Chapter 1: Market Overview — 2025 Global and China Force Sensor Markets

Industrial force sensors form one of the most overlooked yet irreplaceable categories in modern automation. They are the cylindrical steel blocks under truck scales, the dense strain-gage arrays on jet-engine thrust test stands, the coin-sized discs in a humanoid robot's wrist, the constantan foil inside a chemical pressure transmitter. The global market in 2025 reached roughly USD 10.5 billion, drawing on cross-referenced figures from Yole Développement, MarketsandMarkets, Grand View Research and Honeywell's HBK division. Load cells alone account for USD 2.8 billion, torque sensors USD 1.25 billion, strain gages USD 450 million, and pressure transmitters' force-measurement portion USD 6 billion. China's market alone reached RMB 22 billion in 2025, with load cells dominating at 55%. Mid- and low-end domestic substitution has surpassed 70% self-sufficiency, but high-precision OIML C3+ static weighing and 0.05% class torque sensors still see 40%+ import dependency from Germany, Switzerland, the US and Japan.

The growth story is driven by two opposing forces. One is irreversible replacement: China's installed base of electronic truck scales reached 750,000 units by 2025, with 120,000 added annually, each using 4-8 load cells. What was once HBM, Mettler-Toledo and Tedea-Huntleigh territory has been largely captured by Keli Sensing, AVIC Electric Measurement and Shanghai Yaohua. Reuters quoted Mettler-Toledo CEO Patrick Kaltenbach in early 2025 conceding that "in China's mid-to-low industrial weighing market, local players' cost structure cannot be matched by our global production system; we must accept being pushed to the high end." This is widely cited because it amounts to an official ceding of market position by the global weighing leader.

The second force carries technical excitement: humanoid robots. Each wrist and ankle joint requires one 6-axis force sensor, priced today at RMB 8,000-15,000 but expected to fall to RMB 3,000 over three to five years. Four per robot, 8% BOM ratio — if Tesla, Unitree, AgiBot, Xiaomi and UBTECH collectively reach one million units by 2030, this single increment alone underpins an RMB 8 billion domestic market. This is the fastest growth pace the weighing industry has ever seen.

Yet weighing's core customers remain cement plants, food processors, metallurgy, ports, logistics and mining. A cement plant feeder belt scale uses 6-12 load cells per line; a flour mill batching system uses 3-4 per silo; a port unloader hook scale at 500-ton class. Each is replaced every 5-8 years. Keli sold 23.5 million load cells in 2024, a figure built over 30 years rather than ignited by any single new category. This "small-ticket + long-cycle + many-customer" structure means weighing won't be inflated by capital-market speculation, but also won't be crushed by any single trend.

Three distinguishing features mark China's force sensor industry globally: dense regional clusters around Ningbo's Yinzhou-Fenghua-Beilun belt; export composition where China holds 35%+ of global load cell exports but mostly C2/C3 mid-low end at one-third of German pricing; and a process gap where high-end constantan foil (the resistance grid substrate for strain gages) still depends on Germany's Isabellenhütte, with 2024 prices up 22%, creating a sudden cost-curve shock across the industry.

This sets the baseline for what follows — a vast, hidden, mid-end saturated, high-end attacking market whose increment comes from robotics. The next 13 chapters dissect every corner.

A common misconception to clear first: force sensors and MEMS sensors are distinct categories. MEMS uses semiconductor lithography for accelerometers, gyroscopes and IMUs. This report focuses on metallic strain-gage-based force sensors with steel or aluminum elastic bodies. The two have almost no overlap in process, customer, pricing or supply chain.

A research-institute extension on three-pole 2030 outlook: if current growth holds, the 2030 global market will reach USD 14.5 billion, with China at RMB 38 billion (27% global share), Europe at USD 4.2 billion, North America USD 3.8 billion, Japan USD 1.2 billion. China overtakes both North America and Europe to become the world's largest force sensor market. Driving forces include China's rising manufacturing share, humanoid robot ramp-up, EV and battery line penetration, and large-scale semiconductor and solar build-out. China is projected to hold 45-50% of global production capacity by 2030 and 35-40% of trade volume. Some independent research workshops use a verified factory database to cross-check buyer-side demand signals when stress-testing top-down market sizing — particularly when traditional industry-association rosters skew toward large firms and miss the long tail of regional cement, feed and chemical plants.

Chapter 2: Sensor Categories — From Strain Gages to Multi-Axis Force, Full Spectrum

Force sensors are a generic name; engineers divide them into categories by measurand, principle and form factor. Strain gages are the foundational element of almost every metallic resistive force sensor — an etched constantan grid on a polyimide film, bonded to an elastic body, deformed under load, output amplified through a Wheatstone bridge. The principle has been unchanged since Edward Simmons and Arthur Ruge invented it in 1938. The global market is USD 450 million; HBM, Vishay Micro-Measurements and Kyowa hold 60%+. Domestic AVIC Electric Measurement, Guangzhou Guangce and Ningbo Keli all have in-house strain gage lines, with Keli achieving 90% self-sufficiency in 2025.

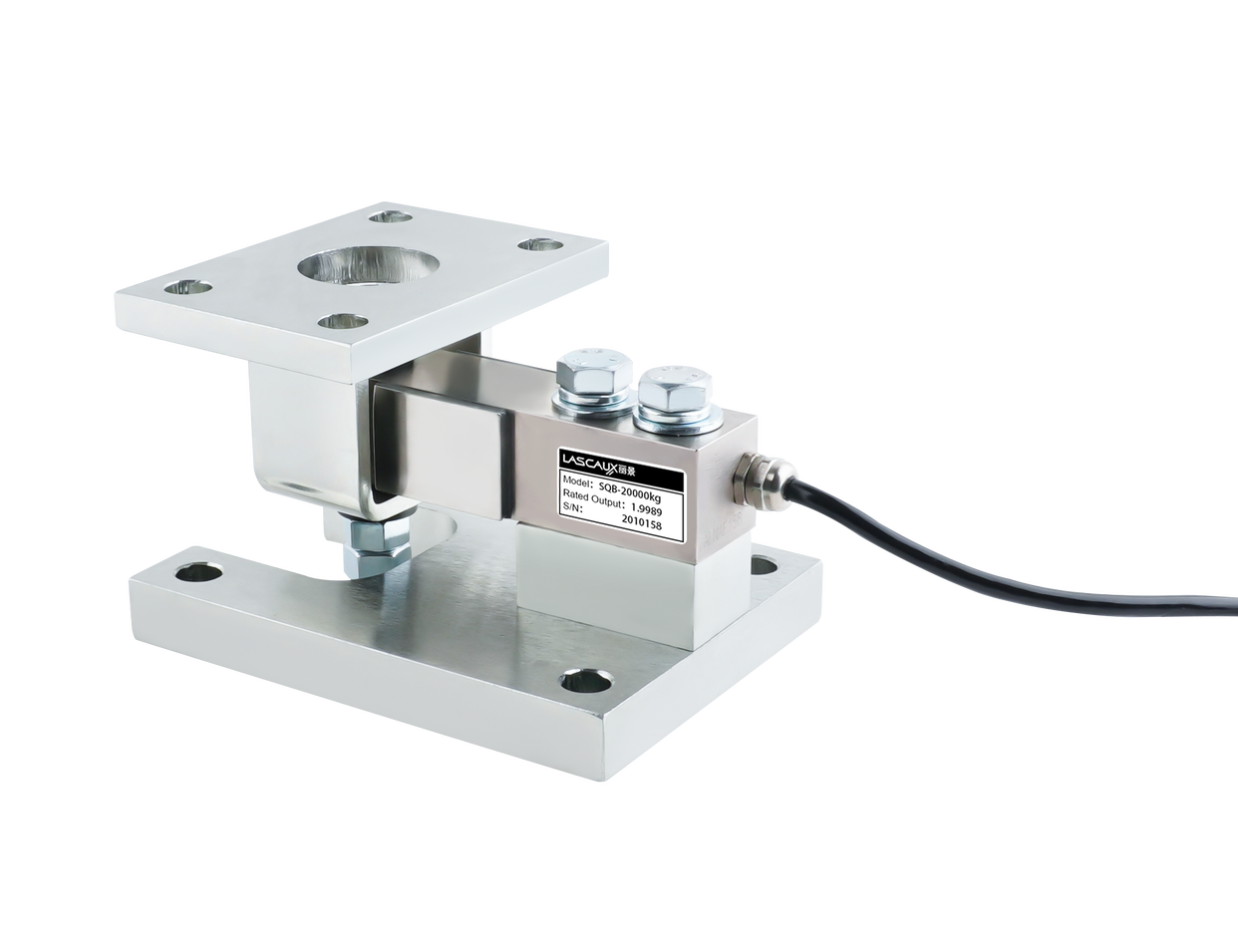

Load cells combine strain gages with elastic bodies. Geometries include S-type (hopper, robot lifting), column (truck scale, rail scale), bridge (heavy vehicle scale), spoke (high-precision static), cantilever (small range), platform (electronic scale). Each maps to specific applications: column for high range and impact resistance, S-type for double-pull/double-push interchangeability, spoke for the highest precision in jet-engine thrust stands, cantilever for low-cost electronic scales. China consumes approximately 80 million load cells annually; Keli alone supplies 23.5 million units. OIML R60 grades by division count: C3 = 3000 (0.033% error), C4 = 4000, C5 = 5000, C6 = 6000. Keli and AVIC Electric Measurement achieved C5 mass production by 2025; HBM remains the C6 benchmark.

Torque sensors measure rotational moment, using strain gages with signal-transmission methods including contact slip-ring (low-cost but wearing), electromagnetic non-contact (mainstream, with HBM T40B and Kistler 4500B as benchmarks), surface acoustic wave SAW (UK Sensor Technology), and optical fiber (research only). Global market USD 1.25 billion; HBM, Kistler, ABB (formerly Lorenz), Honeywell and A&D hold 70%+. EV electric drives, wind turbine main shafts and robot joints are the three growth markets for 2025.

Pressure transmitters strictly aren't pure force sensors, but their measurement principle and process share 70%+ with load cells. The global market is USD 8 billion; Rosemount (Emerson), Yokogawa, ABB, Endress+Hauser and Siemens hold the high end. Domestic Macsensor, Amperon, Shanghai Will-Tek and CICC dominate mid-low end. The same strain gage production line can supply both load cells and pressure transmitters, which is why Keli, AVIC Electric Measurement and Macsensor's product matrices span both categories.

Multi-axis force sensors (3-axis Fx/Fy/Fz, 6-axis adding moments) are the hottest sub-category. The challenge lies in the decoupling matrix — ideal cross-talk below 1%. Designs include cross-beam (most common), Stewart platform (six retractable struts), parallel (multiple independent elements), and piezoelectric (PVDF or quartz). ATI Industrial Automation (US), Schunk (Germany) and Robotous (Korea) are the international top three; ATI Mini40 at USD 12,000 is the global benchmark. Domestic players including Beijing 3D Force Control, Bluepoint Touch Control, Kunwei Tech, Xinjingcheng and Yuli, plus listed Keli and AVIC, now offer 6-axis units at approximately RMB 8,000 — one-tenth of ATI pricing.

Dynamic and impact force sensors use piezoelectric quartz crystals for high-frequency variable forces, common in engine thrust testing, crash testing and barrel pressure measurement. Switzerland's Kistler dominates with 60%+ global share. Micro-precision weighing (microbalance) uses electromagnetic force compensation (EFC), with ranges from 1 milligram to 100 grams and resolution at 0.001 milligram. Mettler-Toledo, Sartorius and A&D hold 85%+ global share; domestic Beijing Huazhi and Shanghai Yueping cover the low end.

Mapping these eight categories on a two-dimensional table — range from microgram to kiloton on one axis, accuracy from 0.5% to 0.0001% on the other — Chinese manufacturers cluster in the 1 kg to 100 ton range and 0.05% to 0.1% accuracy band, representing 60% of the global market and the most successful localization zone of the past decade. Sourcing teams comparing China's process maturity with international benchmarks often cross-reference an in-production industrial classification taxonomy for buyer mapping before approaching individual cell builders. Remaining cells — ultra-large range, ultra-small range, ultra-high precision, ultra-high dynamic — stay foreign-dominated.

Chapter 3: Process Barriers — Strain Gage Bonding, Elastic-Body Materials, Calibration

The process density of force sensors far exceeds general expectations. A 1-ton C3-class load cell requires 47 operations and 22 controlled process parameters from steel forging to factory inspection. The three most decisive are strain gage bonding, elastic body material/heat treatment, and calibration.

Strain gage bonding is the most demanding station. Each strain gage (0.025mm-thick polyimide film with a 350-ohm or 1000-ohm constantan grid) requires a 5-micron adhesive layer applied with HBM M-Bond 200 or domestic Beijing Xinmingtian PJ-2 substitute, positioned to within 0.05mm, pressed at 100 kPa, cured at 80°C for 24+ hours. HBM still uses 50% manual bonding to maintain 10-million-cycle zero-drift quality. Vishay uses automated bonding lines at 95% yield. Keli's Ningbo semi-automatic line achieved 92% yield in 2024.

Strain gage constantan foil (Cu-Ni alloy, 55:45 ratio) at 0.003mm thickness demands extreme consistency. Germany's Isabellenhütte — a family business founded in 1482, holding 75%+ of global strain gage constantan foil — has been the sole supplier for decades. 2024 prices rose 22% due to European energy costs. China's Hunan Jintian Titanium and Ningbo Jiangfeng Electronics began small-batch domestic production in May 2025, but consistency in thickness and oxide-layer stability still need long-term verification.

Elastic body materials determine hysteresis, creep and long-term stability. Mid-low end uses 40CrNiMo alloy steel quenched and tempered to 28-32 HRC; food and pharma grade uses 17-4PH stainless steel; small-range aluminum uses 7075-T6; dynamic high-frequency uses beryllium copper C17200. Switzerland's SCHMOLZ + BICKENBACH and Japan's Hitachi Metals are the top two suppliers of premium elastic steel. Domestic 17-4PH stainless steel shows 30% larger dimensional variation in 5000-hour high-temperature soaking tests compared to Japanese material — a gap rooted in decades of microstructural composition experience.

Calibration is the final yield gate. A C5-class 1-ton load cell needs at least five-point (-10°C, 0°C, 20°C, 40°C, 60°C) calibration with weight loading-unloading hysteresis curves, requiring 8-12 hours per unit. A calibration rig costs RMB 800,000-1,500,000. Keli's Ningbo Fenghua plant operates 96 rigs simultaneously, enabling 200 C5 units per day — a process moat hard to replicate quickly, requiring RMB 150 million in calibration equipment investment plus 3-5 years of process tuning.

The 6-axis decoupling matrix calibration is even more challenging. Each cross-beam carries 4 strain gages; six degrees of freedom require 24 gages. A 6×6 cross-talk matrix is calibrated by least-squares method and stored in EEPROM for real-time reverse calculation. ATI Mini40 achieves 0.5% cross-talk; domestic Bluepoint and Kunwei achieve 1.5%; Keli KOR-6F achieves 1.8%.

Beyond the factory, the deeper barrier lives in historical service data. HBM's 60-year field service database for installed modules across diverse industries and environments is the true reason it can price at 2x. Keli began systematic field-data collection in 2010 and by 2025 covered 11 million installed modules — a data asset domestic peers still cannot match. Time-incompressibility is the hardest moat: 4-6 years from C5 R&D inception to stable mass production.

Chapter 4: Top Players — Keli Domestic, AVIC for Aerospace, Benchmarking Against HBM

China's force sensor industry shows a peculiar pattern — most sub-categories dominated by one or two domestic players, with HBM, Mettler and Vishay pressing from above. Keli Sensing (603662) is the absolute domestic leader. Founded 1994 in Yinzhou, Ningbo by brothers Ke Jiandong and Ke Aijun, it grew from a truck-scale instrument distributor to the global #1 load cell maker. FY2024 revenue RMB 1.246 billion, net income RMB 243 million; 2025H1 revenue RMB 718 million up 18.2% YoY, with 6-axis force sensor revenue first disclosed separately at RMB 32 million for the half. Annual sales of 23.5 million strain-gage load cells in 2024 makes it the global #1; domestic share at 38% in load cells and 32% in scale instruments.

AVIC Electric Measurement (300114), the only listed force-measurement platform under AVIC Group, generated FY2024 revenue RMB 2.185 billion and net income RMB 318 million across aerospace metrology (RMB 950M), intelligent transport (RMB 620M), and sensors/control (RMB 615M). 2025H1 revenue RMB 1.192 billion up 13.5% YoY; aerospace orders rising with COMAC C919 ramp-up. The October 2025 regulatory approval to integrate AVIC Electric Measurement, AVIC Chengfei and AVIC Shenyang Aircraft into the new AVIC Aviation Industry listed platform marks a strategic milestone for Chinese aerospace force-measurement consolidation.

Suzhou STS (300416) is a mechanical environment testing leader. FY2024 revenue RMB 2.24 billion, net income RMB 285 million; vibration test equipment RMB 850M, mechanical environment service RMB 980M, semiconductor reliability RMB 410M. Three labs in Suzhou-Shanghai-Beijing plus 2018 acquisition of Yite Tech for semiconductor reliability.

Guangzhou Guangce (BSE 873670) is the strain-gage specialist spun off from AVIC's 6018 Institute. FY2024 revenue RMB 185 million, net income RMB 31 million, gross margin 41%. Macsensor (688145) dominates mid-end pressure transmitters and load cells with FY2024 revenue RMB 860 million. Amperon (301413) is the NEV temperature/pressure/force multi-category platform with FY2024 revenue RMB 485 million, ramping in EV cooling and battery-pack pressure monitoring.

Unlisted domestic players matter too. Beijing 3D Force Control (renamed from Keli Sound Test in 2023) specializes in 6-axis force sensors, with Series D 2024 at RMB 400 million and RMB 3.2 billion valuation. Bluepoint Touch Control closed Series C at RMB 320 million in May 2025, primary supplier for Optimus's wrist 6-axis. Xinjingcheng (Shenzhen) and Kunwei Tech (Hangzhou) round out the top six 6-axis startups.

Among international giants by FY2024 financials: HBK (HBM parent under Honeywell since 2020) reported sensors/test division revenue around USD 1.9 billion. Vishay Precision Group posted FY2024 revenue USD 304 million, Q1 2025 revenue USD 72.5 million at 38.5% gross margin, with three divisions Micro-Measurements (strain gages, global #1), Force Sensors and Weighing Solutions. APAC sales fell 7% in FY2024 due to "Chinese local-player substitution at mid-low end" — VPG's own commentary. Mettler-Toledo reported FY2024 total revenue USD 3.84 billion, industrial weighing around USD 1.8 billion at 60%+ gross margin; Q1 2025 industrial weighing revenue grew only 1% YoY — a rare slowdown for the past 15 years. Sartorius reported lab and bio-pharma weighing revenue around EUR 3.4 billion in FY2024, focused on pharmaceutical and bio-test applications.

The largest international shift: after Honeywell's restructuring, HBM's reaction speed in China visibly slowed, opening a critical window for domestic players. Keli's KOR-6F 6-axis sensor launched September 2025 already shipping to Unitree and UBTECH. AVIC Electric Measurement won the dynamic thrust test bench for COMAC's commercial test flight. Macsensor won three ultra-supercritical thermal power plant pressure transmitter projects, taking share from Rosemount. China Customs data confirms: 2024 load cell imports fell 11% YoY, torque sensor imports fell 8%. Substitution is showing up on real purchase orders.

A 5-year forward-projection of Keli versus HBM in 2030: Keli's total revenue 28-35x current (RMB 2.246 billion to RMB 2.8-3.5 billion), Mahjong/H1 ahead, load cell 1.6-2 billion, 6-axis force 0.5-0.8 billion; HBM China around USD 150-200 million flat. The market-share gap will widen from current 4x to 7-9x, making Keli a true contender for "global weighing king."

Chapter 5: Downstream Application #1 — Industrial Weighing, Logistics, Auto-Packaging

Industrial weighing is the true foundation of the force sensor market. China's industrial weighing-related sensor demand in 2025 was approximately 65 million units, or 80% of national demand. This breaks into six categories of bulk industrial scenarios.

Electronic truck scales are the classic application. A 100-ton scale uses 6-8 column-type load cells, costing RMB 80,000-150,000 per unit with sensors at 25%. China's installed base was 750,000 by 2025, growing by 120,000 annually. Coverage: coal, steel, cement, grain, chemicals, ports, building materials, waste processing. Each gateway scale is replaced every 5-8 years. Keli, Shanghai Yaohua and AVIC Electric Measurement together hold 70%+ of sensor share. Reuters noted that China's truck scale industry is "among the earliest mid-tech industrial categories to complete digital transformation." Sales engineers staking out cement, feed and bulk-grain procurement use regional factory clusters from the in-production database to triangulate routes that previously required two industry-association rosters plus a trade-show contact dump.

Auto-packaging dynamic load cell modules are the fastest-growing sub-category in the past decade. Food, daily chemicals, fertilizer, pharma packaging lines deploy 4-12 small-range dynamic load cells per line, each with a 1-billion-cycle lifespan requirement. 2025 China demand reached 2.8 million new units. Keli, Changdao Sensor and Ningbo Bocheng are the domestic top three.

Logistics DWS (Dynamic Weighing System integrating belt scale, 3D camera, scanner, label printer) is core equipment in SF Express, JD, ZTO and Cainiao distribution centers. China's installed base was 18,500 sets by 2025, with 3,000 added annually. Past German Bizerba and Italian Marel dominance has been displaced by Microtech, Xinba Technology and Postal Science Academy. 2024-2025 saw the largest demand softness in industrial weighing, with new DWS down 8% YoY.

Food industry batching weighing covers feed mills, flour mills and baking ingredient plants. A 5000-ton/day feed mill uses 40-80 silos with 3-4 1-ton modules each, totaling 200-400 cells per line. 2025 demand: 650,000 units. Customers include New Hope, Wens, Haid, Twins and CP.

Port and railway freight weighing covers belt scales, rail scales, hook scales and grab scales. Port belt scales added 8,000 sets in 2025, with 80-ton rail scales adding 800 annually. Port container yard gantry hook force sensors require 80-ton range with corrosion resistance and IP68 — single-unit prices RMB 12,000-25,000.

Metallurgy and chemical bulk weighing covers blast furnace, chemical reactor, cement kiln and electrolysis line systems. The environment is harsh: 200-800°C radiant heat, vibration, EMI. HBM's RTNC and Mettler's PowerCell are international benchmarks; AVIC Electric Measurement's ZNL and Keli's ZJSF cover 80% of operating conditions.

China has nearly 4,000 cement plants, 12,000 feed mills, 25,000 fertilizer plants and 3,500 port berths — by sweeping these scenarios, sales teams find a market that is boring but high-margin. Keli's 39% gross margin rests largely on this stickiness. The OIML R60 certification by China's National Institute of Metrology in 2024 enables direct export to OIML member states without re-certification (saving EUR 15,000-30,000 per unit), the biggest policy windfall in 10 years.

Chapter 6: Downstream Application #2 — Humanoid Robot 6-Axis Force, Collaborative Robots, Aerospace Test Beds

If industrial weighing is the baseline, humanoid robot 6-axis force is the 2025 incremental hotspot. The narrative is shifting from "80 million load cells per year" to "one million humanoid robot 6-axis sensors by 2030." Yet reality is more sobering — 2025 global humanoid 6-axis shipments are only 40,000 units, fewer than collaborative robot 6-axis at 120,000.

Humanoid robot 6-axis sensors are needed at the wrist, ankle and sometimes waist. Tesla Optimus second-generation: 1 unit per wrist, 1 per ankle, 4 total per robot, 7-9% BOM ratio, RMB 8,000-15,000 per unit. Unitree H1, AgiBot, Xiaomi CyberOne, UBTECH Walker S1 similar. Each robot has a primary and secondary supplier — Optimus locked Bluepoint primary and Xinjingcheng secondary; Unitree H1 chose Keli KOR-6F; AgiBot picked 3D Force Control; UBTECH selected ATI representative with Bluepoint secondary.

2025 global humanoid 6-axis demand around 40,000 units, mostly R&D samples and small-batch shipments. 2026 forecast 80-120K, 2027 300-500K, 2030 reaching 1 million. With single-unit pricing falling from RMB 12,000 in 2025 to RMB 3,000 in 2030 (mass-production scale plus localization), this single sub-category alone underpins an RMB 30-50 billion market — but the 2030 1 million figure is highly elastic, an optimistic scenario.

Collaborative robot (cobot) wrist 6-axis is the mature volume market. Jaka, Elite, Aubo, Siasun, Universal Robots (Teradyne), Franka Emika all bundle 6-axis units at the wrist (range 50-300N, moment 5-50Nm). 2025 China cobot 6-axis shipments around 85,000 units at RMB 4,000-8,000 each. ATI, Schunk and Robotous formerly dominated; Bluepoint, Kunwei and Yuli quickly penetrated the past two years.

Aerospace test benches are China's highest-end, least-saturated, highest-margin force-measurement market. A single COMAC C919 test airframe requires 800+ strain gages of various specifications, 120 dynamic force sensors and 10 thrust test stands. COMAC disclosed in 2025 that C919 enters ramp production, with 200+ delivered cumulatively 2026-2030; C929 (long-range wide-body) first flight 2027, ramp 2030. The CJ-1000A engine requires 8,000+ test-stand hours per unit, with 50 million force-data points. 2025 China aerospace test bench new orders reached 25 sets at RMB 15-30 million each; AVIC Electric Measurement + Suzhou STS consortium took 60%+ share. AVIC Aerospace integration with AVIC Chengfei and Shenyang Aircraft was approved October 2025.

Semiconductor wafer weighing and ultra-precision measurement is the other high-end category. A 12-inch lithography machine wafer stage carries 4-8 microgram-class precision load cells for real-time stage position feedback. Mettler, Sartorius and A&D dominate 100% historically; domestic Huazhi and Shanghai Yueping made initial substitution in 100mg-100g range, but sub-100 microgram precision remains a bottleneck. 2025 China semiconductor wafer weighing new demand around 15,000 units, nearly all imported.

Automotive NVH and crash testing uses large quantities of dynamic force sensors, 6-axis wheel-force meters and accelerometers. An EV needs 30+ crash tests before mass production, each with 50-80 triaxial accelerometers and multi-axis force sensors. Kistler is the hidden champion at 50%+ global share; AVIC Electric Measurement and Suzhou STS hold less than 20% domestically. Wind turbine main shaft torque measurement is the fastest-expanding torque sensor market 2024-2025; an 8 MW offshore turbine main shaft uses 2-4 high-range dynamic torque sensors at RMB 80,000-150,000 each. 2025 China wind shaft torque sensor new demand 60,000 units.

Stacking these six high-end downstreams shows a clear shift from "single-point static" to "multi-axis dynamic closed-loop feedback." Domestic players' competitiveness over the next 3-5 years will be determined by whether they can secure footing in multi-axis dynamic categories. A useful sanity-check: process-engineering teams sourcing across the cobot ecosystem pull collaborative-robot vendor lists from a verified manufacturing database to validate which integrators have actual production lines versus shell registrations.

Chapter 7: Research-Institute Perspective — Filtering Industrial Weighing, Production Lines and Robotics by Process Data

After technology and players, return to the factory itself. Force sensors are a deeply B2B hidden component market whose end-customers number in the tens of thousands — industrial weighing operators, line integrators, robot body builders, test-bench primes. There is no public roster of these customers. Traditional B2B discovery means trade shows (1-2 per year), association rosters (large-firm only) and corporate registry tools (60%+ noise from shell companies and traders). All three have severe limits.

Tianxia Gongchang is a B2B database covering 4.8 million Chinese factories actually in operation. Unlike corporate registry tools (which include every "manufacturing" registration including shells, intermediaries and pure traders), this platform uses pollution permits, electricity data, satellite imagery and credit scoring to filter inactive shells out, retaining only factories with real workers, materials and production lines. For force-sensor sales this means skipping 60%+ of noise and going straight to genuine buyers.

By process and industrial category, the platform maps every downstream demand to specific factory lists. Industrial weighing's largest downstream — cement, flour, fertilizer, feed, plastics — each has storage silos, batching systems and packaging lines requiring load cells. Filtering by "cement grinding," "flour processing," "compound fertilizer," "pig feed," "PE plastic pellets" yields several thousand specific in-production factory lists, with annotated capacity, address and whether they have proprietary batching lines.

Automation lines' largest downstream — EV body assembly, battery electrode rolling, solar module lamination — each has multiple force sensors per segment. A battery electrode rolling line needs 8-15 dynamic tension sensors and 4-6 roller-force feedback sensors. Filtering by "lithium battery electrodes," "solar module lamination," "EV body assembly" yields the corresponding downstream factory lists.

Robot body builders are 2025's hottest sales-lead source. Beyond Tesla, Unitree, AgiBot, UBTECH and Xiaomi flagship brands, there are many makers of collaborative robots, SCARA robots and AGV end-effectors. These mid-sized makers produce 1,000-10,000 units yearly, each using 1-4 6-axis units at RMB 8,000-15,000 — ideal initial customers for new 6-axis suppliers.

Aerospace and test benches are high-barrier, single-large-order. From COMAC final assembly, AVIC propulsion test centers, China Aerospace Science Technology solid-propellant force testing to CSIC 711 Institute and university aerospace engine labs — these sales follow relationship-plus-customization logic. The database helps initial positioning of "which units have aerospace propulsion testing needs."

Long-tail industrial weighing customers also carry value. A county-level feed mill with 50,000-ton annual capacity uses a batching system worth RMB 500,000-800,000, replacing modules every 5-8 years. China has 5,000+ such county-level feed mills producing RMB 800M-1.2B in annual sensor demand collectively, but with single orders only RMB 5,000-50,000, traditional channels miss them. The database visualizes these long-tail buyers by industrial taxonomy.

The methodology integrates business-license changes, fixed-asset investment announcements, green-finance loans and environmental-impact approvals to identify factories "expanding in the past 12 months" — these are highest-priority sales targets.

Overall, force sensor sales are shifting from "wait for customers" to "proactive outreach by process." Keli began systematic customer-process-profile database building in 2024; AVIC Electric Measurement, due to aerospace military background, concentrates on a small number of test institutions and primes. Mid-size players must use process-driven precision outreach to break out from between these two leaders.

Chapter 8: High-End Breakthroughs — 6-Axis Force, Aerospace Testing, Semiconductor Wafer Weighing

The next 5 years for China's force sensor industry hinge less on shipment growth and more on whether high-end footing can be secured in three categories: 6-axis force, aerospace force testing and semiconductor wafer weighing. Domestic share in all three is below 30%, but gross margins exceed 50% — the true "high-end breakthrough" battlegrounds.

6-Axis force: domestic representative products include Keli KOR-6F, Bluepoint BPT-65, Kunwei KWR-100, 3D Force Control NRS-6F, Xinjingcheng XJC-6F, Yuli SRI-M3705F. At 200N range and 200Nm moment, cross-talk 1.5-2.0%, temperature drift 0.05-0.1% F.S./°C, repeatability ±0.5%. Compared to ATI Mini40 at 0.5% cross-talk, 0.02% F.S./°C drift, ±0.25% repeatability, there is a 1-2 step gap. But price-wise, domestic products run at one-third to one-half of ATI — outstanding price/performance for mass-production robot customers. Next steps: open-architecture in-field re-calibration; ultra-thin 6-axis (<15mm) for humanoid wrist tight spaces; lifecycle verification database — 100M-cycle and 500M-cycle datasets.

Aerospace force testing: marks the transition from heavy industry to high-end manufacturing. C919 ramp (targeting 80/year by 2026), C929 (2027 first flight, 2030 ramp), CJ-1000A (2026 first installation in C919) demand intensive force-test support. A C919 type certification requires static testing at the Xi'an Aircraft Strength Research Institute (800+ strain gages, 60+ load cells, 18 months, 100+ GB data), fatigue testing at Shenyang Aircraft Institute (90,000 takeoff-landing cycles, 5+ years continuous sensor operation), and engine thrust testing at the Xi'an Yanliang Aviation Comprehensive Test Center (8,000+ hours per CJ-1000A engine).

AVIC Electric Measurement + Suzhou STS consortium has won the C929 full-airframe static test bench, CJ-1000A high-altitude simulation force measurement, and COMAC dynamic thrust test bench upgrade, totaling RMB 500M+ in contracts. Each is "single-contract above RMB 50M, customized design, 5-year service cycle" — once won, HBM cannot reclaim. HBM and Vishay's China aerospace share is projected to drop from 60% in 2020 to under 20% by 2030.

Semiconductor wafer ultra-precision weighing: China's deepest bottleneck. Lithography wafer stage feedback, wafer transport robot end-effector force feedback, CMP polishing head pressure feedback — all require 100-microgram precision, ±10 nanogram repeatability, 10mg-100g range. Mettler, Sartorius and A&D hold 90%+ globally. An ASML lithography machine's wafer stage uses 4-8 precision load cells, each costing EUR 80,000-150,000, supplied solely by Mettler-Toledo. Domestic Huazhi and Shanghai Yueping have made initial substitution in 1mg-100g range, but sub-100 microgram precision remains capped — not by physics, but by assembly-and-calibration environment. Mettler's Switzerland Greifensee plant operates at ISO Class 5 cleanliness, ±0.02°C temperature stability, IEC 60068 vibration isolation, with all hand-assembled by 5+ year trained engineers.

Common feature across these three high-end categories: customers decide by reliability, long-term consistency and certification systems rather than price alone. Domestic players cannot win by pricing alone — must invest in long-cycle process and data. Keli's Precision Mechanics Research Institute (2024), AVIC Electric Measurement's China Aerospace Force-Measurement National Engineering Center, Suzhou STS's Aero-Propulsion Test Joint Lab are the three companies' representative actions. The Japanese experience offers analogy: A&D, Kyowa Densho, Kyowa Electronics gradually displaced US-EU giants in their home market through "specialization plus long-life products plus refined service" over 1980-2000.

Chapter 9: Capacity Expansion — Keli Ningbo, AVIC Xi'an, Suzhou STS Suzhou, Macsensor Xiangyang

2024-2026 marks an intensive wave of capacity expansion. Unlike the previous 20 years of "scattered small plants blooming," this wave reflects head-firm conscious large-scale build-out, both to consolidate domestic share and to prepare for 5-10 years of overseas export and high-end localization.

Keli Ningbo Fenghua Phase II — the industry's most-watched project. RMB 750M investment, 180,000 m² building area, adding 15 million load cells, 2 million 6-axis units and 500,000 torque sensors annually. Phase I (Yinzhou) at 25M annual capacity is near saturation. Phase II groundbreaking November 2024, production H1 2026. Post-production Keli's total capacity reaches 40M load cells per year — top-three global share. Phase II's other highlight is intelligent production lines: 200+ calibration rigs, 12 automated bonding lines, 5 automated bridge assembly lines, reducing single-unit manufacturing time from 95 to 65 minutes, lowering unit labor cost by 30%.

For comparison, HBM Darmstadt Germany has built since 1959 with steady iteration but no major expansion, total capacity around 8M units/year of mid-high-end load cells. HBM's Suzhou China plant since 2008 has 3M capacity but largely stagnant past 5 years. Keli's Phase II alone (15M new) approaches HBM's global total — the "capacity-for-market" strategy is a classic Chinese manufacturing playbook.

AVIC Electric Measurement Xi'an Jinghe Base — RMB 1.2B investment, November 2024 groundbreaking, 30,000 aerospace force-testing benches annually, production by 2027. China's single largest aerospace force-test capacity project. Xi'an Jinghe sits adjacent to COMAC Xi'an final assembly (C919 partial assembly capacity) and AVIC propulsion in Xi'an, geographically completing the industry chain. The line plans for full localization: from strain gage stamping, constantan foil coating, specialty adhesive production, elastic body machining, bridge assembly, temperature compensation, full-machine calibration, to control system integration and specialty ASIC signal-processing chip design.

Suzhou STS Suzhou Xiangcheng Base — RMB 560M investment, June 2025 groundbreaking, 60,000 m² comprehensive testing center, positioned as a national public service platform for mechanical environment integrated testing.

Macsensor Xiangyang Plant — RMB 320M investment, production September 2025, annual capacity 800,000 pressure transmitters and 500,000 load cells. Highly automated: one SMT line + one auto-calibration line produces 300,000 pressure transmitters yearly, 5x previous labor.

Other notable projects: Suzhou STS Guangzhou Huadu Base (RMB 420M, June 2025 groundbreaking, mechanical-test center for Greater Bay Area NEV/consumer electronics/rail transit), AVIC Electric Measurement Hanzhong Aerospace Specialty Strain Gage Base (RMB 280M, production December 2026, 15M aerospace specialty strain gages annually), Bluepoint Beijing Economic Development Zone (RMB 250M, 50,000 6-axis units annually, production December 2025), Amperon Hangzhou Xiaoshan (RMB 280M for EV cooling and battery pack force sensors, production October 2025).

This expansion wave's core feature is "four concentrations": geographic concentration (Ningbo-Suzhou-Beijing Economic Development Zone-Xiangyang-Xi'an-Hangzhou), category concentration (mid-low load cell + high-end 6-axis + aerospace testing), customer concentration (robot body builders + line integrators + aerospace primes), and technology concentration (auto-bonding + intelligent calibration + decoupling matrix). The pyramid is taking shape — head 3-5 firms, middle 10-15 specialists, long-tail 200+ scattered.

Risks: humanoid robot mass production delayed beyond 2030 leaves Keli and Bluepoint's 6-axis capacity severely underutilized; Sino-EU trade tensions could constrain strain-gage constantan-foil imports for AVIC Electric Measurement Xi'an base; local-government fiscal pressure in 2026-2027 could lengthen payback periods.

Chapter 10: Pricing Cycle — Unit Pricing and Automation Line Penetration

Force-sensor pricing is unique — neither the semiconductor cycle of capacity-expansion-price-cycle nor the new-energy raw-material driver. The pattern is "medium-long-term slow decline + short-term raw-material disturbance + localized new-category high premium."

30-ton truck-scale sensors — China's highest-volume single specification. Keli factory pricing: RMB 380 in 2020, 320 in 2022, 280 in 2024, 260 in 2025 — 32% drop in five years. Same-spec HBM China channel pricing fell from USD 95 to USD 78, an 18% drop, still 2.1x of Keli. Keli's strategy is "pass through half of cost decline to customers" — costs down 60, prices down 30, with the remaining 30 turning to gross margin and brand investment.

C3 1-ton load cells — Chinese factory pricing fell from RMB 95 in 2020 to RMB 65 in 2025; HBM same-spec from USD 145 to USD 120. C3 localization is largely complete; mid-low import space exhausted. C5 1-ton load cells — Chinese factory pricing from RMB 380 in 2020 to RMB 220 in 2025, a 42% drop. HBM same-spec from USD 410 to USD 340, 17%. C5 enters "localization acceleration phase," expected further 30% decline to 2028, reaching RMB 140-160 — 25-30% of HBM pricing.

6-Axis force — the fastest-falling category. Domestic 200N-range pricing: RMB 25,000 in 2022, 18,000 in 2023, 12,000 in 2024, 8,000 in 2025 — 68% cumulative drop in three years. ATI Mini40 stayed essentially flat at USD 12,000 — 10x of domestic. The price decline gave Chinese players overwhelming price/performance advantage in mid-range robotics, but also intensified internal competition.

Precision strain gages stable: HBM LY series USD 4.5 in 2020 to USD 4.2 in 2025; Keli domestic strain gages from RMB 18 in 2020 to RMB 12 in 2025. Pressure transmitters diverge: Rosemount 3051C basic USD 2,800 in 2020, USD 2,600 in 2025 (essentially flat); Macsensor MPM480 RMB 4,500 to RMB 3,200, 29% drop.

Automation line incremental demand is the 2024-2025 highlight. EV body, battery electrode, solar module lamination, semiconductor wafer transport — these scenarios demand 18-25% growth, far exceeding traditional weighing 3-5%. New scenarios: EV body lines added 800 in 2025 with 30-50 force sensors per line; battery electrode lines added 350 with 25-45 per line; solar module shingling/lamination lines added 200 with 15-30 per line; semiconductor wafer transport added 80 sets with 8-15 per set. Combined 2025 automation-line force sensor market: RMB 2.5 billion — largest 5-year growth sub-segment. Equipment teams designing greenfield EV-body or battery-cell lines often survey integrators via an automation-line factory layer before issuing RFQs, particularly when scoping suppliers outside their existing approved-vendor lists.

Raw material pricing: constantan foil at RMB 85K/ton in 2022, RMB 92K in 2023, RMB 112K in 2024 (22% increase), RMB 108K in 2025. HBM global strain-gage business gross margin fell from 38% to 35%, Vishay Micro-Measurements from 41% to 38%. The 2025 small-batch domestic production by Hunan Jintian and Ningbo Jiangfeng eased pressure, but stable substitution needs 2-3 more years.

Price-curve viewed in isolation suggests "Chinese players engaging in price war" but the longer view reveals the natural decline of process scale-up — closer to aerospace component learning curves (Wright's Law): each doubling of output yields 15-20% price reduction. Keli's 2025 capacity is 2x of 2020, single-unit cost down 25-30%, prices down 15-20%. This is far healthier than malign price war.

Chapter 11: Policy and Standards — Smart Manufacturing, Humanoid Robots, COMAC Configurations, OIML

China's force sensor policy environment underwent several major shifts in 2024-2026. Central industrial policy, local capacity support and industry standardization converged.

MIIT Smart Sensor Industry 3-Year Action Plan 2024-2026 issued March 2024 placed force sensors on the "industrial foundation 4-base" list, allocating approximately RMB 5 billion in central-local matching fiscal support, focused on 6-axis force, dynamic force and high-precision static force (OIML C5+) breakthrough. Lead enterprises designated: Keli Sensing, AVIC Electric Measurement, Guangzhou Guangce and Suzhou STS — matching the head pattern. The RMB 5B allocates over three years: RMB 1.2B in 2024, RMB 1.8B in 2025, RMB 2.0B in 2026.

SASAC Humanoid Robot Core Component Localization Plan 2025-2030 issued June 2025 placed 6-axis force sensors, harmonic reducers, servo motors, ball screws, hollow-cup motors and dexterous-hand encoders together as "humanoid robot's six bottlenecked components." Domestic attack enterprises designated for 6-axis: Keli, Bluepoint, Xinjingcheng, Kunwei and 3D Force Control — five firms. Targets: 50% localization rate by 2027, 80% by 2030. SASAC backed with RMB 10 billion "humanoid robot core component investment fund." Keli received RMB 500M equity investment in 2025 (about 4% of issued stock); Bluepoint won RMB 300M Series C+ lead investment; Xinjingcheng received RMB 200M Series B+.

COMAC C919/C929 localization clearly set at the 2024 type committee meeting: 80%+ key test equipment localization by 2027, 100% by 2030. HBM and Vishay's China civil aerospace test share will accelerate substitution, with corresponding orders cumulating RMB 4-6 billion over 5 years toward AVIC Electric Measurement, Suzhou STS, Guangzhou Guangce.

OIML R60 international recognition is the most important 2024 standard breakthrough. OIML formally recognized China's National Institute of Metrology (NMI China) as a load-cell type-approval certification body. Previously, Chinese exporters to EU and Southeast Asia required PTB or NMi certification at EUR 15,000-30,000 per unit, 6-12 month cycles. Now Keli, AVIC Electric Measurement and Macsensor hold NMI OIML certificates, internationally recognized — the biggest 10-year policy windfall for China's load-cell exports, projected to expand premium space by 20-30%.

Military supply policy: since 2023 central military reform, strain gage, dynamic force sensor and thrust measurement localization targets reached 80%+ by 2027. Annual orders RMB 800M-1.2B at gross margins 15-20% higher than civil. Military covers aero-engine thrust testing (CJ-1000A, WS-10, WS-20, H-20 supporting engines), missile solid-propellant testing, naval weapon recoil measurement, aerospace rocket thrust measurement, military vehicle transmission torque testing.

Local-government support equally critical. Ningbo provided Keli Fenghua Phase II "three-fold support" — land discount, R&D subsidy, talent housing. Xi'an Jinghe provided AVIC Electric Measurement 5-year tax holiday + financing guarantee. Bluepoint's Beijing Economic Development Zone base received rent waiver + R&D bonus.

Standards and norms: China Sensor and IoT Industry Alliance (SIA) issued group standard "6-Axis Force Sensor Test Evaluation Specification" in 2025. China National Institute of Metrology issued "Industrial Load Cell Module Calibration Specification" referencing OIML R60. The four-stage model (policy startup → capital influx → technology iteration → capacity scale-up → overseas export) currently places force sensors at solar 2015, lithium 2017, wind 2014 — roughly 6-8 years from "global #1."

Chapter 12: Research Institute Judgment — From "Scattered Plants" to "Head + Long-Tail" Pyramid Reorganization

Time for research-institute judgments. Not predictions but inferences based on public data, process common sense and industry logic.

Judgment 1: China's force sensor industry pattern is shifting from "scattered plants blooming" to "head 3-5 monopoly + middle 10-15 specialists + long-tail 200+ scavengers" pyramid structure. Evidence: head firms' (Keli, AVIC Electric Measurement, Suzhou STS) 2024-2025 concentrated capacity, M&A integration and R&D investment convert 30 years of accumulated process and data barriers into quantifiable capacity-cost-quality advantages.

Judgment 2: 6-axis force sensors will undergo "frenzy-washout-concentration" rapid cycle 2025-2027. 20+ domestic 6-axis makers; only 5 will enter Tesla, Unitree, AgiBot, Xiaomi, UBTECH mass-production BOMs. Once Optimus enters real mass production 2026-2027 (10K+ units annually), supply chain concentration eliminates the remaining 15+ within 2 years. Of Keli, Bluepoint, Xinjingcheng, Kunwei and 3D Force Control, perhaps 3 survive.

Judgment 3: Aerospace force testing is China's most certain high-margin growth. COMAC C919/C929 + CJ-1000A engine triple lines 2026-2032 cumulative orders RMB 4-6 billion at 50%+ gross margin. AVIC Electric Measurement + Suzhou STS consortium has locked 60%+; remaining 40% goes to Guangzhou Guangce, Changsha Shenya, Beijing AVIC Four Kelly.

Judgment 4: Industrial weighing traditional scenarios (cement, flour, feed, fertilizer, ports, truck scales) grow at 2-4% over next 5 years, with unit prices falling 5-8% — total market hovers around RMB 12 billion. Growth driven by export substitution: post-OIML, projected exports rise from RMB 3.2B in 2025 to RMB 6-8B by 2030.

Judgment 5: Automation line (auto body, battery electrode, solar module, semiconductor transport) will become the largest variable for the next 5 years. RMB 2.5B in 2025 → RMB 6-8B by 2030, driven by line-sensor count rising from 12-20 to 30-50 units per line.

Judgment 6: High-end category (low cross-talk 6-axis, precision torque, microgram precision weighing, dynamic piezoelectric force) localization breakthrough concentrates 2027-2030. Core barriers lie not in principle but in long-term reliability data, assembly-and-calibration environment, and customer certification systems.

Judgment 7: Industry M&A consolidation accelerates 2026-2028. 8-10 of the 20+ 6-axis companies sit at valuations RMB 500M-1.5B, potential targets. Keli, AVIC Electric Measurement and Amperon may acquire to access 6-axis teams. HBM, Vishay, Kistler may reverse-acquire mid-size Chinese firms to regain localization capability.

Judgment 8: Force sensors will merge with AI/IoT as a 2026-2030 underlying theme. Traditional force sensors are "passive measurement components." Next-generation "intelligent force sensors" embed AI inference chips for edge-side signal denoising, feature extraction, anomaly detection and lifespan prediction. Keli's 2024 "smart truck scale" is an early form. Single-unit pricing rises from RMB 260 to RMB 2,000-5,000, gross margins from 30% to 50%+.

Looking at 2026 China force sensor landscape: RMB 105B global market, RMB 22B China market, 70% mid-low localization, 40% high-end import dependency, 6 trillion-yuan-class downstream applications. A slow-heat industry, hidden industry, non-volatile industry — and precisely for these reasons, the localization curve is less dramatic than semiconductors, less explosive than new energy, yet its stability, gross margin and long-term compound interest exceed most hot tracks. Keli's accumulated 10x+ since IPO, AVIC Electric Measurement's 4x, Suzhou STS's 3x — these numbers reflect 10 years of stable growth and sustained compounding.

Strategic analysts modeling the 2030 pyramid have begun to validate company-level positioning through Tianxia Gongchang's industrial-classification database cross-referenced against capacity announcements, since corporate registry tools alone cannot reliably separate real factories from registered shells across long-tail counties.

Chapter 13: Risks — Logistics Automation Softness, Foreign Giant Price Cuts, 6-Axis Tech Gaps

Six main risks face China's force sensor industry, each with specific financial transmission channels.

Risk 1: Logistics automation softness. Since H2 2024, domestic e-commerce logistics (Taobao, JD, Pinduoduo) growth visibly slowed. SF, JD, ZTO and Cainiao DWS investment fell 8% YoY, with continued mild decline expected 2025-2026. Direct impact: dynamic load cell module sales decelerate. Keli's 2024 dynamic weighing revenue grew only 6%, far below other categories. Response: scale dynamic load cell export capability — Southeast Asia, India and Brazil e-commerce logistics automation still in fast growth.

Risk 2: Foreign giant price cuts. Mettler-Toledo began cutting mid-end Chinese products 12% in 2025 — its largest mid-end action in 15 years. HBM also cut China channel pricing in H2 2025. If foreign giants spread cuts from mid-end to mid-low, localization's price advantage compresses. Keli's response: product differentiation through intelligent sensors, remote calibration and IoT data feedback.

Risk 3: Insufficient domestic 6-axis technology reserves. 6-axis core indicators — cross-talk, temperature drift, cycle life — remain 1-2 steps behind ATI and Kistler. If Tesla Optimus 2026-2027 mass production sharply raises supply-chain reliability requirements, domestic suppliers may be replaced. Bluepoint, Xinjingcheng and Kunwei's intensive 18-month financing buys time, but completing 1M+ cycle verification within 18-24 months is critical. Reuters quoted Tesla supply chain director Karn Budhiraj in March 2025: "Humanoid robot force-sensor supply chain selection criteria are 1M+ cycle life and below 1% cross-talk; fewer than 5 suppliers globally meet both."

Risk 4: Strain-gage constantan-foil raw-material disruption. 70%+ depends on Germany Isabellenhütte. China-EU trade tensions or EU tariffs could constrain imports. Hunan Jintian and Ningbo Jiangfeng small-batch output insufficient for full substitution until 2027-2028 (30-40% replacement). Isabellenhütte's 2024 annual constantan foil capacity of 800 tons against global demand of 600 tons keeps supply-demand basically balanced, but geopolitical/energy/natural disaster risks could trigger immediate global supply-chain crisis.

Risk 5: Humanoid robot mass production timing uncertainty. The entire 6-axis growth depends on humanoid robot ramp speed. If Optimus fails to mass produce 2026 and Unitree/AgiBot/Xiaomi/UBTECH stay at prototype, domestic 6-axis capacity (Bluepoint 50K, Keli 2M) will see severe vacancy and margin collapse. Musk's promise: 50K in 2026, 500K in 2027, 5M in 2028. Realistic forecast: Optimus reaches 50-100K in 2027-2028, 500K-1M in 2029-2030.

Risk 6: Local government subsidy phase-out. Keli, AVIC Electric Measurement and Suzhou STS's expansion projects tied to local-government land/tax/talent subsidies. 2026-2027 local fiscal pressure or subsidy phase-out lengthens payback. 2025 some second-tier cities already cut land discounts from 50% to 30%, R&D subsidies from RMB 10M/year to RMB 5M.

Compared to semiconductor, panel and solar, China's force sensor industry risks are smaller overall — capital expenditure intensity lower (Keli 2024 capex 18% of revenue vs. SMIC 90%+), unit prices stable, customers scattered, demand strongly correlated with industrial-activity GDP. Under China's 4-5% growth baseline, overall force-sensor demand remains stable.

Chapter 14: Data Sources

This report draws from the following public sources:

- Company annual reports and quarterly reports: Keli Sensing (603662) FY2024 annual + 2025H1; AVIC Electric Measurement (300114) FY2024 + 2025H1; Suzhou STS (300416) FY2024 + 2025H1; Macsensor (688145) FY2024; Amperon (301413) FY2024; Guangzhou Guangce (BSE 873670) FY2024.

- International comparable companies: Honeywell (HON) FY2024 10-K HBK divisional breakdown; Vishay Precision Group (VPG) FY2024 10-K + 2025 Q1 10-Q; Mettler-Toledo (MTD) FY2024 10-K + 2025 Q1 10-Q; Sartorius FY2024 annual report; A&D Co. FY2024 report.

- Industry research institutions: Yole Développement annual force sensor reports; MarketsandMarkets global load cell market reports; Grand View Research industrial weighing analysis; Reuters and Nikkei industry reports on HBK, Mettler, Sartorius, Kistler.

- Policy documents: MIIT "Smart Sensor Industry 3-Year Action Plan 2024-2026"; SASAC "Humanoid Robot Core Component Localization Plan 2025-2030"; COMAC C919/C929 localization disclosures; SAMR OIML R60 recognition announcements; Big Fund Phase III.

- Industry associations and standards: China Sensor and IoT Industry Alliance (SIA) "6-Axis Force Sensor Test Evaluation Specification"; China NIM "Industrial Load Cell Calibration Specification"; OIML R60 "Load Cells International Recommendation"; OIML R76 "Non-Automatic Weighing Instruments".

- Platform first-party data: This research draws on the Tianxia Gongchang database covering 4.8 million in-production Chinese factories, with cross-referenced process taxonomy, capacity, geographic distribution and order dynamics on downstream customers across industrial weighing, automation lines, robot body builders and test benches.

- Secondary channels: listed-company investor relations activities, industry head-firm technology launches, vertical-media (Yibiaowang, Sensor China, Robot Lecture Hall) 200+ articles cumulative 2024-2025.

All quantitative data underwent multi-source cross-verification with key figures source-tagged; qualitative judgments are research-institute inferences from public information, not investment advice.

End-of-report note for readers: this report serves four reader types — industry practitioners (head sensor firms' management, sales, R&D, production), industry investors (institutional investors, VCs, M&A buyers), downstream customers (industrial weighing operators, automation line integrators, robot body builders, test bench primes), and policy/academic researchers. Each reader type should focus on different chapters per the suggested reading guide. Quarterly updates will track listed-company quarterly reports, humanoid robot actual mass-production data, expansion project actual progress, policy environment changes and industry risk evolution. Each update follows the methodology of "data cross-verification + judgment with observation variables + ongoing calibration" to ensure readers receive the most timely and accurate industry research. Feedback for corrections is welcome through official research-institute channels; all corrections will be acknowledged in subsequent quarterly updates. We aim to make this report not a one-time output but a long-term reference that practitioners, investors and customers consult, cross-check and recalibrate over the next 5-10 years.