Abstract

The reducer is the "joint" of manufacturing. Motors spin fast but produce little torque; machines, however, need to work slowly and powerfully — converting high-speed, low-torque rotation into low-speed, high-torque output is precisely the job of the meshing gears inside a reducer. A six-axis industrial robot conceals six to eight reducers within its six joints, which together account for one-third of the robot body's cost; a humanoid robot may use as many as forty to fifty reducers. From the ball mills of mining operations to the nacelles of wind power turbines, from the electric drive axles of new energy vehicles to the wrists of robots, wherever power transmission occurs, reducers are almost invariably present.

China's reducer industry has two faces. On one side is the "small and scattered" general-purpose gear reducer segment: more than five thousand reducer manufacturers crowd into the red-ocean competition of gear, worm gear, and planetary general-purpose products, with the leading player holding less than two percent market share and price wars that have raged for years without end. On the other side is the precision reducer duopoly: the RV reducers and harmonic (drive) reducers that are the most expensive components inside industrial robot joints have long been firmly held by Japan's Nabtesco and Harmonic Drive Systems. The story of domestic substitution has grown from the cracks between these two faces. Using 2026 as its vantage point, this report systematically surveys China's reducer industry — covering market size, industry chain structure, competitive landscape, market segments, technological evolution, risks, and the outlook for the next five years.

Key findings are as follows:

- The two faces are the key to understanding the entire industry. Domestic production of general-purpose reducers already exceeds ninety percent, and competition is on cost and distribution; precision reducers are the high-value territory and the primary battlefield for domestic substitution, with the RV and harmonic lines determining the industry's ceiling.

- Domestic substitution in precision reducers is genuinely happening. The domestic market share of Chinese RV reducers rose from approximately 11% in 2014 to approximately 60.8% in 2024, surpassing foreign brands for the first time; the domestic share of harmonic reducers (by volume) has exceeded 80%. Behind this share reversal, service life and consistency remain unfinished work.

- The bottleneck is upstream, not in assembly. The real barriers lie in the ultra-clean smelting of specialty gear steel, harmonic flexible bearings, five-axis gear-grinding equipment, and batch-to-batch consistency — high-end gear-grinding machines cost more than ten million RMB per unit and some are subject to export restrictions to China, representing the last few barriers to domestic advancement into the high end.

- Humanoid robots represent the greatest upside potential and also the greatest uncertainty. Per-unit reducer consumption is four to six times that of industrial robots; a scale of one million units corresponds to a market of tens of billions of RMB — but 2025 shipments were still dominated by universities and research institutions, and factory-scale deployment may be two to three years away.

- Growth is diverging. General-purpose reducers track fixed-asset investment steadily, wind turbine gearboxes are driven by upscaling and offshore wind, while robot precision reducers and the humanoid track represent high-growth, high-volatility structural opportunities.

Key data at a glance:

- China's overall reducer market was approximately RMB 144.8 billion (narrow definition) in 2024 and approximately RMB 151.0 billion in 2025; precision reducers approximately RMB 9.1 billion (+10%), and general-purpose reducers approximately RMB 60–70 billion.

- Demand for reducers used in industrial robots in 2024 was approximately 1,366,000 units, of which approximately 796,000 were harmonic and approximately 570,500 were RV.

- The domestic market share of Chinese RV reducers was approximately 60.8% (2024, by volume), with Huandong Technology holding approximately 25% to rank first among domestic brands; Nabtesco's share of the RV market in China declined from approximately 54.8% in 2020 to approximately 40.17% in 2023.

- Precision reducers account for approximately 35% of industrial robot body cost; the service life of domestic harmonic reducers is approximately 10,000 hours, compared with approximately 20,000 hours for the Harmonic Drive Systems benchmark.

- China added 295,000 new industrial robot installations in 2024 (54% of global installations, the world's top position for 12 consecutive years), with a robot density of approximately 470 units per 10,000 workers.

Chapter 1 Definitions, Classification, and the Full Industry Chain Landscape

The reducer is an underappreciated protagonist in manufacturing. Motors spin fast but produce little torque; machines, however, need to work slowly and powerfully — converting high-speed, low-torque rotation into low-speed, high-torque output is precisely the task of the precisely meshing gears inside a reducer. From harbor hoists to every joint of a six-axis industrial robot, from the drivetrain of a megawatt-class wind turbine to the electric drive assembly of a new energy vehicle, reducers are everywhere — yet they rarely appear in the public eye. Understanding reducers is the starting point for understanding China's manufacturing power transmission technology landscape.

1.1 Definition and Basic Operating Principles of the Reducer

The standard mechanical engineering definition of a reducer (Speed Reducer / Gear Reducer) is: a mechanical transmission device installed between a prime mover and a working machine that uses the transmission ratio of gears (or other meshing elements) to convert the prime mover's high-speed, low-torque output into a low-speed, high-torque output. Its core function can be summarized in three phrases: speed reduction, torque multiplication, and speed matching.

The basic operating principle is built on the geometric relationship of gear meshing. For a pair of externally meshed spur gears, where the driving gear has Z₁ teeth and the driven gear has Z₂ teeth, the transmission ratio i = Z₂ / Z₁; output speed n₂ = n₁ / i, and output torque T₂ ≈ T₁ × i × η (where η is transmission efficiency). The greater the tooth ratio, the higher the reduction ratio and the greater the output torque. The transmission ratio of a single-stage spur gear drive is typically between 2 and 8; to achieve larger ratios, multi-stage series arrangements, planetary differential mechanisms, or special tooth-profile mechanisms (such as cycloidal-pin wheel drives or harmonic drives) may be used.

Three key performance indicators for reducers run throughout this report:

- Transmission ratio (reduction ratio): the ratio of input speed to output speed, determining the degree of speed reduction; precision reducers typically range from 30 to 160, and some harmonic reducers can reach 320.

- Transmission accuracy (backlash): measures the angular error during forward-to-reverse switching, expressed in arc-minutes (arc-min); precision reducers for robot joints require 1–3 arc-min or less, while general-purpose reducers are generally above 10 arc-min.

- Transmission efficiency (η): the ratio of output power to input power; worm gear reducers have the lowest efficiency (40%–90%), planetary gears and RV reducers have the highest (up to 96%), and harmonic reducers fall in the middle (approximately 80%–85%).

Beyond these three indicators, torque density (torque transmitted per unit of mass or volume), service life (MTTF, Mean Time To Failure), and noise level are also important criteria for reducer selection, especially in the precision reducer segment.

1.2 The Reducer Classification System

Reducers come in many types, and different classification dimensions give rise to various cross-cutting systems. This report uses two parallel classification frameworks: the first distinguishes by transmission mechanism and product form, and the second distinguishes by end-use application scenario. The two frameworks complement each other and together form the basic coordinate system for the analyses in subsequent chapters.

1.2.1 Classification by Transmission Mechanism

General-purpose industrial reducers are the oldest and highest-volume category, covering heavy industrial scenarios such as mining, ports, building materials, metallurgy, and textiles. They are divided into the following main types by tooth-profile mechanism:

- Gear reducers: encompassing two main branches — cylindrical gears (spur/helical/double-helical) and bevel gears. Cylindrical gear reducers are the most basic form; they offer high efficiency (95%–99%), low manufacturing cost, and a single-stage transmission ratio generally not exceeding 8, with multiple stages stackable to approximately 30. Bevel gear reducers are used where the input and output shafts are at a right angle to each other, as commonly found in mixers, mine hoists, and similar equipment.

- Worm gear reducers: the worm and worm wheel mesh in a crossed-axis configuration (typically 90°), with a single-stage transmission ratio of 10–80; compact structure and good self-locking properties make them suitable for applications requiring frequent reversal or anti-reversal (such as elevators and hoisting equipment). The trade-off is relatively low transmission efficiency (40%–90%) and high heat generation; the worm wheel ring typically requires tin bronze to reduce friction and wear.

- Planetary reducers (general-purpose): formed by a differential gear train comprising a sun gear, planet gears, and ring gear; multi-path power splitting results in a compact structure, wide transmission ratio range (3–100+), and self-balancing radial forces. General-purpose planetary reducers have lower accuracy grades than precision planetary units, but their load capacity is strong, making them widely used in construction machinery and port machinery.

- Cycloidal-pin gear reducers (Cyclo type): the planet wheel with a cycloidal tooth profile meshes with pin teeth on the housing; simultaneous multi-tooth contact provides strong load capacity and good impact resistance, with a single-stage transmission ratio of 6–87. Sumitomo's Cyclo® series is the international benchmark for this type; domestic equivalent products are mainly used in mid-to-low-end general industrial scenarios.

Precision reducers are the core focus of this report, designed specifically for scenarios with extremely high demands on transmission accuracy, such as robots, CNC machine tools, and semiconductor equipment. The three mainstream technology routes for precision reducers are as follows:

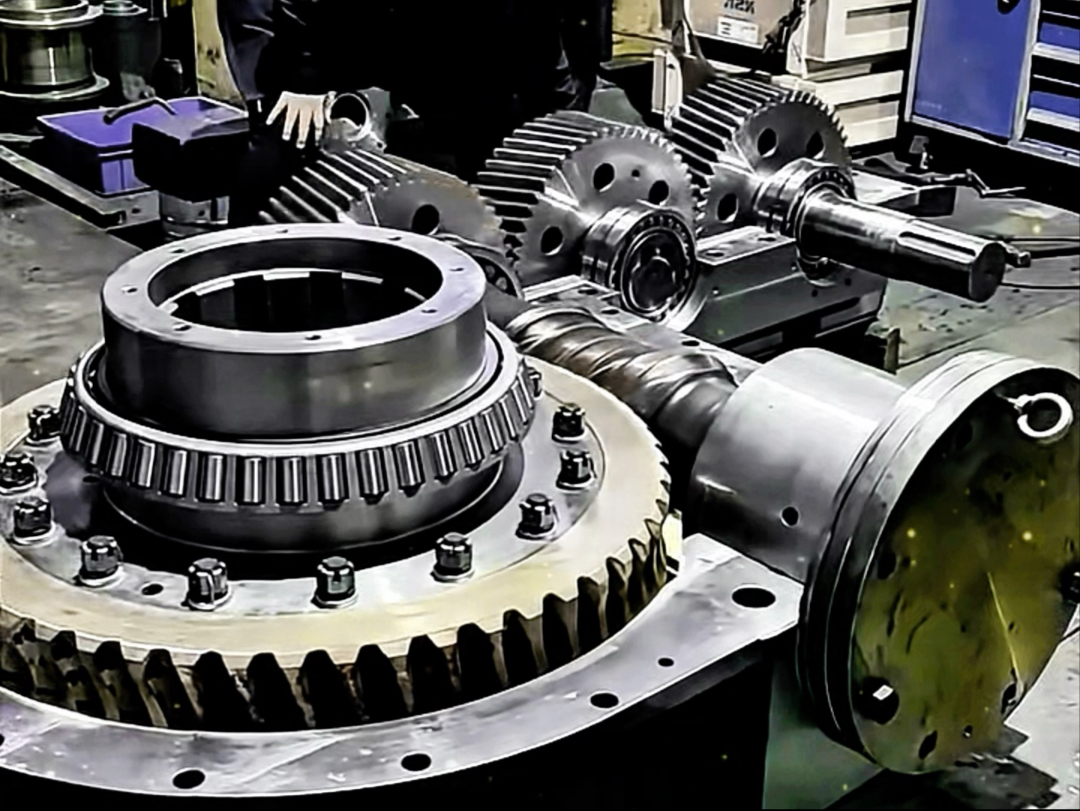

- RV reducer (Rotary Vector Reducer): formed by a two-stage series composite of a front-stage involute planetary gear reduction and a rear-stage cycloidal-pin gear reduction, achieving a combination of large transmission ratio and high rigidity. Key components include the cycloidal disc, pin housing, and crankshaft, with tooth profile accuracy requirements at ISO grades 3–4 and the roundness of the pin housing bore needing to be controlled within 1 μm. RV reducers offer high rigidity and good impact resistance and are the preferred choice for the waist (first axis), upper arm (second axis), and forearm base (third axis) of large six-axis industrial robots.

- Harmonic reducer (Harmonic Drive): uses the elastic deformation of a metal flexspline to achieve transmission, consisting of three major components: flexspline, circular spline, and wave generator. The wave generator drives the flexspline to produce a continuously undulating deformation at the point of meshing with the circular spline; the two have a tooth number difference of only 2, generating an extremely high transmission ratio (typically 50–320). Harmonic reducers are extremely compact and lightweight with near-zero backlash, at the cost of lower rigidity than RV reducers and an efficiency of approximately 80%–85%. They are widely used in robot wrist joints, all joints of collaborative robots, upper limbs of humanoid robots, and precision scenarios such as medical devices and semiconductor wafer handling.

- Precision planetary reducers: built on the general planetary architecture, through high-precision ground gears (IT4/IT5 grade), preloading to eliminate clearance, and tight tolerance fits, backlash is compressed to below 3–5 arc-min while maintaining the inherent high efficiency (92%–97%) and compact structure of the planetary mechanism. Humanoid robot manufacturer Fourier uses 32 precision planetary reducers to construct joint drives, demonstrating the competitiveness of precision planetary units when cost and rigidity balance is emphasized.

The core differences among the three precision reducer technology routes are summarized in the technology comparison table in the next section.

1.2.2 Classification by Application Scenario

From the perspective of end markets, reducers can be divided into the following main scenario categories, each with significant differences in product specifications, accuracy requirements, and market structure:

- Industrial reducers: covering heavy industrial scenarios such as cement and building materials, metallurgy and mining, and lifting and transportation, mainly general-purpose reducers; rated torque per unit ranges from hundreds to millions of Newton-meters, with an emphasis on reliability and service life, lower accuracy requirements, and intense price competition.

- Wind turbine gearboxes: installed inside wind turbine nacelles to convert the low-speed, high-torque rotor input (approximately 12–20 rpm) into high-speed generator input (approximately 1,200–1,800 rpm), with a transmission ratio of 60–100; this is a key component accounting for approximately 9.3% of complete turbine cost. As single-unit capacity continues to expand (onshore at the 6 MW level, offshore already at the 26 MW level), the requirements for torque density, large-scale manufacturing capability, and reliability of gearboxes continue to escalate.

- Automotive electric drive reducers: fixed-ratio speed reduction devices in the electric drive assemblies of new energy vehicles; the vast majority use single-stage or two-stage helical cylindrical planetary/parallel-shaft structures to reduce the speed of high-speed motors (maximum speeds up to 18,000–20,000 rpm) before driving the wheels. The core difference from conventional gearboxes is: no gear-shifting required, fixed transmission ratio, and extremely high requirements for NVH (noise, vibration, harshness).

- Robot precision reducers: used in industrial robots (six-axis/collaborative), humanoid robots, service robots, and other applications; dominated by RV and harmonic types with precision planetary as a supplement; the single largest demand market for precision reducers and the most fiercely contested battlefield for domestic substitution.

- Rail transit traction gearboxes: installed between the traction motors and wheels of high-speed rail and urban rail vehicles; mainly parallel-axis helical gear drives, requiring extremely high fatigue life (design life over 30 years) and quiet operation; domestic localization rate has exceeded 90%, with supply mainly integrated within the CRRC system.

1.3 RV, Harmonic, and Precision Planetary: A Technical Comparison of the Three Major Precision Reducers

The three major precision reducer technology routes have long coexisted and are not mutually substitutable; rather, each has its applicable domain under different load, rigidity, size, and efficiency requirements. The table below provides a cross-sectional comparison across six dimensions: mechanism, rigidity, efficiency, load, weight/size, and typical applications.

| Dimension | RV Reducer | Harmonic Reducer | Precision Planetary Reducer |

|---|---|---|---|

| Transmission mechanism | Two-stage composite: involute planetary + cycloidal-pin gear | Flexspline elastic deformation (strain wave gear) | Involute planetary gears (high-precision ground) |

| Transmission ratio range | Approx. 30–200 | Approx. 50–320 | Approx. 3–100 |

| Transmission efficiency | Approx. 90%–96% | Approx. 80%–85% | Approx. 92%–97% |

| Rigidity (torsional) | High, suitable for heavy-load impact | Lower, flexspline is an elastic element | Medium-high, multi-tooth-face contact |

| Backlash | Very low (≤1 arc-min in top-tier products) | Very low (theoretically near zero, depending on flexspline accuracy) | Low (typically 3–5 arc-min) |

| Weight and size | Heavier, larger volume | Light, extremely compact structure | Relatively compact, between the other two |

| Rated torque density | High | Medium | Medium-high |

| Service life (domestic) | Approx. 8,000 hours | Approx. 10,000 hours | Typically ≥ 10,000 hours |

| Service life (international benchmark) | ≥10,000 hours (Nabtesco) | ≥20,000 hours (Harmonic Drive Systems) | ≥10,000 hours |

| Manufacturing challenges | Cycloidal disc grinding accuracy, pin housing bore roundness | Flexspline thin-wall machining, flexible bearing | Planet carrier accuracy, preload clearance-elimination process |

| Typical applications | Industrial robot waist/upper arm/forearm base, heavy-duty cobots | Industrial robot wrist axis, collaborative/service/humanoid robot upper limbs, medical, semiconductor | Humanoid robot lower limbs, CNC machine tool FA axis, automation equipment |

| Global leading companies | Nabtesco | Harmonic Drive Systems | SEW-EURODRIVE, Neugart, multiple domestic manufacturers |

A few notes: First, "near-zero backlash" is an advantage of harmonic reducers at the principle level, but in practice the flexspline's elastic fatigue toward the end of service life will cause backlash to widen; Harmonic Drive Systems' process advantage lies precisely in its ability to maintain low backlash throughout the entire service life. Second, the "heavier" trade-off of RV reducers is a relative cost, but their high rigidity and impact resistance make them irreplaceable in large robot joints — even in humanoid robots, RV solutions are retained for lower-limb load-bearing requirements. Third, precision planetary reducers have a natural advantage in cost control — they do not rely on non-standard proprietary components such as flexsplines, have a higher degree of standardization, and are expected to benefit from cost reduction once humanoid robots enter mass production.

1.4 Full Industry Chain Landscape: From Specialty Steel to End Equipment

The reducer industry chain can be divided into three levels: upstream materials and components, midstream reducer manufacturing, and downstream end applications. The three levels do not have a simple linear relationship; rather, there is a cascading transmission of technical bottlenecks: whether bottlenecks in the upstream are broken directly determines whether midstream enterprises can challenge high-end categories; the rise in the domestic rate in the midstream, in turn, reshapes the cost structure and supply chain security of downstream terminal equipment.

1.4.1 Upstream: Materials, Components, and Equipment

The upstream of reducers can be organized into three levels:

Raw materials layer

Gears are the core transmission components of reducers, and the quality of gear steel fundamentally determines the performance ceiling of the reducer. The mainstream material for industrial reducer gears is low-alloy carburizing steel, with typical grade 20CrMnTi (conforming to GB/T 3077 standard); after carburizing and quenching, surface hardness can reach HRC 58–62 while the core retains toughness. For precision reducers, material requirements are significantly elevated: the wall thickness of a harmonic reducer's flexspline is less than 1 mm and it endures approximately two reverse bending deformations per revolution; the mainstream material is 40Cr or 40CrNiMo (Japanese grade SNCM439), requiring ultra-clean smelting with impurity content controlled below 0.015%. Domestic producers Baosteel and CITIC Special Steel have production capabilities, but the supply of dedicated high-end grades for robot precision reducers is still ramping up and there is a gap relative to specialized suppliers such as Japan's Daido Steel. In terms of castings, industrial reducer housings are mostly formed from gray cast iron or ductile iron, with ample supply and full competition — not a bottleneck. The worm wheel rings of worm gear reducers use copper alloys such as tin bronze to meet the requirements of good wear-resistant tribological pairs.

Core components layer

Precision bearings are the highest-volume general components inside reducers, serving the triple functions of support, friction reduction, and precision retention. The bearing requirements differ fundamentally across reducer types: in RV reducers, multiple high-precision bearings are installed between the crankshaft and cycloidal disc, operating in confined spaces with difficult lubrication; in harmonic reducers, the flexible bearing built into the wave generator is one of the three core components — its inner and outer rings must continuously elastically deform following an elliptical profile, making it a highly non-standard proprietary component whose fatigue strength and material purity requirements are no less demanding than those of the flexspline itself. China's bearing production in 2024 was approximately 29.6 billion sets; ordinary-precision products (P0/P6 grade) are domestically dominant, but more than 50% of P4/P2 ultra-precision bearings still rely on imports from SKF (Sweden), FAG (Germany), NSK, NTN (Japan), and other foreign brands. The localization of flexible bearings is one of the core weaknesses limiting domestic harmonic reducers from closing the service life gap with Japan's top-tier products.

Servo motors are the direct upstream pairing for reducers in robot joint applications. As the trend toward integrated joint modules (reducer + frameless motor + dual encoder + torque sensor + driver) accelerates, the supply chain coupling between reducer manufacturers and motor manufacturers is deepening continuously; domestic motor enterprises such as Inovance Technology and Hechuan Technology have formed deep ties with multiple reducer companies.

Key equipment layer

Gear grinding machines are the final finishing equipment for precision gear machining, determining the accuracy grade (ISO grades 3–5) and surface quality achievable by gears, and directly affecting the backlash and noise level of reducers. The high-end gear-grinding market has long been monopolized by three European companies: Reishauer (Switzerland), specializing in continuous generating grinding; Gleason (USA), with a product line covering the full range from hobbing to grinding; and Klingelnberg (Germany), renowned for bevel gear grinding — the cost of a single top-tier machine exceeds RMB 15 million. Some high-end Japanese equipment is subject to export restrictions to Chinese reducer companies, constituting a clear technology blockade. Qinchuan Machine Tool (000837) is the largest domestic gear-grinding equipment manufacturer, with an approximately 60% domestic market share; it has achieved breakthroughs in the mid-range gear-grinding machine segment, but equipment for high-end precision robot reducer grinding remains a shortcoming.

Heat treatment equipment is equally critical. The standard process route for reducer gears is "blanking → forging → annealing → rough and finish machining → carburizing & quenching → precision grinding"; carburizing & quenching is the core process step that establishes the "hard surface, tough core" performance gradient. Thermal distortion from quenching is one of the main challenges for dimensional stability in precision reducers; domestic engineering capabilities have established a foundation in this area, but batch-to-batch consistency still lags behind Japanese companies and is an important factor affecting the service life consistency of domestic reducers.

1.4.2 Midstream: Reducer Manufacturing

Midstream reducer manufacturers exhibit a pronounced bipolar divergence — a characteristic that will recur throughout subsequent chapters and is a key prerequisite for understanding the entire industry's competitive structure.

One pole consists of the small number of leading enterprises in precision reducers. In RV reducers, Nabtesco has long dominated globally, with domestic substitution led by Huandong Technology under Shuanghuan Driveline (002472); in harmonic reducers, Harmonic Drive Systems has held more than half the global share, with domestic Leaderdrive (Lvde Harmonic) (688017) as the most important domestic challenger. The core capabilities of these enterprises lie in long-term accumulation in high-precision tooth-profile machining, proprietary material formulations, and heat treatment processes — entry barriers are extremely high.

The other pole consists of the vast number of small and medium-sized manufacturers in the general-purpose reducer segment. There are approximately 5,766 reducer companies nationwide (2023 data), predominantly small and medium-sized private enterprises with highly homogeneous products, intense competition, and below-average profit margins. Although the geographic concentration of these enterprises is relatively notable, at the firm level the industry is extremely fragmented — the leading player, Guomao (603915), holds only approximately 1.7% market share, and price wars are the norm.

1.4.3 Downstream: Diversified End-Use Applications

The downstream of reducers covers almost all motion control scenarios in manufacturing. The core end markets focused on in this report include the following four categories:

- Industrial robots: China added 295,000 new industrial robot installations in 2024 (IFR data), with the installed base reaching 2,027,000 units, ranking first globally for 12 consecutive years. Each six-axis industrial robot uses approximately 3–4 RV reducers (for higher-load joints such as waist, shoulder, and elbow) and approximately 2–4 harmonic reducers (for precision joints such as wrist and hand), totaling approximately 6–8 precision reducers, with precision reducers accounting for approximately 35% of industrial robot body cost — the highest cost share of any single component category. Domestic brand installation share has exceeded foreign brands for the first time (57%), accelerating the release of demand for domestic reducers.

- General industry: heavy industrial scenarios such as cement and building materials, metallurgy and mining, and lifting and transportation are the largest downstream group for general-purpose reducers, accounting for more than 50% of general-purpose reducer demand in aggregate. Cyclical fluctuations in downstream demand (infrastructure investment, manufacturing capital expenditure) are directly transmitted to the pace of general-purpose reducer demand.

- Wind power: wind turbine gearboxes are among the highest per-unit-value reducer categories. China added approximately 86 GW of new wind power installations in 2024, with cumulative installations exceeding 520 GW; the industry continues to scale up unit size, with the proportion of offshore wind increasing year by year, placing higher demands on the technical specifications and supply chain assurance of gearboxes.

- New energy vehicles: China's new energy vehicle sales in 2024 were approximately 12.9 million units, with a penetration rate of approximately 44%, accounting for approximately two-thirds of global sales. Electric drive reducers have grown rapidly with electric vehicle sales; fixed-ratio single-stage planetary or parallel-axis helical gear structures have become the standard configuration for electric drive assemblies; the domestic production rate is extremely high, and competitive dynamics have entered a phase of cost control and NVH performance competition.

Beyond the four core markets above, rail transit traction gearboxes, construction machinery planetary reducers, elevator hoist reducers, and agricultural machinery transmissions are all reducer downstream sub-segments with varying volumes; each will be addressed in dedicated sections in subsequent chapters.

1.5 Chapter Summary: Two Faces and One Main Thread

The reducer classification system reveals an essential contradiction: while product forms are numerous and application scenarios broad, the technical barriers and industrial value are highly unequal. General-purpose reducers are large in volume with relatively low barriers, forming a highly fragmented landscape dominated by price competition; precision reducers are smaller in volume but with extremely high technical barriers, long dominated globally by a small number of Japanese and European companies, with domestic substitution a protracted and costly process.

The industry chain perspective reveals another main thread: from upstream specialty steels, ultra-precision bearings, and high-end gear-grinding equipment, to midstream cycloidal disc grinding and flexspline heat treatment, to the integrated verification in downstream robot bodies — the technical bottlenecks of the reducer industry are systemic, not solvable with a single-point breakthrough. The state of upstream materials and equipment localization determines whether midstream enterprises can truly achieve mass production consistency for high-end precision reducers; the leap in midstream domestic rates, in turn, reshapes the supply chain landscape and cost structure of downstream industries such as industrial robots, humanoid robots, and wind power equipment.

The definitions, classifications, and industry chain landscape set out above form the basic coordinate system for the analyses in all remaining chapters of this report. Subsequent chapters will progressively unfold from global dynamics, policy environment, China market size, upstream bottlenecks, corporate competition, industrial cluster ecology, and market segments to technology trends.

Chapter 2 The Global Reducer Landscape and the Overseas Duopoly

The global map of the reducer industry is underpinned by two fundamentally different competitive logics: in the general industrial reducer segment, several century-old German, Japanese, and Italian manufacturers have long held leading positions through gear-motor platforms and global distribution networks; in the precision reducer segment, two Japanese specialist companies — Nabtesco and Harmonic Drive Systems — have almost exclusively occupied the robot joint track for decades. Understanding the origins of these two structures is a prerequisite for observing the pathways by which China's reducer industry is breaking through.

2.1 Global Market Size: Fragmented Scope Definitions and True Scale

When discussing global reducer scale, one must first clarify a scope-definition dilemma that has long troubled market researchers.

Taking industrial gearboxes as an example, baseline-year figures from different research institutions differ by nearly a factor of three: Precedence Research, using a narrow "industrial gearbox" definition, puts the 2025 global market at approximately USD 11.5 billion; SNS Insider, IMARC Group, Market Research Future, and others, by including gear motors in their statistics, arrive at a broad-scope figure of approximately USD 32–32.7 billion. The two figures are not contradictory — they result from different statistical boundaries. In the broad-scope market, gear motors account for approximately 54% of total revenue, making them the true dominant segment. When reading market research reports, comparisons between figures are meaningless without first confirming the scope definition.

Global industrial gearbox annual production (2024) exceeded 24 million units, supplied by more than 16,000 companies in 72 countries. In terms of regional shipment structure, Germany, China, and the United States together account for approximately 37% of global shipments, making them the absolute manufacturing centers. By region: Europe produces approximately 5.7 million units per year, centered on Germany with contributions from Italy and Northern Europe; Asia-Pacific totals more than 7.9 million units, with China alone contributing approximately 4.3 million and Japan, South Korea, and India each holding shares; North America is primarily oriented toward domestic consumption, with relatively concentrated manufacturing.

The precision reducer market is far smaller than the general gearbox market, but its growth rate is significantly higher. Combining harmonic reducers and RV reducers, the 2024 global market was approximately USD 2.1 billion (approximately RMB 15.2 billion), and projections from multiple institutions suggest this could grow to approximately USD 3.15 billion around 2031, corresponding to a CAGR of approximately 6%. The annual growth rate of precision reducers for robot joints is noticeably faster than the 4%–5% overall pace for general industrial reducers. This growth differential is fundamentally rooted in the divergence of downstream application structures: the main downstream of general-purpose reducers is heavy industry and basic manufacturing, which has entered a mature phase dominated by stock replacement; the main downstream of precision reducers is industrial robots and automation, which is still in an incremental phase with penetration rates continuously rising.

Within the precision reducer segment, data divergence also exists. Under the industrial robot precision reducer scope, some institutions project a 2025 market of approximately USD 3.1 billion; counting only harmonic and RV reducers, the combined 2025 total is approximately USD 1.88 billion. Taken separately, the RV reducer market in 2024 was approximately USD 2.08 billion, projected to reach approximately USD 3.8 billion by 2033; the harmonic reducer market in 2024 was approximately USD 1.2 billion, projected to reach approximately USD 2.5 billion by 2034. The key source of divergence among institutions is whether precision planetary reducers and collaborative-robot-specific reducers are included in the scope. This report's precision reducer aggregate scope is primarily based on harmonic plus RV, without double-counting the precision planetary component.

The core variable driving expansion of precision reducer demand is installation growth in industrial robots and emerging humanoid robots. Global new industrial robot installations in 2024 have exceeded 500,000 units; China accounts for 54% of the global increment, and domestic brands have for the first time surpassed a 57% market share. Each six-axis industrial robot requires 6–8 precision reducers, with RV units handling the heavy-load joints such as waist and upper arm, and harmonic units covering light-load end effectors such as wrists. This installation base constitutes the most stable demand floor for precision reducers.

2.2 Nabtesco: The Global Dominant in RV Reducers

If the entire precision reducer industry is a pyramid, Nabtesco (Tokyo Stock Exchange: 6268) has long sat at the RV reducer apex.

Nabtesco's RV reducers (Rotate Vector, cycloidal-pin gear drives) account for more than 35% of global industrial robot RV consumption; their market share in the waist and upper-arm joints of medium-to-heavy robots once exceeded 90%. This dominance was not formed naturally: Nabtesco began deep partnerships with Japanese robot manufacturers such as FANUC and Yaskawa in the 1980s, transplanting the precision cycloidal-pin structure from aircraft landing gear systems into industrial robot joints, and built a technological moat through more than thirty years of process accumulation. The core barrier of RV reducers lies in the machining tolerance control for precision cycloidal discs and pin housings — meshing clearances are typically required to be at the micron level, and any process variation is directly reflected in transmission accuracy and service life. Nabtesco has long provided strict service life and accuracy guarantees (rated life exceeding 10,000 hours) to downstream robot manufacturers; this certification barrier is extremely difficult to quickly circumvent in industrial settings.

In terms of capacity layout, Nabtesco's production network spans Japan and China. The Tsu plant in Japan is the primary production base; in 2024, a new plant in Hamamatsu, Japan, commenced operations with a designed annual capacity of 1.2 million units specifically for emerging demand from humanoid robots and similar applications. The combined capacity of the Tsu plant in Japan and the wholly-owned plant in Changzhou (Wujin), China is approximately 1.06 million units per year. The company has publicly announced plans to double total RV reducer production capacity by 2026, reflecting its anticipation of continued expansion in the robotics market.

In terms of its China business, Nabtesco's Changzhou plant is the only local production base among foreign RV reducer companies in China, with advantages in proximity to downstream customers and reduced transportation costs. However, the pace of domestic substitution has exceeded external expectations: Nabtesco's share of the Chinese RV reducer market fell from 54.80% in 2020 to 40.17% in 2023, and by around 2024 had dropped into the 30%-plus range. Meanwhile, the domestic market share of Huandong Technology, a subsidiary of Shuanghuan Driveline, surged from approximately 5% to approximately 25%, becoming the leading domestic RV brand. Nabtesco's share decline is the most direct illustration of domestic substitution in China's precision reducer sector.

2.3 Harmonic Drive Systems: Founder and Guardian of Harmonic Drive Technology

The history of harmonic reducers is nearly inseparable from Harmonic Drive Systems (Tokyo Stock Exchange: 6324). The harmonic drive principle was invented by American engineer C.W. Musser in 1955; Harmonic Drive Systems commercialized it in the 1970s and has dominated the global market ever since.

Harmonic Drive Systems holds more than 50% of the global harmonic reducer market, and under some statistical scopes the figure is even higher. China is one of its most important single markets; estimated China sales as a share of total revenue were approximately 40% (around 2022). On a financial level, Harmonic Drive Systems' net sales for FY2025 (ending March 2025) were approximately JPY 55.65 billion, with net profit of approximately JPY 3.47 billion; though modest in scale, it is one of the most representative companies for profitability in the precision reducer sector.

Noteworthy is the potential impact of humanoid robots on Harmonic Drive Systems' business structure. In FY2024, Harmonic Drive Systems' reducer revenue from humanoid robot customers was less than JPY 100 million; the target for FY2025 has been revised upward to approximately JPY 3.4 billion — a more than 30-fold increase in less than two years, though this still represents approximately 6% of total revenue. This change indicates that the commercial validation of harmonic reducers in the humanoid robot track has moved from concept to orders.

On its China strategy, Harmonic Drive Systems chose a path completely different from Nabtesco: it established a sales subsidiary in Shanghai, with all products imported from Japanese plants — no local production in China. This arrangement maintains centralized control over core processes, but it also means that in the event of exchange rate fluctuations, tariff adjustments, or supply chain disruptions, Harmonic Drive Systems' China delivery capability faces higher policy and logistics risks. Domestic competitor Leaderdrive's pricing is approximately 40%–60% of Harmonic Drive Systems' comparable products, and Leaderdrive has already passed Tesla's supply chain qualification — the price scissors between the two are accelerating the migration of downstream customer choices.

2.4 General-Purpose Reducer Global Leaders: A Model of Platform-Based Competition

Global competition in the general industrial reducer segment presents a landscape fundamentally different from precision reducers: leading companies build their moats through gear-motor platforms and globally distributed service networks, not through single-point technology monopolies.

- SEW-EURODRIVE (Germany): FY2024 revenue approximately EUR 4.5 billion, global industrial gearbox market share approximately 23.5%, confirmed as the largest player by scale. The company has operations in 57 countries, with approximately 22,000 employees and 17 production plants. In 1931, SEW-EURODRIVE was the first to introduce integrated gear motors; since then, it has built high repeat-purchase barriers through a standardized platform and localized service system — no other single company's market share approaches this level in general industrial reducers.

- Flender (Germany, owned by Carlyle Group): originally Siemens' drive technology division, acquired by Siemens for approximately EUR 1.2 billion in 2005 and sold by Siemens to Carlyle Group for approximately EUR 2.025 billion in 2021, at which time revenue was approximately EUR 2.2 billion with approximately 8,600 employees. Flender's wind power gearbox brand Winergy is one of the major suppliers in the global wind power drivetrain.

- Bonfiglioli (Italy): FY2024 revenue approximately EUR 1.191 billion, with three business segments in industrial automation, off-road mobile equipment, and wind power; primarily family-owned, maintaining a stable position in the mid-size industrial gear motor track.

- Sumitomo (Japan): its Cyclo® brand is the primary manufacturer of cycloidal gear reducers globally; the global cycloidal gear market in 2024 was approximately USD 1.7 billion. Sumitomo Drive Technologies has long-established customer bases in textiles, logistics, food processing, and other industries.

- ZF (Germany): Bosch Rexroth's large gearbox and wind power gearbox divisions were integrated into ZF in 2015, along with the former Bosch Rexroth production base in Wuhan. ZF also consolidated the Winergy wind power gearbox brand (which subsequently appears alongside Flender in industry literature, with ownership relationships complicated by multiple rounds of M&A), focusing on large drivetrain systems and wind power.

The common characteristics of the above five companies are: broad and deep product lines, customers diversified across industries, downstream lock-in achieved through certification systems and distribution density — not through the technology dominance of a single product. This stands in sharp contrast to the "single-point monopoly" logic of the precision reducer segment.

In terms of growth drivers, the earnings elasticity of these general-purpose reducer leaders comes more from cyclical fluctuations in industrial automation investment than from structurally driven demand expansion led by technology upgrades. SEW-EURODRIVE's revenue grew from approximately EUR 3.5 billion in 2021 to approximately EUR 4.5 billion in 2024, a three-year CAGR of approximately 8.8%, benefiting in part from global manufacturing inventory restocking and warming automation investment; Bonfiglioli's growth trajectory over the same period was highly correlated with European industrial output indices. In other words, the "wide moat" of general-purpose reducer leaders is essentially a risk-diversification platform, not a technology dependency on a small number of suppliers as in precision reducers. China's domestic production rate in general-purpose reducers has already exceeded 95%; foreign general-purpose leaders' China business is mainly in high-end custom orders, certified scenarios, and installed-base maintenance — with quite limited room for scale expansion.

2.5 Global Robot Demand: The Primary Growth Engine for Reducers

Industrial robots are the most direct engine pulling precision reducer demand, and humanoid robots are becoming the next order-of-magnitude imaginative space — although the commercial pace of the latter remains highly uncertain.

The logic on the industrial robot side is already quite clear: a standard six-axis robot typically uses 3–4 RV reducers (for higher-load joints such as waist, shoulder, and elbow) plus 2–4 harmonic reducers (for precision joints such as wrist), totaling 6–8 units. RV and harmonic together account for 15%–20% and 10%–15% of robot body cost, respectively; combined they represent approximately 35%, the highest value share of any single component. According to IFR statistics, global industrial robot RV reducer demand in 2024 has exceeded 4.6 million units, with Nabtesco supplying more than 35% of that.

The logic of humanoid robot reducer demand differs fundamentally from industrial robots: more joints, higher requirements for lightweighting and miniaturization, and a greater proportion of harmonic reducers. According to third-party estimates, current mainstream humanoid robot solutions require approximately 25–50 reducers per unit; highly integrated solutions can reach 40–50 units, four to six times that of industrial robots. Taking Tesla's Optimus as an example: according to publicly available third-party analysis, a single unit contains approximately 14 harmonic reducers and 14 planetary roller screws; actuators as a whole account for approximately 56% of the total BOM, with harmonic reducers accounting for approximately 16%. An alternative solution, the Fourier humanoid robot, uses approximately 32 precision planetary reducers, following a different technology path.

At the volume-value estimation level, according to third-party estimates, if humanoid robot annual production reaches the one-million-unit scale, the corresponding reducer market could exceed RMB 23 billion; projections that the global humanoid robot reducer market could grow from approximately USD 520 million in 2025 to approximately USD 5 billion in 2035 have also been modeled by some institutions, corresponding to a CAGR of more than 13%, with more aggressive high-growth forecasts giving a range of 40%–46%. It must be made clear that 2025–2027 is still a validation period: global humanoid robot shipments in 2025 are approximately 14,400 units (according to third-party estimates), a significant proportion of which flows to universities and research institutions, with the inflection point for large-scale factory deployment perhaps not arriving until around 2028.

From the perspective of the overseas duopoly, humanoid robots present a structural challenge rather than a pure opportunity: the rapid growth in harmonic reducer demand both brought Harmonic Drive Systems approximately JPY 3.4 billion in new humanoid customer revenue in FY2025, and opened a window for competitive entry by Chinese domestic substitution enterprises — because the formation period of the humanoid robot supply chain coincides almost exactly with the time window during which domestic harmonic reducers are completing quality certification. The long-term dominance of the duopoly is now facing the most concentrated wave of challenges from China's industrial cluster.

2.6 Overseas Manufacturers' China Strategies: Two Strategies, Two Risk Profiles

The China strategies of Nabtesco and Harmonic Drive Systems represent the two archetypal choices available to foreign precision reducer companies facing the Chinese market, and each carries different risk exposures.

Nabtesco chose deep localization. The wholly-owned plant in Changzhou Wujin can respond quickly to local downstream customer rapid delivery needs and to some degree insulates against the exchange rate and transportation costs of Japanese plants. However, local production did not prevent market share erosion — as domestic RV reducers gradually closed the reliability gap, the responsiveness advantage of local capacity could no longer support premium pricing. According to industry data, Nabtesco's share of the Chinese RV market declined from 54.80% in 2020 to approximately 30% around 2024, with the pace of domestic substitution erosion clearly visible.

Harmonic Drive Systems chose centralized control. The Shanghai subsidiary handles only sales; all products are shipped from Japanese domestic plants. This arrangement maintains Harmonic Drive Systems' lockdown on core processes, but also means that its China delivery is entirely dependent on cross-border logistics chains. Should the trade environment tighten or exchange rates fluctuate significantly, cost advantages will shift further to domestic competitors. Harmonic Drive Systems' share of the Chinese harmonic market is approximately 40% (by sales value), still holding first place, but Leaderdrive's pricing strategy and Tesla supplier qualification are keeping this landscape under sustained pressure.

For foreign companies in the general-purpose reducer segment, China strategies are mainly joint ventures or wholly-owned production; SEW-EURODRIVE and Bonfiglioli both have manufacturing bases in China, primarily serving large local industrial customers. Domestic substitution in this sub-market has already exceeded 95%; foreign companies' presence in China is more about serving high-end customers and special-scenario applications than mainstream competition.

Looking across the global reducer landscape, a structural judgment has gradually come into focus: the main battlefield of general industrial reducers is efficiency, cost, and distribution — foreign leaders' advantages persist but incremental room is limited; the main battlefield of precision reducers is technology certification and mass production consistency — the moat of the overseas duopoly is being systematically eroded, and the accelerator of this process is precisely the local demand density generated by the scale of China's robotics industry, a structural condition that Nabtesco and Harmonic Drive Systems cannot replicate in the Japanese market.

Chapter 3 PEST Environmental Analysis: Four Driving Forces of Policy, Economy, Society, and Technology

Reducers are not random beneficiaries of a cyclical industry — they are structural beneficiaries of manufacturing upgrading. Understanding the medium-to-long-term logic of this industry requires simultaneous observation along four dimensions: targeted policy support, the switching of economic engines, the accumulation of social variables, and the convergence of technology pathways. The superposition of these four driving forces constitutes the fundamental backdrop against which precision reducer domestic substitution has accelerated and general-purpose reducers have moved toward consolidation over the past decade.

3.1 Policy (P): From "Key Research" to "Inclusion in National Plans"

3.1.1 Industrial Foundation Program and Mother Machines: The Foundational Status of Precision Reducers

China's industrial policy attention to reducers originated from a systematic identification of "bottleneck" issues. The Industrial Foundation Program listed high-precision gears and high-end reducers alongside high-end bearings and precision ball screws as core foundational components requiring breakthroughs in mechanical power transmission. This designation established the policy priority of precision reducers and laid the foundational logic for a series of specialized policies that followed.

In June 2023, five ministries including the Ministry of Industry and Information Technology (MIIT) jointly issued the "Implementation Opinions on Improving Manufacturing Reliability," explicitly requiring that efforts be focused on "improving the reliability, consistency, and stability of dedicated components such as ball screws, guideways, and spindles for mother machines and precision reducers for industrial robots, as well as general foundational components such as high-end bearings and precision gears." This was the first time at the policy level that precision reducers were included alongside mother machine reliability in a joint ministerial document. Notably, the document's focus was not on "making reducers" but on "making them dependably" — the policy shift from coverage rate to reliability reflects that domestic substitution has entered its second half.

In September of the same year, seven ministries including MIIT jointly issued the "Mechanical Industry Stable Growth Work Plan (2023–2024)," listing precision reducers for industrial robots in the scope of specialized components to be prioritized for improvement, driving the industry toward comprehensive domestic substitution across three dimensions: capacity, accuracy, and service life. The dense issuance of two documents in the same year sent a clear signal.

"Mother machines" were re-emphasized in the "15th Five-Year Plan" recommendations released in 2025, indicating that the policy priority of precision reducers as core transmission components for mother machines will continue through the next five-year period.

3.1.2 Dedicated Robot Industry Plans: RV and Harmonic Reducers Enter National Documents for the First Time

The policy turning point came in December 2021. Fifteen ministries including MIIT jointly issued the "14th Five-Year Plan for Robot Industry Development," for the first time including the core technology breakthroughs for RV reducers and harmonic reducers in a national-level industry plan, explicitly stating the goal to "develop advanced manufacturing technologies and processes for RV reducers and harmonic reducers, improving reducer accuracy retention (service life) and reliability." The plan proposed that manufacturing robot density double by 2025, with robot industry revenue growing at an average annual rate of more than 20%. National-level targets translate directly into hard demands for reducer output and quality.

In November 2023, MIIT issued the "Guidance on Innovative Development of Humanoid Robots," targeting the breakthrough of key "brain, cerebellum, and limb" technologies and achievement of batch production by 2025, and a comprehensive capability reaching world-leading levels by 2027. The document listed precision transmission (reducers) alongside perception and encoders as key limb technologies. Humanoid robots were positioned as "an important new engine of economic growth" — this designation means precision reducers have been elevated from robot components to core components of strategic emerging industries, with commensurately increased allocation of policy resources.

Beijing simultaneously released the "Robot Industry Innovation Development Action Plan (2023–2025)," listing high-precision reducers, high-performance servo motors, and drivers as key breakthrough targets, with supporting funding and opening of application scenarios. The follow-through of local policies creates a complete policy coverage chain for precision reducers from the national to the provincial and municipal levels.

3.1.3 First-Unit Equipment Catalogue and Specialized & Sophisticated SMEs: Clearing the Last Mile of "Getting It Used"

Domestic precision reducers face not only technical challenges but also market access challenges: robot system integrators, under established certification systems, tend to stick with Japanese products, and even when domestic newcomers' performance meets standards it is difficult to quickly enter the mainstream supply chain. The first-unit equipment policy was designed to address this pain point.

In September 2024, MIIT issued the "Guidance Catalogue for Promotion and Application of First-Unit (Set) Major Technical Equipment (2024 Edition)," including high-precision industrial robot reducers in the scope of first-unit equipment promotion. By using policy insurance to reduce the risk to buyers purchasing domestic new products, this policy helps reducer companies break through the commercial closed loop of "develop → get it used → iteratively improve." The updated "Industrial Structure Adjustment Guidance Catalogue" issued by the National Development and Reform Commission in the same year also explicitly lists "high-precision reducers for industrial robots" under the encouraged category.

The specialized & sophisticated "little giants" cultivation policy continues to tilt toward the precision transmission sub-segment. Leaderdrive (688017) and Huandong Technology under Shuanghuan Driveline (002472) have received national-level specialized & sophisticated SME recognition, enjoying policy dividends in tax incentives, credit support, and capital market green channels. This kind of recognition is not an honorary title — it is a substantive resource lever.

Taken together, from Industrial Foundation Program breakthroughs to dedicated industry plans, to first-unit equipment promotion and specialized & sophisticated SME cultivation, the policy system for precision reducers now covers the entire chain of R&D, production, certification, application, and financing. The depth of policy penetration into the industry is among the top tier in Chinese manufacturing sub-segments.

3.2 Economy (E): Four Demand Engines in Resonance

The effect of the economic environment on the reducer industry is not a single cyclical pull, but the superposition of multiple demand curves. Industrial robots, humanoid robots, new energy vehicle electric drives, and wind power installations — four growth curves are at different ramp-up stages, together constituting the structural upward support for the precision reducer market.

3.2.1 Industrial Robots: Volume Accumulation and Qualitative Migration

According to IFR's World Robotics 2025, China's new industrial robot installations in 2024 reached 295,000 units, a historical high, accounting for 54% of global total installations and ranking first globally for 12 consecutive years. China's industrial robot installed base exceeded 2,027,000 units. The figure with greater structural significance is: domestic brands' market share rose to 57% for the first time in 2024, surpassing foreign brands. This means the growth of domestic robot systems simultaneously drives demand for domestic reducer supplies.

Each six-axis industrial robot's standard configuration is approximately 3–4 RV reducers (for high-load joints such as waist, shoulder, and elbow) and 2–4 harmonic reducers (for precision joints such as wrist and hand), totaling 6–8 units. Precision reducers account for approximately 30%–35% of industrial robot body cost, the highest cost share of any single component. In 2024, harmonic reducer consumption in the industrial robot sector was approximately 796,000 units (up 18.86% year-on-year), RV reducer consumption was approximately 570,500 units (up 9.69% year-on-year), totaling approximately 1,366,000 units, up approximately 14.85% year-on-year according to Zhiyan Consulting statistics. The absolute scale and growth rate of demand volumes cement industrial robots' position as the largest downstream engine for precision reducers.

3.2.2 Humanoid Robots: The Highest-Upside and Highest-Risk Incremental Track

Humanoid robots' per-unit reducer consumption is four to six times that of industrial robots. Tesla's Optimus uses approximately 14 harmonic reducers for its rotary joints, plus planetary roller screws and other actuators, bringing total actuator count to over 40 per unit; domestic Fourier's humanoid robot uses 32 precision planetary reducers. Per-unit humanoid robot reducer consumption is in the range of 25–50 units (basic biped approximately 25–35 units, highly integrated versions including dexterous hands approximately 40–50 units); according to third-party estimates, the value of reducers per unit accounts for approximately 13% of the total BOM.

Global humanoid robot shipments in 2025 were approximately 14,400 units, of which Chinese companies accounted for approximately 84.7%; Zhiyuan Robotics shipped 5,168 units, Unitree Robotics shipped more than 5,500 units, and UBTECH delivered more than 500 units. Global shipments in 2026 may exceed 50,000 units. According to Qianzhan Industry Research Institute estimates, at one-million-unit scale the humanoid robot reducer market would exceed RMB 23 billion.

It must be emphasized that these figures are in a highly uncertain range. 2025–2027 is the commercial validation period for humanoid robots; shipments flow mainly to research institutions and leading customers, with large-scale factory deployment possibly not appearing until after 2028. The actual scale of humanoid robots' pull on precision reducer demand will remain in the category of elastic space rather than certain incremental demand until 2027. For this reason, this track offers directional opportunity, not a basis for linear projection.

3.2.3 New Energy Vehicle Three-in-One Electric Drive: Large in Volume but Limited Pull on Precision Reducers

China's new energy vehicle sales in 2024 were approximately 12.9 million units, with a penetration rate of approximately 44%, accounting for approximately two-thirds of global new energy vehicle sales. The reducers in the electric drive systems of pure electric vehicles (BEV) use a fixed-ratio design, primarily single-stage planetary gears or helical gears — far simpler in structure than robot precision reducers, but enormous in volume. Global electric vehicle reducer production in 2024 was approximately 18.26 million units, with an average selling price of approximately USD 117, giving a global market of approximately RMB 15.5 billion and a CAGR of approximately 19.3%.

For the reducer industry, the significance of the new energy vehicle electric drive track lies in volume support — the technical barrier of automotive electric drive reducers is between general-purpose reducers and precision reducers, with lower domestic substitution difficulty but also lower value per unit than robot precision reducers. Shuanghuan Driveline (002472) is the leading domestic automotive gear company, having smoothly transitioned from fuel vehicle transmission gears to new energy electric drive gears — a typical pathway for traditional general-purpose reducer companies extending into new emerging tracks.

3.2.4 Wind Power Installations: Scale-Up Driving Higher Per-Unit Value

Under the "dual carbon" targets, China's newly connected wind power installations in 2024 were approximately 86 GW, with cumulative installations exceeding 520 GW, representing nearly 50% of global cumulative wind power installations. Wind turbine gearboxes, as the core scenario for large reducers, had a Chinese market size of approximately RMB 17.9 billion in 2023 (according to Sina Finance scope) and approximately RMB 43.5 billion globally. They account for approximately 9.3% of complete turbine cost (as disclosed by Ming Yang Smart Energy).

Scale-up to larger megawatts is the core theme of the wind turbine gearbox track: a 3 MW turbine gearbox costs approximately RMB 2–3 million, while a 10 MW or above turbine exceeds RMB 8 million per unit. Dongfang Electric released a 26 MW offshore wind turbine in May 2025 (reported as a world record for single-unit capacity), continuously driving per-unit gearbox value higher. This trend is a structural positive for domestic leading suppliers such as NGC (China High Speed Transmission) and Chongqing Gearbox — the pace of value increase per unit is outpacing production volume growth, tightening industry concentration.

It should be noted that rising penetration of semi-direct drive and direct drive turbine types creates sustained structural pressure on geared solutions, but in the large-megawatt offshore segment above 10 MW, semi-direct drive solutions still dominate due to weight and economic advantages, and substitution of the main transmission gearbox has not yet formed a trending impact.

3.3 Society (S): The Dual Lock-In of Labor Costs and Robot Density

3.3.1 Rising Labor Costs: The Fundamental Driver of Machine-for-Human Substitution

The sustained rise in manufacturing wage levels is the fundamental economic driver behind Chinese factories deploying industrial robots. From 2005 to 2024, average manufacturing wages in China increased by more than five times; in parts of the eastern coastal regions, the average annual wage for manufacturing workers has exceeded RMB 80,000. At the same time, recruitment difficulties in labor-intensive industries became significantly more acute after the pandemic; electronics assembly, automotive stamping, welding, and other positions requiring high precision or repetition are the areas where robot penetration is advancing fastest.

For the reducer industry, rising labor costs create a predictable, sustained demand curve rather than a pulsed policy stimulus. Factory owners' investment decisions are driven by payback periods — when the ratio of industrial robot acquisition cost to labor cost falls to a sufficiently low level, substitution occurs. This threshold has now been crossed in an increasing number of industries.

3.3.2 Robot Density: China Has Taken the Global Top Spot and Is Still Accelerating

The most intuitive indicator of manufacturing roboticization is robot density (number of industrial robots per 10,000 manufacturing workers). According to IFR data, China's manufacturing robot density in 2023 reached 470 units per 10,000 workers, entering the top position globally for the first time. This figure was approximately 68 units in 2016 — a nearly sevenfold increase in seven years.

The rapid rise in density is driven by simultaneous progress at both ends: on the denominator side, the total manufacturing workforce gradually contracts due to aging demographics and industrial upgrading; on the numerator side, annual new industrial robot installations continue to set historical highs. With both variables moving in the same direction, the rise in robot density carries long-term certainty.

It should be added that while the 470 units per 10,000 workers figure is the highest globally, internal distribution is highly uneven: automotive and electronics manufacturing density far exceeds the average, while labor-intensive industries such as food, textiles, and wood still have ample penetration space. This means the domestic market for industrial robots is far from saturated, and the demand ceiling for precision reducers has not been reached.

3.3.3 Manufacturing Upgrading: Migration from Quantity to Quality

The core proposition of China's manufacturing industry during the 14th Five-Year Plan period is the shift from scale expansion to quality improvement. In the reducer sector, the concrete manifestation of this proposition is: general-purpose reducers migrating from price competition toward reliability and customized service competition; precision reducers migrating from "being able to source them" to "using them dependably."

The quality consciousness of downstream system integrators is also upgrading in parallel. System integrators in new energy vehicles, high-end machine tools, collaborative robots, and other fields have begun proactively incorporating reducer service life and accuracy consistency (CPK metrics) into supplier evaluation systems, rather than purely making selections on price. This change places higher systemic engineering demands on precision reducer suppliers while also constructing higher competitive barriers.

3.4 Technology (T): Four Convergent Pathways — Details Deferred to Chapter 9

The impact of technology trends on the reducer industry is essentially the reshaping of demand structure. This chapter marks only the directions; the mechanistic details are systematically developed in Chapter 9.

Integrated joint module design is the most closely watched direction at present. Highly integrating the reducer, frameless motor, dual encoder, torque sensor, and drive controller into a unified actuator is the mainstream technology path for humanoid robots and high-end collaborative robots. This trend requires reducer manufacturers to transform from "supplying components" to "supplying actuation systems," shifting the value center of gravity in the industry chain toward the integration layer. Kinco, Zhaowei Electromechanical, Moons' Industries, and others have already made commercial deployments in this direction.

The deepening of domestic substitution is reflected along two main lines in precision reducers. The domestic rate of RV reducers (by volume) has risen from approximately 11% in 2014 to approximately 60.8% in 2024, for the first time achieving comprehensive surpassing of foreign brands; the domestic rate of harmonic reducers (by volume) also exceeded 80% in 2024. However, a significant gap remains between the volume metric and the revenue metric — domestic manufacturers win share with pricing approximately 40%–60% below Japanese products, meaning foreign brands still account for a substantial portion by market value. In the next phase of technology catch-up, the core challenge shifts from "being able to make them" to "making them dependably and consistently."

The cost reduction pathway for harmonic reducers is quite predictable. Mainstream domestic brand pricing is already equivalent to 30%–60% of Harmonic Drive Systems' comparable products. As annual production capacity of one million units progressively forms, harmonic reducer unit prices are expected to decline a further 20%–30% over the next two to three years. Cost reduction will further lower the total BOM of industrial robots and humanoid robots, stimulating downstream demand and forming a positive cycle.

Lightweighting and miniaturization are the special technical requirements that the humanoid robot track places on precision reducers. Dexterous hands' demand for micro harmonic reducers at the outer diameter of approximately 10 mm and requirements for backdrivability exceed the standard specifications of industrial robot applications. This track is still in the technology development stage, but will catalyze a product spectrum fundamentally different from that of industrial robot precision reducers.

3.5 PEST Summary: The Cross-Effects of Four Variables

The analysis across four dimensions points to a single conclusion: the external environment surrounding precision reducers is, among Chinese mechanical sub-sectors over the past decade, one of the combinations with the strongest policy support, most certain demand growth, and most intensive technology iteration.

At the policy level, coverage extends from foundational breakthroughs to first-unit equipment promotion, clearing the full commercialization chain; at the economic level, the four major engines are at different ramp-up stages, avoiding dependence on a single track; at the social level, rising robot density and increasing labor costs provide a long-term stable demand foundation; at the technology level, joint module integration and deepening domestic substitution are reshaping the competitive landscape.

The superposition of these four variables is not simple addition — there are cross-amplification effects. Policy promotes first-unit equipment, helping domestic products overcome certification barriers; domestic substitution cost reduction, in turn, amplifies the pull of economic engines on robot installation volumes; rising robot density further reinforces the legitimacy of continued policy support. The four driving forces constitute a mutually reinforcing system — which is also the deep logic behind how precision reducer domestic substitution was able to accomplish the leap from 11% to 60% in just ten years.

Of course, a favorable environment does not mean the absence of risk. Service life gaps at the high end, certification lock-in, and humanoid robot mass production ramp-ups falling short of expectations are all known uncertainties. These risks will be discussed specifically in Chapter 10. The conclusion of this chapter is: the external environment in which the industry finds itself is, overall, in the most favorable window of the past ten years; the question is not whether demand exists, but whether the supply side's technical capability and consistency can keep pace.

Chapter 4 China Market Scale and Dynamics

4.1 Defining the Scope: Getting the Numbers Straight First

China's reducer industry market size varies from 144 billion yuan to nearly 300 billion yuan across different reports — a gap so wide that the root cause lies not in data quality but in fundamentally different statistical boundaries. Before examining specific figures, these two definitions must be separated and clarified.

Narrow scope: covers only industrial reducers (general-purpose industrial reducers, precision reducers, and wind turbine gearboxes), excluding passenger-car automatic transmissions and industrial integrated gear motors. According to research institutions including Zhiyan Consulting, the narrow-scope market size of China's reducer industry in 2024 was approximately 144.8 billion yuan, up 4.4% year-on-year; in 2025 it is projected at approximately 151 billion yuan, with a CAGR of 4%–5%. This scope is the baseline used throughout this report and is appropriate for cross-comparisons with listed-company revenues and robot component market-share metrics.

Broad scope: adds passenger-car and commercial-vehicle automatic transmission systems and integrated industrial gear motors on top of the narrow scope. The 2025 estimate is approximately 291 billion yuan, spanning virtually all power-transmission products from desktop miniature planetary reducers to megawatt-class mine gearboxes. The broad scope more closely approximates the complete concept of the "power transmission market" and is better suited for macro-level industry-size reference, but is not directly comparable to component-manufacturer market-share analysis.

The two scopes must not be conflated. The broad scope is approximately twice the narrow scope; the difference primarily reflects the automotive powertrain and industrial gear motor markets — both large yet highly fragmented. Unless otherwise stated, all subsequent chapters of this report use the narrow scope.

4.2 Internal Structure of the Overall Market

Within the 144.8-billion-yuan narrow-scope market, the landscape is far from uniform. Breaking down by product category reveals three tiers that differ sharply in scale, growth rate, and profit margin.

The first tier is general-purpose industrial reducers — the largest, most foundational segment. In 2024, China's general-purpose industrial reducer output was approximately 15.32 million units, demand approximately 12.24 million units, and market size approximately 60–70 billion yuan, accounting for 40%–50% of the narrow-scope total. This tier covers traditional heavy-industry applications: hoisting and transportation (approximately 25% of downstream), cement and building materials (approximately 15%), metallurgy and mining (approximately 10%), and electric power and wind power (approximately 9%). Average selling prices per unit are low; gross margins are generally 15%–30%; industry concentration is extremely low — segment leader Guomao holds approximately 1.7% market share, and the overall CR5 for general-purpose industrial reducers is below 15%. This is a textbook incumbent-competition market.

The second tier is precision reducers — the aggregate of harmonic drive reducers, RV reducers, and precision planetary reducers. In 2024 the market size was approximately 9.1 billion yuan, up more than 10% year-on-year. In absolute scale this is a fraction of the general-purpose segment, but the growth rate is more than double the industry average, and profit margins are substantially superior. The growth engine for precision reducers is the continued expansion of the industrial robot and collaborative robot (cobot) industry — a sharp contrast to the sluggishness of general-purpose reducers. This divergence is explored further in the domestic-substitution-rate section of this chapter.

The third tier is wind turbine gearboxes. In 2023, China's wind turbine gearbox market size was approximately 17.9 billion yuan by Sina Finance's scope (with a broader 27.57-billion-yuan figure that includes the full drivetrain), according to available data. Wind turbine gearboxes carry high per-unit value: a gearbox for a 3MW wind turbine costs approximately 2–3 million yuan, while the main gearbox for an offshore unit above 10MW exceeds 8 million yuan per unit. The overall market is driven by both installed-capacity additions and the trend toward larger turbines; in 2024, China's new wind power installations of approximately 86 GW continued to expand the segment.

Combining all three tiers and adding sub-markets such as EV electric-drive reducers (global production approximately 18.26 million units in 2024, with China contributing approximately two-thirds) yields the 144.8-billion-yuan narrow-scope base. Within this, the segment with the highest per-unit value, the fastest growth, and the greatest domestic-substitution potential is the precision reducer market — a segment of under 10 billion yuan.

4.3 Industrial Robot Demand: The Core Pull Factor for Precision Reducers

The growth logic of precision reducers is tightly bound to industrial robot installation volumes. In 2024, China's new industrial robot installations reached 295,000 units — an all-time high, representing 54% of the global total; the installed base surpassed 2.027 million units, which according to IFR data has been the world's largest for twelve consecutive years.

Each six-axis industrial robot is typically equipped with 3–4 RV reducers (for high-load joints such as the waist, upper arm, and forearm) and 2–4 harmonic drive reducers (for precision low-load joints such as the wrist and hand), totaling 6–8 units. Collaborative robots, with relatively uniform joint loads, typically use harmonic drive reducers in all joints — approximately 6–7 per unit. Applying these ratios, 2024 demand for precision reducers from industrial robots was approximately:

- Harmonic drive reducers: approximately 796,000 units, up 18.86% year-on-year

- RV reducers: approximately 570,500 units, up 9.69% year-on-year

- Combined industrial-robot precision reducer demand: approximately 1.366 million units, up 14.85% year-on-year

Both sub-categories achieved double-digit growth, but divergence has emerged — harmonic drives benefit from rising cobot penetration and are growing faster, while RV growth is more moderate, partly because the traditional downstream markets served by six-axis heavy-load robots (automotive welding and material handling) are expanding more slowly.