Chapter 1. Industry Overview: From Boiler-Room Auxiliary to AI-Era Heat Hub

For the past thirty years, the heat exchanger has been treated in China as the silent auxiliary next to the boiler. It does not carry the rated power placard of a compressor, nor the unit price of a pump. It is a stack of thin metal plates, a tube bundle, or a plain vessel that quietly transfers heat from one fluid to another. Because of that silence, the entire market has long been underestimated, sidelined, and viewed as an appendage of heavy machinery.

By 2026 that picture is being turned upside down. The first driver is the energy mix; the second is computing power. Energy transition has rewritten heat-exchanger demand across petrochemicals, chemicals, power and HVAC, with sharper requirements on efficiency, pressure and corrosion resistance. The compute explosion has dragged a few sheets of stainless steel out of the boiler room and into the racks of AI data centers, making them a core component of modern thermal infrastructure. Together those two forces have, in 2026, finally pulled the heat exchanger from the wings to the front of the stage.

Per industry consultancies, the China heat exchanger market reached roughly RMB 970–1,000 billion (about RMB 100 billion) in 2024 and grew about 7–8% in 2025 to cross RMB 105 billion. Shell-and-tube remains the single largest sub-segment, accounting for about 45–50%; plate heat exchangers account for about 28–30%; air coolers, plate-fin, microchannel and double-pipe together account for about 20%. Behind the static structure lies a dynamic one. Shell-and-tube's downstream — petrochemicals, coal-to-chemicals, power and the like — contributed more than seventy percent of its volume, yet capital expenditure in those four industries stayed flat in 2025–2026, pulling shell-and-tube growth down to 3–4%. Plate heat exchangers, by contrast, accelerated to above 12% thanks to HVAC, heat pumps and data-center liquid cooling. Plate-fin and microchannel — historically used in radiators, off-road equipment and aftercoolers — now grow above 20% on the back of NEV thermal management and AI data centers.

Globally, market research houses estimated 2025 world heat-exchanger sales at about USD 18.7 billion, growing 8.1% year on year. China's RMB 970 billion converts to USD 135–140 billion at the year's average exchange rate, accounting for over forty percent of the global market by certain segment counts. China is both a demand center and a production base, with capacity concentrated in Jiangsu, Shandong, Liaoning and Jilin.

This chapter sets the macro picture. The next thirteen chapters walk through products, process barriers, vendors, downstream demand, capacity, pricing, policy and risks. Our verdict: by 2029 China's heat-exchanger market will cross RMB 150 billion, with data-center liquid cooling, NEV thermal management and heat pumps contributing more than two-thirds of the incremental volume. The exchanger is no longer just a heavy-machinery accessory — it has become the cooling backbone of advanced manufacturing.

A clarification on scope. Many reports lump heat exchangers together with pressure vessels, towers and reactors to claim larger numbers; this paper counts only the equipment whose main function is heat transfer, excluding storage tanks, towers, reactor internal coils and double-pipe-only modules. The resulting number is smaller but more faithful to actual transactions.

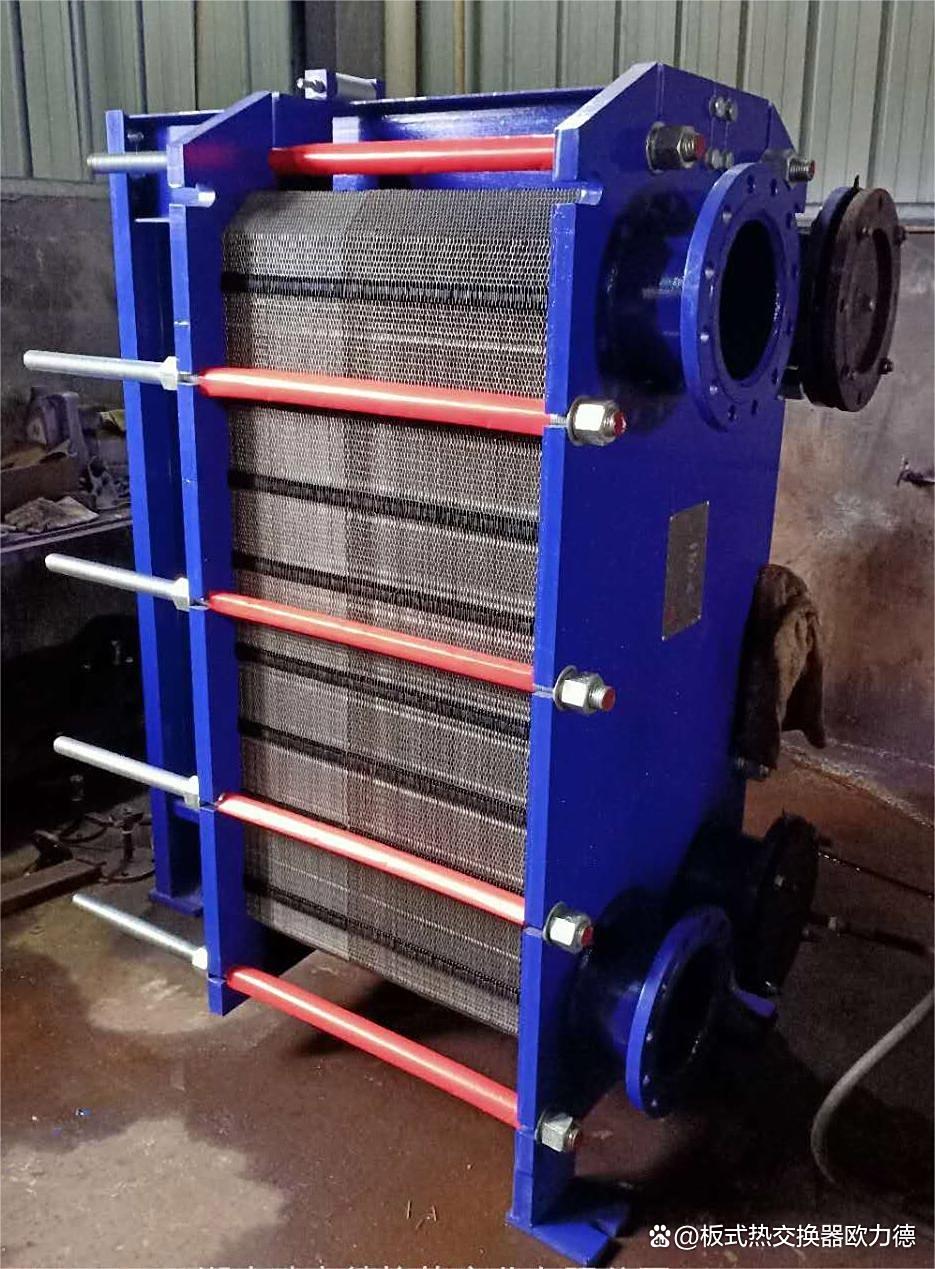

Chapter 2. Product Taxonomy: Plate, Shell-and-Tube, Microchannel and the Forgotten Middle Forms

The textbook split — plate versus tube, single-phase versus two-phase, sensible heat versus latent heat — is not the most useful for industrial research. This paper groups industrial heat exchangers into five families by process and downstream.

The first family is plate heat exchangers (PHEs). Two fluids cross over corrugated metal sheets. Three process routes coexist: gasketed plate (sealed by rubber gaskets, easy to clean, used in HVAC, chemicals, food and beverage); brazed plate (BPHE) with copper or nickel braze, used in refrigeration, heat pumps and CDU for data-center liquid cooling; and fully welded plate with laser or roll welding, used in high-temperature high-pressure petrochemical and metallurgical service. Market share is roughly 60-20-20 across the three routes in China, while growth rates run in reverse — BPHE and fully welded both grow above 15% per year.

The second family is shell-and-tube heat exchangers (STHE). A tube bundle inside a shell, with the two fluids running on either side. Variants include fixed tube sheet, floating head, U-tube and packed-shell designs. STHE dominates high-pressure, high-temperature service such as petrochemicals, coal-to-chemicals, nuclear secondary loops and power-station bypasses.

The third family is microchannel. The classic round tube is replaced by sub-millimeter flat tubes sandwiched between fins. The format originated in residential air conditioning, then was promoted to industrial use by NEV battery cooling plates and data-center cold plates. China's microchannel market was about RMB 2.1 billion in 2024, growing 16.67% YoY — the fastest among sub-segments.

The fourth family is plate-fin. Alternating plate and fin sheets brazed into a compact metal brick. Historically used in aerospace, air separation and air-compressor aftercooling, the plate-fin format is being rediscovered for NEV battery cooling and liquid-cooled data centers. Hongsheng Co. is a domestic leader, an aluminum plate-fin pioneer that now supplies Atlas Copco, Siemens, Sany and Weichai, and entered data-center liquid cooling via a 2024 joint venture.

The fifth family is air coolers. Air replaces water as coolant, blown by axial fans over finned tubes. Air coolers are mandatory in water-scarce sites such as refineries, coal-to-chemicals plants and dry-cooled power stations. Harbin Air Conditioning Co., Ltd. (Hakong) is the longstanding domestic leader.

Two often-ignored middle forms also deserve mention: heat-pipe heat exchangers and evaporative-spray heat exchangers. Both are smaller in volume but matter for waste-heat recovery and water-electric efficiency.

What truly matters is the structural shift in incoming order mix. A sample of large-EPC tenders in H2 2025 shows that fully welded plate and brazed plate together rose from under 10% to about 22% of high-value orders, the steepest decade-long share migration. The logic is simple: many jobs a traditional shell-and-tube can do, a plate cannot; but high-efficiency compact jobs the plate can do, the shell-and-tube almost cannot.

Chapter 3. Process Barriers: Plate Stamping, Brazing, Large-Scale Manufacturing and Rare-Metal Metallurgy

The fastest way to understand localization is to break the process into four core barriers.

The first is plate stamping. PHE plates are typically 0.4–0.8 mm thick, with chevron, wavy or dimple patterns pressed into the sheet. The shape directly determines heat-transfer coefficient and pressure drop. Stamping a 0.5 mm sheet into a complex 3D pattern while keeping geometric consistency across tens of thousands of plates demands top-tier tooling. China has long relied on German SCHULER and Austrian ANDRITZ presses at several-million-RMB price tags. Domestic substitutes from Jiangsu and Jilin have brought the unit price to under half, but tool life is only about 60% of imports — the bottleneck on further plate-cost reduction.

The second is brazing. BPHE plates must be brazed in vacuum furnaces using copper or nickel filler. Temperature gradient, hold time and vacuum profile dictate seam quality and pressure rating. A qualified vacuum brazing furnace costs over RMB 10 million; fewer than ten domestic firms own ten or more such furnaces. SWEP, owned by Dover, operates five production sites globally — two in Asia — and shipped over 3.5 million BPHE units worldwide in 2023. Chinese makers have raised single-unit pressure rating from 25 bar to 50 bar over the past five years, matching SWEP, Alfa Laval and Danfoss, though per-line output is still 30–40% of SWEP's.

The third is scale. Once shell-and-tube exceeds 3,000 sqm of single-unit heat-transfer area, with tube sheet over 300 mm thick and bundle weight over 100 tons, manufacturing difficulty rises geometrically. The key processes — thick tube-sheet forging, deep-hole drilling, tube-end expansion and welding, full-unit hydrostatic test — limit qualified suppliers to under twenty firms in China. Shuangliang Eco-energy, Sifang Cryogenic, Ruixing Group and Lanshi Heavy each shipped representative large units in 2025. Shuangliang's 2025 annual report shows full-year revenue of RMB 7.565 billion, energy-saving segment revenue of RMB 2.723 billion with gross margin up 0.92 ppt to 27.72%; Sifang's 2025 revenue was RMB 1.69 billion.

The fourth is rare and special-metal metallurgy. Heat exchangers run on more than carbon and stainless steel — they also use titanium, zirconium, nickel-based alloys, duplex stainless and Hastelloy in highly corrosive service. Titanium is especially critical. As of early 2026, TA1 titanium plate 1–3 mm trades around RMB 90/kg; TC4 5–10 mm trades at RMB 150–155/kg. Titanium prices have held steady through 2024–2026; no chronic shortage, although sponge titanium can be pinched by aerospace orders in certain windows.

Of the four barriers, plate stamping and brazing make the heart of the PHE; scale is the heart of STHE; rare-metal metallurgy is a shared bottleneck across all severe-corrosion applications. Chinese vendors have caught up to within touching distance on the first three; the fourth runs neck and neck with foreign players.

Chapter 4. Major Vendors: Domestic Camp Versus the Four Foreign Giants

The Chinese heat-exchanger industry has an unusual feature: foreign giants and domestic champions rarely fight head-on in the same lane; they hold complementary positions.

Foreign side. Alfa Laval is the unchallenged leader. The Lund, Sweden–based firm reported SEK 69.674 billion (about EUR 6.6 billion) of revenue in 2025, up 8% YoY, with a record full-year sales and earnings. Its line spans gasketed PHE, fully welded PHE, Compabloc, AlfaQ, spiral and traditional shell-and-tube. Manufacturing or service hubs exist in Kunshan, Shanghai, Qingdao and Suzhou. In 2025 Alfa Laval committed to phase Compabloc standard plates over to low-CO2 stainless steel, targeting full coverage by early 2026.

Kelvion ranks second. Spun out of GEA in 2015, it operates two main China sites — Wuhu (shell-and-tube and PHE) and Changshu (air coolers). The five largest manufacturers including Kelvion contribute about 35% of the Asia-Pacific shell-and-tube market in 2025; China contributed over USD 1.1 billion of revenue, leading the region with about 44.1% share.

Third, Tranter, a US-origin brand owned by Alfa Laval, focuses on gasketed and fully welded PHE for refinery and power replacement markets.

Fourth, SWEP, Sweden-born and US-owned via Dover since 2004, focuses exclusively on BPHE. It operates five global sites and shipped over 3.5 million units in 2023.

Danfoss is a Denmark-based diversified player; in 2025 H1 it reported about USD 5.5 billion of group revenue. In May 2025 it launched the H48T-CH series brazed CO2/water exchanger for transcritical refrigeration.

Domestic side. The first-tier players include: Yuanda Group (unlisted, the leading PHE-plus-absorption-chiller integrator), Sipingshi Juyuan Hanyang (Sino-German JV, China's first state-level "Little Giant" PHE firm, with annual PHE plate capacity over one million sqm), Lanshi Heavy (SOE with PHE and microchannel exposure to controlled-fusion projects), Sifang Cryogenic (Jiangsu listco, RMB 1.69 billion revenue in 2025), Ruixing Group (Shandong veteran for shell-and-tube), Shuangliang Eco-energy (RMB 2.723 billion of energy-saving revenue in 2025), Hongsheng Co. (aluminum plate-fin leader, H1 2025 net income RMB 46 million, up 49% YoY, entered data-center liquid cooling via 2024 JV with Hexin Precision), Epsteam, Hakong (Harbin Air Conditioning Co., Ltd., the long-standing air-cooler leader) and Ningbo Halle.

Stacking the two camps, an interesting picture emerges. In residential and commercial HVAC PHE, domestic players have squeezed the four foreign giants down from near 70% in 2015 to about 35% in 2025. In industrial BPHE, SWEP, Alfa Laval and Danfoss still hold above 50%. In fully welded PHE, Alfa Laval Compabloc and domestic Shuangliang/Sifang are roughly even. In large shell-and-tube, domestic localization has hit about 80% in refinery and coal-to-chemicals projects. In air coolers, Hakong alone holds over half. In plate-fin and microchannel, domestic vendors lead, foreign brands trail.

Chapter 5. Downstream Group One: The Three Heat-Density Gaps of Chemicals, HVAC and Data-Center Liquid Cooling

Downstream demand cannot be lumped as a single block. We compare heat-exchanger demand intensity per unit of GDP — what we call the heat-density gap — across three downstream tracks.

Group one is chemicals and petrochemicals. It is the largest and most mature, contributing about 30% of 2025 demand. Ethylene, PTA, polyethylene, polypropylene, caustic, soda ash, calcium carbide, fertilizers — almost every process unit needs at least one heat exchanger. A one-million-ton ethylene project's heat-exchanger package can exceed RMB 1 billion. Yet in 2025–2026, new PTA, PE and caustic capacity addition slowed; shell-and-tube growth fell to 3–4%. The structural opportunity lies in retrofit: replacing traditional shell-and-tube with Compabloc-class fully welded PHE saves 60% footprint and doubles heat-transfer coefficient.

Group two is HVAC. It contributed about 18% of 2025 demand. Commercial central chiller plants, ground-source heat pumps, air-source heat pumps, urban heating substations, and integrated complex HVAC systems are the natural habitat of plate heat exchangers. The April 2025 NDRC document calling for a national heat-pump action plan ((Fa Gai Huan Zi (2025) No. 313) named new heat exchangers a priority. Heat-pump industry revenue grew from about RMB 8 billion in 2014 to about RMB 33 billion today, 17%+ CAGR. Penetration in building heating remains below 5%; industrial heat pumps account for less than 1% of industrial heat — vast headroom.

Group three is data-center liquid cooling. This is the most aggressive incremental track, nearly doubling each year. The China liquid-cooling server market was about USD 2.37 billion in 2024, with 46.8% CAGR projected through 2029 to USD 16.2 billion. China's 2025 liquid-cooling server market may exceed RMB 29 billion, surpassing RMB 40 billion by 2027. Within cold-plate liquid cooling systems, the CDU plus liquid manifold combined account for about 45% of cost — CDU alone about 25% — and the BPHE is the heart of the CDU.

Data-center waste-heat recovery is another emerging downstream. A 2025 SWEP case shows BPHE used to channel waste heat from data-center coolant into a city heating network, turning a data center into both a power consumer and a heat supplier.

Chapter 6. Downstream Group Two: NEV Thermal Management, Energy Storage and Charging Piles

The NEV thermal-management envelope is far broader than that of internal-combustion vehicles. ICE thermal management covers the radiator, evaporator and condenser — about RMB 2,000 per vehicle. NEV thermal management adds battery cooling, motor cooling, electronics cooling, cabin AC and heat-pump heating — about RMB 6,400 per vehicle, roughly three times the ICE figure. Within that, plate exchangers and microchannel exchangers are the second-largest value bucket, behind only electronic water pumps and cooling plates.

Among Chinese suppliers, Sanhua Intelligent Controls leads in electronic expansion valves and integrated thermal-management modules — global number one in both. Yinlun Co. focuses on heat exchangers and bundles PHE, multi-way valves and pumps into integrated systems for OEMs. Nabaichuan focuses on microchannel cold plates.

Global NEV thermal-management revenue is projected at about RMB 87 billion in 2025; China's automotive thermal-management industry is projected at RMB 149 billion in 2025, with NEV accounting for 59.3% of the domestic figure.

Energy storage and charging piles are two further small-form factors. A 300 kWh commercial ESS cabinet's combined cold plate and PHE bill comes in around RMB 10,000–20,000; per-GWh storage thermal cost runs RMB 50–80 million. Mega-power liquid-cooled supercharger modules embed BPHEs and liquid-cooled connectors, with per-unit thermal cost of RMB 6,000–8,000.

NEV plus storage plus charging together total about RMB 23–26 billion of heat-exchanger demand in 2025, nearing a quarter of the whole industry. Three new requirements emerge: extreme compactness (plate thickness from 0.5 mm to 0.3 mm), automotive-grade reliability (vibration, salt spray, humid heat, thermal cycling), and faster iteration (OEM model cycles down from five years to one or two).

Chapter 7. Platform View: Mapping the Heat-Exchanger Supplier Universe

A formal note on our platform. Tianxia Gongchang is a B2B platform covering about 4.8 million active factories in China; its mission is to help upstream salespeople, traders and industry researchers find qualifying factory customers fast. Compared with the better-known Qichacha and Tianyancha, our differentiator is not on aggregating business-registry data. Those tell you a company's registered capital and legal representative; our platform tells you whether the company is a real factory, what products it makes, and which downstream it serves.

Within the heat-exchanger industry, our platform has identified about 12,000–13,000 entire-machine manufacturers, concentrated in Jiangsu, Shandong, Liaoning, Jilin, Shanghai, Guangdong, Zhejiang and Anhui. By process: about 6,400 plate-heat-exchanger makers, 4,800 shell-and-tube makers, 1,200 microchannel and plate-fin makers, 600 air-cooler and cooling-tower makers, and 200 heat-pipe and evaporative-spray makers. Out of more than 30,000 entities whose registered scope lists heat exchanger, only about 40% are true entire-machine factories.

Around that pool, our platform offers three filter dimensions: by process (gasketed, brazed, fully welded, fixed tube sheet, floating head, U-tube, microchannel, plate-fin, air cooler), by downstream (petrochemicals, coal-to-chemicals, power, HVAC, refrigeration and cold chain, NEV, data center, energy storage, hydrogen, food and beverage, pharma, marine, nuclear), and by region down to city level (Siping for plate, Jiangyin for shell-and-tube, Wuxi for plate-fin, and so on).

If readers want to search directly on our main site, the following entry points are available — all under the ?q= URL convention: plate heat exchanger (https://www.tianxiagongchang.com/search?q=plate%20heat%20exchanger), brazed plate heat exchanger (https://www.tianxiagongchang.com/search?q=brazed%20plate%20heat%20exchanger), gasketed plate heat exchanger (https://www.tianxiagongchang.com/search?q=gasketed%20plate%20heat%20exchanger), fully welded plate heat exchanger (https://www.tianxiagongchang.com/search?q=fully%20welded%20plate%20heat%20exchanger), shell and tube heat exchanger (https://www.tianxiagongchang.com/search?q=shell%20and%20tube%20heat%20exchanger), fixed tube sheet heat exchanger (https://www.tianxiagongchang.com/search?q=fixed%20tube%20sheet%20heat%20exchanger), floating head heat exchanger (https://www.tianxiagongchang.com/search?q=floating%20head%20heat%20exchanger), U tube heat exchanger (https://www.tianxiagongchang.com/search?q=U%20tube%20heat%20exchanger), microchannel heat exchanger (https://www.tianxiagongchang.com/search?q=microchannel%20heat%20exchanger), plate fin heat exchanger (https://www.tianxiagongchang.com/search?q=plate%20fin%20heat%20exchanger), air cooled heat exchanger (https://www.tianxiagongchang.com/search?q=air%20cooled%20heat%20exchanger), heat pipe heat exchanger (https://www.tianxiagongchang.com/search?q=heat%20pipe%20heat%20exchanger), cooling tower (https://www.tianxiagongchang.com/search?q=cooling%20tower), liquid cooling distribution unit (https://www.tianxiagongchang.com/search?q=liquid%20cooling%20distribution%20unit), data center liquid cooling (https://www.tianxiagongchang.com/search?q=data%20center%20liquid%20cooling), NEV thermal management (https://www.tianxiagongchang.com/search?q=NEV%20thermal%20management), heat pump heat exchanger (https://www.tianxiagongchang.com/search?q=heat%20pump%20heat%20exchanger), industrial heat pump (https://www.tianxiagongchang.com/search?q=industrial%20heat%20pump), energy storage liquid cooling (https://www.tianxiagongchang.com/search?q=energy%20storage%20liquid%20cooling).

Chapter 8. Localization Milestones: BPHE, Fully Welded PHE and Large Shell-and-Tube

Localization is not an abstract slogan; it can be broken into measurable milestones. We focus on three near-final ones.

The first is BPHE. Ten years ago BPHE was a four-foreign-house duopoly — SWEP, Alfa Laval, Danfoss, API (with Heatric exposure). Most Chinese players were small-form integrators. Over the past five years domestic vendors have advanced via two tracks: hiring European seasoned heads of process engineering, and outsourcing large vacuum-brazing-furnace builds to medium-size domestic furnace makers, dropping furnace cost from RMB 20 million to RMB 11 million. By 2025, domestic share of BPHE entire-machine reached about 42%, nearly doubling from 25% in 2020. Yet within this 42%, the bulk remains mid-to-low-end orders. In data-center liquid cooling, high-spec BPHEs (50 bar, 400 m3/h, nickel-braze, double-circuit) are still 70% foreign. The next decisive milestone is whether one or two domestic players can enter the core supplier shortlist for Tencent, Alibaba, ByteDance, Huawei or SenseTime's flagship supercomputing centers within 2026–2027.

The second is fully welded plate. Alfa Laval Compabloc and AlfaQ are the benchmarks. Three core challenges define this class: fully welded (not brazed) plate-to-plate joints requiring laser- or roll-welding precision; no rubber gaskets, so seams must seal entirely on their own across hundreds of meters; service in refineries up to 350°C and 50 bar. Domestic Shuangliang, Sifang and one or two private firms have produced Compabloc-class competitors in the past three years. In H2 2025, domestic fully welded plate won majority share for the first time in a major Chinese coal-to-chemicals revamp.

The third is large shell-and-tube. Domestic substitution there is largely done by 2018–2022, except for niche high-alloy applications in fine chemicals, pharma and offshore. The competition has shifted from "can we make it" to "are we willing to take long-cycle, low-margin orders." A 300 MW coal-to-chemicals package can hit RMB 100 million but takes 18 months to execute, during which steel-price volatility can erode five points of gross margin. The next decisive step is whether domestic champions can win replacement orders at foreign refineries — Saudi Aramco, Mideast independents, Southeast Asian coal-to-chemicals plants — at RMB tens of millions to RMB 100 million per contract.

Chapter 9. Capacity Expansion: Five Production Maps of Yuanda, Shuangliang, Sifang, Hongsheng and Yinlun

We pick five representative capacity maps.

First, Yuanda Group. Headquartered in Changsha, Yuanda focuses on absorption chillers, plate heat exchangers and centralized cooling/heating systems. Yuanda is unlisted; its Changsha plant is one of China's single largest PHE manufacturing sites, with single-line plate output of millions of plates per year.

Second, Shuangliang Eco-energy. Jiangyin-based, with energy-saving segment revenue of RMB 2.723 billion in 2025 and gross margin of 27.72%. The exchanger unit broadened its mix beyond air separation to CCUS, nuclear and petrochemicals; operating cash flow turned to a positive RMB 2.022 billion in 2025 from a near-zero level the prior year.

Third, Sifang Cryogenic. Yancheng-based, with 2025 revenue of RMB 1.69 billion. Cold-chain exchanger products cover evaporators, condensers, fan coolers, evaporative condensers, dry coolers and open/closed cooling towers.

Fourth, Hongsheng Co. Wuxi-based, aluminum plate-fin leader with H1 2025 net income of RMB 46 million, up 49% YoY. Long-term supplier to Atlas Copco, Siemens, Sany and Weichai. In 2024 it set up Wuxi Hehongzhi via a JV with Hexin Precision (51%–49%) to enter data-center cold-plate cooling.

Fifth, Yinlun Co. Tiantai-based; expanding NEV battery, motor and electronics cooling alongside European and North American factory build-outs in Poland and Mexico.

Stacking the five maps, three priorities surface: energy saving and new energy (Shuangliang, Sifang), data-center liquid cooling (Hongsheng, Yuanda), and NEV and storage (Yinlun, Sanhua, Nabaichuan). All three align with heat-pump policy, AI compute and EV electrification.

Chapter 10. Pricing Cycle: From Unit Price to Steel-Plate and Titanium-Plate Cost Transmission

Pricing trends across plate, shell-and-tube and air-cooler categories.

Plate exchangers ran a "stable then up" curve from 2024 to 2026. Gasketed mid-small (100–300 sqm) traded at RMB 1,200–1,800/sqm in 2024, drifting up to RMB 1,300–1,900/sqm in late 2025 on stainless-steel base price rises and a softer RMB. BPHE mid-small (50 m3/h nominal flow) sold for RMB 15,000–20,000 in 2024 but jumped to RMB 18,000–23,000 in 2025 on copper price spikes and tight capacity, easing slightly into 2026. Fully welded and Compabloc-class plates held stable at RMB 3–10 million per unit, more sensitive to engineering capability than to material prices.

Shell-and-tube prices showed downstream-driven divergence. Large units in petrochemicals and coal-to-chemicals stayed at RMB 5–30 million; large units in power and nuclear at RMB 20–100 million; mid-size shell-and-tube (100–500 sqm) trended up 5–8% on stainless prices. Air coolers held RMB 2–20 million depending on project schedules.

Material transmission. The largest cost block is stainless. 304 cold-rolled stainless held RMB 14,000–18,000/ton from 2024–2026; 316L held RMB 22,000–26,000/ton. Copper rose about 25% from H2 2024 to H1 2025, hitting BPHE margins. Aluminum was stable. Titanium TA1 1–3 mm traded around RMB 90/kg in early 2026; TC4 5–10 mm at RMB 150–155/kg.

Contracts: leading domestic players sign material-linkage clauses with major buyers; small players generally do not, and absorb material spikes.

FX: RMB depreciated about 3–4% versus USD in 2025, raising RMB-translated foreign quotes by the same amount and giving domestic vendors a mild pricing edge, while easing domestic exporters' RMB margins.

Chapter 11. Policy: Three Drivers from Dual Carbon, PUE and Hydrogen Subsidies

Driver one. The April 2025 NDRC heat-pump action plan ((Fa Gai Huan Zi (2025) No. 313) names new heat exchangers a priority. Industry revenue grew from RMB 8 billion (2014) to about RMB 33 billion now, 17%+ CAGR. Building penetration below 5%; industrial under 1% — huge runway.

Driver two. East-Data-West-Compute requires Eastern-hub data center PUE ≤ 1.25, Western-hub ≤ 1.2; new large/super-large facilities ≤ 1.3; Shanghai requires new AI compute centers PUE ≤ 1.25 and liquid-cooled racks ≥ 50% by 2025. Liquid-cooling penetration: about 13% in 2023, above 20% by 2025, around 33% by 2030. Within a CDU, the BPHE costs RMB 20,000–100,000 per unit; a typical super-compute center's CDU package exceeds RMB 10 million.

Driver three. China electrolyzer demand was about 3 GW in 2024 and roughly 6 GW in 2025 — nearly doubling. Per MW of alkaline electrolyzer: RMB 200,000–300,000 of heat-exchanger spend; per MW of PEM electrolyzer: RMB 300,000–500,000. Our estimate: RMB 12–18 billion of electrolyzer-coupled heat-exchanger orders in 2025, doubling by 2026–2027 on shipment doubling.

Layered together, these drivers form a five-to-seven-year policy window.

Chapter 12. Platform Research Judgement: Three-to-Five-Year Outlook

Drawing on the prior chapters and the about 4.8-million-active-factory database accumulated by Tianxia Gongchang, our verdicts on the next 3–5 years.

Verdict 1. China's market crosses RMB 150 billion by 2029, average growth around 8%, but with sharply diverging sub-segment growth — petrochemicals below 3%, HVAC and heat pumps 12–15%, data-center liquid cooling and NEV thermal above 25%.

Verdict 2. Domestic champions become the dominant player in plate, shell-and-tube and plate-fin. Foreign giants — Alfa Laval, Kelvion, SWEP, Tranter, Danfoss — collectively retreat from about 30% in 2025 to about 20% by 2029.

Verdict 3. Data-center liquid cooling becomes the single biggest incremental engine. Cumulative 2026–2029 orders exceed RMB 30 billion, with BPHE 70%, plate-fin/microchannel 20%, and other types 10%.

Verdict 4. NEV and storage thermal management localization reaches the world's highest level — domestic content above 90% by 2029 across PHE, microchannel and plate-fin.

Verdict 5. Hydrogen exchangers grow fast but stay small in absolute terms — RMB 10 billion cumulative for 2026–2029, gaining heft only after 2030.

Verdict 6. Consolidation is inevitable — at least twenty M&A deals over RMB 100 million each, lifting CR10 from about 28% to about 40% by 2029.

Verdict 7. Overseas market becomes the next growth engine for domestic champions; foreign-revenue share rises from about 10% to above 25% by 2029.

Verdict 8. Process innovation centers on three vectors — 3D-printed high-alloy small-batch units, phase-change-material thermal storage exchangers, and AI-aided design optimization.

Chapter 13. Risks: Property Slowdown, Foreign-Giant Pricing and Rare-Metal Volatility

Three principal risks.

Property slowdown. Residential new starts fell double digits in 2024–2025; commercial new supply down about 10%. Domestic heat-exchanger industry lost an estimated RMB 3–4 billion of orders.

Foreign-giant price war. Last severe round in 2017–2019 cut gasketed mid-small PHE prices about 20%, crushing domestic margins to single digits. We estimate a 30–40% probability of a new round in 2026–2027 as Chinese vendors continue to take share in data-center liquid cooling and NEV thermal management.

Rare-metal volatility. Sponge titanium and titanium plate are tight at the high end; copper rose about 25% from H2 2024 to H1 2025; nickel directly transmits into high-end stainless. A simultaneous 20% rise across titanium, copper and nickel would compress industry-wide gross margin by about two percentage points.

Secondary risks. CBAM imposes carbon-cost on EU exports starting 2026, raising domestic exporters' costs by 3–8%. Capacity overhang risk if data-center liquid-cooling orders disappoint in 2027–2029. Geopolitical risk on certain high-alloy steels and special titanium alloys. Certification lag on BPHE, microchannel and new-material exchangers.

Chapter 14. Data Sources and Further Reading

Our methodology: public filings first, industry interviews for cross-validation, and platform samples as the backstop.

Public filings used in this paper include Alfa Laval AB 2025 full-year results and 2025 sustainability report; SWEP press releases and Dover investor relations; Kelvion corporate site and APAC briefings; Danfoss H1 2025 update and product launches; Shuangliang Eco-energy Co., Ltd. 2025 annual and semiannual reports; Sifang Cryogenic Co., Ltd. 2025 annual and semiannual reports; Hongsheng Co. 2025 deep dive by Soochow Securities; Yinlun Co. coverage initiation; Sanhua Intelligent Controls 2025 research notes; Harbin Air Conditioning Co., Ltd. 2025 semiannual disclosure.

Policy documents include the April 2025 NDRC and six-ministry heat-pump action plan ((Fa Gai Huan Zi (2025) No. 313); East-Data-West-Compute strategy documents; Shanghai's smart-compute PUE rules; the ecological ministry's waste-heat recovery guidelines; the EU CBAM and F-gas regulations.

Industry research consulted includes Global Market Insights, Grand View Research, Zhiyan Consulting, Qianzhan Industry Institute, Baogaodating, Reuters, Nikkei Asia, LeadLeo Sullivan, Huatai Securities, and Soochow Securities.

Platform sample. Tianxia Gongchang's about 4.8-million-factory database, pulled by industry, region and process for heat-exchanger makers. Identification accuracy across about 12,000 factories materially exceeds general business-registry data thanks to multi-signal voting across business registry, ES full-text on websites and e-commerce pages, official-site crawls, image recognition on product photos, and manual verification.

Further reading from this institute: China Industrial Pumps 2026, China Industrial Valves 2026, China Data-Center Liquid Cooling 2026, China Vacuum Pumps and Compressors 2026 — together with this paper they form a complete Industrial Thermal Management & Fluid Machinery matrix.

Closing remark. Readers seeking the broader platform dataset can explore the platform for sector-, region- and process-specific factory shortlists, or contact our research team for tailored data sets and bespoke industry studies.