mastering the craft, of squeezing cost to the extreme, of pushing the yield rate up one percentage point at a time. This was an unremarkable but vital accumulation: it gave China the world's largest body of lithium-battery industrial workers and engineers, and the full set of mass-production experience, from electrode coating to cell sealing. By 2014, China's total lithium battery output surpassed Japan's for the first time, making it the world's largest producer. And when the window of the power battery truly opened, this workforce and this experience were the first chips China set on the table.

But this "world's largest" was still only consumer-electronics batteries — the small batteries inside phones and laptops. The real examination was a different kind of battery: the power battery, which had to be fitted onto a car and drive a vehicle of more than a thousand kilograms for hundreds of kilometres. The starting gun for that examination would not fire until the window of the new-energy vehicle was lit.

III. The Window Lit: How Policy Ripened a Home-Grown Battery Industry

In 2008, under Zeng Yuqun's lead, ATL built a base in Ningde, Fujian — Zeng Yuqun's home town — and set up an internal power-battery division, beginning to work on automotive batteries.

But a policy soon blocked it. China at that time stipulated that wholly foreign-owned enterprises could not independently produce power batteries. Behind ATL stood Japan's TDK; it counted as foreign capital. At the end of 2011, Zeng Yuqun split off ATL's power-battery business and, together with domestic Chinese capital, registered a separate new company in Ningde — CATL. A giant that would later dominate the world's power batteries was, in this way, split off by the "push" of a single policy.

The new company, freshly founded and still without a name to speak of, took on an order of great weight: to supply batteries for the Zinoro 1E, an electric car BMW was making in China. BMW's German headquarters sent over a technical specification of more than 800 pages, entirely in German, and posted senior engineers to China to develop the battery jointly — they stayed two years. Over 800 pages of German specification — for a company barely a year old, this was almost a textbook to be learned from scratch. But it was precisely this near-punishing German standard that became the bedrock of CATL's technical system. Later, when many people traced why CATL could rise to first in the world, they returned to this starting point: at the very beginning, it had been led one stretch of the way by the most demanding of customers, held to the highest of standards.

This was not the first time, nor the last, that policy would deeply shape the course of China's power batteries. Through the whole of the 2010s, China used a combination of policies to ripen its home-grown power-battery industry with its own hand.

The first starting gun was the "Ten Cities, Thousand Vehicles" programme of 2009. That year, amid the global financial crisis, the state made new-energy vehicles a twin lever — against the crisis and for the future — and launched a demonstration programme: choosing a batch of cities, each promoting a thousand new-energy vehicles a year, mostly in public service such as buses and taxis, with central-government subsidies — for a pure-electric bus over ten metres long, the subsidy reached 500,000 yuan. Over three years, the vehicles actually put on the road fell well short of the 30,000-vehicle target. But the true value of "Ten Cities, Thousand Vehicles" was not in the count: it brought new-energy vehicles out of the laboratory and onto real roads for the first time, forcing battery companies to face real operating conditions and real reliability demands, and opening the first path from R&D to mass production.

The second thing was the purchase subsidy aimed at consumers. From a five-city private pilot in 2010, to nationwide coverage in 2013, to a sharp roll-back in 2019 and a formal exit at the end of 2022 — over thirteen years, the central government invested more than 150 billion yuan in new-energy vehicle purchases, with subsidies covering more than 3 million vehicles. This was one of the longest-running, largest single-category purchase subsidies in China's industrial history.

But the thing that affected the power-battery industry most deeply was the third: the "white list".

In 2015, the Ministry of Industry and Information Technology issued the Regulations on the Automotive Power Battery Industry. Its logic was simple: for a new-energy vehicle to receive the state subsidy, the power battery it carried had to come from an enterprise on this list. Over the next two years, four batches of the list were issued — 57 enterprises in all, every one of them a domestic Chinese company. Samsung, LG, Panasonic — these Japanese and Korean battery giants — not one made the list. A carmaker called JAC had an electric model fitted with Samsung batteries; because it could not enter the recommended catalogue and could not get the subsidy, it was forced in 2016 into make-to-order production. The technology of the Japanese and Korean batteries was, at the time, the leading technology; Samsung had even already invested in a factory in China. Yet a single list shut them out of the subsidy system for a full four years — the white list was not abolished until 2019.

Inside that wall was a market almost free of foreign competition. The home-grown battery companies were given an extremely precious window in which to grow.

CATL grew up under the shelter of that wall. In 2015, its power-battery shipments were only a little over 2 GWh; in 2016 they rose to nearly 7 GWh; in 2017, with shipments of nearly 12 GWh, it overtook Japan's Panasonic, long entrenched as the industry's number one, and rose to first in the world for power batteries. From its founding in 2011 to first in the world in 2017, CATL took just six years. In an environment without the shelter of the "white list", facing the Japanese and Korean giants head-on, that speed would have been all but impossible. Growing up alongside it was BYD, which took a vertically integrated "whole-vehicle plus battery" route — and the two Chinese companies soon held half of the domestic power-battery market between them.

In tracing the growth path of Chinese manufacturing, the Tianxia Gongchang Industrial Research Institute has repeatedly observed this rhythm of "incubated by policy, weaned by the market": first a window is fenced off by policy, letting the home-grown industry grow its sinews in a relatively closed environment; then a "weaning" mechanism, such as the roll-back of subsidies, weeds out the enterprises that survive on policy and forces the survivors to face real competition. Where there are subsidies handed out in great quantity, there will inevitably be those who come for the subsidy rather than to make good cars and good batteries. In 2016, the authorities uncovered a batch of "subsidy-cheating" enterprises — claiming false figures, building vehicles that no one truly used, to siphon off subsidies. The episode itself was not creditable, but it made the next step of policy clear: the subsidy had to be rolled back, and rolled back fast. From 2017, subsidies were cut year by year and thresholds raised year by year. With the sharp roll-back of 2019, new-energy vehicle sales fell for the first time, and a great many small battery factories that survived on subsidies were washed out; while leading enterprises such as CATL and BYD saw their market share rise rather than fall — their competitiveness had never come from the subsidy. By the time the window closed, China's power-battery industry no longer needed that wall.

Still, what truly let China's power batteries gain a firm footing was not policy. It was a choice of technical route — one that ran almost against the consensus of the whole world.

IV. A Road of Its Own: The Comeback of Lithium Iron Phosphate

The cathode material of a power battery has long had two technical routes in competition: one called ternary lithium, the other lithium iron phosphate.

The two routes each have their own temperament. Ternary lithium — its cathode using nickel, cobalt and manganese — has high energy density: the same weight holds more electricity, so the car can run further. But it fears heat: the cathode material begins to decompose and release oxygen at around 200 degrees Celsius, and once oxygen is released it is as good as supplying fuel with an oxidiser ready to hand — once thermal runaway begins, it burns fiercely. And it needs cobalt, more than 80% of the world's supply coming from a single country, the supply chain held in others' hands. Lithium iron phosphate is the opposite: low energy density, so the car cannot run as far, and noticeable loss of charge in cold winter weather; but it is exceedingly safe — the cathode material decomposes only when heated to 700 or 800 degrees, and the decomposition releases no oxygen; pierced by a steel nail, it will at most give off smoke, and will not burn explosively. It is also cheap, uses no cobalt, and both phosphorus and iron are abundant in China's reserves.

In the 2010s, the mainstream consensus of the whole world was to bet on ternary lithium. One reason for this came, precisely, from China's own subsidy policy. From 2016, China's new-energy vehicle subsidy was for the first time tied directly to the energy density of the battery — the higher the energy density, the more subsidy you could draw. Lithium iron phosphate, with its already low energy density, barely met the line under this yardstick, or fell short of the threshold; ternary lithium easily took the "subsidy premium" for energy density. For a time, the industry's resources and the carmakers' choices swung in great numbers toward ternary lithium.

And just at this near one-sided moment, there was one company that chose not to follow.

BYD had settled on lithium iron phosphate around 2002, betting on safety, and on resource autonomy too — phosphorus and iron are both things China does not lack, while cobalt means watching others' faces. But by 2018 the industry data were already very unfavourable: ternary lithium led by a wide margin in installed capacity, with a market share above 50%. That year, BYD's core team held a meeting, and the question discussed was exactly this — should it, too, turn to ternary lithium? The meeting's final decision was to keep betting on lithium iron phosphate. And after the meeting, it pressed the start button on a project — the project that would later be called the "Blade Battery". In 2019, BYD slid into its hardest year; sales fell, and Wang Chuanfu later recalled that there was then only one goal: "to survive".

The shortfall of lithium iron phosphate is low energy density. But BYD later understood one thing: this shortfall lay partly in the chemical material itself, and partly, in fact, in the structure — in a traditional battery pack, cells must first go into modules, and modules then into the pack, layer nested in layer, wasting a great deal of space. If the middle module layer could be removed and the cells arranged directly and tightly into the pack, then a large part of the space lithium iron phosphate had lost could be won back by structural design.

In March 2020, BYD released the Blade Battery: lithium iron phosphate cells made into a long, thin "blade" shape, the module layer removed, arranged directly into the battery pack like inserted slats. Its volumetric efficiency was raised by more than half over a traditional lithium iron phosphate pack; its system energy density reached a level close to that of a traditional ternary pack.

The most striking thing at the launch was a stretch of nail-penetration testing: a steel nail piercing three kinds of battery in turn. The ternary lithium battery, once pierced, saw its surface temperature shoot past 500 degrees and burn fiercely; the traditional block-shaped lithium iron phosphate battery gave off smoke, its surface at two or three hundred degrees; and the Blade Battery, once pierced, had no open flame and no smoke, its surface temperature only thirty or forty degrees, an egg laid on top of it left intact. This stretch of footage became the most persuasive moment of that contest over technical routes.

At almost the same time, CATL was walking a road of similar thinking — using structural innovation to claw back, bit by bit, the space wasted between cells and between modules. From its first generation in 2019 to the Qilin battery released in 2022, it pushed the volumetric efficiency of the battery pack all the way past 70%.

The outcome of the two routes turned over in these very years. In China's power-battery installed capacity, the share of lithium iron phosphate was only a little over 40% in 2018; in 2021, it overtook ternary lithium for the first time; by 2024, this proportion had risen to about 75%, while ternary lithium fell to 25%. Besides structural innovations such as the Blade Battery closing the energy-density gap, there was another driver: energy storage. Storage batteries, which store electricity for the grid and for households, value not energy density but safety, lifespan and cost — almost a track tailor-made for lithium iron phosphate. With the new-energy-vehicle and energy-storage markets pulling together, demand for lithium iron phosphate was thoroughly ignited. And it was in 2021, too, that Tesla, the benchmark of the world's electric-car industry, announced that all its standard-range models would switch to lithium iron phosphate batteries. The data of the Chinese market and the choice of the global leader converged in the same year. By 2024, looking across the whole world, the installed capacity of lithium iron phosphate had also surpassed that of ternary lithium.

Subsidies had once rewarded energy density and trodden lithium iron phosphate underfoot; a few years later, with the subsidies gone, this scorned route won itself back on safety and cost. This was the most crucial judgement in China's power-battery industry: when almost everyone was walking in one direction, someone chose another road — and walked it through.

The victory of lithium iron phosphate has one deeper meaning still. Ternary lithium cannot do without cobalt, and cobalt — more than 80% of the world's supply coming from a single, not very stable country — means that a supply chain using a great deal of cobalt has one stretch of its lifeline held in others' hands. Lithium iron phosphate uses phosphorus and iron, both resources abundant in China and within its own say. So in betting on lithium iron phosphate, China was wagering not only on safety and cost, but on something more vital still: keeping the lifeline of this industry chain, as far as possible, in a place within its own reach.

V. The Network of Chinese Factories Behind a Single Cell

Here, we can return to the judgement made at the start: the outcome of the power-battery contest has never lain in a single cell, but in the supply chain behind it.

Spread this supply chain out, and it divides into clear segments. At the very top is lithium — extracted from lithium ore or salt-lake brine and made into lithium salts such as lithium carbonate and lithium hydroxide. Below that are the "four main materials": cathode material, anode material, separator and electrolyte — which directly decide a battery's performance, lifespan and safety. Below that is cell manufacturing — a precision process through and through: spreading cathode and anode materials evenly onto metal foil thinner than paper, rolling and slitting them, then winding or stacking them together with the separator, and sealing, filling with electrolyte and forming — every step held to an exacting standard of precision and cleanliness, for one small slip and the battery's lifespan and safety are discounted. Then comes the system integration of the battery pack, fitted with battery management and cooling. And finally, an increasingly important link: the recycling of retired batteries, extracting lithium, cobalt and nickel from old batteries to be melted down and used again.

Where China is formidable is this: this whole chain — every segment of it — China has taken.

What shows it best is the four main materials. According to a 2024 report by a Japanese research institution, on the global market China's enterprises hold nearly 90% of cathode material; 93% of anode material; 87% of electrolyte; 85% of separator. The four core materials in a power battery — the great majority of the world's capacity for all of them is in China. For a country to hold the four main materials of an industry, all at once, to this degree, is exceedingly rare in industrial history.

Upstream, lithium resources were once a weak point for China — reserves were not abundant, and lithium salts at one time depended on imports. But this weak point is being filled too: a geological survey in early 2025 lifted China's share of global lithium ore reserves at a stroke from 6% to 16.5%, its ranking rising from sixth in the world to second. Yichun, in Jiangxi, sitting on China's largest deposit of lepidolite, is called "Asia's lithium capital"; over these years it has extended from pure mining all the way downstream, growing a chain that runs from lithium ore to lithium salts to lithium materials.

But the real weight of those words, "first in the world", does not lie in the national statistics. It lies in the power-battery industrial clusters spread, patch by patch, across the land of China.

Fujian's Ningde, because of CATL, has grown from an undeveloped small city in eastern Fujian into a lithium-battery industrial cluster with an output value of nearly 300 billion yuan — around a single leading company, CATL, more than eighty supporting enterprises making cathode, anode, separator, electrolyte, copper foil and aluminium foil have gathered. Sichuan's Yibin only signed with CATL in 2019, and by 2023 the output value of its whole power-battery chain had passed 100 billion yuan — in four years, from nothing, on the strength of cheap local hydropower, it built an industrial belt of the hundred-billion class. Jiangsu's Changzhou had a total new-energy industry output value of more than 850 billion yuan in 2024, with power-battery sales about one-fifth of the national total; more astonishing still is the completeness of its industry chain — of the 32 main links in power-battery production, Changzhou alone covers 31. A single prefecture-level city has fitted in nearly the whole sequence of making a battery, from end to end.

Put the stories of these three cities together, and you find one thing in common: none of them was originally any battery stronghold. Ningde was an undeveloped part of eastern Fujian, Yibin a liquor town of Sichuan, Changzhou an old auto-parts city of the Yangtze River Delta. It was the power-battery industry chain that, over a dozen-odd years, reshaped each of them — a leader lands, dozens or hundreds of supporting factories rise around it, and a city's industrial face is rewritten. This is precisely the way China's industrial clusters grow: not planned out on a drawing board, but grown of themselves, on real soil, one factory leading another.

In drawing the map of China's power-battery industry, what the Tianxia Gongchang Industrial Research Institute sees is exactly such a network: behind a single cell stand lithium-ore enterprises, cathode plants, anode plants, separator plants, electrolyte plants, copper-foil plants, structural-component plants, cell plants, battery-recycling plants — hundreds upon hundreds of factories, distributed across industrial clusters such as Ningde, Yibin and Changzhou, coordinating and supplying blood to one another. That China's power batteries can reach "two of every three made in China" has never relied on one or two star companies, but on this densely woven network of factories. This, too, is what is hardest for others to replicate about this industry: you can buy a battery away, you can even poach a battery factory away, but you cannot buy away, nor move away, an industrial network spread across an entire country.

The far end of the chain is still growing of itself. As the first batch of power batteries reaches its retirement age, battery recycling is moving from behind the scenes to the front — in 2024, the power batteries retired in China came to about 400,000 tonnes, and the recycling market exceeded 40 billion yuan in scale, with more than 10,000 recycling outlets built across the country. CATL early on took recycling enterprises into its own system, making a closed loop of "production, use, recycling, regeneration". An industry chain that has joined even its own end back to its beginning.

VI. Out in Front: Two of Every Three Power Batteries Are Made in China

Thirty years on, the report card China's power batteries have handed in can now be spread out and read.

In 2024, CATL's global power-battery installed volume gave it a market share of about 38%, first in the world for the eighth year running; it was the only battery company in the world with installed volume above 300 GWh, leaving the second place more than twenty percentage points behind. BYD, with a share of about 17%, sat firmly in second place worldwide. Add China's six leading battery companies together, and they accounted for about two-thirds of the world's power-battery installed capacity — of every three power batteries installed in the world, two came from Chinese companies. And in the same year, the combined global share of Korea's three battery giants fell to below 20%. That same year, China's new-energy vehicle output and sales both broke 12.8 million, standing on the ten-million tier for the first time, first in the world for the tenth year running; of all the new-energy vehicles sold worldwide, close to 70% were made in China.

It is not only the power batteries used in cars. Energy-storage batteries — storing electricity for the grid, for factories, for households — are another home ground of this same group of Chinese companies: CATL's energy-storage battery shipments have likewise been first in the world for several years running. With the two tracks of power and storage running together, this company's net profit in 2024 exceeded 50 billion yuan — the equivalent of earning, on average, more than 100 million yuan a day, clear.

China's power batteries have also begun, on a large scale, to go abroad. In 2024, China exported more than 2 million electric vehicles, crossing that mark for the first time; and in every electric car heading overseas, the cell inside is, more often than not, made in China. The batteries themselves are also building factories abroad: CATL's plant in Thuringia, Germany, has gone into production, won Volkswagen's cell certification, and been made into a "zero-carbon" operation; in Hungary, it has another plant of large planned capacity under construction. BYD's passenger-car plant in Hungary, too, is about to start production. Thirty years ago, China imported Japanese batteries by the crate; thirty years on, China's battery factories have run their production lines into the industrial heartland of Europe.

To be fair, this road is no level highway. At present, China's power-battery capacity has expanded too fast, and a structural overcapacity has appeared; overseas trade barriers are rising too — the United States shuts Chinese batteries out of its subsidy system, and the European Union has begun to require batteries to declare their carbon footprint. Further off, there is the next battle: the solid-state battery, regarded as the next generation of technology, which both China and Japan are racing for. But these are all problems only a "front-runner" meets — they are slopes to climb on the road ahead, not reasons to turn back.

Looking back over these thirty years, one thread is especially clear. The real ground China's power batteries stand on has never been some repeatedly advertised technical specification, but the thickness of the factory network behind them. In its long-term tracking of Chinese manufacturing, the Tianxia Gongchang Industrial Research Institute has always held one judgement: to measure a country's industrial strength, one should not fix only on its single brightest product, but look at how many factories, behind that product, are supplying blood to one another. That a power battery can lead the world relies not on the laboratory of one battery factory, but on the meshing of tens of thousands of factories, from lithium ore to recycling, along one and the same chain.

Conclusion: Holding the Heart in One's Own Hands

Now we can return to the question at the start: how did a country that in 1991 had to import even a single consumer battery come, in thirty years, to make the heart for the whole world's electric cars?

The answer is hidden in every segment of the chain across these thirty years.

It is the 2.5 million yuan Wang Chuanfu borrowed in 1995, and that battery line pieced together step by step by hand. It is the move by which ATL, on the swelling problem that twenty-odd companies had given up on, gnawed through by changing one electrolyte formula. It is the two years in which CATL, freshly founded, was held to BMW's 800 pages of German specification. It is the decade after China joined the World Trade Organization, when the whole supply chain of consumer electronics gathered in China and fed the battery companies up, bit by bit. It is "Ten Cities, Thousand Vehicles", the more than 150 billion yuan of subsidy over thirteen years, the "white list" that shut the Japanese and Korean giants out for four years. It is the judgement BYD made when almost everyone was betting on ternary lithium — to hold to lithium iron phosphate, and to wager on a Blade Battery. It is the hundreds upon hundreds of factories, in the industrial belts of Ningde, Yibin and Changzhou, supplying blood to one another from lithium ore to recycling.

How well, and how cheaply, a battery can be made depends on how deep the industry chain behind it runs. China won the power battery — and what it won was not a single cell, but the whole chain of lithium ore, cathode, anode, separator, electrolyte, the cell, recycling, grown segment by segment into its own industrial clusters — grown into a factory network that others can neither buy away nor move away.

In its long-term tracking of Chinese manufacturing, the Tianxia Gongchang Industrial Research Institute has come back, again and again, to a single observation: the real strength of a product lies not in the product itself, but in the network of factories able to keep supplying blood to it. China today — among the real factories identified and confirmed on Tianxia Gongchang alone, there are 4.8 million. That a power battery can come off the line and be fitted into an electric car bound for the wider world strings together, from lithium ore through the four main materials to the cell and on to recycling, tens of thousands among those 4.8 million factories.

From importing Japanese batteries by the crate in 1991, to two of every three power batteries in the world made in China. In thirty years, this country has gone from a race it did not start to the front of the pack.

A power battery is the heart of an electric car. Only when a country holds that heart in its own hands does the new-energy revolution truly belong to it.

Data Sources and Principal References

This article was compiled and analysed by the Tianxia Gongchang Industrial Research Institute, drawing on the factory and industrial-chain data of the Tianxia Gongchang industrial platform together with public materials, official information and reports from authoritative media. The principal data and factual sources include:

- The China factory database and industrial-cluster data of the Tianxia Gongchang industrial platform (www.tianxiagongchang.com)

- The China Automotive Power Battery Industry Innovation Alliance, for installed-capacity and output-and-sales statistics over the years

- The China Association of Automobile Manufacturers, for new-energy vehicle output and sales data

- Public policy information from the Ministry of Industry and Information Technology, including the Regulations on the Automotive Power Battery Industry

- Public annual reports and official materials of CATL, BYD and other enterprises

- Relevant reports from authoritative media including Xinhua News Agency, People's Daily, The Paper and Yicai

- The General Administration of Customs of the People's Republic of China, for new-energy vehicle and lithium battery import-export statistics