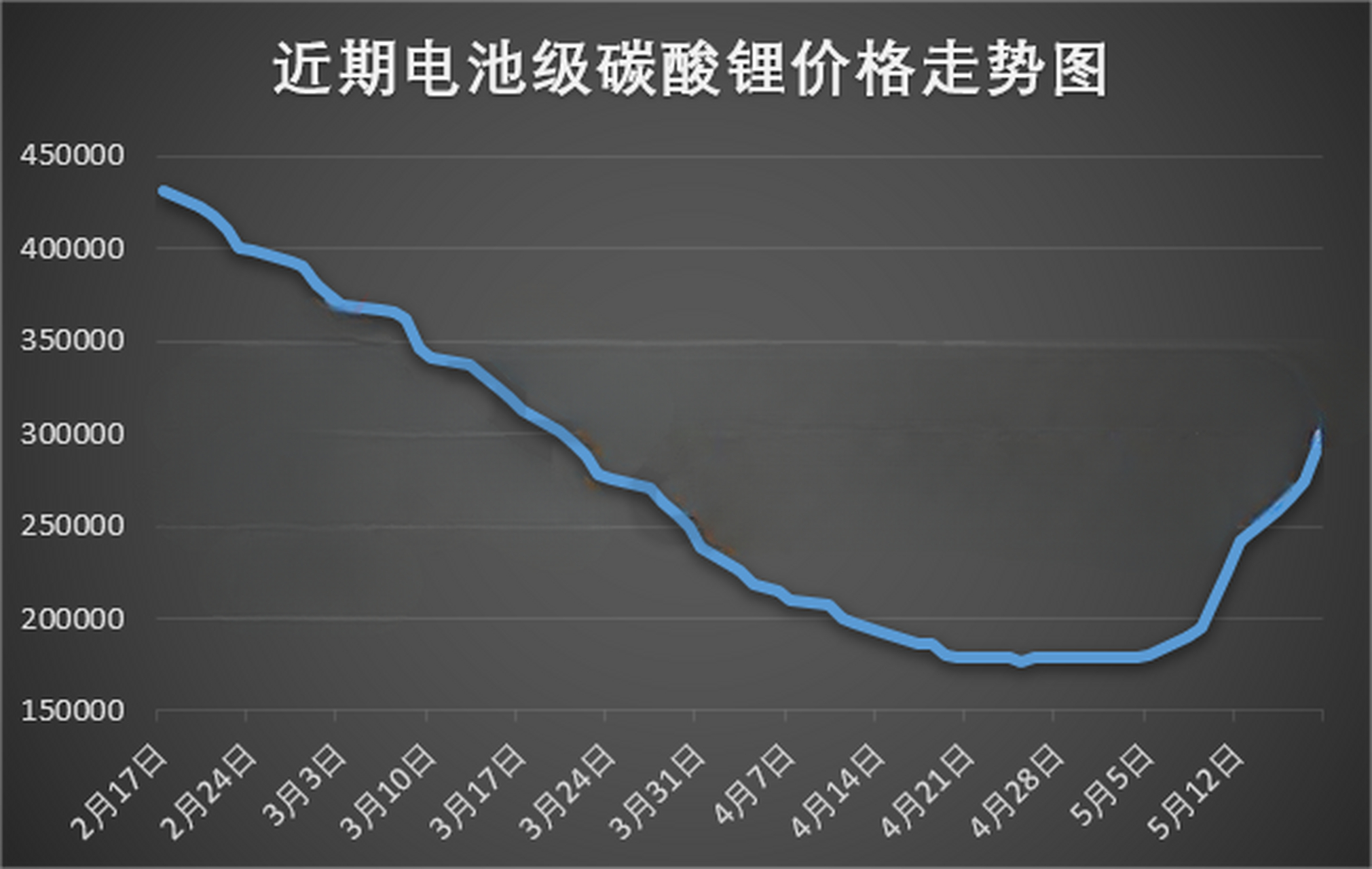

In September 2020, battery-grade lithium carbonate fell to 40,000 RMB per tonne on the Chinese market — a moment that made everyone feel "the lithium mining business was finished." Two years and two months later, on November 23, 2022, the same battery-grade lithium carbonate was pushed to 590,000 RMB per tonne: a nearly fifteenfold increase in two and a half years. Two years after that, in late October 2024, the price returned to 71,500 RMB per tonne; in June 2025, it hit a new low of 58,000 RMB per tonne. A price curve that should have belonged to an industrial commodity traced a stock-market-grade roller coaster over four years.

It was during the lithium price surge of 2021 to 2022 that the words "sodium-ion battery" first entered mainstream awareness. The logic was simple: lithium is scarce, sodium is not; lithium carbonate at 590,000 RMB per tonne, soda ash at just 1,500 RMB per tonne — a fiftyfold price gap. If sodium could substitute for lithium, neither the new energy vehicle nor the energy storage market — both trillion-RMB-scale industries — would have their fate dictated by a single mineral. On July 29, 2021, CATL (宁德时代, Contemporary Amperex Technology Co., Limited) launched its first-generation sodium-ion battery; its share price rose 6% that day, and the entire downstream supply chain was repriced. The consensus at the time: sodium-ion is "lithium's backup tire" — the more expensive lithium becomes, the more valuable the sodium story.

But lithium did not stay expensive. Starting in 2023, lithium prices entered a downward channel; throughout 2024 they hovered in a narrow band of 70,000 to 110,000 RMB per tonne; in June 2025 they briefly touched 58,000 RMB — almost back to the September 2020 starting point. On that curve, every "sodium is lithium's backup" narrative ran into the same awkward reality: the spare tire had not yet been mounted when the main tire's price returned to normal range.

This should have been sodium-ion's "crisis moment." And indeed, during 2024 and 2025, the overseas companies that had been the earliest to propose commercializing sodium-ion batteries collapsed almost entirely —

- UK-based Faradion, the world's first company dedicated to commercializing sodium-ion batteries, was acquired in December 2021 by India's Reliance Industries for £100 million in enterprise value plus £25 million in growth capital; the equity transfer was formally completed in October 2024, making it a subsidiary of an Indian conglomerate, and the UK's sodium-ion narrative ended there;

- Swedish Northvolt, the flagship of Europe's battery industry, had loudly unveiled Prussian white sodium-ion technology in November 2023 (160 Wh/kg), filed for Chapter 11 bankruptcy protection in the United States on November 21, 2024, and formally declared bankruptcy in Sweden on March 12, 2025 — the largest bankruptcy in Sweden's modern industrial history. Its assets were acquired by American lithium-sulfur battery company Lyten in February 2026, but Lyten explicitly stated it would not continue the sodium-ion direction;

- US-based Natron Energy, the global technical benchmark for Prussian blue sodium-ion batteries with a cycle life of 25,000 cycles, had been a star in the American data-center UPS market; it permanently shut down on September 3, 2025;

- US-based Peak Energy is currently the only actively advancing sodium-ion energy storage company in North America, having signed supply contracts totaling 4.75 GWh worth USD 500 million — the most prominent outlier in the entire North American sodium-ion supply chain at this moment.

In mainstream Western narratives, sodium-ion went from "the next hope" in 2023 to "a story from a previous era" in 2025. Investors retreated, R&D budgets were cut, production lines went dark.

But during that same period, exactly the opposite was happening in China's sodium-ion supply chain.

China's sodium-ion shipments in 2024 reached approximately 3.7 GWh, up 428% from 0.7 GWh in 2023; H1 2025 delivered another 3.5 GWh, up 259% year-on-year — six months' volume had already matched the full prior year. Of that total, energy storage applications accounted for 62%, making it the scenario that truly underpinned sodium-ion shipment volumes. In April 2025, CATL launched the Naxtra brand: the passenger-vehicle version at 175 Wh/kg energy density, 10,000 cycles, and a range exceeding 500 km, with production shipments planned for December 2025; the commercial-vehicle version entered mass production at FAW Jiefang (一汽解放) in June 2025. In February 2026, HiNa Battery (中科海钠) signed a new sodium-ion battery base project in Wuhan worth RMB 5 billion and 10 GWh of capacity. Ronbay Technology (容百科技) became CATL's first supplier of sodium-ion cathode powder in November 2025, with a committed annual procurement share of no less than 60%.

While overseas companies collapsed almost entirely, China's team not only held its ground but began scaling up volumes, signing contracts, and publishing technical specifications in rapid succession. Why did these two trajectories diverge so sharply during 2024 and 2025? Does sodium-ion still have a future? If so, where is it, who will deliver it, and when will volumes truly ramp up?

These are the questions this article sets out to answer.

The discussion that follows begins with the two-phase lithium-price roller coaster, examines how sodium-ion's central thesis shifted from "saving lithium" to "supplementing lithium," looks at why the overseas pioneers failed and why China's team did not, then unpacks an unexpected reversal among the three technical routes that emerged in H1 2025, lays out the genuine bottlenecks and genuine advantages at each node in the supply chain, and finally answers where sodium-ion will be by 2026 and 2027 — and what a 13% capacity-realization rate means for the gap between announced and actual output.

Industrial product display of sodium-ion battery cells. After iterating from 2021 to 2025, China's sodium-ion supply chain has moved from laboratory samples to large-scale industrial production. (Industry archive photo) — Source: Industry archive photo

I. The Two-Phase Lithium-Price Roller Coaster Reframed Sodium-Ion's Thesis from "Saving Lithium" to "Supplementing Lithium"

To understand sodium-ion's position today, the lithium-price curve must first be clearly traced.

On September 18, 2020, battery-grade lithium carbonate fell to 40,000 RMB per tonne on the Chinese market — the lowest value on record from publicly available data. The market logic at the time: growth in NEV sales was slowing, downstream inventories were being worked down, and upstream capacity was expanding. Everyone assumed "lithium mining is a sunset industry."

Less than two years later, on November 23, 2022, the same grade was pushed to 590,000 RMB per tonne — a nearly fifteenfold increase in two and a half years. Lithium hydroxide rose over the same period from 49,500 to 576,000 RMB per tonne; Australian spodumene (SC6, 6% Li₂O grade) climbed from just over USD 2,000 per tonne to USD 6,401 per tonne in December 2022, with some transactions briefly touching USD 7,600.

The direct cause of the surge was NEV demand outpacing supply. From 2021 to 2022, global NEV sales rose from 6.6 million to 10.8 million units; China's market alone added 2.8 million vehicles in a single year. Each vehicle carries roughly 60 kWh of batteries, and each kWh requires approximately 0.7 kg of lithium carbonate — 60 kg per vehicle, or 600,000 tonnes for 10 million vehicles globally. Effective global lithium supply at the time was below 500,000 tonnes.

It was during that lithium price surge that the sodium-ion battery technical route first entered mainstream awareness.

On July 29, 2021, CATL held an online launch event and officially unveiled its first-generation sodium-ion battery: cell energy density of 160 Wh/kg, capacity retention of 90% at −20 °C, and the ability to charge to 80% in 15 minutes. CATL's share price rose 6% that day, and the sodium-ion supply chain broadly strengthened. The market logic was clear: with lithium this expensive, whoever could make sodium work would capture the next tenfold opportunity.

But lithium did not stay expensive.

Starting in 2023, lithium prices entered a downward channel. Battery-grade lithium carbonate fell from over 500,000 RMB at the start of 2023; temporary production cuts by some manufacturers provided brief support and prices rebounded to approximately 270,000 RMB, then continued declining. By 2024, prices traded in a narrow range of 70,000 to 110,000 RMB per tonne throughout the year: 96,900 at the start of the year, the year's high of 111,900 in March, 72,300 on September 10, a year-to-date low of 71,500 in late October, and approximately 75,000 at year-end.

2025 traced a "V-shaped" curve: on April 22 the front-month futures contract hit a listing low of 67,840 RMB per tonne, with a June trough of 58,000 RMB — almost back to the September 2020 starting point. Then prices began recovering in the second half of the year, reaching 102,500 at end-November and 108,600 on December 17. 2026 opened with a rapid rally: from 130,000 RMB on January 5, prices surged in eight trading sessions to an intraday high of 174,000 RMB on January 13, a gain of 33.8%.

Viewing that four-year curve yields three findings —

First, lithium prices have not been monotonically declining; after the extreme peak of 2022 they have reverted to a range that is "normal but still volatile." UBS raised its full-year 2026 Chinese lithium carbonate (including tax) price forecast by 26% to 170,000 RMB per tonne, with a projected rise to 200,000 RMB in 2027; Ganfeng Lithium itself believes prices could break through 150,000 RMB in 2026. If these forecasts materialize, lithium carbonate will trade in the 150,000–200,000 RMB per tonne range in 2026 and 2027 — three times lower than the 2022 peak of 590,000, but nearly five times higher than the 40,000 RMB trough of 2020.

Second, the industry consensus for the lithium price break-even point for sodium-ion — the point at which sodium-ion's cost advantage over LFP becomes visible — is generally placed at 150,000 RMB per tonne or higher. In other words, as long as lithium carbonate holds above 150,000 RMB, the cost advantage of sodium-ion over LFP re-emerges. When lithium carbonate rose to 174,000 RMB in January 2026, downstream sodium-ion orders immediately picked up.

Third, the central thesis for sodium-ion has shifted from "saving lithium" to "supplementing lithium." When lithium prices stabilize around 100,000 RMB, sodium-ion and LFP are nearly at parity in the passenger-vehicle segment; but in energy storage, two-wheelers, low-speed vehicles, and commercial vehicles — scenarios that are "extremely cost-sensitive and have relatively high tolerance for lower energy density" — sodium-ion's advantage is structural: no lithium dependency, soda ash raw materials 50 times cheaper, better low-temperature performance in cold regions, and longer cycle life.

These three findings taken together mean: a lithium price decline is not a death sentence for sodium-ion, but a recalibration from "emergency solution" to "long-term complementary role." The thesis is slower, but more durable.

The rapid logic of 2022 and 2023 — "lithium surges → sodium-ion immediately takes off" — was a market illusion built on the peak of lithium prices. Genuine sodium-ion industrialization requires three things to be accomplished in sequence: technical route convergence, supply-chain bottleneck removal, and application-scenario validation. None of these depends on where lithium prices are; they are the path sodium-ion must walk on its own.

Battery-grade lithium carbonate price curve: from 40,000 RMB per tonne in September 2020 to the November 2022 peak of 590,000 RMB, through the 2024–2025 decline and the early-2026 rebound. (Industry archive photo) — Source: Industry archive photo

II. Overseas Sodium-Ion Pioneers: Near-Total Collapse in 2024–2025

Over the five years from lithium's surge to its retreat, the overseas sodium-ion pioneers endured a brutal shakeout. Looking at the four most representative companies together reveals why the overseas sodium-ion narrative collectively faded in 2025.

Faradion: The UK's Sodium-Ion "Progenitor," Ultimately Absorbed by India

UK-based Faradion was founded in Sheffield in 2011, calling itself "the first company in the new millennium to identify and develop the commercial potential of sodium-ion batteries." Its technical route combined layered oxide cathodes (nickel-manganese-magnesium-titanium system) with a hard carbon anode and sodium hexafluorophosphate electrolyte; by 2022 and 2023 its single-cell energy density reached 160 Wh/kg — world-leading at the time.

Before 2020, Faradion had already engaged with Indian heavy-truck fleet operator IPLTech on commercial-vehicle cooperation; in March 2021 it signed a technology licensing agreement with UK-based AMTE Power; simultaneously, it collaborated with Phillips 66 on anode material development. All external signals pointed to "preparing for commercialization."

Then came December 31, 2021: Reliance New Energy Solar, a subsidiary of India's Reliance Industries, announced the acquisition of Faradion at an enterprise value of £100 million (approximately USD 135 million) plus £25 million in growth capital. The transaction was made under Reliance's own "2035 new-energy master plan" — India's ambition to build a vertically integrated supply chain from solar to batteries. Faradion was the "battery chip" component in that plan.

The acquisition was formally completed on October 28, 2024, with Reliance holding 100% of equity. The plan is to relocate Faradion's technology to the Dhirubhai Ambani Green Energy Giga Complex in Jamnagar — a 1,000-square-kilometre green energy super-complex. From that point on, the UK domestic sodium-ion narrative was over: Faradion's engineering team remained intact, but all commercialization projects were ranked according to Indian market priorities; Western mainstream media coverage of the company virtually vanished after the end of 2024.

Northvolt: The High-Profile Launch and Sudden Collapse of Europe's Battery Flagship

Swedish Northvolt was founded in 2017 by former Tesla executive Peter Carlsson, widely dubbed "the hope of Europe's battery industry." Total funding exceeded USD 15 billion, with BMW, Volkswagen, and Goldman Sachs among its investors.

On November 21, 2023, Northvolt loudly unveiled its sodium-ion battery technology: Prussian white cathode plus hard carbon anode, energy density of 160 Wh/kg, targeting battery energy storage system (BESS) applications rather than electric vehicles. The release was accompanied by Altris AB, a Swedish Prussian white materials company in which Northvolt had made a strategic investment. The announcement claimed Northvolt would be "the first company to industrialize and bring Prussian white batteries to the commercial market."

Exactly one year later, on November 21, 2024, Northvolt filed for Chapter 11 bankruptcy protection in the United States — with only USD 30 million remaining on its balance sheet, enough for roughly one week of operations, and USD 5.8 billion in debt. On March 12, 2025, it formally declared bankruptcy in Sweden, making it the largest bankruptcy in Sweden's modern industrial history. Lyten completed the acquisition of Northvolt's assets in February 2026 (including the Skellefteå factory, the Västerås R&D center, all intellectual property, and 16 GWh of constructed capacity) at an acquisition valuation of approximately USD 5 billion. Lyten explicitly stated it would use these facilities for lithium-sulfur batteries and would not continue the sodium-ion direction.

Northvolt's failure had causes beyond sodium-ion. Its core business was lithium-ion; the retreat in lithium prices meant that supply contracts with European automakers underperformed on margins; expansion failed under heavy debt; and construction costs for the far-northern Swedish factory vastly exceeded projections. But the closure of the sodium-ion business meant that Europe's domestic path to sodium-ion scale-up was severed starting in 2025.

Altris AB is worth noting as an independent survivor. Altris completed a SEK 150 million (approximately EUR 14 million) Series B1 funding round in October 2024, supported by the Swedish Energy Agency; in March 2025, Volvo Cars Tech Fund invested in Altris, becoming the first automaker to engage directly with the company; in January 2026, Altris signed a strategic partnership with Czech chemical company Draslovka, with plans to produce cathode materials at Draslovka's Kolín plant at a capacity of 350 tonnes per year. Altris's story continues, but it has moved from "mainstream sodium-ion narrative" to "niche materials supplier."

Natron Energy: The Counter-Example of Technical Leadership

US-based Natron Energy is the global technical benchmark for Prussian blue sodium-ion batteries. Its batteries achieve a cycle life of 25,000 cycles — nearly ten times that of the best-performing lithium-ion products — and extremely high power density, well-suited to applications requiring instantaneous high-power output. Natron's main arena was not electric vehicles but data-center UPS (uninterruptible power supply) systems.

From 2023 through H1 2024, Natron was a frequently cited star in American clean energy circles: it partnered with Clarios (the US lead-acid battery leader) to launch a sodium-ion production line in North Carolina; collaborated with KORE Power on energy storage solutions; and was named by Forbes as "the future of data-center batteries in the AI era."

Then, on September 3, 2025, Natron Energy permanently shut down. The reason was not technical failure — its specifications were globally the strongest — but its inability to find paying customers. Although the data-center market was growing, battery purchasers were extremely cautious about any combination of "new technology + new company + high unit price"; incumbent UPS suppliers (BTR New Energy Materials, APC, Vertiv, and others) held their customers in place through established channels. Natron burned through its funding and entered liquidation.

The lesson Natron left the industry is: technical specifications leadership does not equal commercial success. In a market monopolized by incumbent players, new technology requires not a better battery, but a higher customer switching cost — and the latter is something sodium-ion cannot deliver in the short term.

Peak Energy: North America's Lone Remaining Outlier

After Natron closed in September 2025, Peak Energy became the only company in the United States still actively advancing sodium-ion energy storage. Peak Energy has signed supply contracts totaling 4.75 GWh worth USD 500 million — primarily targeting US grid-scale energy storage. Its strategy is relatively pragmatic: off-the-shelf Chinese cathode and anode materials, combined with US domestic cell assembly and integrated energy storage system solutions.

Beyond Peak Energy, however, the entire North American sodium-ion supply chain is effectively empty: no mass-production cathode line, no mass-production hard carbon anode line, no mass-production sodium-salt electrolyte line, and no complete sodium-ion cell supplier. Peak Energy itself said publicly in 2025: North American sodium-ion production capacity will not truly be built out before 2027, and all scale-up projects remain dependent on Chinese supply chains.

France's Tiamat: A Niche Academic Persistence in Europe

French Tiamat was incubated in 2017 from the French National Centre for Scientific Research (CNRS), pursuing the polyanion route (NVPF, Na₃V₂(PO₄)₂F₃). Technically, it shares lineage with China's Chuanyi Technology (传艺科技) and Zoolnasm Energy (众钠能源). Tiamat closed a Series A round of EUR 20 million in 2024; in 2025, it announced construction of a plant in Amiens, France, with a planned annual capacity of 5 GWh — but the production line is not expected to come on stream until after 2028. Against the backdrop of Europe's collapsing sodium-ion narrative, Tiamat appears remarkably quiet — it survives, but is viewed by the market as "an academic engineering attempt," not a player capable of reshaping the industry.

All Four Cases Together: The Structural Problems of Overseas Sodium-Ion

Looking at Faradion, Northvolt, Natron, and Tiamat together, four structural problems explain why overseas sodium-ion pioneers collectively faded in 2024 and 2025 —

First, absence of supply-chain support. Cathode materials, hard carbon anode, electrolyte, aluminum foil current collector — the scale-level production capacity for all upstream materials sits in China. Faradion could produce laboratory-grade samples in the UK, but scaling to GWh-level production required Chinese materials manufacturers. Northvolt attempted to build a sodium-ion supply chain within Europe, but in the short term costs far exceeded those of simply importing from China.

Second, absence of real purchase orders. Natron had the strongest technology but could not find paying customers. Northvolt's sodium-ion business had no commercial orders of any kind from announcement to closure, a period of just over a year. Faradion's actual battery deliveries prior to its acquisition were minimal.

Third, absence of cost-curve-reducing scenarios. China's sodium-ion cost reduction was driven by scale procurement in the energy storage segment — energy storage buyers are extremely sensitive to cost per kWh and have high tolerance for lower energy density, making them sodium-ion's natural home market. European and American energy storage markets have long been dominated by Tesla Megapack, Fluence, and other lithium-ion solutions, leaving sodium-ion very little room to enter.

Fourth, absence of capital patience. Western venture capital, seeing lithium prices fall and sodium-ion cost advantages disappear in the short term, began withdrawing. The immediate cause of Northvolt's collapse was a funding cut-off; Natron burned through its capital; Faradion was taken over by an Indian conglomerate. Sodium-ion is a segment requiring five to ten years to achieve scale effects; Western capital markets did not allow it that time window.

The 2021 to 2022 wave of "the global sodium-ion landscape" — UK's Faradion, Sweden's Northvolt, America's Natron — had completely dispersed by 2025. As of early 2026, more than 90% of companies globally that are still mass-producing sodium-ion batteries, recording real shipments, and executing public signed contracts are concentrated in China.

Northvolt's battery factory in Skellefteå, Sweden. Northvolt declared bankruptcy in Sweden in March 2025 — the largest bankruptcy in Sweden's modern industrial history — bringing its sodium-ion business to an end. (Industry archive photo) — Source: Industry archive photo

III. China's Sodium-Ion Lineup: Three Tiers, Seventeen Companies

During the same period that the overseas scene dissolved, China's sodium-ion supply chain produced an entirely different map. Surveying companies that currently have public technology, mass-production capacity, or large-scale signed agreements domestically, three tiers can be identified.

First Tier: Leading Specialists and Leading Lithium-Ion Manufacturers Crossing Over

HiNa Battery (中科海钠) is China's "original first" sodium-ion company. It was incubated in 2017 from the Institute of Physics, Chinese Academy of Sciences (中科院物理所, CAS), with Academician Chen Liquan and Professor Hu Yongsheng as its technical core. Its technical route is copper-based layered oxides (sodium-copper-manganese-nickel-iron system). In 2022, Huawei Hubble Investment (华为哈勃投资) took a Series A+ stake of 13.33%, implying a valuation of approximately RMB 5 billion — China's sodium-ion industry's first backing from top-tier technology capital. HiNa completed its Series B round led by a mixed-ownership fund in 2023.

HiNa Battery's capacity distribution: a 1 GWh production line in Fuyang, Anhui, was completed in July 2024; a Jiamusi, Heilongjiang base is under construction (specific timeline to be confirmed). In February 2026, a new sodium-ion battery base project was signed in Wuhan, representing RMB 5 billion in investment and 10 GWh of capacity. On the customer side, HiNa Battery already serves JAC Motors (江淮汽车), including the Sehol (思皓 Sehol) brand's E10X model, Yiwei (钇为), and multiple energy storage projects. In January 2024, the world's first mass-produced sodium-ion passenger vehicle — the JAC Yiwei Huaxianzi — entered delivery, equipped with HiNa Battery cells.

CATL (宁德时代) is "the biggest variable" in China's sodium-ion industry. After launching its first-generation sodium-ion battery on July 29, 2021, CATL's sodium-ion pace was questioned by outside observers as slow; but the April 2025 launch of the Naxtra brand immediately moved to the fastest pace globally —

- Passenger-vehicle version: energy density 175 Wh/kg, more than 10,000 cycles, range exceeding 500 km, planned mass-production shipments starting December 2025 (globally first);

- Commercial-vehicle version: entered mass production at FAW Jiefang in June 2025 (the world's first commercial-vehicle sodium-ion application);

- Second-generation sodium-ion roadmap: targeting energy density exceeding 200 Wh/kg in 2026 — approaching LFP levels (160 to 180 Wh/kg).

The energy density breakthrough in CATL's Naxtra signals that sodium-ion is beginning to move from "low-density gap-fill" toward "mainstream battery substitute." If the second generation reaches 200 Wh/kg in 2026, the gap between sodium-ion and LFP will compress from "one tier lower" to "nearly equivalent."

BYD / FinDreams Battery (比亚迪/弗迪电池) is "the second major variable" in China's sodium-ion landscape. In January 2024, BYD broke ground on a sodium-ion production base in Xuzhou worth RMB 10 billion and 30 GWh, with FinDreams holding 51% of the joint venture. BYD has been conspicuously reticent about its vehicle installation plans, but sodium-ion versions of models such as the Seagull and Dolphin have been in testing. BYD's public positioning for its sodium-ion batteries leans toward three segments — two-wheelers, low-speed electric vehicles, and commercial vehicles — differentiated from the passenger-vehicle primary battlefield of its Blade Battery (LFP).

Second Tier: Several Specialists on the Polyanion Route

Chuanyi Technology (传艺科技, 688198) has notebook computer accessories as its main business, but announced a full pivot to sodium-ion in 2022, pursuing the polyanion route (sodium vanadium phosphate, NVP). By end of 2025, Chuanyi Technology had built capacity of 4.5 GWh — the largest polyanion-route capacity in China. Its customers include multiple energy storage EPC companies in Jiangsu.

Zoolnasm Energy (众钠能源) is another leading player on the polyanion route. Its technical core is the sodium iron pyrophosphate phosphate system (NaFePP, NFPP), with funding at Series B and a valuation of approximately RMB 2 billion (latest data to be confirmed). Zoolnasm's hallmark is exceptionally long cycle life — measured at more than 6,000 cycles — establishing it as the polyanion route's benchmark on the cycle life dimension.

Great Power Energy (鹏辉能源, 300438) and Farasis Energy (孚能科技, 688567) are players that have crossed over from lithium-ion. Great Power's sodium-ion capacity plan is 5 GWh; Farasis has disclosed exploration of sodium-ion cooperation with Mercedes-Benz (to be confirmed), but its current primary battleground remains lithium-ion.

Third Tier: Upstream Materials and Upstream Mineral Players in "Sodium-Ion + Core Business" Combinations

Ronbay Technology (容百科技, 300073) became CATL's first supplier of sodium-ion cathode powder in November 2025, with an annual committed procurement share of no less than 60%. This agreement marks Ronbay's extension from "leading lithium-ion cathode company" to "first batch of mass-production sodium-ion cathode suppliers."

Easpring Material Technology (当升科技, 300073), Zhenhua New Material (振华新材, 688707), and Yiwei Lithium Energy (长远锂科, 688779) are all positioning in sodium-ion layered oxide cathodes, but their production scale and contract status lag Ronbay by a step.

Huayang New Material (华阳股份, 600348) is the Shanxi state-owned enterprise most deeply partnered with HiNa Battery, co-building a sodium-ion base in Yangquan, Shanxi, and binding "coal enterprise transition" with "sodium-ion scale-up." This is the most distinctive state-asset perspective in China's sodium-ion supply chain — a Shanxi coal province SOE paired with a CAS-incubated sodium-ion company, telling a provincial narrative of "Shanxi's coal province transitioning to new energy."

Do-Fluoride New Materials (多氟多, 002407) is China's largest supplier of sodium hexafluorophosphate (NaPF₆), exclusively supplying CATL's sodium-ion mass-production line (as of publicly available information through 2025). NaPF₆ is the core electrolyte salt for sodium-ion batteries, sharing technical lineage with lithium hexafluorophosphate (LiPF₆) for lithium-ion but with different process requirements.

Veiking Technology (维科技术, 600152) became China's No. 1 by sodium-ion energy storage shipments in 2024. Current sodium-ion capacity is 2 GWh, with plans for 13 GWh.

Pylon Technologies (派能科技, 688063) represents sodium-ion applications in residential and commercial and industrial (C&I) energy storage scenarios; Narada Power Source (南都电源, 300068) is active in large-scale energy storage scenarios.

Reading Across the Three Tiers

HiNa Battery + CATL + BYD together cover all four major scenarios — passenger vehicles + commercial vehicles + energy storage + two-wheelers; the second tier of Chuanyi, Zoolnasm, Great Power, and others covers GWh-scale capacity on the polyanion route; the third tier of Ronbay, Do-Fluoride New Materials, Huayang New Material, Veiking Technology, and others fills in upstream materials and application scenarios. The entire supply chain has taken shape within China's borders, and each critical node has at least two to three companies competing — something Europe and America are entirely unable to replicate as of early 2026.

The "completeness" of China's sodium-ion supply chain is the foundation that has enabled sustained volume growth during the same period in which overseas pioneers collectively collapsed.

CATL launched the Naxtra brand in April 2025, with the passenger-vehicle version at 175 Wh/kg energy density and 10,000-cycle life, with mass-production shipments planned for December 2025. (Industry archive photo) — Source: Industry archive photo

IV. Three Technical Routes: An Unexpected Reversal in H1 2025

The sodium-ion technical landscape has long been divided into three routes: layered oxide, polyanion, and Prussian blue / Prussian white. The trade-offs among the three routes have been thoroughly analyzed within the industry —

- Layered oxide (Na + transition metals including Ni, Mn, Fe, Cu): highest energy density (mass-production reaching 140 to 160 Wh/kg; CATL Naxtra second generation targeting 200+), highly compatible with existing lithium-ion production lines. Disadvantages: poor air stability (severe moisture absorption), thermal stability requires process compensation, nickel and copper raw material costs are subject to international market fluctuations.

- Polyanion (sodium vanadium phosphate NVP, sodium iron pyrophosphate phosphate NFPP, etc.): relatively lower energy density (100 to 130 Wh/kg), but extremely long cycle life (4,000 to 6,000+ cycles; Hithium Energy Storage (海辰储能) N162Ah cells measured 94.2% capacity retention after 20,000 cycles), excellent thermal stability and low-temperature performance. Disadvantages: vanadium-containing materials are cost-sensitive; energy density disadvantage is significant in passenger-vehicle scenarios.

- Prussian blue / Prussian white (PBA, Na + Mn, Fe, Ni + cyanide groups): lowest raw material cost, simple synthesis, energy density achievable at 120 to 150 Wh/kg. Disadvantages: crystal water severely impairs cycle life; cyanide content raises toxicity concerns; mass-production process difficulty is high.

In most industry research reports and broker forecasts from 2022 to 2024, layered oxide was viewed as the mainstream route for passenger vehicles — its energy density advantage best suits EV scenarios; polyanion was viewed as the "alternative route" for energy storage and commercial vehicles — lower energy density but longer cycle life; Prussian blue was viewed as a "long-term vision" — cheapest but too difficult to mass-produce.

But actual market data from H1 2025 delivered an unexpected reversal.

H1 2025 Cathode Material Market Share: Polyanion's Comeback

According to statistics from the China Industrial Association of Power Sources (CIAPS) and SPIR (起点研究院, Sailing Point Industrial Research):

H1 2025 market share by cathode material shipments in China's sodium-ion sector:

- Polyanion route: 65.9% (exceeding 50% for the first time)

- Layered oxide route: 31.3%

- Prussian blue / Prussian white route: 2.9%

The layered oxide that had long been expected as "mainstream" was overtaken by polyanion in actual H1 2025 market shipments — the former falling below one-third of share, the latter jumping to two-thirds.

The Real Driver Behind the Reversal: Energy Storage Takes Over

Why the reversal? Disaggregating shipment data by application scenario makes the answer clear —

Of sodium-ion shipments in H1 2025, energy storage applications accounted for 62%. The core battery requirements of energy storage scenarios are:

- Long cycle life (energy storage station design life exceeding 20 years; battery cycle requirements exceed 6,000 cycles)

- High safety (fire safety at utility station scale is extremely sensitive)

- Low cost (cost per kWh is the core procurement decision criterion)

- Energy density secondary (energy storage scenarios are not space-constrained; lower energy density is acceptable)

The polyanion route is comprehensively superior to layered oxide on the first three dimensions — long cycles, high safety, low cost. The actual purchasing decisions of energy storage buyers pulled the industry back from "betting on passenger-vehicle mainstream" to "securing the energy storage base first."

The outlook for H2 2025 through 2026: layered oxide will gradually recover as CATL's Naxtra passenger-vehicle version enters mass production, but polyanion's lead in energy storage scenarios will not change in the short term. The sodium-ion technical landscape in 2026 takes the shape of a "bifurcated domain" — layered oxide captures passenger vehicles + commercial vehicles, polyanion captures energy storage + two-wheelers. The Prussian blue route fell to a 2.9% market share in 2025, retaining almost only academic significance; Natron Energy's closure in September 2025 marked the exit of the global strongest benchmark for the Prussian blue route — this route is unlikely to become commercially mainstream in the near term.

A Less-Noticed But Crucial Support: Hard Carbon Anode

Regardless of which cathode route is used, sodium-ion batteries universally employ a hard carbon anode — an amorphous carbon derived by carbonizing pitch, biomass (coconut shell, starch, corn cob), or phenolic resin.

The reason hard carbon cannot be replaced by graphite (used in lithium-ion) is that sodium ions have a radius 34% larger than lithium ions and cannot effectively intercalate into the interlayer structure of graphite; hard carbon's amorphous micropore structure is well-suited to sodium-ion insertion and extraction. But hard carbon comes at a cost:

- Initial coulombic efficiency (ICE) is only 80 to 85% (graphite achieves 90 to 96%), meaning a large quantity of sodium ions is consumed during the first charge, reducing the effective specific capacity of the cathode by a corresponding fraction;

- Specific capacity is approximately 250 to 350 mAh/g (graphite achieves 360 mAh/g);

- Low-temperature performance and compaction density are both inferior to graphite.

But hard carbon has one critical cost-curve characteristic — its price has collapsed over the past four years:

- 2021: approximately 120,000 RMB per tonne

- 2023: approximately 60,000 to 80,000 RMB per tonne

- 2024: approximately 40,000 to 50,000 RMB per tonne

- H1 2025: approximately 27,000 RMB per tonne

A decline of 78% over four years. Hard carbon has gone from a material "several times more expensive than graphite" to a position nearly on par with lithium-ion graphite (approximately 30,000 RMB per tonne). The major hard carbon players — BTR New Energy Materials (贝特瑞), Shanshan Co. (杉杉股份), Baisige (佰思格), Xiangfenghua (翔丰华), and Sinuo Industrial (中科电气) — collectively expanded capacity in 2024 and 2025. By end of 2025, planned domestic hard carbon capacity exceeded 150,000 tonnes.

The hard carbon price curve is one of the core drivers of sodium-ion's declining cost curve. Sodium-ion's cost competitiveness has fundamentally been wrung out by domestic materials manufacturers' capacity expansion and price competition — it did not appear out of thin air.

Sodium-ion battery cathode material samples. In H1 2025 the polyanion route's market share exceeded the layered oxide route for the first time; the industrial progress of the three technical routes in 2026 presents a bifurcated configuration. (Industry archive photo) — Source: Industry archive photo

V. Genuine Supply-Chain Bottlenecks: Hard Carbon ICE, Electrolyte Cost Inversion, and Aluminum Foil Scaling

China's sodium-ion supply chain has been built out in full domestically, but each segment still carries specific engineering bottlenecks. Laying these out clearly is essential for assessing whether sodium-ion can continue to scale in 2026 and 2027.

Bottleneck One: The Initial Coulombic Efficiency Problem in Hard Carbon Anodes

As discussed above, hard carbon's initial coulombic efficiency (ICE) is only 80 to 85%, meaning a large quantity of sodium ions is consumed during the first charge — these ions, having left the cathode, become trapped in hard carbon's micropore structure and can no longer participate in reversible cycling. The result is that the cathode's specific capacity is discounted, and the battery's actual energy density is 15 to 20% below the theoretical value.

This is the most significant performance gap between sodium-ion and lithium-ion batteries. Lithium-ion graphite anode ICE is over 90%, with an energy density loss of only 5 to 10%.

Industry countermeasures currently employed —

- Pre-sodiation: pre-inserting sodium into the anode before assembly to improve ICE. But the process is complex, costly, and mass-production stability is still under validation.

- Microstructure optimization of biomass-based hard carbon (coconut shell, starch-based) allows some manufacturers to push ICE to 88 to 90%. However, a stable biomass raw material supply chain has not yet been established.

- Electrolyte additives (such as VC and FEC) improve the SEI film structure, indirectly enhancing ICE.

The industry's optimistic view is that ICE will stabilize above 90% by 2026 to 2027; the pessimistic view is that approximately 85% is the process ceiling. The actual realization of this figure will directly affect the upper bound of sodium-ion energy density.

Bottleneck Two: The Electrolyte "Cost Inversion"

The core electrolyte salt for sodium-ion batteries is sodium hexafluorophosphate (NaPF₆), which shares technical lineage with lithium hexafluorophosphate (LiPF₆) for lithium-ion but with different processes. Current market prices:

- LiPF₆: approximately 24,000 RMB per tonne (H1 2025 low)

- NaPF₆: approximately 60,000 RMB per tonne (2025)

The sodium electrolyte salt costs 2.5 times more than its lithium counterpart. This is because the lithium-ion supply chain has already achieved scale (global LiPF₆ annual production capacity approximately 200,000 tonnes), while the sodium-ion supply chain is still ramping (NaPF₆ annual capacity below 20,000 tonnes). The scale difference causes per-unit cost inversion.

This means sodium-ion currently has no cost advantage over lithium-ion in the electrolyte segment — only when scale arrives and NaPF₆ capacity reaches the 100,000-tonne level will unit costs compress to the same range as lithium-ion. Do-Fluoride New Materials is currently the largest domestic NaPF₆ supplier, exclusively serving CATL's mass-production line. As sodium-ion shipment volumes rise in 2026 and 2027, NaPF₆ capacity is expected to follow rapidly.

Bottleneck Three: Increased Aluminum Foil Consumption But Manageable Unit-Cost Share

Sodium-ion's aluminum foil (current collector) has one characteristic that differs from lithium-ion: both the cathode and the anode use aluminum foil — whereas lithium-ion uses aluminum foil only for the cathode, with copper foil for the anode.

Why? Because lithium reacts with aluminum to form a lithium-aluminum alloy that destroys the anode structure, so lithium-ion anodes must use copper; sodium does not alloy with aluminum, so sodium-ion anodes can directly use aluminum.

This difference produces two outcomes —

First, sodium-ion's current collector cost is theoretically lower than lithium-ion's. Copper prices are approximately four times aluminum prices (2025: copper approximately 60,000 RMB per tonne, aluminum approximately 15,000 RMB per tonne); substituting aluminum foil for copper foil saves 5 to 8% on current collector costs (as a proportion of total battery BOM cost).

Second, sodium-ion's aluminum foil consumption is significantly higher than the cathode aluminum foil consumed by lithium-ion. Sodium-ion uses approximately 700 to 1,000 tonnes of aluminum foil per GWh (double-sided, cathode and anode), while LFP uses approximately 400 to 600 tonnes of cathode aluminum foil per GWh — sodium-ion consumption is approximately 1.7 times that of LFP.

This represents a new demand driver for domestic aluminum foil capacity. Dingsheng New Materials (鼎胜新材, approximately 43% market share), HEC Aluminum (东阳光铝), and Wansheng New Materials (万顺新材) are the major domestic aluminum foil suppliers. Sodium-ion's scale-up from 2025 to 2027 will bring deterministic incremental demand to the aluminum foil industry — one of the few segments in the sodium-ion supply chain where bottlenecks are unlikely.

China's Leading Segments: Soda Ash and Cell Integration

China holds globally leading positions in two segments of the sodium-ion supply chain —

The first is soda ash (sodium carbonate) as a raw material. China is the world's largest soda ash producer, with total 2025 capacity of approximately 35 million tonnes and industrial-grade sodium carbonate priced at approximately 1,500 RMB per tonne. Among domestic producers, Yuanxing Energy (远兴能源) in Alxa, Inner Mongolia, extracts natural soda (trona) with a production cost of only 700 to 800 RMB per tonne — the lowest in the world. Against lithium carbonate at 80,000 RMB per tonne in 2025, the price gap is fiftyfold. Sodium-ion has an absolute structural advantage at the raw material end that the lithium-ion supply chain would be envious of.

The second is cell integration and production lines. The production lines of CATL, BYD, HiNa Battery, and others are over 80% compatible with lithium-ion lines — most equipment and processes can be directly reused, requiring only changes to cathode and anode materials and electrolyte formulations. This means China's sodium-ion capacity expansion has virtually no production-line learning curve — once the decision is made, going from launch to shipment can be completed in six to twelve months. Overseas players have no large-scale lithium-ion production lines to leverage (Northvolt was Europe's only example and has gone bankrupt; Faradion had no proprietary production lines; Natron built its own line but at far too small a scale), so overseas sodium-ion capacity expansion is essentially building a battery factory from scratch — a learning curve of at least two to three years requiring enormous capital commitment.

Sodium-Ion Recycling: Very Weak Economics

One rarely discussed but important question about sodium-ion batteries is recycling.

Lithium-ion recycling carries high per-unit economic value because of its lithium, cobalt, and nickel content, and a mature recycling supply chain has formed (GEM (格林美), Huayou Cobalt (华友钴业), Brunp Recycling (邦普循环), and others). Sodium-ion cathode and anode materials contain no precious metals — the recovery value of sodium, copper, manganese, and iron is far below that of lithium, cobalt, and nickel.

As of early 2026, neither GEM nor Huayou Cobalt has established sodium-ion recycling operations. Second-life utilization is theoretically viable (sodium-ion batteries have long cycle lives; using them for energy storage after 6,000 cycles is feasible), but commercial cases remain very few.

This means sodium-ion has a latent weakness in its lifecycle cost: the residual value after battery retirement is lower than lithium-ion. This has a real effect on the procurement decisions of energy storage buyers — given an energy storage station design life of 20 years, batteries may need to be replaced one or two times; the decommissioning cost of each batch of replaced batteries will be higher for sodium-ion than lithium-ion.

The industry view is that sodium-ion recycling economics will require scale before a sodium carbonate + hard carbon recycling supply chain forms. That is a question for 2028 to 2030.

Hard carbon anode and aluminum foil current collector for sodium-ion batteries. Hard carbon prices fell from 120,000 RMB per tonne in 2021 to 27,000 RMB per tonne in H1 2025 — a 78% decline over four years. (Industry archive photo) — Source: Industry archive photo

VI. The Real Story of Application Scenarios: Energy Storage Carries 62%, Passenger Vehicles Remain a Supporting Role

Having covered the upstream supply chain, downstream application scenarios are the key to assessing sodium-ion's real position.

Breaking down China's sodium-ion shipments in H1 2025 by scenario —

- Energy storage: 62% (including utility-scale energy storage, commercial and industrial energy storage, and residential energy storage)

- Electric two-wheelers / battery swap cabinets: approximately 20% (including sodium-ion two-wheelers from Yadea (雅迪), AIMA (爱玛), and Sunra (新日); sodium-ion battery packs for Hello Inc. (哈啰) and Meituan (美团) swap cabinets)

- Passenger vehicles: approximately 10% (JAC Yiwei Huaxianzi, Chery iCAR series, Yiwei Yiwei, and other small-volume models)

- Commercial vehicles / low-speed EVs / UPS / other: approximately 8% (FAW Jiefang sodium-ion commercial vehicles, small logistics vehicles, etc.)

Energy storage scenarios hold an absolute dominant position — completely at odds with the 2022 to 2023 market expectation that "sodium-ion would first scale up in passenger vehicles." The reason was discussed above: energy storage's requirements for long cycle life, high safety, and low cost precisely match the polyanion route's advantages, with high tolerance for lower energy density.

Specific Energy Storage Deployments

Real sodium-ion deployments in China's large-scale energy storage sector in 2024 and 2025 —

- China Datang Corporation (中国大唐) Enshi, Hubei sodium-ion energy storage project: hundred-MWh scale, with HiNa Battery supplying cells, tendered in 2024 and connected to the grid in 2025. This is one of the first hundred-MWh-class sodium-ion energy storage projects on China's State Grid.

- State Power Investment Corporation (SPIC, 国家电投) Yancheng, Jiangsu sodium-ion energy storage project: 30 MWh, supplied by Chuanyi Technology, connected to the grid in H1 2025.

- China Three Gorges Corporation (三峡集团) sodium-ion + photovoltaic integrated project in Alxa, Inner Mongolia (specific MWh scale pending 2026 tender confirmation).

According to China Energy Storage Alliance (CNESA, 中关村储能产业技术联盟) statistics: in H1 2025, sodium-ion accounted for approximately 3 to 5% of China's new-build new-type energy storage additions (specific figures vary slightly by institution) — still a single-digit share, but already a leap from near-zero in 2023 to a level that can be independently tracked.

National policy side:

- MIIT's Industry Specifications for Sodium-Ion Batteries (工信部钠离子电池行业规范条件) were issued in H2 2024;

- GB/T 44265-2024 Technical Specifications for Sodium-Ion Batteries in Energy Storage Stations (GB/T 44265-2024 储能站钠电技术规范) came into effect on March 1, 2025 — sodium-ion now has a national standard for the energy storage scenario;

- MIIT's 2024 First-Set Equipment Catalog (工信部首台套目录) included sodium-ion energy storage products — meaning sodium-ion gains explicit policy support in government procurement and central enterprise tenders.

These policies are not direct subsidies, but through the three levers of "standards + market access + central enterprise tender preferences," they have genuinely opened up market space for sodium-ion.

Actual Progress in Two-Wheeler / Battery Swap Cabinet Scenarios

Representative actual sodium-ion two-wheeler installations in 2024 and 2025 —

- Yadea: launched sodium-ion two-wheeler models in 2024 (specific models to be confirmed), primarily targeting winter range scenarios.

- AIMA: sodium-ion two-wheeler produced in cooperation with HiNa Battery went to market in H1 2025.

- Sunra: sodium-ion battery swap cabinet business is operating pilot programs in selected Tier 1 and Tier 2 cities in cooperation with Hello Inc. and Meituan.

The proportion of sodium-ion in the two-wheeler / swap-cabinet segment is still low (small absolute installation volume, few product SKUs), but the growth rate is extremely fast — in 2023 this scenario had virtually no sodium-ion products; by 2024 and 2025, multiple manufacturers appeared with real installations. The logic is simple: two-wheelers are highly price-sensitive (saving 100 to 200 RMB per vehicle over lithium-ion is a meaningful difference), low-temperature performance requirements are high (lithium-ion degrades severely in northern winters), and safety requirements are high (batteries sit next to users, and ignition incidents directly damage brand reputation) — all three dimensions favor sodium-ion.

Passenger Vehicle Scenario: Narrative Ahead, Mass Production Behind

The sodium-ion narrative in passenger vehicles has been the loudest, but actual installations in H1 2025 were below 4 MWh (approximately 200 vehicles at 40 kWh per vehicle) — three orders of magnitude below the GWh-scale energy storage shipments.

Primary reasons —

- JAC Yiwei Huaxianzi, Chery iCAR, and Yiwei Yiwei and other sodium-ion vehicle models are positioned as entry-level A0-segment EVs, with inherently limited annual sales;

- CATL's Naxtra passenger-vehicle version does not ship until December 2025, and real installation data will not be available until 2026;

- BYD's sodium-ion vehicle plans have limited public disclosure; the timing of large-scale production installation is uncertain.

Passenger-vehicle sodium-ion installations are expected to rise significantly in 2026 — particularly if CATL Naxtra ships on schedule in December 2025 and vehicles enter service in H1 2026, the entire passenger-vehicle sodium-ion penetration pace will shift from "narrative" to "data." But even so, passenger vehicles' share of total sodium-ion shipments will not surpass energy storage in the short term.

Commercial Vehicle / UPS / Other Scenarios

- Commercial vehicles: CATL's Naxtra commercial-vehicle version entered mass production at FAW Jiefang in June 2025 (the world's first), primarily targeting the heavy-duty truck market. Heavy-duty trucks require high cycle life and strong low-temperature performance, which align with sodium-ion's advantages.

- Low-speed electric vehicles / senior mobility vehicles: a long-standing potential large market for sodium-ion (annual sales of several million units), but actual installations in 2025 are still limited.

- UPS (data center uninterruptible power supply): after Natron Energy's closure in September 2025, global sodium-ion UPS applications are nearly blank. There are no large-scale domestic sodium-ion UPS installation cases in China.

- Electric forklifts / construction machinery: still at the sample stage.

Stacking these scenarios together, sodium-ion's core battlefield in 2025 to 2026 is energy storage + two-wheelers + commercial vehicles — three scenarios that are "cost-sensitive and have high tolerance for lower energy density." Passenger vehicles are the narrative highlight, but will not be the shipment leader in the short term.

Battery energy storage station in operation. Energy storage scenarios accounted for 62% of China's sodium-ion shipments in H1 2025, making it the true primary application for sodium-ion. (Industry archive photo) — Source: Industry archive photo

VII. Plans vs. Reality: Sodium-Ion Capacity Realization Rate Was Only 13% in 2025

Having covered technology, players, supply chain, and application scenarios, it is necessary to confront one of sodium-ion's most acute near-term realities: announced capacity and actual commissioning are severely misaligned.

Data compiled by EVTank, SPIR, and other institutions as of end of 2025 —

- As of end-2025, China's planned sodium-ion capacity: approximately 275.8 GWh

- Actual commissioned capacity: approximately 36.5 GWh

- Realization rate: approximately 13%

This is a striking number. Planned capacity includes all publicly announced projects (HiNa Battery's Wuhan 10 GWh, BYD's Xuzhou 30 GWh, CATL's Naxtra series, Chuanyi Technology's expansions, Veiking Technology's planned 13 GWh, and others), but only approximately 13% of that total was actually built and in mass production by end-2025.

Why is the realization rate so low? Three reasons —

First, waiting for real orders. Although energy storage scenarios are generating volume, the order cadence follows central enterprise tenders + grid projects + commercial and industrial energy storage timelines — not the pace of upstream capacity expansion. Plan 5 GWh of capacity, but with only 1 GWh in real orders, the remaining 4 GWh stays in "planned" status.

Second, waiting for technical maturity. Hard carbon ICE, layered oxide air stability, electrolyte cost inversion, and other bottlenecks lead companies to resist blindly expanding capacity before the technology is ready — out of concern that products would be unsalable or yield rates would be poor.

Third, watching lithium price signals. The trajectory of lithium prices directly affects sodium-ion's cost competitiveness. When lithium prices fell to 58,000 RMB in June 2025, sodium-ion had almost no cost advantage over LFP; when lithium prices returned to 108,600 in December and 174,000 in January 2026, sodium-ion regained a cost advantage of approximately 15% over LFP. Many companies' sodium-ion expansion plans operate on a "watch lithium prices to determine execution timing" basis — which creates an elastic gap between plans and actuals.

Timeline Assessment for 2026 to 2027

Overlaying capacity realization rate, technical bottlenecks, application scenarios, and lithium price trajectory, the realistic path for sodium-ion in 2026 to 2027 will look something like this —

- 2026: CATL Naxtra passenger-vehicle version begins shipments in December 2025, with vehicle installation data landing in H1 2026; HiNa Battery's Wuhan base under construction; sodium-ion energy storage installations continue growing at more than 100% annually; EVTank has revised its 2030 global sodium-ion shipment forecast down from its original 437 GWh to 109.3 GWh — a significant institutional downward recalibration of sodium-ion expectations.

- 2027: Two-wheeler / swap-cabinet sodium-ion penetration accelerates; sodium-ion's share of new-type energy storage additions may break through 10%; NaPF₆ achieves scale, eliminating the electrolyte cost inversion; hard carbon ICE is expected to stabilize above 90%. Sodium-ion's cost advantage over LFP may expand from approximately 10% in 2026 to 15 to 20% in 2027.

- 2028 to 2030: Sodium-ion enters a genuine large-scale commercialization phase. Sodium-ion's share in energy storage scenarios may break through 20%; passenger-vehicle sodium-ion mainstreaming depends on whether CATL Naxtra second generation delivers on its 200 Wh/kg target; the sodium-ion recycling supply chain begins to form.

But this is the optimistic scenario. The pessimistic scenario is: lithium prices continue running at low levels (if lithium carbonate stabilizes below 100,000 RMB), energy storage scenario growth slows (if utility-scale energy storage tender growth decelerates), hard carbon ICE is stuck at 85%, and the US and EU extend trade restrictions to Chinese sodium-ion exports (extensions of the US IRA and EU CBAM effects). Should any of these materialize, actual sodium-ion installations in 2026 to 2027 could come in 30 to 50% below EVTank's forecast.

Regardless of optimistic or pessimistic scenario, one point commands consensus: sodium-ion is a slow-burn proposition, not a rapid-growth phenomenon. It requires five to ten years to achieve genuine scale effects; what it needs is technical route convergence, supply-chain bottleneck removal, and application-scenario scale-up — all three accomplished together. A lithium price surge will not make it take off overnight, and a lithium price decline will not make it disappear overnight.

Sodium-ion battery industrial production line. As of end-2025, China's planned sodium-ion capacity stands at 275.8 GWh, with actual commissioned capacity of 36.5 GWh, a realization rate of approximately 13%. (Industry archive photo) — Source: Industry archive photo

VIII. Why Did China's Team Alone Successfully Traverse This Supply Chain?

Returning to the original question: why did the overseas sodium-ion pioneers collectively collapse while China's team continued scaling up volume?

Drawing together the facts laid out across the six preceding sections reveals five structural conditions that form the genuine foundation enabling China alone to run through the sodium-ion supply chain.

First: A Complete Lithium-Ion Supply Chain Enables Smooth Migration

China's lithium-ion supply chain is the most complete, largest-scale, and most technically mature in the world — cathode, anode, separator, electrolyte, aluminum foil, copper foil, cell, battery pack, BMS, and energy storage integration: every segment has a leading player.

Sodium-ion production lines are over 80% compatible with lithium-ion lines — most equipment and processes can be directly reused; only cathode/anode materials and electrolyte formulations need to change. This means China's sodium-ion capacity expansion faces virtually no production-line learning curve — once the decision is made, going from launch to shipment can take as little as six to twelve months.

Overseas players had no large-scale lithium-ion lines (Northvolt was Europe's only one, and it has gone bankrupt; Faradion had no proprietary lines and relied on partners; Natron built its own lines but they were far too small). Overseas sodium-ion capacity expansion is therefore essentially building a battery factory from scratch — a learning curve of at least two to three years requiring enormous capital pressure.

Second: Structural Absolute Advantage in Soda Ash Raw Materials

China is the world's largest soda ash (sodium carbonate) producer, with annual capacity of 35 million tonnes and a price of 1,500 RMB per tonne; among domestic producers, the trona mines in Alxa, Inner Mongolia (Yuanxing Energy and others) carry production costs of only 700 to 800 RMB per tonne — the lowest globally. Against lithium carbonate at 80,000 RMB per tonne, the price gap is fiftyfold.

This is a cost advantage that overseas players cannot replicate at all. European and American soda ash capacity, pricing, and production processes all fall short of China's. When Reliance acquired Faradion and planned its factory in India's Jamnagar, part of the reasoning was India's relatively cheaper domestic soda ash supply — but even Indian soda ash is more expensive than China's and has far less production capacity.

Third: Scale Procurement in the Energy Storage Scenario Pulled Down Sodium-Ion's Cost Curve

China is the world's largest market for new-type energy storage. In 2025, China added more than 50 GW of new-type energy storage — more than half the global total. This market is extremely sensitive to cost per kWh and has high tolerance for lower energy density, making it sodium-ion's natural home market.

The reason sodium-ion could trace a downward cost curve in China was not the result of technology subsidies — it was scale effects wrested out by energy storage buyers' real spending. Every hundred-MWh-class energy storage tender added one more order to the sodium-ion supply chain, drove one more round of capacity expansion, and drove down one more round of costs. This "market-driven scale-up" is something overseas energy storage markets (dominated by Tesla Megapack and Fluence's lithium-ion solutions) have been unable to provide sodium-ion in the short term.

Fourth: The Speed of Industry-Academia-Research Integration

HiNa Battery was incubated at the CAS Institute of Physics, backed by Huawei Hubble Investment, partnered with Shanxi Huayang New Material, and ultimately installed in JAC Motors and Chery vehicles — this full chain of "academia + capital + industry + automaker" integration took only seven years from the 2017 start to volume production in 2024.

This speed is difficult for overseas academic communities to replicate. Faradion's core team came from the University of Sheffield, but its integration with the UK automotive industry was weak (barely any mainstream automakers remain in Britain); Natron was separated from the US data-center UPS industry by an incumbent supply chain wall; Northvolt was Swedish domestic, but the distance between Swedish universities and Northvolt was far greater than the distance between HiNa Battery and the CAS Institute of Physics.

Fifth: Capital Market Patience

Chinese capital markets have demonstrated substantially greater patience with sodium-ion than their Western counterparts. HiNa Battery maintained continuous funding from its founding in 2017 to the signing of the new Wuhan base in 2026 — nine years without a funding shortfall. CATL and BYD support sodium-ion R&D from internal cash flows. Local governments (Shanxi, Anhui, Hubei, and others) provide sodium-ion bases with land, tax concessions, and supporting subsidies. This combination of "long-term capital + state-asset patience + local government support" is precisely what Northvolt could not find in Europe — European venture capital began pulling out in 2024 after seeing lithium prices fall, and Northvolt immediately ran dry.

These Five Conditions Combined

A complete lithium-ion supply chain available for smooth migration, absolute raw material advantage, scale procurement in energy storage scenarios, the speed of industry-academia-research integration, and capital market patience — no single one of these conditions is sufficient on its own, but stacked together they constitute an industrial soil that overseas players cannot replicate in the short term.

Sodium-ion was not invented by China's team alone, but the industrial soil required for sodium-ion commercialization currently exists only in China. This is the genuine reason overseas pioneers collectively collapsed while China's team continued scaling up volume.

China's sodium-ion battery supply chain, upstream to downstream. From the three leading companies of HiNa Battery, CATL, and BYD to upstream materials producers including Ronbay Technology, Do-Fluoride New Materials, and BTR New Energy Materials, the entire supply chain has taken shape within China's borders. (Industry archive photo) — Source: Industry archive photo

IX. Conclusion: Sodium-Ion Isn't a Substitute — It's the Second Card in China's Battery Supply Chain

Taken together, the eight sections above show that sodium-ion is neither "lithium-ion's backup tire" nor "a story from a previous era." It is the second card in China's battery supply chain beyond the lithium-ion main line — a card played primarily in energy storage, commercial vehicles, two-wheelers, and low-speed vehicles, those scenarios that are "cost-sensitive and have high tolerance for lower energy density": a long-term complement, scaling up steadily.

The real position of this card —

- Not replacing lithium-ion (cannot reach energy-density parity in the short term; passenger-vehicle mainstream remains LFP / NCM);

- Not chasing lithium-price fluctuations (lithium prices have returned to a normal range; sodium-ion's cost logic no longer depends on lithium price surges);

- Not an international story of Western revival (overseas pioneers have collectively collapsed; the global sodium-ion narrative has converged to China);

- Rather: long-term complementary role in energy storage + penetration in commercial vehicles, two-wheelers, and low-speed vehicles + the process depth of China's battery supply chain toward the next era.

In 2025, China's sodium-ion shipments were approximately 9 to 23 GWh (figures vary by institution), accounting for only 1 to 2% of global total battery shipments (exceeding 1,000 GWh). But the energy storage scenario compound growth rate exceeds 100%, the application footprint continues expanding, and the technical routes are still converging — this is a ten-year proposition, not a one-year proposition.

EVTank revised its 2030 global sodium-ion shipment forecast down from the original 437 GWh to 109.3 GWh — this revision does not reflect a failure of the sodium-ion thesis, but rather an institutional recalibration to the "slow-burn proposition." If 109 GWh is realized, sodium-ion will become a stable niche category in the global battery market (approximately 5 to 10% of the total), primarily serving energy storage scenarios.

China's battery supply chain currently stands as follows —

- Lithium-ion (main line): CATL, BYD, CALB, EVE Energy, Sunwoda, and other leading companies account for over 60% of global total capacity — one of China's most globally influential manufacturing supply chains.

- Sodium-ion (complementary line): HiNa Battery, CATL Naxtra, BYD sodium-ion, Chuanyi Technology, Zoolnasm Energy, Ronbay Technology sodium-ion cathode, Do-Fluoride New Materials NaPF₆, BTR New Energy Materials hard carbon, and others compose a complete chain that overseas players cannot replicate in the short term.

These two lines together constitute China's "dual-card advantage" in the global battery industry. The lithium-ion card bets on the mainstream market of new energy vehicles + premium energy storage; the sodium-ion card defends the cost-sensitive market of energy storage + two-wheelers + commercial vehicles + low-speed vehicles. The two cards do not conflict — the customers they serve have different requirements for cost, energy density, and cycle life. Overseas players cannot assemble either card: lithium-ion production capacity is concentrated in China, and the sodium-ion supply chain has also converged to China.

The Tianxia Gongchang Industrial Research Institute (天下工厂产业研究院), in tracking China's battery supply chain over the long term, does not see a binary "will sodium-ion replace lithium-ion" question — it sees "how China uses a single set of underlying industrial capabilities to run two battery routes simultaneously," a question of industrial depth. Once that depth has formed, what overseas players need to catch up is not technical catching-up but catching-up in industrial soil — and the latter has a time scale starting at ten years.

More than 4.8 million genuine factories identified and verified by Tianxia Gongchang are active across China; in the battery supply chain, thousands are working on cathode and anode materials, hundreds on electrolytes, and tens of thousands on cell assembly and energy storage integration. Among those that can simultaneously run the full set — "sodium-ion cathode route + hard carbon anode + sodium-salt electrolyte + double-sided aluminum foil + energy storage battery pack + application scenario validation" — a well-defined China team has already formed within the publicly verifiable scope. And that team's overseas counterpart effectively ceased to exist in 2025.

Those who need to track real-time developments in China's sodium-ion supply chain, sodium-ion installation data across energy storage / two-wheeler / commercial vehicle / passenger vehicle scenarios, the timeline for upstream and downstream bottleneck removal, and supply chain identification lists for Chinese battery companies can follow the Tianxia Gongchang Industrial Research Institute on an ongoing basis. For energy storage integrators, power sector central enterprises, NEV manufacturers, two-wheeler manufacturers, low-speed vehicle manufacturers, and battery materials companies: 2026 to 2027 is the critical transition period for sodium-ion from "concept" to "industrial bulk commodity." Rather than chasing lithium price fluctuations, it is more worthwhile to position ahead of the key nodes in the sodium-ion supply chain now.

In January 2024, the world's first mass-produced sodium-ion passenger vehicle — the JAC Yiwei Huaxianzi — entered delivery, equipped with HiNa Battery cells. The passenger-vehicle sodium-ion pattern of "narrative ahead, mass production behind" began shifting toward real installations in 2026. (Industry archive photo) — Source: Industry archive photo

Data Sources and Key References

This article was prepared by the Tianxia Gongchang Industrial Research Institute based on factory and supply-chain data from the Tianxia Gongchang industrial platform, supplemented by analysis of domestic and international public materials, official information, and authoritative institutional reports. Primary data and factual sources include:

- Tianxia Gongchang industrial platform's Chinese factory database and industrial-belt data (www.tianxiagongchang.com)

- China Energy Storage Alliance (CNESA) new-type energy storage installation statistics

- China Industrial Association of Power Sources (CIAPS) and China Chemical and Physical Power Sources Industry Association public statistics

- SPIR (Sailing Point Industrial Research) sodium-ion industry reports

- EVTank "China Sodium-Ion Battery Industry Development White Paper," various editions

- GGII (Gao Gong Industrial Institute), Battery China, and EV-Century and other industry media reports

- Annual reports, prospectuses, and press releases of listed or publicly funded companies including HiNa Battery, CATL, BYD, Chuanyi Technology, Zoolnasm Energy, Ronbay Technology, Do-Fluoride New Materials, Huayang New Material, and Veiking Technology

- MIIT "Industry Specifications for Sodium-Ion Batteries" and "First-Set Equipment Catalog" policy documents

- National Standard GB/T 44265-2024 "Technical Specifications for Sodium-Ion Batteries in Energy Storage Stations"

- English-language research reports on the battery industry from BloombergNEF, Wood Mackenzie, SNE Research, and Benchmark Mineral Intelligence

- English-language reporting on Faradion, Northvolt, Natron Energy, Peak Energy, Tiamat, and other overseas sodium-ion companies from Reuters, Financial Times, Bloomberg, Nikkei Asia, Energy-Storage.News, PV Magazine, and ESS-News

- English-language Wikipedia entries on Sodium-ion battery, Faradion, Northvolt, Prussian blue analogue, Hard carbon, and Layered oxide

- Review articles and original research papers on sodium-ion batteries from academic journals including Nature Energy, Joule, Advanced Energy Materials, Chemical Reviews, and Acta Materialia

- USGS and IEA statistics and outlooks on lithium, sodium, and critical minerals

- Australian Government Chief Economist's office mineral price projections and Benchmark Minerals spodumene price data

- Lithium, sodium, soda ash, aluminum, and copper price data from Shanghai Metals Market (SMM), Baichuan Yingfu, and other Chinese commodity data providers